Trading Prices Riding High, Where To Next?

Monthly Market and Economic Update – November 2021

Peter Flannery Financial Adviser CFP

“If you have one economist on your team,

it’s likely that you have one more than you’ll need.”

Warren Buffett

Key Points:

- Trading prices remain expensive.

- Markets feel bullish.

- The market noise is getting loud.

- The global economy continues to grow.

- NZ entering a new Delta virus phase.

- Speculation is common.

- FOMO is increasingly widespread.

- Am I sounding old, out of touch?!

THE MARKETS

Where Is The Volatility?

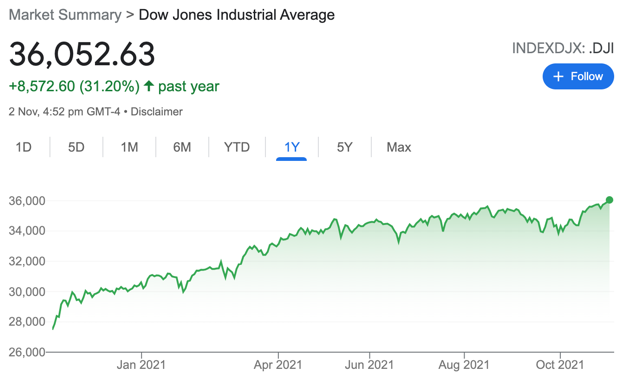

The US Market was down by about 5% over September and then as one client put it…”It’s shooting for the moon once again!”

The volatility over September was short-lived. Over October, markets rebounded, and it’s almost as though there was no volatility. Indeed, I was hoping for much more.

It simply wasn’t enough because the volatility we saw over September meant trading prices were slightly less expensive but, a long way from cheap.

Still, with rising interest rates, there is a good chance that we’ll see volatility in due course.

The chart on the left shows the US share market (the Dow Jones) over the last six months. The chart on the right shows the US share market (the Dow Jones) over the last year.

Sometimes one month is a long time across the markets. However, when we look at what worries the market, the major items remain mostly the same as last month.

What’s slightly amusing, is that when you think about the wall of worry over the last 30 days, indeed over the last 60 days, none of it really mattered when we see where things are now across markets and the global economy.

Anyway, here are some items that the market does worry about still:

- Rising inflation and rising interest rates. Interest rate direction and pricing are usually difficult to predict. What we can see is that 10-year US Treasuries have increased measurably since the beginning of September this year. As the chart below shows, 10-year Treasuries actually reached a peak of around 1.75% towards the end of March this year.

The above graph tracks the Yield on 10-year Treasuries and highlights the increase since the beginning of September this year.

- Global supply chain constraints. This item has been noteworthy for several months and continues to impact economic productivity. There is no end in sight at this stage. Even here in New Zealand for example, many looking to build a home are facing lengthy delays. Apple recently missed their latest expected earnings number which they say is directly related to chip shortages.

- There are other items that I believe may appear on this list in due course, which might include:

- Stretched trading price valuations. Markets are hovering around all time highs.

- Re-emerging debt ceiling uncertainty in the US. Due to be debated again in a few weeks.

- Evergrande, the large property developer in China currently struggling to service its debt. There may be others.

- Further down the road, rising oil prices could also start to impact.

Both Apple and Amazon reported results that did not meet market expectations for the recent reporting period. For Apple, it is a case of those supply chain issues as outlined earlier. For Amazon, it is supply chain issues along with increasing wages costs and transportation costs as well. The point here is that fourth-quarter reporting could see lower results still. Time will tell.

Does this mean that we should scale back or bail out of Amazon and/or Apple? In a word, no. Unless of course, you like to play the markets. Playing the markets does work sometimes but is unreliable. In the end, for most, it is best to simply stay put with a quality business and ride through the volatility, possibly taking advantage of lower pricing along the way.

Both Apple and Amazon are strong businesses with solid underlying business economics. It’s beneficial in the long run not to confuse pricing movement (popularity or otherwise) with the fundamentals and the quality of the business.

Meanwhile, Australia is opening its doors to flights from other countries, specifically to Sydney, for the first time in over 12 months.

In New Zealand, interest rates have been rising notably. It will be interesting to see if further interest rate rises are forthcoming or whether the rise moves into a holding pattern.

More medium-term, the expectation is for ongoing interest rate rises. However this won’t be enough for those who persevere, trying to earn an income off term deposits, but might be enough for some homeowners or property investors who borrow, to start noticing the difference.

All that said though, the NZ Reserve Bank has imposed restrictions such as the loan-to-value ratios and looks set to implement the debt-to-income (DTI) ratio restriction soon as well (possibly over the next six months).

The DTI, along with other restrictions already imposed on bank lending help to build a safety buffer for the banking system and therefore the New Zealand economy. This means that interest rates would possibly need to rise in New Zealand above 7% before creating serious problems.

Meanwhile, residential property prices continue to rise, although that increase appears to be mixed across New Zealand and is slowing down in some areas but continuing to boom in others. For example, Canterbury has seen prices increase strongly in the last quarter as though it is catching up with the rest of the country after years of sluggish growth compared to faster price increases elsewhere.

The Global Economy

Global Economic Growth

*The above table shows economic growth (contraction) over 2020 and projections for 2021 and 2022.

Global economic growth looks reasonably solid as the global economy emerges from the coronavirus pandemic recession. Although you never know what’s around the corner, at the moment, things look reasonably steady.

More specifically, as you know, I look for black swans (serious market and economic events that are difficult to see until they erupt). However, it is difficult to see one at the moment.

There are always grey swans swimming about, and these tend to be more obvious. The likes of supply chain disruption, rising interest rates, and those other items outlined above are what we often refer to as grey swans.

They may cause consternation across the markets and challenges for the global economy but are generally resolved at some point without causing serious problems.

The sceptics among us will add that central bank intervention has significantly helped to engineer the current environment. Still they are very unlikely to remove support for the global economy any time soon. Why would they?

Perhaps one interesting item ( a possible black swan?) that sits below the surface is a possible military engagement between China and the US over Taiwan.

Anyway, the American economy appears to be growing steadily. The Chinese economy is growing fast but slowing to a more moderate pace. The European economy is growing, although not fast, but growth nonetheless is underway across Europe generally. Japan is growing slowly.

Increasing labour costs worldwide and supply chain constraints are headwinds to economic growth in the immediate future. A reversal of monetary and fiscal policy support will create headwinds in the future as well.

On the other hand, pent up demand helps support short term growth.

