Invest In Brands That Make You Money

The Investment Perspective – April 2022

Peter Flannery Financial Adviser CFP

“Neither the investing method nor the fundamentals of the business are right or wrong because the mood of the market is favourable or unfavourable toward the “stock”. That is because when you really think about it, “stocks” (shares) are all about the financials and the trading price, the share price… the cash up value. What matters more is the economics of the business”

Peter Flannery

Brand Power

Key Points:

- Why invest in well known brands?

- Who are the most valuable brands in the world?

- Rights issues vs stock splits. Which is best?

- What about the Air New Zealand rights issue?

- Heico vs Air New Zealand

Branding, as you may know, is an important business economic. That’s because a successful brand represents, in very simple terms, the shortcut to the decision-making process for consumers and users.

In other words, a good brand also means trust.

Consumers don’t look elsewhere but go straight to the trusted brand and readily use their goods and services. They don’t look around. They don’t wonder what options are available. Simply, they go directly to the trusted brand.

Those businesses that are able to have their company name take the place of the good or service can have the most powerful brands of all. Lux (Electrolux) from way back, meant vacuuming. Mums around the world luxed the carpet. Alphabet or Google is a very good recent example. People don’t search engine for information but rather Google it.

When markets are in turmoil and become volatile, strong brands prevail. Over time, those businesses attached to strong brands grow.

Working Out The Brand Value

Every year, a research group known as Kantar BrandZ ranks businesses based on their brand value. They measure it by:

- the brand’s total financial value, which is the financial contribution that the brand attracts to the parent company (dollar value)

- This is multiplied by its proportional value, proportional impact on its parent company sales (percentage value)

These results are then combined with quantitative information sourced from over 170,000 global consumers. In the end, is a holistic view of a company’s brand equity, reputation and ability to generate value.

Strong branding is powerful, but only part of the puzzle. There are other business economics that, when they all come together help to reduce risk for investors and increase the chances of a successful outcome in the long run.

Rights Issues and Air New Zealand

You may have seen the media information around Air New Zealand’s rights issue.

Although I haven’t been flying much over the last couple of years, as a regular customer of Air New Zealand prior, I favour them as my preferred carrier and look to travel with them whenever I can. Overall, I feel they do a good job for me as a customer.

As an investment, I have a different view. In short, they fall well short of the criteria that we use at WISEplanning when we’re looking for businesses that will prove successful for us as investors long term, with minimal risks and maximum profitability.

Air New Zealand (AIR) may provide some investors with a short term trading opportunity but the merit of investing long term remains questionable.

Rights Issues and Stock Splits

Rights issues are generally where a company looks to raise capital for the purpose of repairing its balance sheet (as in the case of Air New Zealand) and/or for growth.

Whilst it’s in some ways a good thing to raise capital for growth, the fact that when a business needs to do that, speaks to the underlying economics of the business and how well or otherwise they use capital.

Successful businesses don’t often find themselves needing to carry out rights issues to fund future growth. They can do so through cash flow. The reason they can do it through cash flow is that they have a higher return on equity and use capital well.

Stocks splits are something different.

That’s where a company will decide to increase the number of shares on offer and at the same time, reduce the price of the shares so that everybody finishes up in the same place in terms of the value of their holdings. They just own a greater number of shares at a lower price.

Companies generally do this because they want smaller shareholders to be able to invest, at least that’s what they say. The reality is that they want plenty of activity around their stock to look good and also, it may be beneficial in terms of any funding they need to undertake.

If I have to fall one way or the other between a company that was involved in raising capital through rights issues or another company that simply carried out stock splits, I will go for the stock split company almost everytime.

That’s because they probably have more growth going on, which is one of the reasons they split their stocks. We as business owners see stock splits as a bit silly and a cost that business owners have to bear. Stock splits are a form of ‘window-dressing’ and there is actually no fundamental advantage from a business perspective.

