Gold, Cryptocurrency, Business

The Investment Perspective – July 2021

Peter Flannery Financial Adviser CFP

“Neither the investing method nor the fundamentals of the business are right or wrong because the mood of the market is favourable or unfavourable toward the “stock”. That is because when you really think about it, “stocks” (shares) are all about the financials and the trading price, the share price… the cash up value. What matters more is the economics of the business”

Peter Flannery

Gold, Cryptocurrencies, Business

Long story short – I have received inquiries recently about investing in gold and some rather coy queries about the possibility of investing in cryptocurrencies.

Whilst I’m oversimplifying things, gold has resurfaced again because it is considered to be a store of long-term wealth (I’m not sure that I’d be comfortable owning gold as a long store of wealth though) and that it’s supposedly a hedge against inflation.

Cryptocurrencies of course have captured the imagination of those who like a ‘king hit’ or ‘home run’ approach to investing and others who are somewhat anti-establishment and are keen for an investment that is as far away as possible from the controlling tentacles of government.

Cryptocurrencies supported by blockchain technology looks like the ideal solution.

Although it is difficult to know what cryptocurrencies will exist in 10 years from now, when we look closely at the mechanism behind bitcoin, for example, there is definitely some sustainability to this system for the long-term. The same cannot be said for all other cryptocurrencies.

The point here is that cryptocurrencies differ. They are not all the same.

Like other types of investments, there are those in the crypto world that perhaps represent a greater chance of survival long term (e.g., bitcoin, Ethereum) and a good many others that are of dubious ‘quality’ (e.g., dogecoin). Indeed, as you may know, dogecoin was created as a joke but quickly gained popularity seeing its trading price soar.

Although academic arguments can be made for investing in these assets, this I think brings home the bottom line about gold and cryptocurrencies:

- Their trading price is determined significantly by demand / popularity. High demand / popularity, prices rise. Low demand / popularity, prices decline.

- Neither gold nor cryptocurrencies are quality capital assets. There remain questions around how sustainable any income stream off cryptocurrencies is and gold does not have an income stream.

- Therefore establishing an intrinsic value is problematic. Therefore how do we know how much to pay when we invest? Are we happy just relying on the trading price driven by popularity?

This does not mean that investors cannot make money investing in gold and crypto currency. Indeed, we’ve seen, particularly with cryptocurrencies of late, the meteoric rise of the trading prices of many cryptocurrencies.

Of course, we’ve also seen trading prices decline but even taking that into account, those early investors have probably done quite well.

This brings us to the next point which I believe is about the certainty and reliability of the investment in the future.

I may be old-fashioned however, measured risk and some degree of reliability around investment outcomes is something that I believe still has merit.

This does not mean that perhaps cryptocurrencies or even gold might not have some use for some investors (not that I am recommending investing in either).

Although this may be obvious, it is probably wise to avoid the risk of confusing investing in the likes of gold as being the same thing as investing in cryptocurrencies as being the same thing as investing in direct shares, etc.

Different investments are different and behave differently.

What do you believe?

Here is the question. “Is gold a hedge against inflation?”

Which box did you tick?

Source: Ashley Owen, Chief Investment Officer, Standford Brown and the Lunar Group.

The above chart shows the returns achieved from a variety of asset classes during different inflation periods. Look for PM (precious metals) coloured yellow.

If you look at the table above you will see that precious metals, which includes gold, silver and the like, do not fare especially well when compared to other asset classes. In short, there is little evidence to support the idea that gold is a credible hedge against inflation in the long run.

Sure, any asset class during specific phases of certain market cycles can be a world-beater. The further out you stretch the data though, the more the reality of real performance becomes apparent.

Short-term data as we know is an unreliable source of information. Arguably too, data points that are too lengthy start to become irrelevant in some situations.

The point is …

Although some lengthy explanations along with a number of charts, graphs, and complex formulas can offer a degree of evidence to prove a point, my observation is that most points of view can be rationalised. Those rationalisations are usually valid.

As always though, the real question is whether or not they are right?

Certainty and reliability r us.

We can always argue that there is merit in diversification. It’s valid. For those less advanced investors, we can even argue that it’s right.

More advanced investors however have a different understanding and likely a different mindset.

They are able to invest in a different way than others.

Capital assets provide that important relationship between the income stream and the amount of capital involved to generate that income stream.

The ideal investment needs minimal capital to generate lots of cash flow. Although income from crypto currency might be possible (e.g. mining), gold does not generate income.