In the meantime, the race is on to roll out the coronavirus vaccine across populations worldwide so that the virus can be contained, and the pandemic recession can be ‘kicked into touch’ once and for all.

Of course, we all know that we’ll likely be living with this virus for a long time. From an economic and market perspective however, we appear to be heading down the right path.

The United States of America

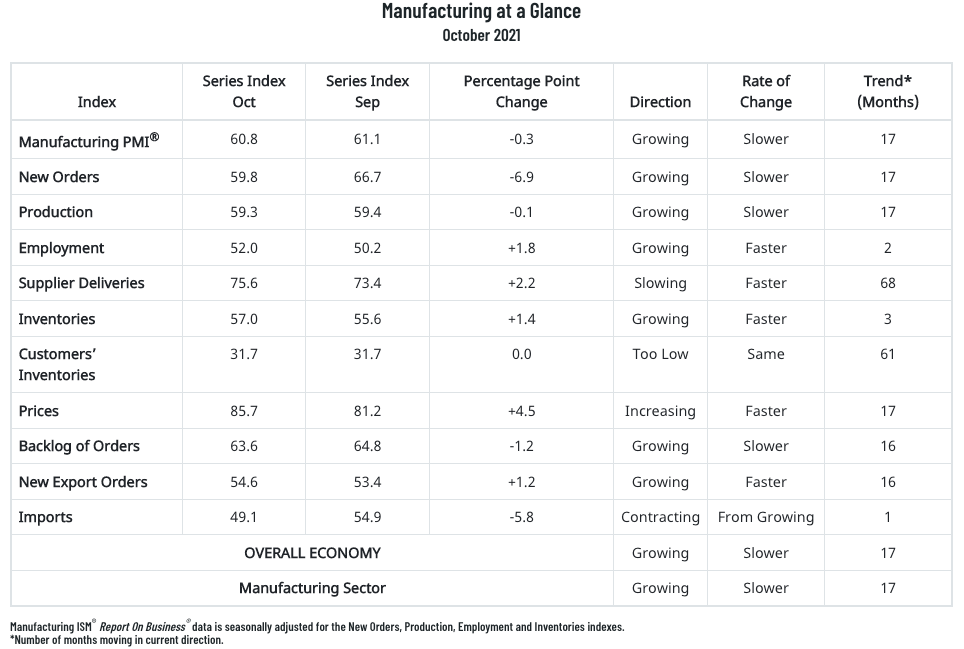

Manufacturing – USA

The above table tracks manufacturing in America.

Manufacturing in America is back. As mentioned elsewhere though, we’re not seeing much easing of pricing and supply chain pressures, which remain a headwind for economic growth.

Notably, the six largest manufacturing industries (food, beverage, and tobacco products; computer and electronic products; chemical products; fabricated metal products; petroleum and coal products; and transportation equipment in that order) all registered moderate to strong growth over October.

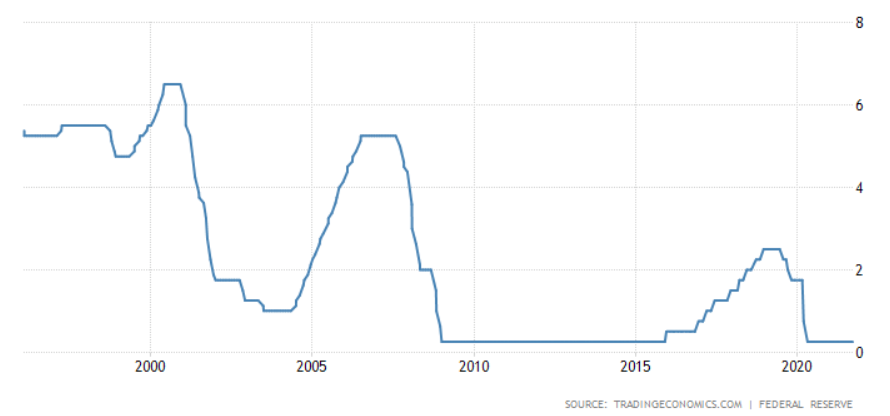

Interest Rates – USA (The Fed Funds Rate)

The above graph tracks the Federal Reserve Funds interest rate prior to 2000, to date.

The US Fed has just begun tapering, although they believe it is too soon to start raising interest rates.

The Fed points to supply bottlenecks that are still creating problems for economic activity, and by some measure, this has deteriorated more recently. The Fed believes that wages inflation growth is high but will likely last until 2022 and then subside.

They also added that if they see inflation pressures persisting, “we will use our tools”.

To me, that suggests that whilst, part of inflation pressures at the moment are transitory, they also go along with the idea that some inflation may not be transitory and flow through to 2022 and beyond. That, of course, can be a trigger for higher interest rates.

China

Manufacturing – China

The above graph tracks manufacturing in China.

The Chinese economy continues to grow strongly, particularly when compared to other economies. However, that growth is slowing. The crackdown by the Chinese Communist Party is one reason.

They have been looking to redistribute the wealth away from ‘the greedy capitalists and billionaires’ to everyday citizens across China. This action has hurt some well-known large businesses in China (e.g. Alibaba, Tencent).

Another recent issue that has emerged is what some are calling an energy problem (the media use the word crisis, of course). Simply, pent up demand has seen demand for Chinese goods surge. In order to manufacture these goods, energy is required.

The demand for energy is significant to the extent that some parts of China have seen power shortages and even black-outs. There have been isolated instances of traffic lights not working, sometimes causing traffic jams and people occasionally being caught in lifts that stop because power is cut off.

To be clear, the Chinese economy is not being brought to its knees because of the power ‘crisis’. This significant demand for energy though, has stretched resources.

Interestingly, electricity prices are regulated in China and some electricity companies are losing money as they generate a significant amount of energy for their end-users.

This energy shortfall will likely dissipate in due course but right now appears to be a real problem for manufacturing in China.

