Making Money Out Of The Real Price

The Investment Perspective – March 2022

Peter Flannery Financial Adviser CFP

“Neither the investing method nor the fundamentals of the business are right or wrong because the mood of the market is favourable or unfavourable toward the “stock”. That is because when you really think about it, “stocks” (shares) are all about the financials and the trading price, the share price… the cash up value. What matters more is the economics of the business”

Peter Flannery

The Power of Price

Key Points:

- Profit and profitability, what is the difference?

- Do you invest in the business or the stock?

- If you answered the business, where does the trading price fit then?

- What is the real price that matters anyway?

- How does the real price make your portfolio perform better?

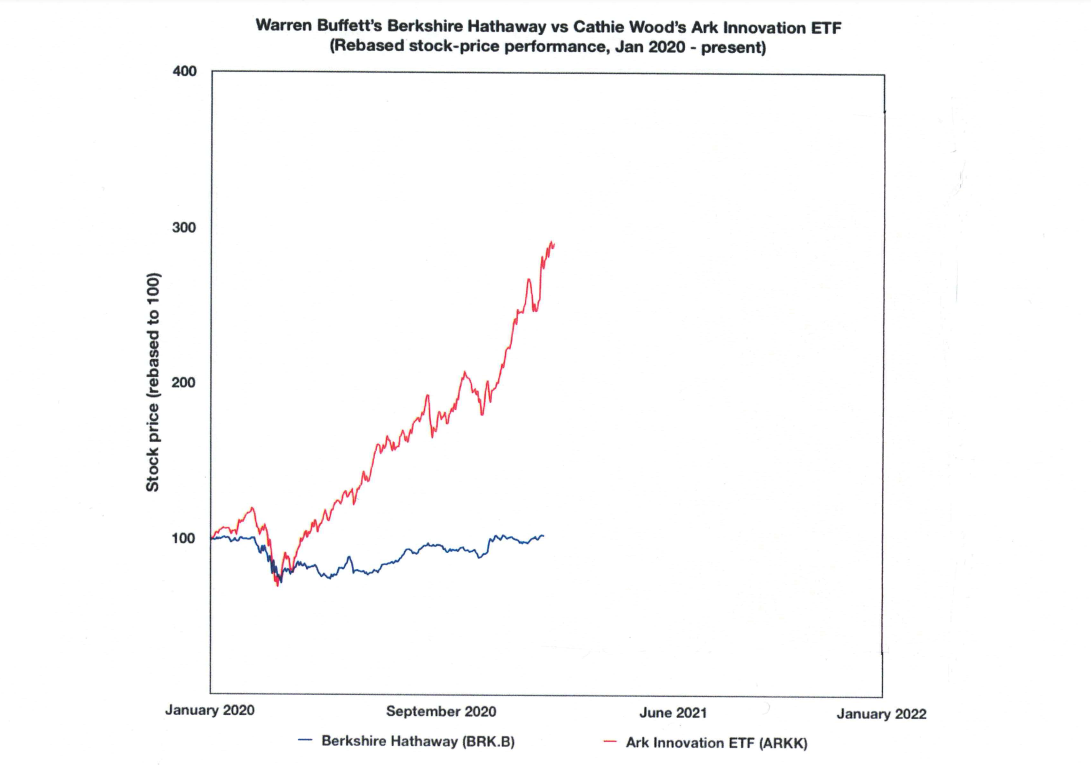

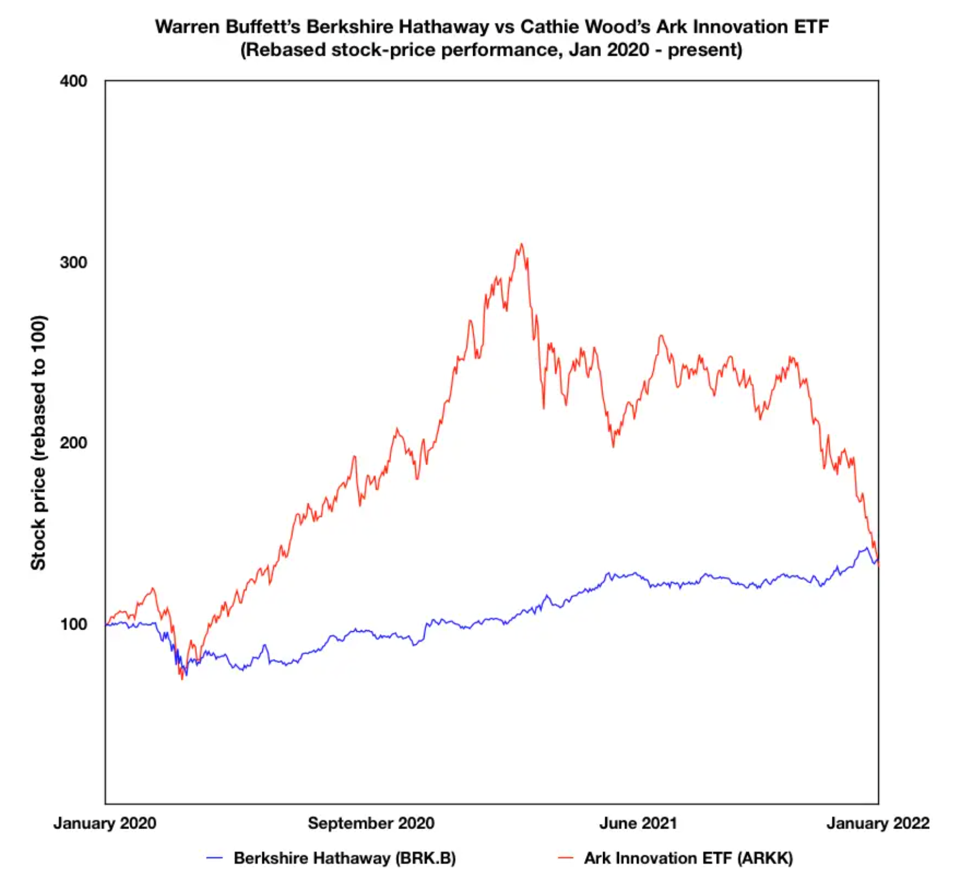

The above graph compares the trading price of The Cathie Wood Ark Fund and Berkshire Hathaway.

The First Price

The first price is the trading price of each ‘stock’.

If we look at the attention that the trading price has bestowed upon it, suffice to say, it is significant, massive to the point where many investors struggle to separate the fact that the trading price often has little to do with operational profits, the underlying economics of the business, or the intrinsic value.

The trading price indeed is determined by market sentiment. Yes, I know you’ve heard it all before.

Honestly

The question though is, honestly … how long ago was it that you unwittingly caught yourself over rating or under rating the quality of a business using the trading price of the stock as your benchmark?

