What If Something You Always Believed Was Just Wrong?

The Investment Perspective – August 2021

Peter Flannery Financial Adviser CFP

“Neither the investing method nor the fundamentals of the business are right or wrong because the mood of the market is favourable or unfavourable toward the “stock”. That is because when you really think about it, “stocks” (shares) are all about the financials and the trading price, the share price… the cash up value. What matters more is the economics of the business”

Peter Flannery

September’s coming, is volatility coming with it?

Typically, the period from August to October is a volatile time across the markets.

What about this year?

There’s no way of really knowing however if we look at the probability based on historical evidence, one could conclude that volatility at some point over August, September, and October is likely but not definite.

Some of the reasons for volatility in the past include the likes of holiday time in America ( lower trading volumes), rebalancing portfolios for tax purposes, and rebalancing portfolios for year end purposes. Certainly, there have been some major share market corrections over this time in the past.

Notable events throughout history in October include the 1907 panic.

Essentially this was a banking crisis where speculative investments had been financed by certain banks because of the easy money conditions at that time (sound familiar?).

Ultimately runs on New York banks and trust companies led to banks falling into liquidity problems and resulting in the panic of 1907 (as depositors struggled to get their money back).

Not well-known by many people today but a notable event at that time. Interestingly, JP Morgan stepped in with funding to help bail out surviving Wallstreet banks and other financial institutions.

This event led to the establishment of the Aldrich Commission and the historical meeting at Jekyll Island, Georgia where we have the beginnings of the Federal Reserve System.

Other notable events include Black Tuesday, Thursday, and Monday in 1929. Black Monday in 1987.

Going back in history, the original Black Friday actually occurred in 1869. Two other significant single-day declines in the Dow Jones Industrial Average (the US share market) were in 2001 after the 9/11 event and in 2008 as the subprime mortgage crisis began ramping up. I could go on however you can see what I mean about the numerous events in history over September and October.

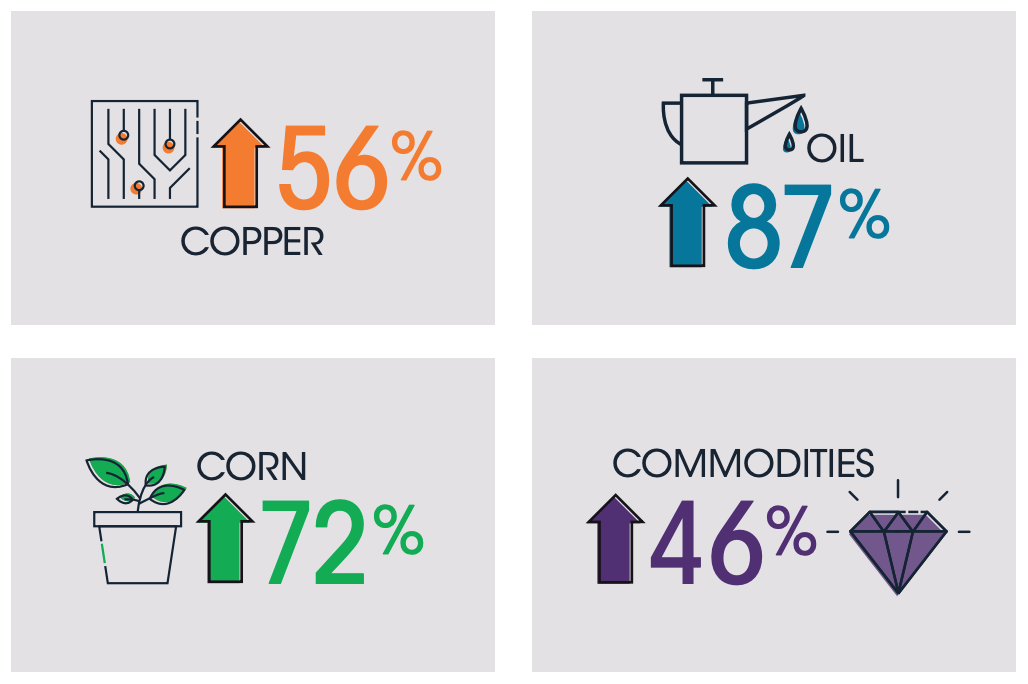

Commodity returns

The above diagram shows the increase in specific commodity prices recently.

When you read about upward historical price movement that is significant whether it be property, cryptocurrency, commodities, direct shares … do you ever feel the sting of FOMO?