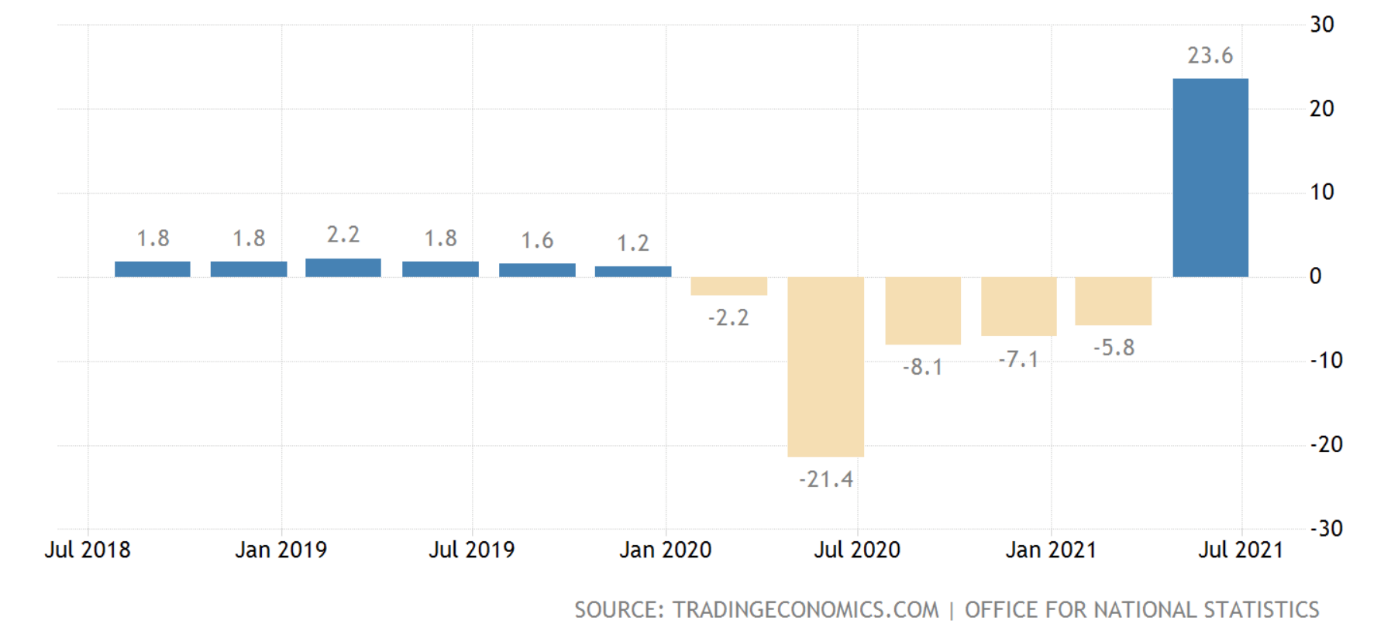

The United Kingdom

Economic Growth – UK

The above graph tracks economic expansion (contraction) in the United Kingdom.

The above graph is very strange-looking. It demonstrates how challenging the coronavirus and the resulting pandemic recession has been for the British economy. Part of the challenge was / and remains Brexit. By the way, the level of economic growth (as measured by GDP) is now 3.3% below where it was pre-pandemic.

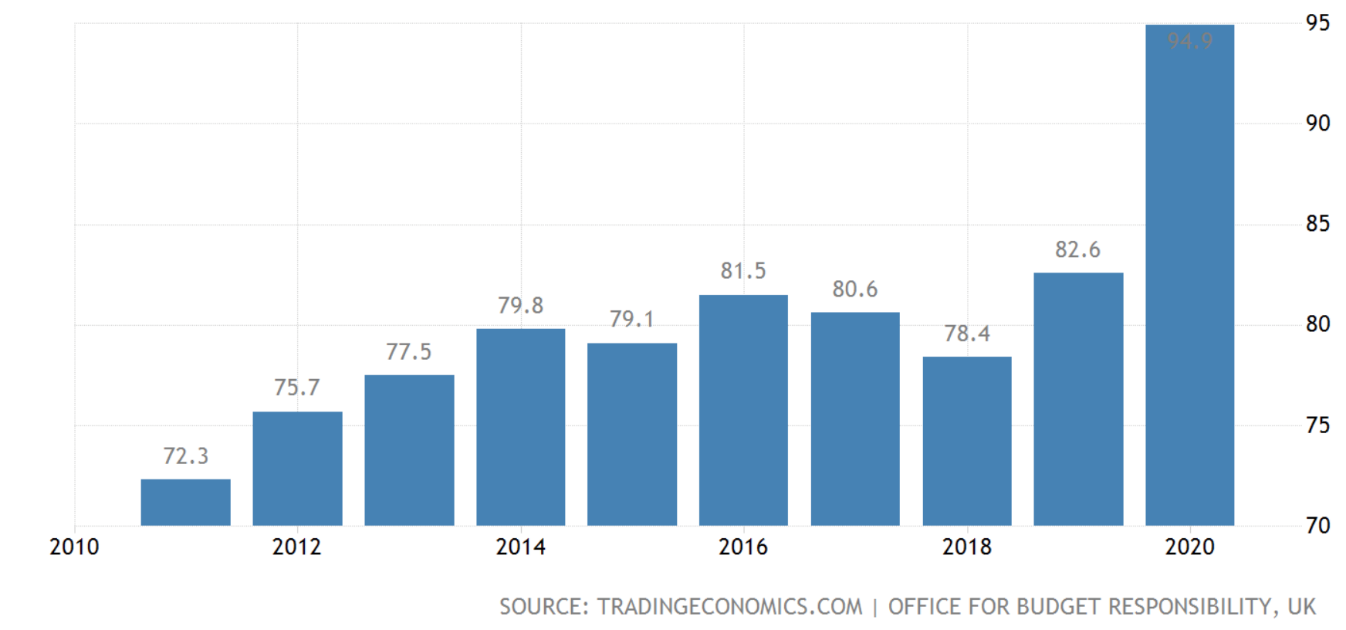

Public Sector Net Debt To GDP – UK

The above graph tracks the net public sector debt compared to economic growth as measured by GDP. Net debt is approaching 95% of annual economic activity.

As the chart above shows, debt funding has increased markedly as a result of the coronavirus.

There has also been some talk about the Delta+ strain of the virus. However, that is not widespread and so far not an issue.

The real risk, of course, not only for Britain but the global economy as well, is the emergence and spread of a virus like the Delta virus that becomes difficult to contain.

The real point here is that balance sheets, incomes, and individual mental wellness have been impacted across the globe as a result of the coronavirus so far.

A second round of the virus similar to the first one is almost not a thought that I would want to hold for too long. It would see levels of debt skyrocket from already high levels for most countries, and whilst some people would be hardened to the environment, others might be damaged and find it difficult.

And then, with every crisis of magnitude, there are the winners and the losers.