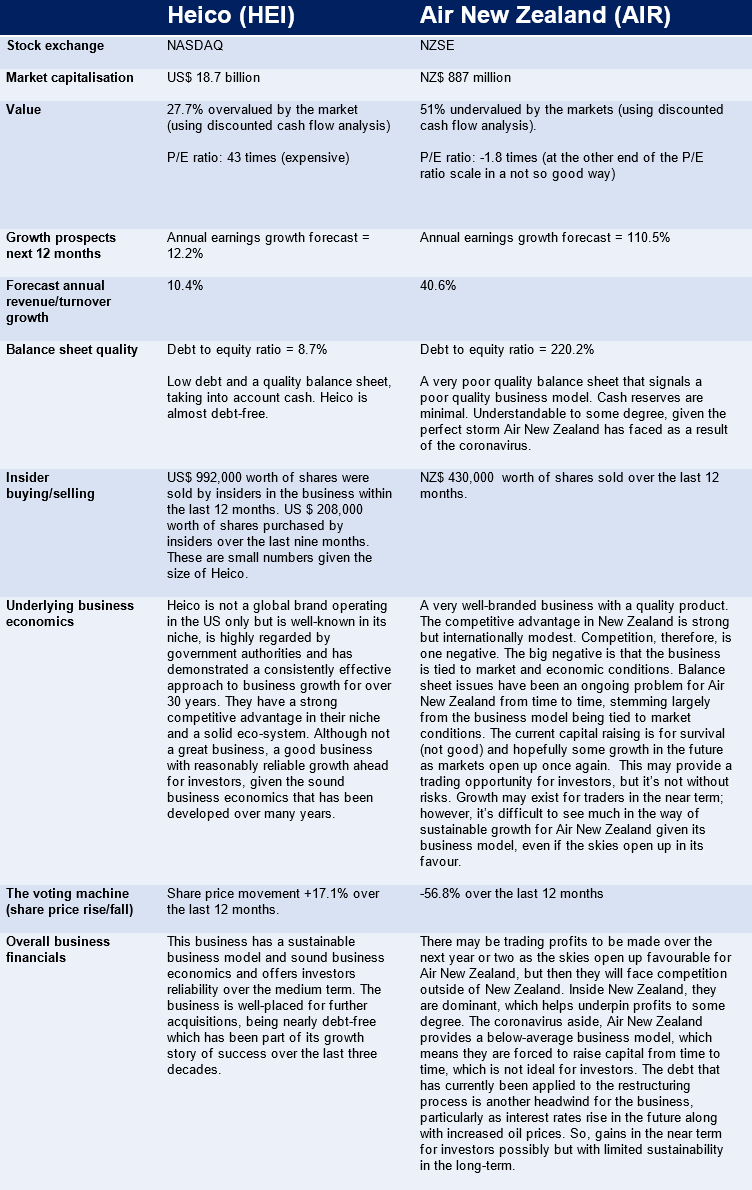

Heico vs. Air New Zealand

Since Air New Zealand are in the throes of restructuring its balance sheet, I thought it might be an idea to compare Air New Zealand with Heico. They are very different operations, but of course, it is all about investing in a business that offers the more favourable prospects. As you know, neither of these are specific recommendations for you right now. This is just comparing two businesses for the fun of it.

The above comparison between Heico and Air New Zealand may offer limited clarity around the importance of the underlying economics of each business as it overviews the financials and, to a limited degree, the underlying economics of each business for comparison purposes.

What do you think about Heico and Air New Zealand? Which one do you prefer?

Interestingly the rights issue offer price of AIR was significantly discounted from the prior trading price. That’s because the institutional investors would have struggled to participate in the rights issue without a sensible offer price.

The discounted cashflow used to value AIR and HEI showed that AIR looks cheap. That’s because this analysis, based on estimated future cash flows (commonly used across the market), does not include the balance sheet (or the business economics).

In short Heico offers ongoing growth medium to long term, with a good amount of reliability. Air NZ may provide a short term trade but limited reliability for investors medium to long term.

Brand Value

Because we invest in the business rather than the stock, we might give up possible trading gains that others may enjoy. The trade-off though, is that over time, we will have more reliable returns that are more likely to be profitable (even if it is a bit more boring).

Strong branding generally means a shortcut to the decision-making process for consumers. That’s extremely valuable for businesses and investors alike as it cuts out a layer of costs for the business and reduces the need to allocate profits to attracting customers. That can mean more profit and that is good for investors.

That’s also why another business economic, the competitive advantage, is so valuable. Profits can be redeployed for growth. Businesses can use capital at a higher and more effective rate providing reliable performance for investors long-term.

For investors, this avoids the need to chase markets and trading prices, hoping that they always rise or that they don’t decline.

You and I love pricing declines and we love volatility, don’t we?

“ Life is really simple, but we insist on making it complicated”

Confucius