Do you ever have that feeling “if only I had known…if only I had taken action, etc.”?

Truthfully, we all have a sense of FOMO at one time or another although more experienced investors are better able to put these types of numbers into some sort of perspective. They notice them but readily move on knowing that there are better things to focus on.

There are three kinds of lies…

“There are three kinds of lies: lies, damned lies and statistics”

Mark Twain

We need statistics, numbers, and analysis to be able to understand investments.

We don’t need the lies though!

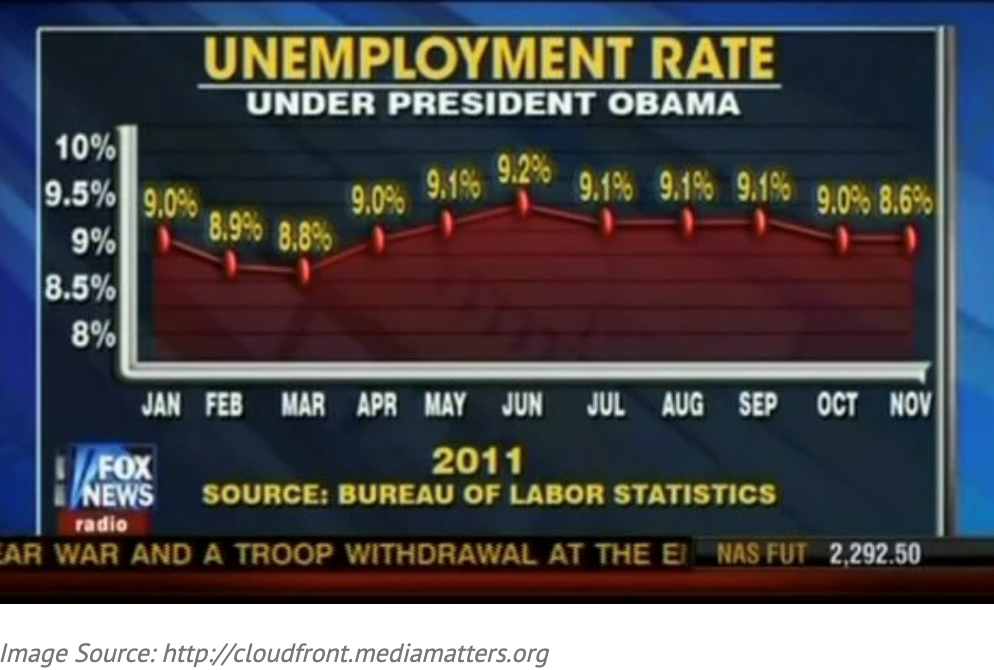

Fox News stretching the truth

The above graph when we take a closer look is somewhat misleading.

Looking more closely at the graph above, we can see that the value for November (8.6) has not been plotted correctly. It’s placed at the 9.0 position. Also, with the way that this graph is structured, it looks as though there is ongoing growth that is semi-exponential when in fact the overall trend is reasonably stable at around 9%.

