The Changing Credit Cycle, Good or Bad?

The Investment Perspective – January 2022

Peter Flannery Financial Adviser CFP

“Neither the investing method nor the fundamentals of the business are right or wrong because the mood of the market is favourable or unfavourable toward the “stock”. That is because when you really think about it, “stocks” (shares) are all about the financials and the trading price, the share price… the cash up value. What matters more is the economics of the business”

Peter Flannery

Investing in the changing credit cycle over 2022 and beyond

Key Points:

-

The credit cycle is changing, now.

-

Life will be more interesting for some, difficult for others.

-

What might it mean for you?

-

How should you invest?

How does one do that?

First, we’ll take a quick look at the credit cycle. What is it? What does it mean? How does it behave? And how does it impact on investors?

We’ll then take a look at where things might be heading.

From there, we’ll look at how to invest successfully.

What is the credit cycle?

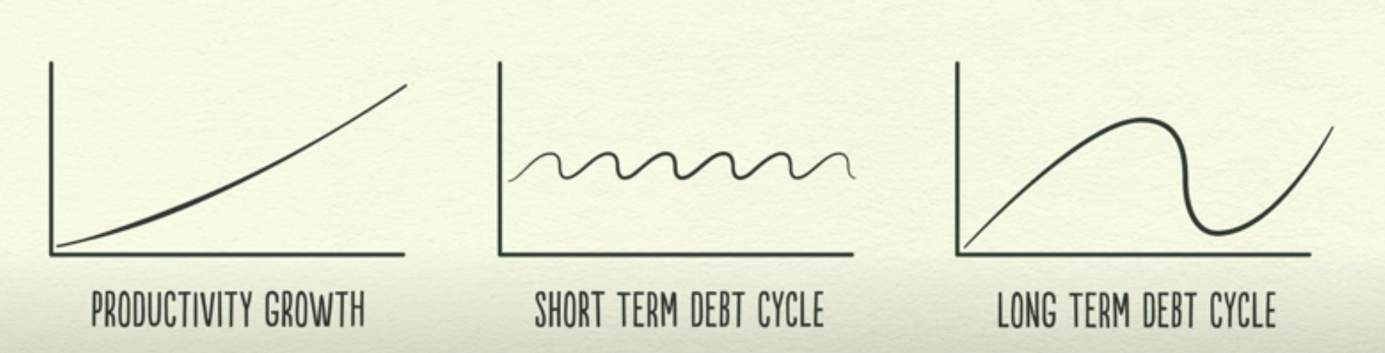

Components of the credit cycle

The above diagram shows the three components of a credit cycle.

So as you can see from the diagram above, the credit cycle consists of

- productivity growth

- the short-term debt cycle

- the long-term debt cycle

If you’ve been around with WISEplanning long enough, you may recall that back in 2003, I started talking about the long-term debt cycle.

I referred to it as “The 70-year hit”.

Back then, very few attendees in those public addresses that I presented throughout New Zealand were familiar with words like liquidity bubble, money printing, federal reserve, and so on.

As we moved closer to 2008, the number of hands rising when I asked the question about who were familiar with those terms, gradually increased until the majority of people were beginning to be familiar with those terms, as we moved closer to The Global Financial Crisis in 2008.

I’m not sure, though, that they understood the implications.

Although not everyone was affected back then, most people were to some degree. Many people had heard of the global financial crisis, and a good many were right in it, in a way that was fast becoming uncomfortable.

Of course, the credit cycle is not as even as the lines in the above diagram suggest. It is unpredictable to some degree in terms of timing but predictable in terms of how the process works.

Credit and money

Simply, credit and money are two different things.

Credit, you could say, is borrowing money, whether it be by mums and dads, corporations, or governments.

Money, we could argue, is income that people earn through productivity.

If you would like to know more about the details of how the credit cycle works, click here to review Ray Dalio’s 30-minute video, which offers a simple and, in my view, great explanation of how it all works.

Transactions and the economy

Simply, transactions or spending basically make an economy.

When you and I buy something, this helps create income for someone else. The more people transact by going about their everyday lives, then the higher incomes may grow.

