Investing: What Is The Wrong Question?

The Investment Perspective – September 2021

Peter Flannery Financial Adviser CFP

“Neither the investing method nor the fundamentals of the business are right or wrong because the mood of the market is favourable or unfavourable toward the “stock”. That is because when you really think about it, “stocks” (shares) are all about the financials and the trading price, the share price… the cash up value. What matters more is the economics of the business”

Peter Flannery

The wrong question…

As investors, there is lots to think about. There’s no lack of information and data. Because of the internet, we now have more than ever. Indeed, the problem can be too much … confusion.

Too much of it can also lead to distraction and going down the wrong path with investing. That inevitably leads to underperformance or, worst-case scenario, investment pain.

The wrong question?

The wrong question to ask is, “When are the markets going to correct or crash?”

The right question…

The right question to ask is, “How do we position our investments to make money out of any correction or so-called crash that comes along?”

At first look, logic suggests that if we knew markets were going to decline, why would we not scale back your investments to increase levels of cash, wait for the markets to decline, and then go back in at lower prices? After all, are we not supposed to be value investors who go after the bargains!?

In short, it is important that we move away from what to invest in or where to invest, to how to invest.

It’s not what or where; it is how.

That, of course, brings us to methodology.

The problem

The problem with trying to time markets is that it is unreliable. It can work at times but invariably is challenging to execute in a way that makes money. The reason of course, is because markets behave in a random way.

Indeed, we know from history that September and October is generally a time for market volatility.

Timing the markets is challenging because knowing when to exit or scale back is difficult to get right.

If we scale back or exit and the market continues to rise for long enough, we could simply have stayed put and we would be in a similar situation anyway without having the brokerage costs of getting out, not to mention going back in again (even though they’re not significant, they do add up).

Assuming we get out in a timely manner and there is an easily identifiable significant market correction, this may provide the cue to get back in. Then again, it may not.

This brings us to the next part of the transaction, which is knowing when to get back in and what to use as a reference point that will be reliable?

Without ‘going down the rabbit warren’ of that discussion, over time, I observe that we are generally just as well to focus on our investing methodology, which does not include trying to time the markets.

What is the methodology?

The methodology is e-Biz Investing at WISEplanning.

It’s called e-Biz Investing because it’s about investing in the business, not the stock.

It’s called eBiz investing because it is about investing in the underlying economics of the business along with the financials (not just the financials).

Although I’m simplifying things here for the sake of an easy discussion, we can argue that whilst Alphabet (Google) has been great, it is tagged for anti-trust action and therefore, how great will it be once the US government unleashes its court action on Alphabet?

We’ve only got to look at the recent crackdown by the Chinese government on major tech companies to see the impact on the trading price.

You may recall Alibaba (if that was part of your portfolio in the past) which saw its share price go from US$220 per share (my recommended sell price) up to US$300 per share, only to decline to below US$200 after the Chinese Government crackdown.

Governments and, more specifically, anti-trust action can materially impact businesses and the trading price as this type of event unfolds.

Then we can look at Microsoft (previously subject to anti-trust action) to get an idea as to how things work out over time once the dust settles and the anti-trust action is a thing of the past.

Microsoft easily survived and has since gone from strength to strength.

The key to that business was always and remains its underlying economics. For example, a strong competitive position, a strong ecosystem, very strong branding, and “sticky customers” that remain loyal to the brand.

What are we missing?

There is no real immunity from rising and falling trading prices. But then, we don’t want immunity, do we?

Of course we don’t because, lower trading prices make for better buying.

Also, we are investors rather than traders.

We’re not looking to second-guess a random market. Nor do we want to become overly distracted by current events.

I can also say with some degree of certainty, that we want to mostly ignore the mainstream narrative or the current theme across the popular media.

Remember that the agenda of the popular media is very different to yours and mine. Their agenda is to sell advertising.

Your and my objective is to keep our capital secure and make it grow as much as possible within certain parameters. See the difference!?

The right answers

The right questions help generate the right answers.

The right answer is to focus on our methodology, which for us at WISEplanning is the e-Biz Investing methodology.

To be clear, we’re not fund managers asset allocating, targeting sectors, diversifying to manage risk. We don’t ‘hug the index’.

Nor are we sharebrokers applying the momentum approach to investing, targeting popular sectors.

We’re not looking to chase fast-rising stocks in popular sectors. For example, the computer chip sector is totally across the popular media. It includes some businesses that I would like to invest in and recommend to you, but not at the current pricing levels, which are elevated (thanks in part to the popular media).

We are certainly not traders looking to buy, sell and transact in order to outguess the market.

This is why we are fortunate.

We are fortunate because we are not relying on prices to rise soon in the hope that we’ll make money.