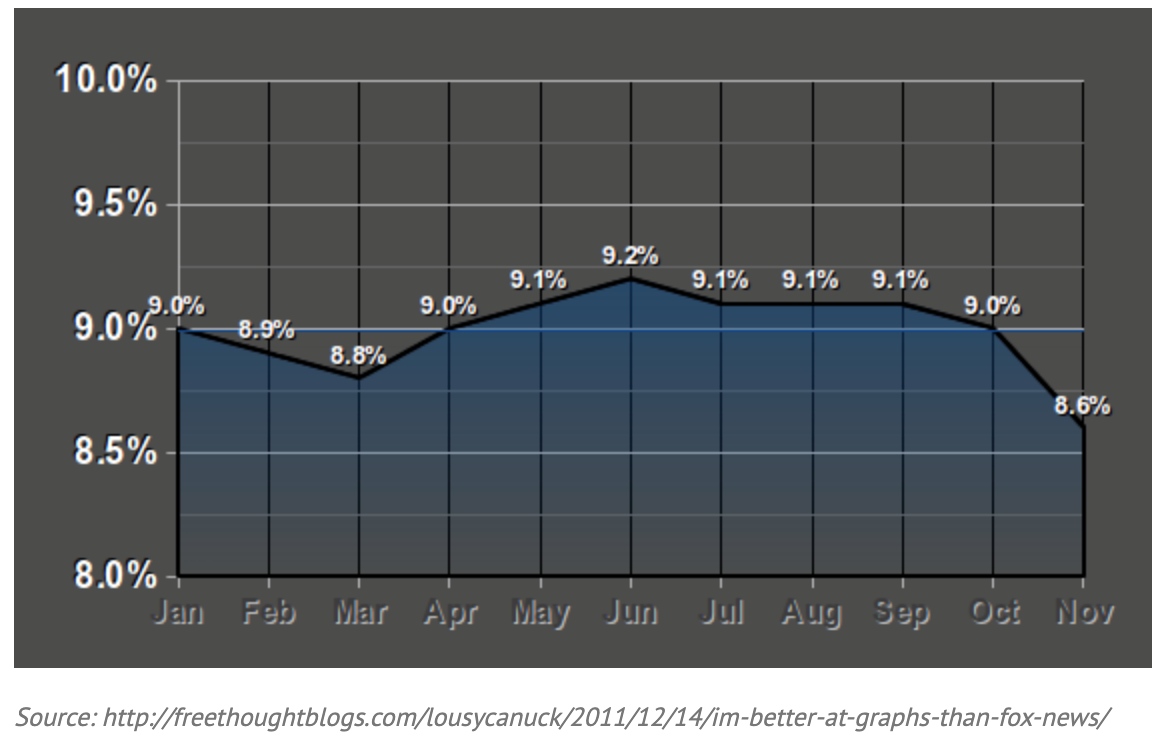

The graph above reflects the true position.

When comparing the two graphs above, it becomes clear that the top graph is incorrect and somewhat misleading. There are lots of examples of misleading information and indeed those looking to be creative because of self-interest can be quite convincing.

Two Other “lies”

There are all kinds of “permutations of the truth”.

There are a couple of classics in the investment world that you may have heard about.

Although some diversification can be beneficial, one is the myth that diversification is somehow a rite of passage to successful investing. For example, over the global financial crisis from 2007 over the next few years, diversification was of minimal benefit to many investors.

Not that you would contemplate such a tactic however a number of Kiwis invested large sums of their money in finance companies. The idea was that they would spread their eggs around different baskets in the finance company sector so that if something didn’t work out too well with one, they still had all the rest.

They didn’t figure that the global financial crisis placed most of this sector in New Zealand and other countries, all of a sudden at high risk – just because liquidity dried up. This is what we call a credit crunch and is the opposite of what we have across the global economy now.

Still on diversification, there are many who believe that diversifying their investments particularly in managed funds and the like are protecting the capital by doing so.

It may help to reduce volatility but then the very nature of diversification slows down investment returns longer-term.

This is easily explained when you think about the fact that when investing in a so-called balanced fund, if half of the investment is in term deposits and other forms of fixed interest alongside the other half that is in direct shares and perhaps property, then 50% of this investment mix simply cannot grow.

In a low-interest rate environment as we’ve seen, balanced funds can achieve some growth from the 50% that grows (which is doing all the heavy lifting and then some), to counteract the other 50% in a balanced fund that generates limited income but no growth.

Looking again at growth managed funds where the majority of assets are indeed in growth assets like direct shares, again we see significant diversification across a variety of different shares. In some cases, there are literally hundreds of different companies in which investors money is spread across.

There is more to it, but if you think about it for a moment, it is not possible for 5 or 10 different large businesses to all have the competitive advantage in one sector ( one, maybe two, not three or 10).

Therefore, by default, diversification reduces the performance that can be achieved. This is because those less competitive businesses cannot be as profitable and therefore cannot grow at the same pace when compared to the one with a competitive advantage and strong economics.

The challenge of course is that you won’t see evidence of this in any income statement, balance sheet, P/E ratio, or discounted cash flow analysis.

And so, it’s not the bare facts that can be distorted but also the absence of critical information as well.

Another classic…

Another one that is quite pervasive across the market is that companies that pay a high level of dividend and indeed increase the level of dividend every year for the last 10, 12, or 15 years must be good companies to invest in.

If we leave aside any tax issues (bearing in mind that we pay tax on income as individual investors) it could be that a company that is able to pay a high level of dividend is indeed a sound business.

It’s always interesting to look below the surface to establish what is driving the ability of that business to be able to continue to pay healthy levels of dividends year in, decade out.

At some point, there is a so-called “pattern interrupt” whereby a market or company event suddenly means that the company can no longer pay at that level or in a worst-case situation needs to stop paying any kind of dividend at all.

Cast your mind back to Telecom back in the day … there are many other examples.

What happens to the share price then? Only one thing.