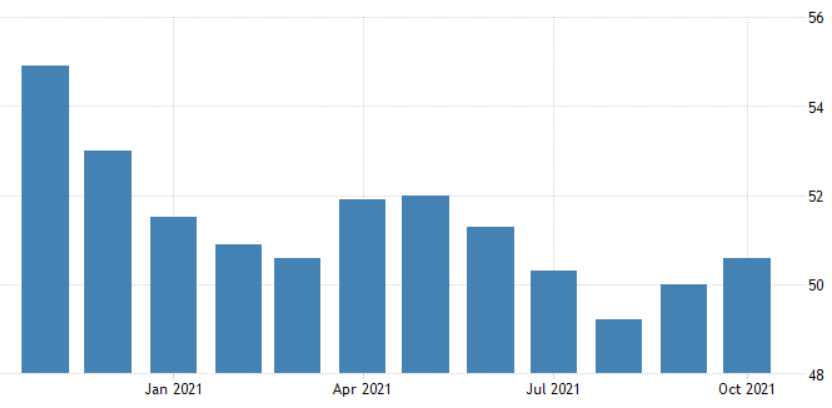

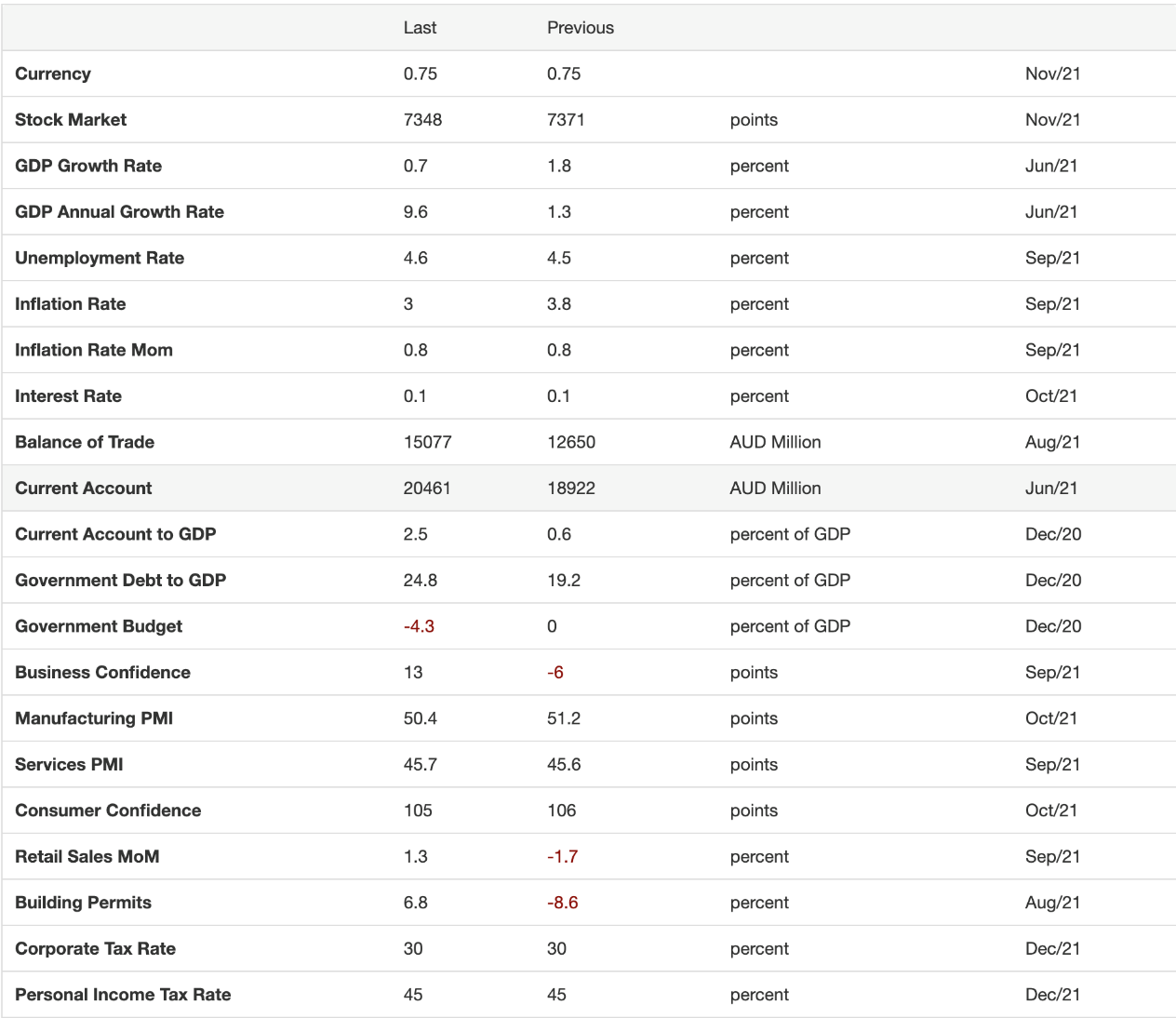

Australia

Economic Indicators – Australia

The above table provides a variety of economic data across the Australian economy.

The Australian economy continues to grow, despite its ongoing spat with China. Also, the coronavirus has spread significantly across Australia, causing severe restrictions and lockdowns.

Looking at the table above, we can see that unemployment is sitting at around 4.6%, inflation around 3%, and interest rates around 0.1%. Manufacturing is positive at 54%, whereas the contribution to economic growth from services is contracting, showing a score of 45.7. A number below 50 means contraction.

However, with the recent arrival of the first airliner from the United States to Sydney, at this stage, it looks as though they might be heading down the other side of the coronavirus mountain.

Note the personal income tax rate at 45% at the bottom of the above table – how would you feel about that?