Rising incomes mean that people can borrow more money to improve their lives and indeed spend more. Of course, when we borrow money to buy things, we are using credit rather than money through productivity.

More credit in the economy means …

As people take on more debt (credit increases in the economy), debt levels rise faster than incomes grow. Long story short, we can get to the phase where, in order to help keep the economy ticking over (without pain to everyday citizens), central banks lower interest rates to the point where they hit zero.

From there, central banks print money in order to keep the economy from falling into a deflationary abyss.

A number of measures can be adopted, such as transferring wealth from the rich to the poor, austerity measures where governments, mums and dads, and corporations tighten their belts, which unfortunately does not help. That’s because with mums and dads, governments and corporations spending less, incomes decline, exacerbating the problem.

Long story short, this situation leads to central banks printing money. Whilst it can lead to a Germany in the 1930s-style hyperinflation event, with the right balance, printing money can actually work to stabilise an economy.

That is, providing it offsets falling credit. That’s because transactions or spending is what really matters. Spending and incomes.

The challenge for the central bank is to get the balance right so that there is enough printed money going into the economy to stimulate incomes to the point where incomes rise faster than the debt burden.

To be clear, the amount of money printed needs to stimulate income growth. But, central banks face a real challenge: everyone loves printed money because it is so easy. No matter what anyone says, no matter how educated or intelligent, we are all only human, if you know what I mean? If we can get money without having to work for it (e.g. lower interest rates, easy to acquire debt) then that is what we gravitate to and don’t try to take it away from us either!

So, assuming the central bankers can get the balance right, borrowers can become more credit-worthy, so lenders will lend more. This means that spending will increase as people’s incomes rise and the economy can begin to grow once again.

It can take ten years.

The above diagram demonstrates the full long-term cycle (“the 70-year hit”).

So, as the diagram above shows, it takes several decades to build up, and with regards to the long-term cycle, there can be two to three years of depression, although that’s not guaranteed.

From there, in the past, there has been a 7 to 10-year recovery process of reflation.

Although again, with the current approach by central banks, it’s difficult to know whether that still holds true. It could be that reflation happens sooner. On the other hand, it could be that it takes much longer, but the pain is spread over a longer period than a sharp 2 to 3-year depression. Time will tell.

It’s also worth noting that the current cycle may not behave as uniformly and neatly as the above diagram shows. As I mentioned, it could be a more drawn-out process. One thing we know is that predicting exactly where we are and where we’re heading is not easy.

However, when it comes to investing, that’s okay, for us.

Real evidence of the changing credit cycle in NZ

What we do know is that easy money conditions are in the past – history.

Just ask anyone in the last 12 months, especially the last three months, how they’ve enjoyed working with their bank.

They’re probably feeling as though the bankers are picking on them. Of course, the bankers are not.

The New Zealand Reserve Bank is responsible for new legislation implemented towards the end of last year, which means that banks are much more accountable for every loan to every customer.

In short, if they deliver loans to customers and don’t meet compliance obligations, they will suffer the consequences. Banks will not want to go there. That means that some would-be borrowers will not be able to borrow money from banks under the new rules.

That pushes those at the margin to second tier lenders. Higher interest rates and very limited tolerance when market conditions change for the worse (meaning they won’t hesitate to call in a loan regardless of the borrower’s situation – where does that leave those borrowers?)

We’re also seeing the healthy homes legislation and other regulatory requirements for residential property investors squeeze some investors out. Even though you may not be an investor in property, this sector contributes to the economy and helps push up property prices.

The bottom line is that every day Kiwis feel wealthy when the selling value of their home increases. They feel as though they can spend more money which, as we discussed earlier, helps in the short term to increase other people’s incomes as those that spend more money to just that.

The problem though is that when the increased spending is based on credit, it eventually becomes unsustainable.

How to invest

Notice I did not say where to invest.

Where to invest or what to invest in is the wrong question.

The right question is, “How do I invest”?

The answer is that we invest in quality assets that will be resilient in changing credit conditions ( no, not a bank account. Cash and term deposits are sometimes referred to as melting ice cubes because inflation erodes their value).