That one thing of course is that it declines by a significant amount because the reason they traded at the previous trading price for so many years was of course because the market loved the dividend. Lots of income hungry investors purchased the shares for the dividend.

As the old saying goes, “When the money runs out, the love runs out.”

When the high dividend-paying companies for whatever reason are not able to pay at the same level or indeed can no longer pay a dividend, watch the market sell en masse and the trading price ‘drop like a stone’, as they say.

The methodology developed at WISEplanning shows that businesses that pay out most of their profits as dividends are relying on a lot of things to go right to be able to continue paying out their dividend, at that same rate in the future.

Other businesses that perhaps pay a much lower level of dividend may not be favoured by that section of investors however they are able to keep profits inside the business and redeploy for growth.

The compounding effect on the growth of a good business is a worthwhile investment, particularly in the long run.

Perhaps to finish off this part of our conversation, sometimes investors think that they should be investing in high dividend-paying companies when they retire so that they can receive an income.

At WISEplanning, we have a system developed over the last few years called The CASH Tap.

Simply, it does not rely on investing in high dividend-paying companies but rather quality businesses that continue to grow.

Their income from the portfolio flows to them every month, regardless of market and economic conditions. Over time the portfolio can often continue to grow as well.

Further, adhoc lump sums can be withdrawn too.

As sometimes is the case, things are not always as they seem with a superficial look.