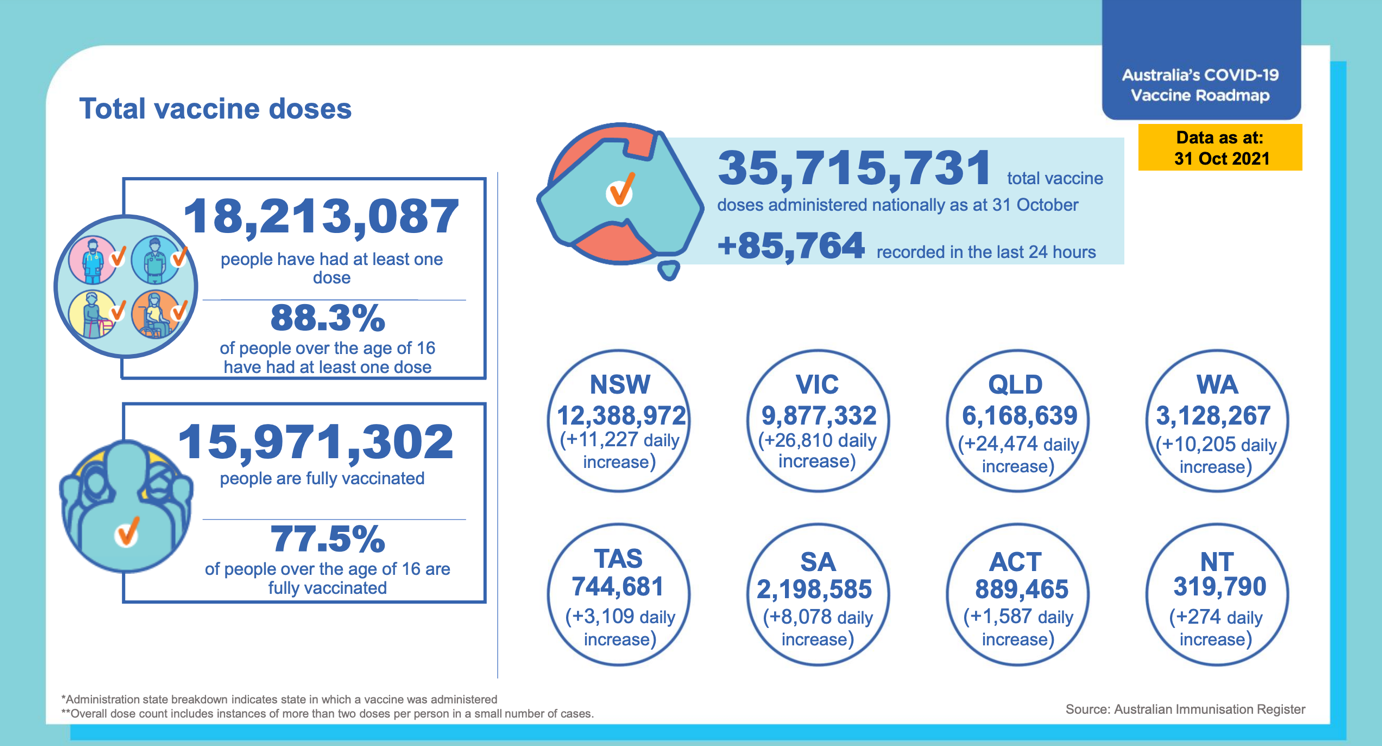

The above infographic shows single and double vaccination rates across Australia as well as the state-by-state number.

So, Australia is reducing restrictions in some states in favour of getting things back to so-called “normal”. Will it work, or is it too soon?

If we look at the experience of the likes of the US and the UK, whilst it’s too early to be sure, the current evidence suggests that it might work as the high level of vaccination rate and importantly, the building natural herd immunity combined together help contain the spread of the virus. Fingers crossed for the Aussies because, that means in due course, we can interact and trade more with them, which is good for us all economically.

More specifically, Australia is opening up to returning Australians and from the 21st of November this year for fully vaccinated travellers from Singapore, the second country after New Zealand that they have opened up to. Those travellers from Singapore can enter the states of New South Wales and Victoria without having to quarantine.

Singapore has announced it will allow travellers from Australia and Switzerland to enter from next week, which adds to their list of 9 other countries (Canada, Denmark, France, Germany, Italy, The Netherlands, Spain, The United Kingdom, and The United States). I understand that Singapore has opened up “vaccinated travel lanes” at border control. Although some will disagree with me, personally, I’m not sure I would be keen on walking up the unvaccinated travel lane – what do you think?