As you know, at WISEplanning, we invest in assets (property, direct shares, our own private enterprise) that demonstrate sound economics.

When it comes to direct shares, we invest in the business not the stock. We do not play the stock market.

Still, the market plays the stock market and almost all of what you’ll read and hear about revolves around playing the stock market.

At WISEplanning, we invest in the business because we know that it provides better protection for our capital.

It can also help us to achieve better long-term performance (depending on our investing strategy).

So the first thing, is that we invest in the business and resist the temptation to play the share market.

Then (again it depends on the investment risk preferences and your investing strategy) if you are looking to protect your capital and minimise volatility, you’ll look for large businesses that are well established, well-financed, and consistently profitable.

What we are looking for here is to maximise probability and certainty on our investment outcome.

We want a high probability of investment success along with the certainty of return. We want the return on our capital and the return of our capital – and to sleep soundly at night.

The e-Biz investing methodology provides that. Not perfect, but works reliably across all phases of the changing credit cycle.

There are, of course, no guarantees, but we want to be at the high end of certainty rather than the low end where it’s basically guesswork and hope for the best. In that space (playing the share market) investors are unwitting speculators who rely on the economy playing nice and trading prices of shares to rise all of the time.

The types of reliable businesses that come to mind would be the likes of Alphabet, PayPal (even though I know its trading price has declined sharply recently), Diageo, Unilever, Microsoft, and those larger, well-known, consistently profitable businesses.

Again, it may depend on your investment risk preferences and your investing strategy, however, when a credit cycle tightens significantly, you might be less inclined to invest in Small Caps because they can be more vulnerable. Also businesses that perhaps have yet to develop a sustainable track record and those who aren’t yet profitable and may be using large amounts of debt to help fund their progress.

Sexy new name tech stocks may also fit in this category (e.g. Tesla, Palantir, DocuSign, Zillow …). These companies may continue on to great success. The probability of that success varies. The certainty is not high.

Next …

Then, I suggest it might be useful to focus on your investing strategy. Strategies vary from one investor to the next.

At WISEplanning, a more advanced strategy means a more concentrated portfolio where diversification is no longer useful. As well, we include Small Caps.

Less advanced investing strategies do not participate in portfolio concentration and use diversification to help manage portfolio volatility and risk. Small Caps tend to be avoided with the emphasis on large sustainable businesses.

I know this explanation is high level. This is about as far as we can go without getting into each individual investor’s circumstances. That is what we do during our meetings and as I routinely review your investment portfolio.

What can we expect over 2022 and beyond

My expectation is for increased levels of volatility, and at some point, the markets could seriously correct, which could amount to a 20% pullback.

Indeed, if we could achieve such a pullback, I would be very happy about that because it provides a great opportunity for definitive action.

I’m not saying that we will necessarily, absolutely have a 20% correction. However, this environment of a tightening credit cycle, with less money flowing through the economy can create that kind of response from the market.

To be clear, in an environment like we’ve had, particularly since the 2008 global financial crisis where central banks have almost forced money into the economy, has allowed some businesses to succeed whereas under normal circumstances this would not be possible.

We are moving into a different phase now.

It’s important for an investor not to confuse volatility with whether it’s a good time or a bad time to invest or whether so-called shares on the share market is still a good idea.

Quality assets are always good.

It’s also important that investors avoid confusing the intrinsic value with pricing. The trading price of your investments are determined by the market and its response to news and events, if you see what I mean.

One question that comes to mind is whether your portfolio has sufficient cash to take advantage of the upcoming volatility?

If you’re happy riding things through and being patient, then don’t panic about whether or not there is sufficient cash.

On the other hand, if you like a more active approach and are keen to target volatility, then give it some thought and let me know either at your next review or anytime if you would like to consider raising cash within your portfolio. You can also add cash from outside as well if funds are available.

Remember, too, that we are not trying to time the markets. Simply, we are looking to invest in good businesses at hopefully better pricing – bring on that volatility!

The more, the better.

“Men’s natures are alike. It is the habits that carry them far apart.”

Confucius