Good examples at the moment would be the likes of Zoom Video, PayPal and Dot Digital which have all seen their trading price plummet. Certainly, the trading prices were expensive and now would not be regarded as ‘bargains’ but are starting to represent value. Recent insider buying at PayPal may be confirming this point.

The challenge investors face is that we never know when a company that is growing quite fast, showing top line growth and bottom line growth, suddenly comes up short of market expectations.

PayPal

For example, that’s what PayPal did with regards to its earnings for the most recent quarter. Further, the number of new users has slowed down and they have signalled that this number may also continue to slow in the future.

Although there’s more to it than this, it is interesting to note that the market often looks to the number of new users as a metric to gauge some measure of value (not one that I would use), or at least a reference point that indicates future growth. Like many things that are not based on the fundamentals, it works until it doesn’t.

We know that PayPal management have opted to trim back the number of users deliberately so that they maintain a core base of quality users with the view to slowing down user growth for the same reason. They only want quality customers.

That makes sense to me. I know from experience that quality customers are not only profitable but also easy to work with, but further, they appreciate what we do and recommend others.

Multiply dissatisfied customers by a significant number for a large corporate with global scale, and we have a serious headwind against profitability right there. Ambivalent or unhappy customers are not always profitable.

Anyway, some investors just cannot resist a fast, upwardly mobile trading price. Particularly one that tracks up for multi-year periods (e.g. Amazon, PayPal, Tesla).