New Zealand

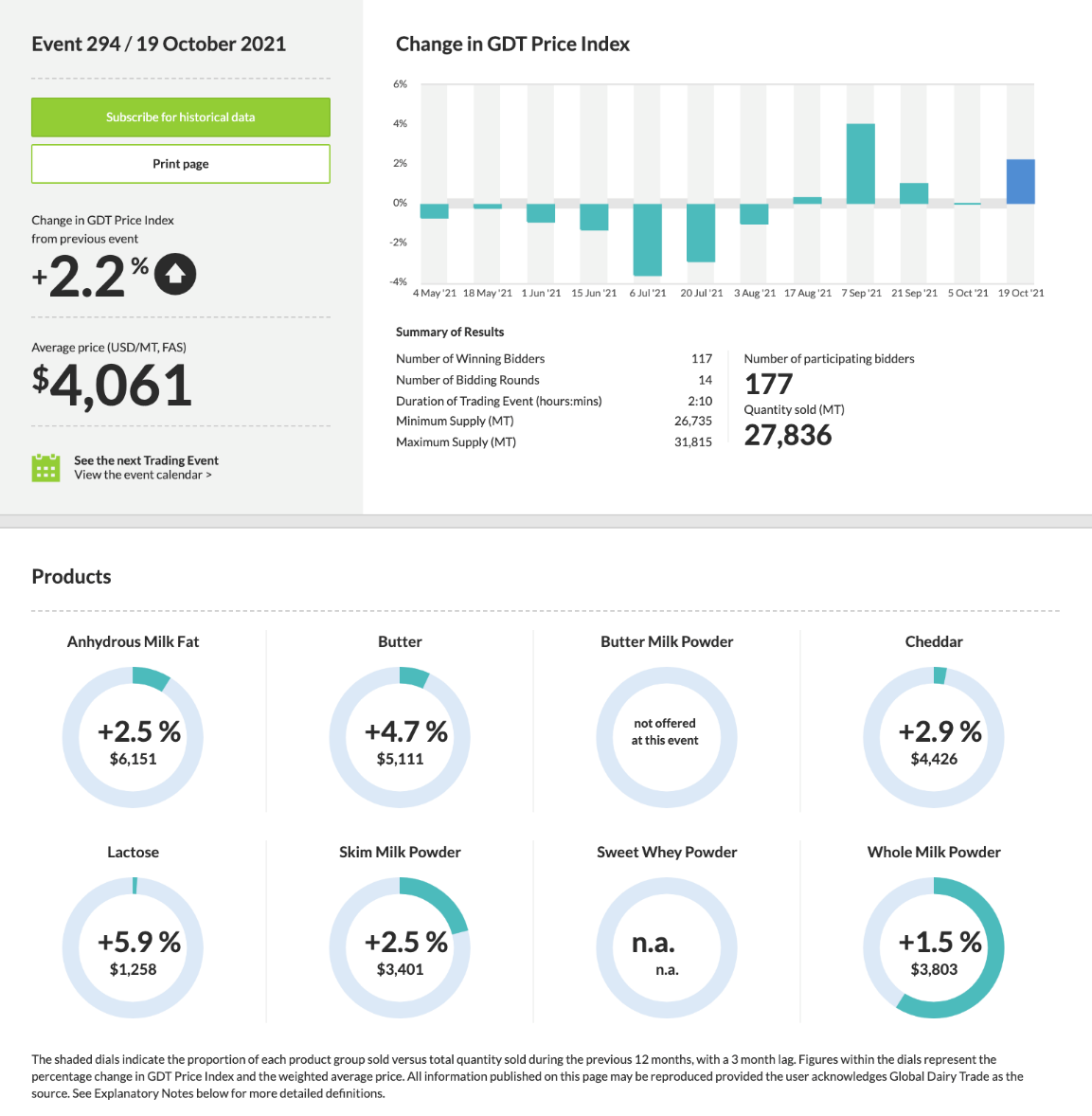

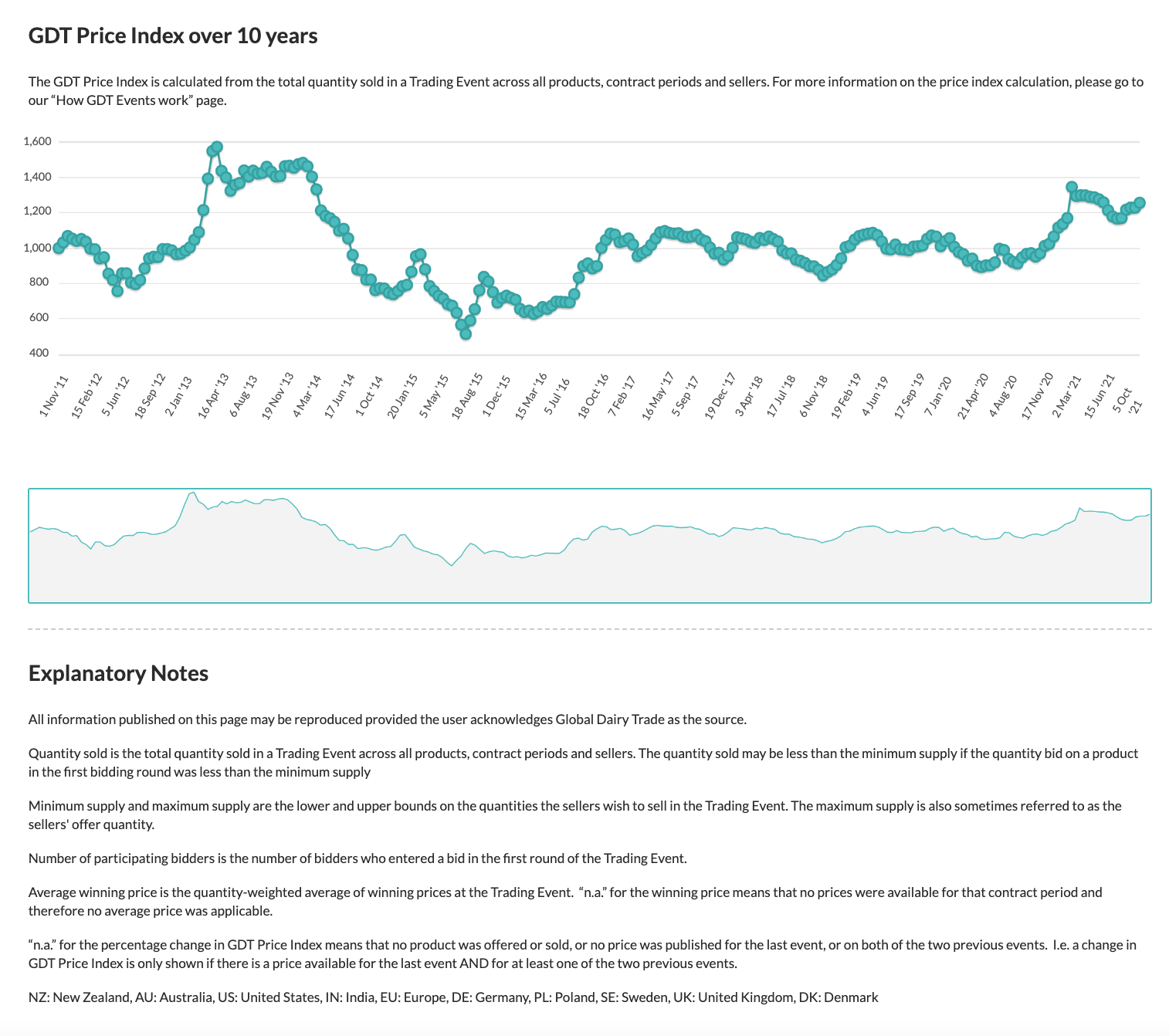

The Global Dairy Trade

The above tables and graphs provide a variety of information from recent dairy trade auctions.

The New Zealand economy is tracking reasonably well, all things considered. I know people are generally tired of hearing about the coronavirus and the Delta strain. Unfortunately, it’s far from over. The good news is that we are heading in the right direction, all things equal. Especially if the international experience is anything to go by.