We are relying on the quality of our businesses. They will grow and compound. The trading price will inevitably follow. Large businesses usually in a more stable way. Small caps can be much more fun ( a ‘bumpier’ ride).

Fortunately, we don’t have to target specific sectors or limit our options to well-known large stocks that everyone else follows.

We are fortunate because we have a unique methodology that takes us outside of the mainstream investing arena. This helps to protect investment capital and support ROI long-term.

It can all seem a bit confusing though, because the money that your portfolio and mine will make in the short term is based simply on market sentiment. We are neither investing idiots nor gurus because markets sharply decline or rise fast over a few months or a couple of years.

It takes time for the quality of our investments to shine through.

We are fortunate because, at the very least, we tolerate volatility at a level that few have an appetite for. This means that we stay the course and achieve results that others struggle to achieve, because they trade rather than invest. They lack that long attention span.

Better still, some of us are fortunate because we understand that volatility is an advantage and an opportunity rather than a problem or a risk.

All we need to do is follow the methodology and, to some degree, ensure that the analyst, the financial adviser, and the investor keep out of the way enough, to allow good business to grow and compound. I’m not promoting the idea of buy, hold, and hope. That is never a strategy.

I know from experience that quality investments are resilient and will continue to grow long term.

Just look at your own portfolio, and you’ll also see over time how different businesses grow compared to some others within the portfolio.

Better still, patience and some discipline don’t cost much but can go a long way for us as investors.