Ok, so the first price we are discussing today is the trading price of shares, the trading price of each listed business in your investment portfolio.

As Warren Buffett mentioned many years ago, “The trading price tells you exactly nothing about the business“.

The Second Price

The next price we are talking about is the ability of the business to price strongly in the absence of meaningful competition.

Alphabet is the most obvious example, but there are a number of others. PayPal is another good example (you may not believe that if you only looked at the trading price over the last 12 months), although we could argue that this is the reason why competition is now emerging for PayPal.

They’ve had global payments all to themselves for a long time, and so others want in on the action.

Competition for PayPal then is something to watch, although it’s hardly an immediate threat given the strength of the underlying economics of this business.

Let’s Keep Unpacking It.

A business (as distinct from the stock) is a different thing.

The stock is all about the financials, which by the way, are plucked out of the most recent quarterly report, six-monthly report, or annual report.

This is useful data but … the point here is that this is all historical information.

Just because a company’s profit declines over the last quarter does not mean that the business is no longer as good or with the increase in profit, the business is not necessarily somehow a lot better. It could mean those things, but annual data is short term and unreliable as an indicator of long-term growth for any business.

As for quarterly data …

In the case of Alphabet (Google), they control over 90% of search engine activity around the globe. Yes, we’ve seen a number of articles across the internet stating that this technology is now old and ho-hum as if to say, it won’t be long before Alphabet starts to decline and become a dinosaur.

Well, anything is possible and there is a long list of once powerful companies that are no longer so dominant.

However, at this point, it would be a significant stretch for any business to ‘pull the rug’ from under Alphabet’s position because of their strong financials and their powerful business economics (competitive advantage, extensive ecosystem, and powerful brand strength).

Back To PayPal, Just For The Fun Of It

There are a number of things to like about PayPal, even though some investors may not like the notable decline in the trading price.

For example, PayPal carries a modest level of debt which in a low-interest-rate environment enables them to leverage their resources in a well-managed and calculated way. Not too much debt but enough so that it provides that leverage.

Another characteristic of PayPal’s business is the fact that they retain 100% of earnings and reinvest it back in the business.

Whilst over one year that may not mean much, however over 5 or 10 years, that is powerful and significant. Look at where PayPal is now. They transacted over $1 trillion worth of payments over 2021.

Return On Capital Employed (ROCE)

Simply, this just means, the return that they can achieve off capital employed.

Obviously, the larger the return for every dollar of capital employed, the better the business.

Profit vs Profitability

I’ll stop soon(!). However, it is important to distinguish between profit and profitability. Just as the trading price tells us nothing about the business, profit equally tells us very little.

That’s because profit is a short-term number, always historical and can be an unreliable source of information about the future prospects of the business.

Profitability on the other hand, looks at the return on the capital employed or return on assets. Return on capital employed looks across the income statement and the balance sheet, whereas profit only looks at the income statement.

Pricing Strength

So, pricing strength is about how much a business can charge its customers. It comes out of strong underlying business economics. Not the rise or fall in the trading price, make sense?

The Trading Price

The trading price is something that many investors unwittingly consider an indicator of business performance.

It indicates market sentiment, which in turn may be looking at certain financial metrics that it likes or does not like.

The challenge, or the opportunity for you and I as investors is to understand those metrics and to know whether they are reliable or not.

Finishing Where We Started

As the above comparison shows, short-term price movement is a poor indicator of long-term business performance.

Shooting for the moon and going for king-hits can work but is difficult. Very difficult to replicate at will, especially long term.

I smiled when I read reporters quipping about The Tortoise and The Hare as if to say that Cathie Wood’s ARK exchange-traded fund is the Hare and Warren Buffett’s Berkshire Hathaway is the tortoise (yet they both wound up in the same place). I wonder about that comparison if you see what I mean?

By the way, I hold Cathie Wood’s ARK Fund in high regard. It is made up of a number of disruptors, and whilst it is not something that I would invest in, I also hold Cathie Wood in high regard.

I prefer to invest directly in carefully selected businesses rather than across lots of stocks. That way I contain costs and have more control over the investment outcome.

What do you think?

“There is more to life than increasing its speed”.

Mahatma Gandhi