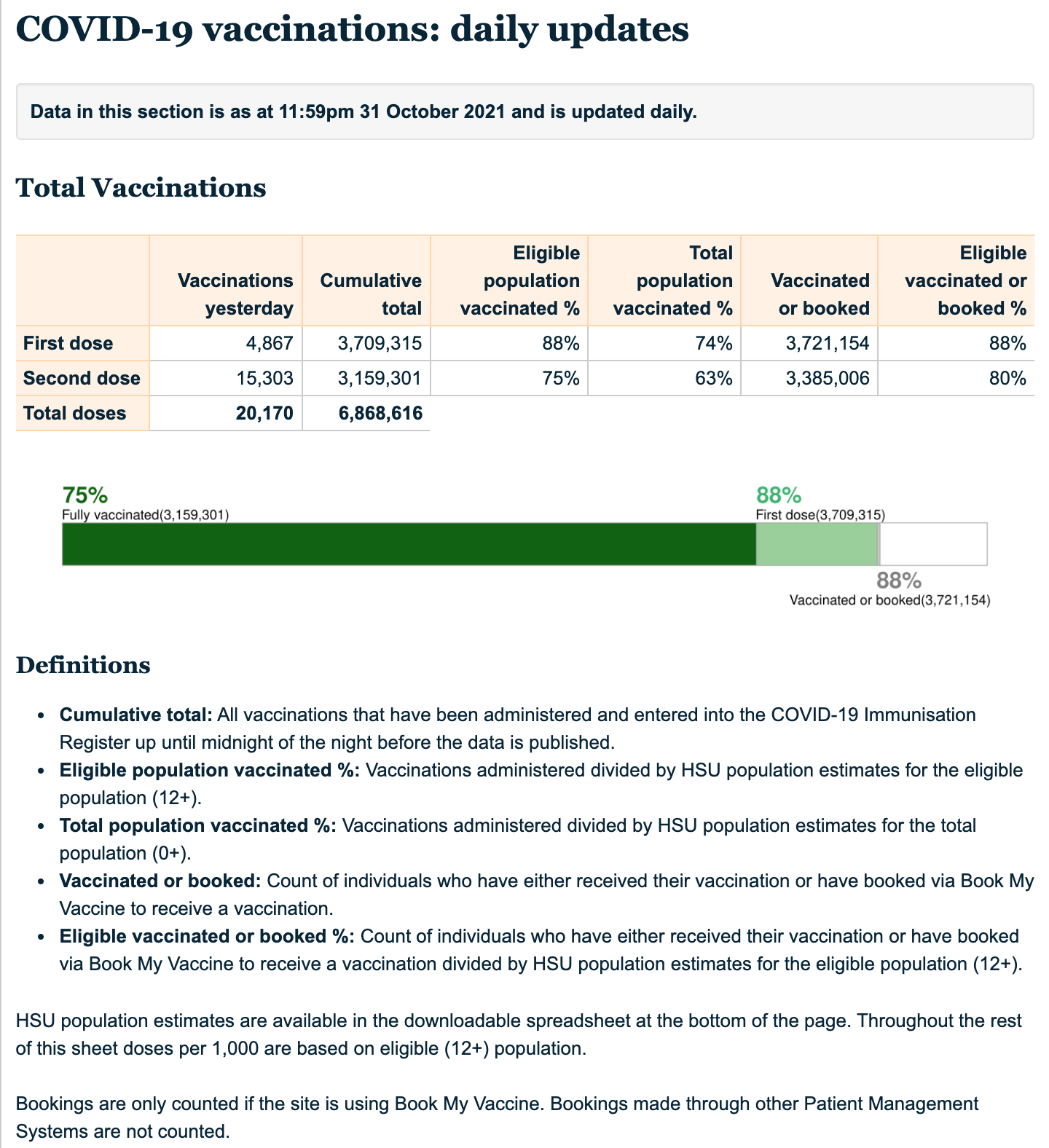

The above graphs indicate vaccination rates across New Zealand.

Of course, we can complain that we’re behind where we should be, which might be true (annoyingly!).

At the same time, we are heading down the right path, although I would like it to be faster (I’m not saying that I am for or against vaccinations). I would put myself out there and say that I am for economic growth, minimal pain and suffering for people and maximising opportunity. Sure, some have benefitted from the impact of the pandemic recession but it hasn’t been good for everyone, though. I know… life is not like going to kindergarten. Life is not always fair.

I’m no epidemiologist but, looking at the experience of other countries such as the US and the UK, I suspect we may see the Labour government in New Zealand move away from lockdown restrictions (whilst taking advantage of them as much as they can) as the feeling among the people is becoming more vocal by some factions against ongoing lockdowns. They run the risk that it could become politically challenging for them, and they won’t want to go there.

I suspect they will rely on an increasing vaccination rate (as in double vaccination), and they will continue their campaign up to around 90% or so (although, in my opinion, 95% would be a better idea). That’s because even 5% of New Zealand’s population is thousands upon thousands of people wandering around with a greater possibility of winding up in hospital, creating problems for the hospital system, but more importantly for those citizens who have other health issues that present acutely requiring serious care. That said we need some herd immunity to push back against the virus. If we are all vaccinated, there is no natural resistance against the virus – not good.

Anyway, everybody is entitled to healthcare in New Zealand. Is it right that someone who chooses not to vaccinate takes one bed over somebody vaccinated but requires other urgent treatment?