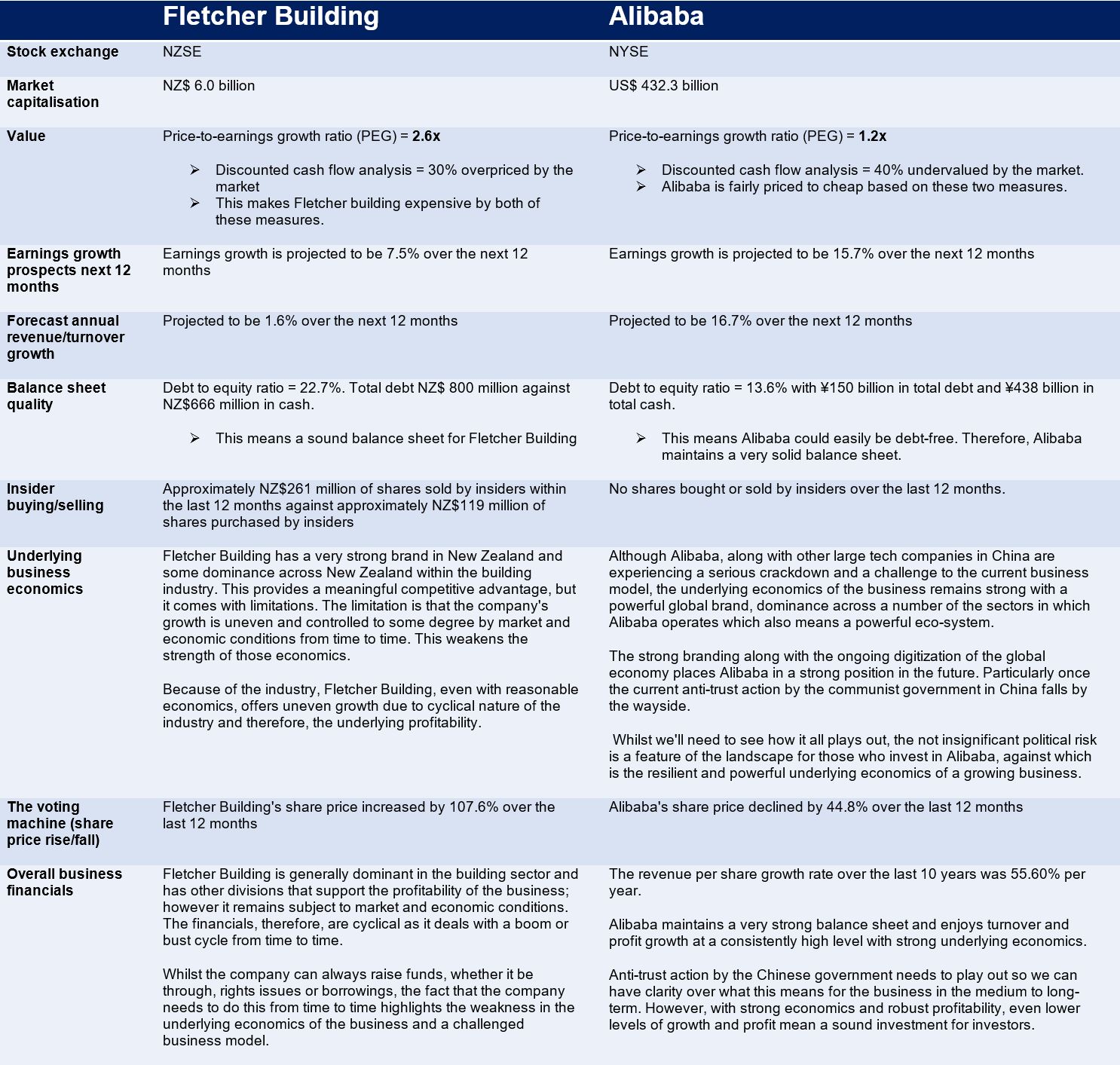

Fletcher Building vs. Alibaba

Just for fun, let’s look at two totally different businesses. Neither are recommendations. This is just for your information and learning.

The above comparison between Fletcher Building and Alibaba may offer limited clarity around the importance of the underlying economics of each business as it overviews the financials and, to a limited degree the underlying economics of each business for comparison purposes.

Looking at the above information, if you had to pick one, which one would you choose on the basis of the information above?

Fletcher Building is well-known to everybody in New Zealand, although of course, globally, it does not have a presence.

Alibaba, on the other hand might be less well-known to Kiwis but is well-known globally, particularly of course in China.

What we know is that the cyclical nature of Fletcher Building will likely continue in the future, given how the company’s fortunes are closely tied to prevailing conditions.

As for Alibaba, whilst the anti-trust action by the Communist Party is not insignificant, it would appear that the purpose of this action is for a more level playing field. This may mean that Alibaba cannot generate super-profits and stellar growth like it has in the past, but may well remain a worthy investment for those who are comfortable tolerating the political risk attached to a powerful business from China, continuing to benefit from the ongoing digitisation of the global economy.

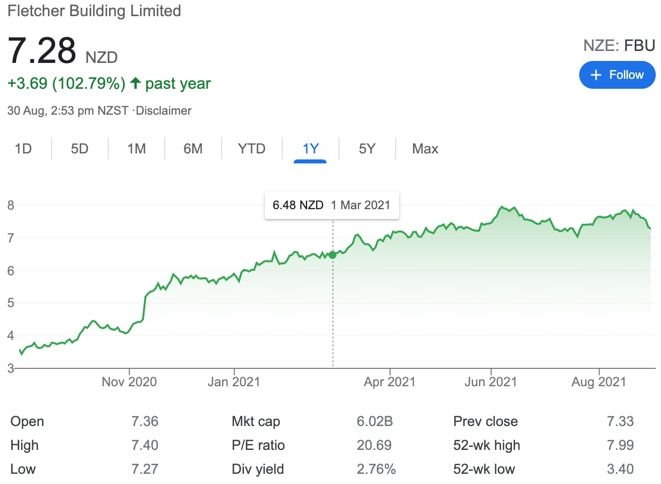

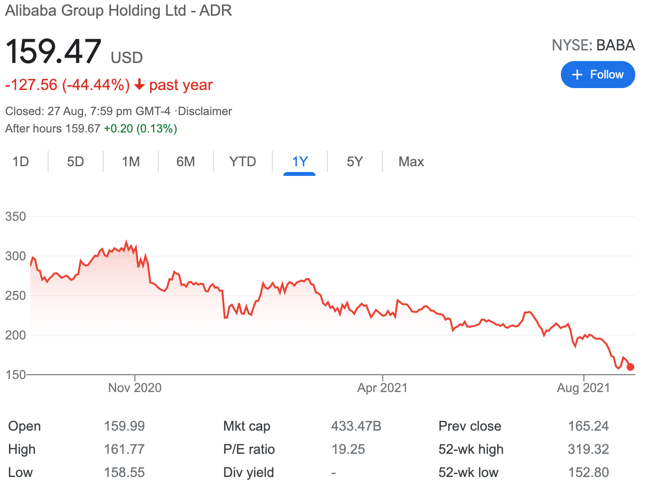

One question before us now is, taking a simplistic view, putting other metrics to one side for a moment, would you jump into Fletcher Building because the trading price has increased by over 100% over the last 12 months, or would you buy Alibaba because its trading price has declined by circa 45% over the last 12 months?

The graph to the left (the green line) tracks the Flecher Building share price over the last 12 months. The chart to the right (the red line) tracks the Alibaba Group share price over the last 12 months.

I imagine you’re thinking that you need more information than just looking at the trading price!

The temptation for many, of course, is to “jump on the bandwagon”, to follow the herd and hope that the trading price continues to climb.

Fortunately, whilst sometimes that approach can work, you and I know differently – don’t we…

“Quality is not an act; it is a habit.”

Aristotle