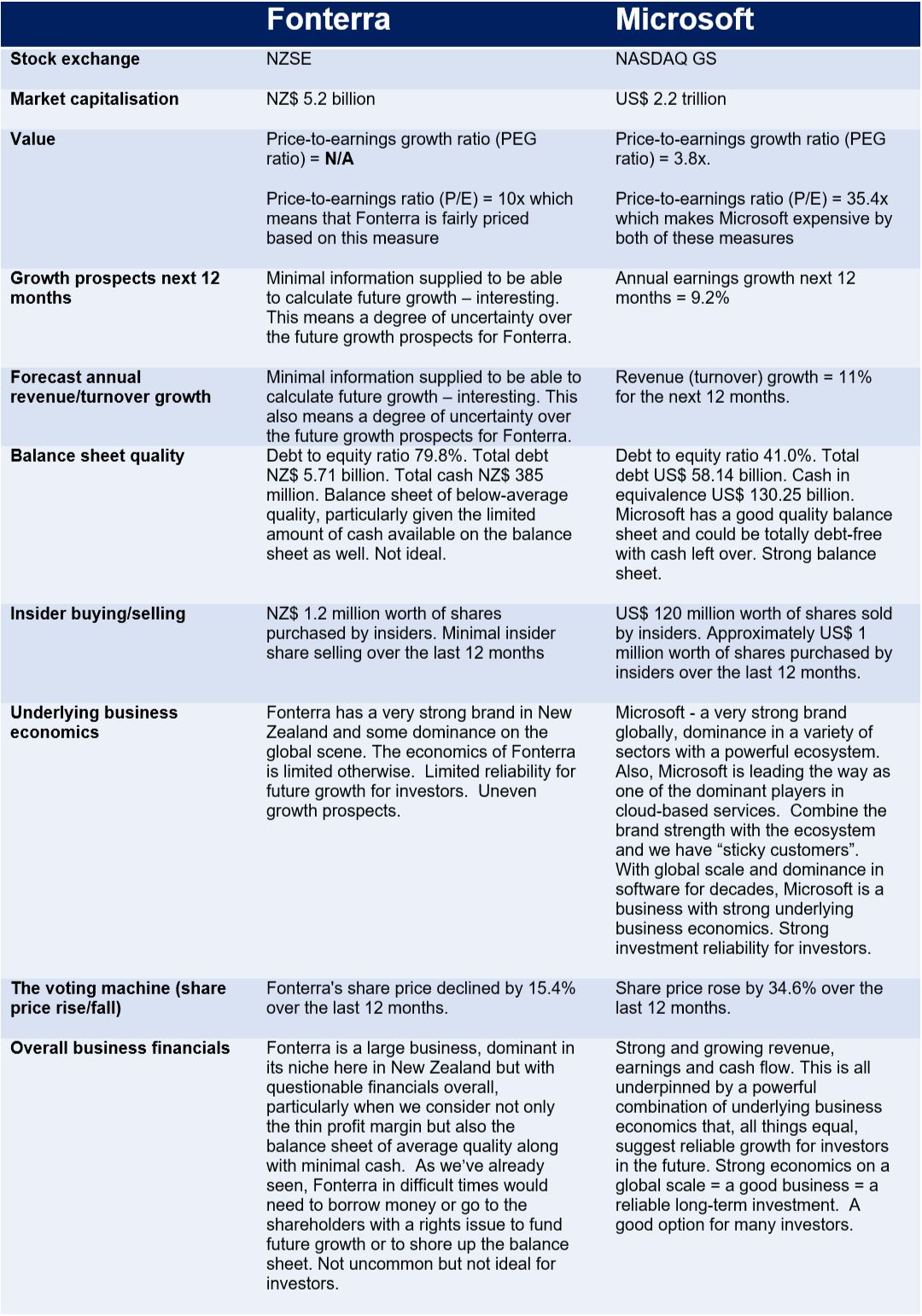

Fonterra vs. Microsoft

Just for fun, let’s take a look at two totally different businesses. Neither are recommendations. This is just for your information and learning.

The above comparison between Fonterra and Microsoft may offer limited clarity around the importance of the underlying economics of each business as it overviews the financials and to a limited degree the underlying economics of each business for comparison purposes.

On the basis of the above information, if you had to fall one way or the other, which of the above two businesses above would you invest in?

Fonterra has a strong brand within New Zealand and is a favoured investment by some who see the demand for protein from Asian and other developing economies as a tailwind for the company.

However, Fonterra is a good example of a company that, despite the tailwind trend, the underlying business is actually not that good. Evidence of this is the thin profit margin and as a result, a poor-quality balance sheet which makes for a potentially problematic combination.

This doesn’t mean that there may not be periods of positive growth in the future, however the reliability of that growth is questionable given the average financials and poor underlying economics of Fonterra the business overall.

Microsoft on the other hand ticks a lot of boxes with sound financials and powerful underlying economics suggesting reliable growth for investors long-term.