So, we have a reliable way of assessing investments and whilst, I don’t know that we have 100% certainty about anything, we have a greater degree of reliability when we apply our investing efforts to capital assets.

I should add that, speculating on Tesla, A2 Milk, Brierley Investments, Fletcher Building or (you add your own company name here) does not mean that you have automatic certainty and reliability.

We may need more than a good sounding idea, a popular company that everyone is chasing and some potentially good-looking financials to have a good investment.

Of course, we can always just ‘wing it’ and in a rising market, it is surprisingly common for investors to do well – funny that!

Investments that stand the test of time are key to success as distinct from good ideas that are shooting stars for a while, but were only ever popular because the market became intoxicated with the idea of a company – and the soaring share price.

On another note, rotation and big tech …

Just to change the subject, I often see (as you possibly do if you’re looking at the markets regularly) ongoing comments around rotation out of big tech into value-based investments such as healthcare, banking, and energy. This play-the-market approach is valid however we’ll see in the future how it all ‘washes out’ down the track.

There’s also increasing noise about the day of reckoning for big tech, whether it be the fact that interest rates will rise, that anti-trust action will clip their wings, or just the fact that there is almost a sense of technology exhaustion amongst some analysts who may have been looking in other directions?

The point I’m making here of course is that we invest in the underlying business more so than the idea of it or last year’s profit.

Investing because the trading price is soaring is one of the less reliable ways to invest that I can think of. Of course, sometimes it actually works (for a while) – especially in a market like we have at the moment.

As I’ve mentioned elsewhere, capital is readily available currently and in a highly liquid environment we’ll see property prices and share prices rise easily, as though there is no such thing as underlying economics or fundamentals (investing gravity).

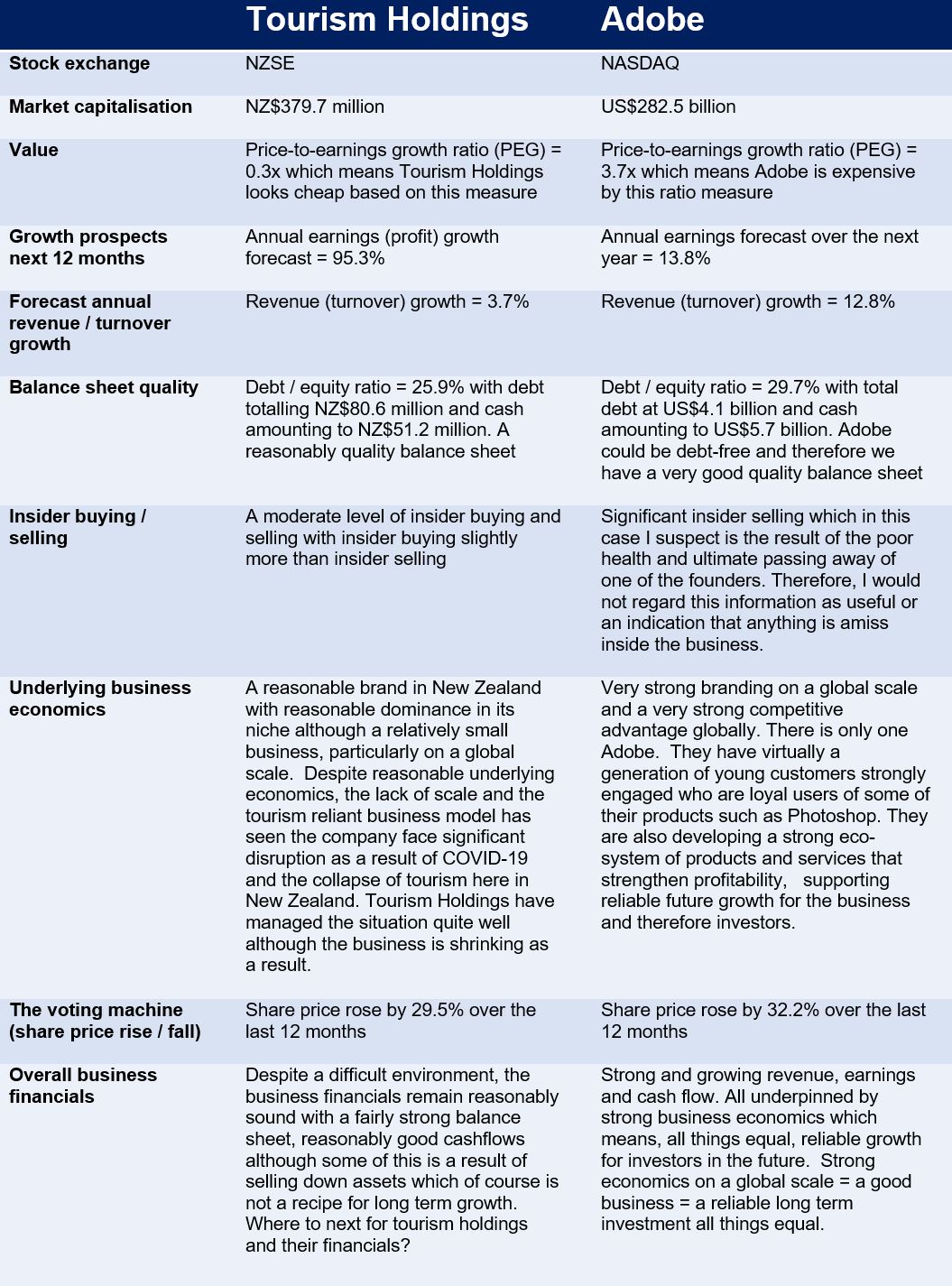

Tourism Holdings and Adobe

Just for fun, let’s take a look at two totally different businesses. Neither are recommendations. This is just for your information and learning.

The above comparison between Tourism Holdings and Adobe may offer limited clarity around the importance of the underlying economics of each business as it overviews the financials and to a limited degree the underlying economics of each business for comparison purposes, some learning and just for fun.

So, on the basis of the information above, if you have to fall one way of the other, which of the above two businesses, in theory, would you invest in?

Whilst it’s always crystal clear in hindsight, when we look at the business model of Tourism Holdings, the idea of the business is sound and represented promise. Not a bad idea and not a bad business generally but not ideal, and not the only game in town for you and I as investors, which is the real point – there are many other options.

BTW – the projected profit growth of 95% for Tourism Holdings sounds good but to me is a ‘red flag’. I prefer ADBE’s 13% estimated growth because it is more likely to be repeated. 95% growth suggests the business is possibly subject to market conditions that it is struggling to control.

When we look at Adobe by comparison, we have a much larger business which means resilience and reliability but also, the strength of the underlying business economics represents sustainable profitability for the business. This may help to underpin a better ROI for investors long-term.

We can’t see into the future and therefore the future’s difficult to predict. What we can do though is assess the strength and reliability of various investment options and select in a considered way.

Remember, the above table is just for fun, and they are not specific recommendations for you today.

One investing secret worth big money for investors

The answer is not the name of a business or some hot share tip.

The answer revolves around what versus how.

Instead of looking what to invest in or even where to invest, best results can be achieved by focusing on how we go about it.

So, it’s not what or where, but rather how.

You might have a different view however, many of my clients and I prefer a well-reasoned approach to investing rather than relying on outside influences to come together to make the investment work in our favour.

That relationship between cash flow and the amount of capital deployed to generate that cash flow is in the how category. This is a more reliable approach when compared to what to invest in or where (e.g., cryptocurrencies, gold, etc).

Direct shares can sometimes appear to behave a bit like cryptocurrencies and gold because the markets determine the price. The market can be fickle.

Still, prices bobbing up and down don’t necessarily reflect operational earnings or strong underlying business economics – that cannot be said for cryptocurrency and gold because of the difficulty establishing an intrinsic value.

Perhaps another point worth considering too is the fact that when we establish an intrinsic value and look at the relationship between cashflow and the capital used to generate the cashflow, more than likely we can understand it.

Do you understand gold? I know it sounds simple.

What about cryptocurrencies?

Simple does not mean no good. Indeed, as the old saying goes, “Less is more.”

Complicated, difficult to understand and tricky does not necessarily mean a better return on our money.

In my experience, no amount of analyses, mathematical calculations, complex formulas, spider graphs and the like, can make up for an investment that is fundamentally challenged at its core.

That type of investment relies on a combination of variables to all pull together in the same direction for that type of investment to work. That can happen but tends to be temporary, not sustainable long term.

Capital assets on the other hand can be measured simply and understood.

As the table above demonstrates, it’s not that hard to see which investments offer more promise and reliability than others.

Investing need not be complex and difficult.

Investing can be simple.

“The truth is not always beautiful, nor beautiful words the truth.”

Lao Tzu