One more example

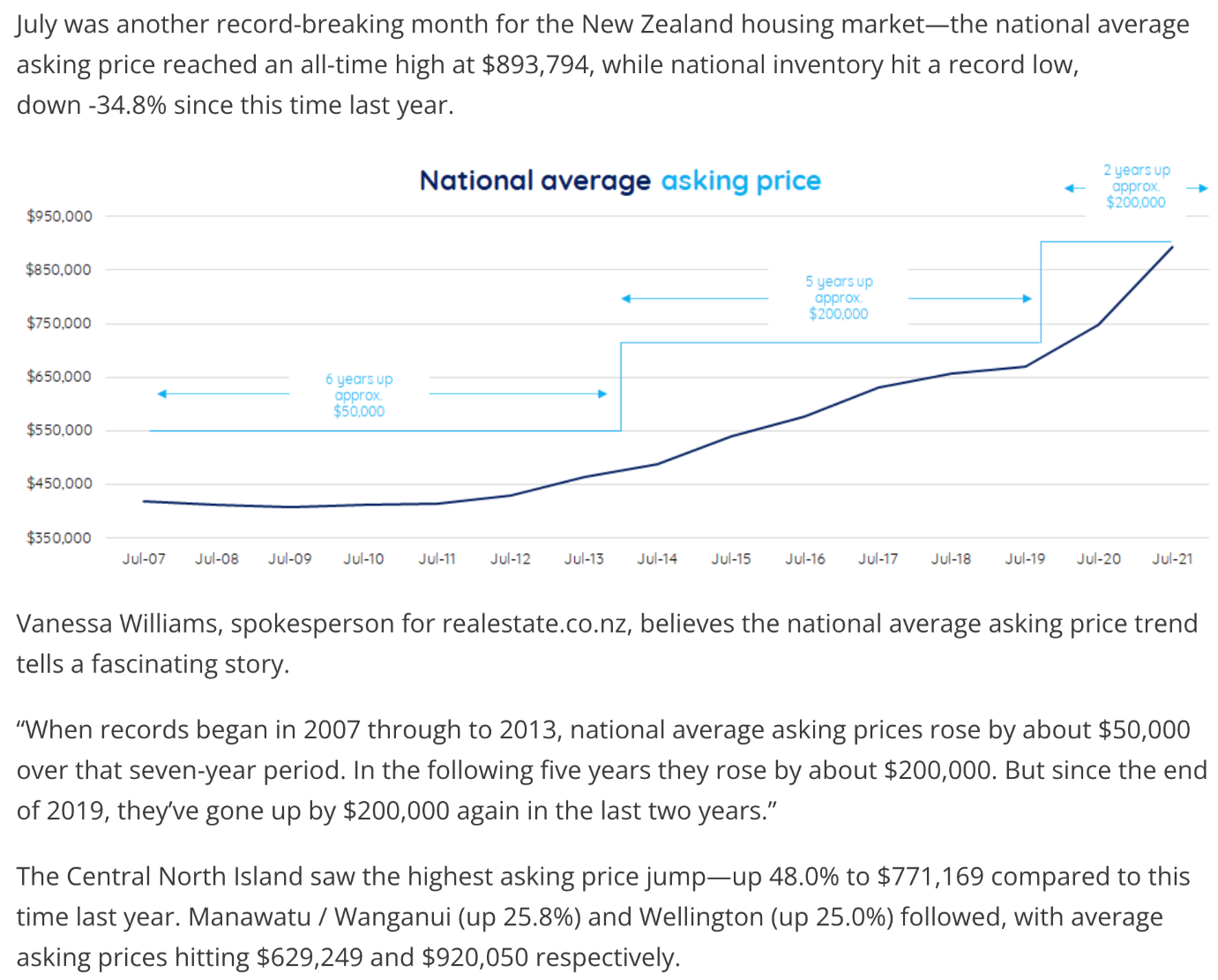

Whether it’s lies, fake news or indeed the absolute truth, I’ll let you decide. Here is a copy and paste from realestate.co.nz.

The combination of a graph and some commentary discusses the rise in residential property prices since July 2007.

Reading the above commentary, looking at the easy-to-understand graph, one could be forgiven for thinking that residential property is a “no brainer” in terms of an investment worth considering. It hasn’t actually been that horrible in the past.

The real question for us though is whether that historical performance is intrinsic to the asset or whether other external forces are driving the outcome for prices?

For example, there’s no question that residential property has its own characteristics in terms of the ability to leverage it, the supply and demand equation that pushes prices up when demand exceeds supply, and the fact that, in share market parlance, the “brand strength” of residential property as an investment is strong.

In other words, brand strength in simple terms means the shortcut to the decision-making process – action with no need to question anything.

Another way to look at this is, when everyone else is doing it, it must be okay.

Without getting too carried away or deep about it, humans are herd animals and instinctively gravitate to this type of behaviour (stick with the herd, safety in numbers) – it is instinctive.

Anyway, if we take away the liquidity bubble from the last 30 years, I wonder where residential property prices in New Zealand might be?

For example, interest rates have been declining for over 30 years.

Reducing interest rates is a significant tailwind for residential property prices.

Not only investors, but mums and dads too have an increased capacity to borrow and upgrade their property to a better property with a larger price ticket. Property investors too are able to add yet another property on the strength of the equity that has emerged from ever-increasing residential property prices.

In short, ideal market and economic conditions providing a significant tailwind to residential property owners. Increasingly difficult though for those wanting ‘to get on the property ladder’ as it were.

By the way, one advantage that residential property has is that it is a capital asset.

In other words, it has an income stream (rent) much like direct shares (earnings) or one’s own closely held business enterprise (profits).

To cut to it, I wonder how much of an increase in interest rates it might take for mums and dads and property investors to become less excited about ‘the brand strength’ of residential property?

What impact would say, a debt to income ratio if introduced have, in addition to other existing regulations on future residential property prices?

How to make sense of it all?

Whether it be misleading graphs, convenient property narrative (telling us what we all want to hear as property investors and homeowners) promises of the elusive king-hit or home run result, there are plenty of opportunities for us to be led in the wrong direction.

Although it’s not obvious to most people, a fundamental approach to investing does help to block out most of that noise.

This doesn’t mean that those looking for a convenient answer to their wealth-building challenges won’t follow that convenient path, believing the nice-sounding platitudes that support what they want to believe.

Not everyone, but many people are looking for the story that they can buy into and believe rather than make the effort to carry out some simple due diligence to look below the surface to what’s actually going on.

The best answer I can come up with is to look at the fundamentals and the underlying economics of the asset.

Whether it’s residential property, your own privately held business, or big businesses listed on the share market, the underlying economics are a solid step in the right direction when it comes to breaking through the noise, the misleading banter, and getting on with investing in a way that is reliable and profitable long term, regardless of market and economic conditions in the short-term.

Better still, the volatility this coming September / October, if it does eventuate, will deliver to you lower trading prices and better buying value.

Your requirements as an investor, your goals, some proper investing strategy including the economics of the asset, and a bit of help along the way – it’s not complicated.

“The truth doesn’t rely on being believed.”

Dina Hillier