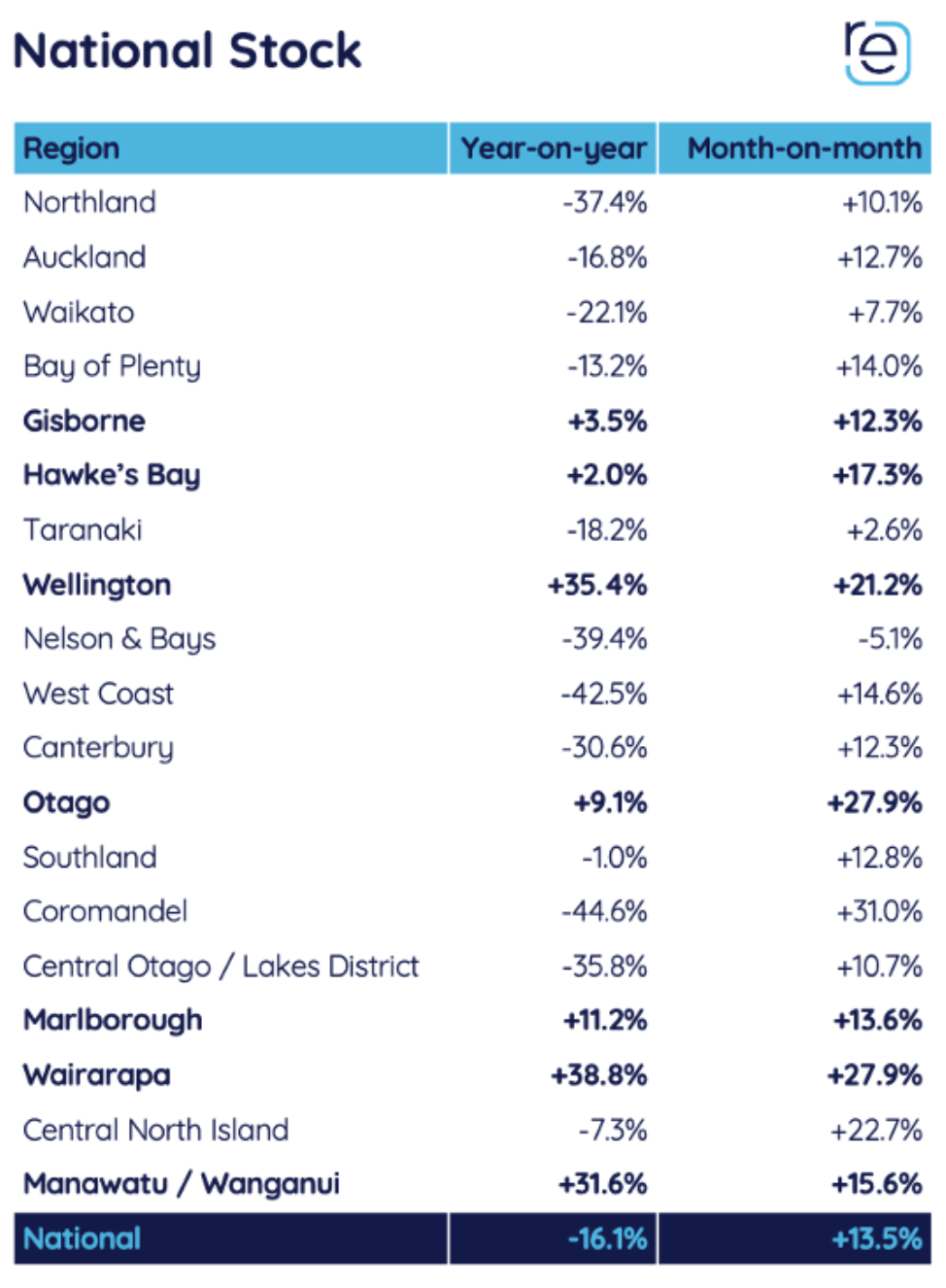

Residential Property

The above table shows the year-on-year movement in the amount of housing stock across New Zealand as well as the change over the last month.

Housing stock declined by 16.1% over the last 12 months but is up by 13.5% over the last month.

It’s difficult to know whether that’s a signal for future increases in property supply, but nonetheless, it is a step in the right direction. Although it’s not easy to know for sure, however, it could also be that there are more listings making more property available.

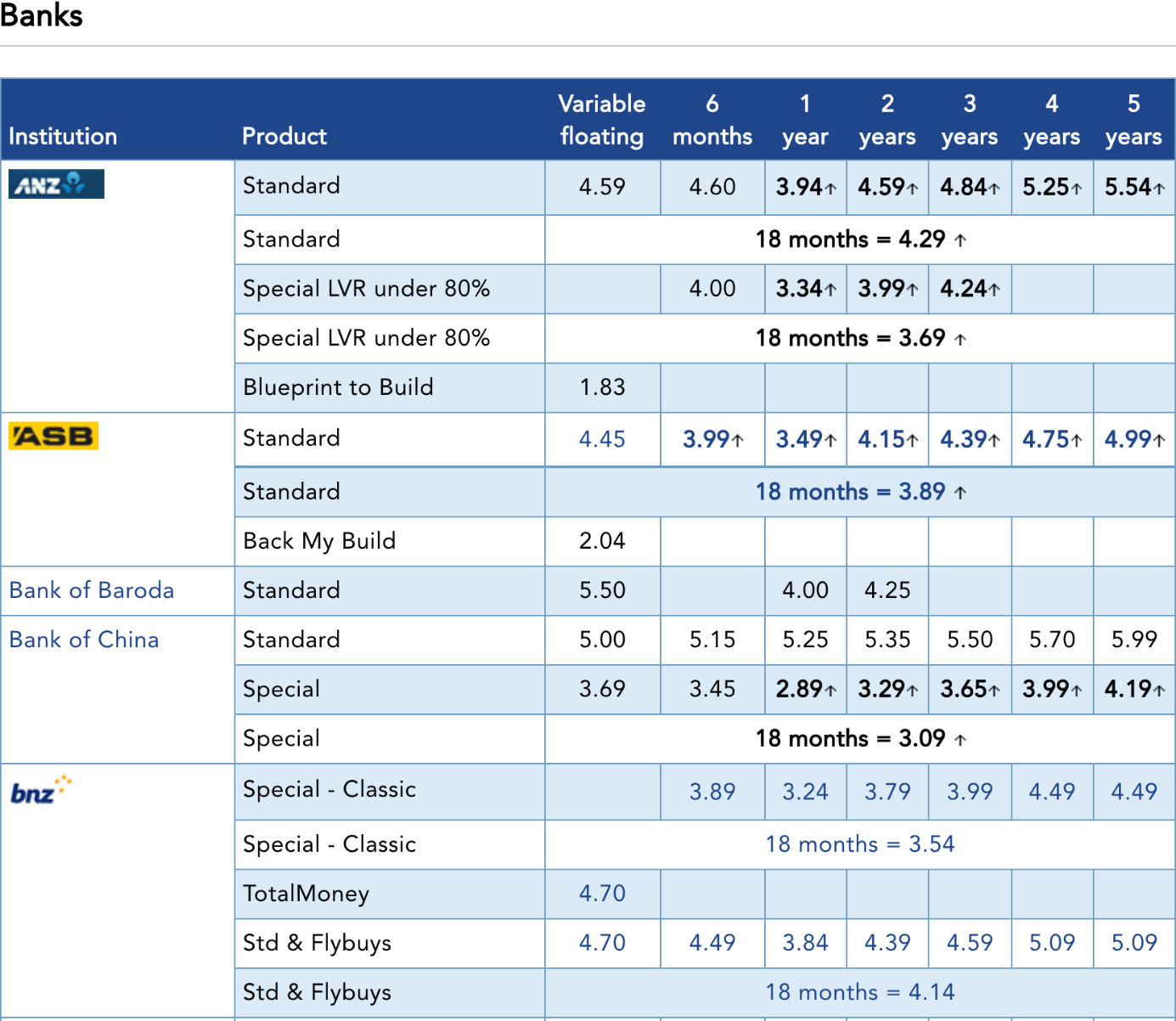

The above two tables show mortgage interest rates (the top table) and term deposit interest rates (the bottom table).

Interest rates are rising. It’s a question of how far they will go.

It’s difficult to see anything like double-digit interest rates in New Zealand and other parts of the world anytime soon.

For investors, though, rising interest rates may cause some anxiety. That, of course, means volatility and our opportunity hopefully, for some better buy prices.

Currently, trading prices in most countries around the world are expensive. That’s why in general terms, we’ll be generally sitting tight on our portfolios rather than allocating money to expensive businesses in the hope that their trading prices will continue to rise (as per the noisy market narrative).

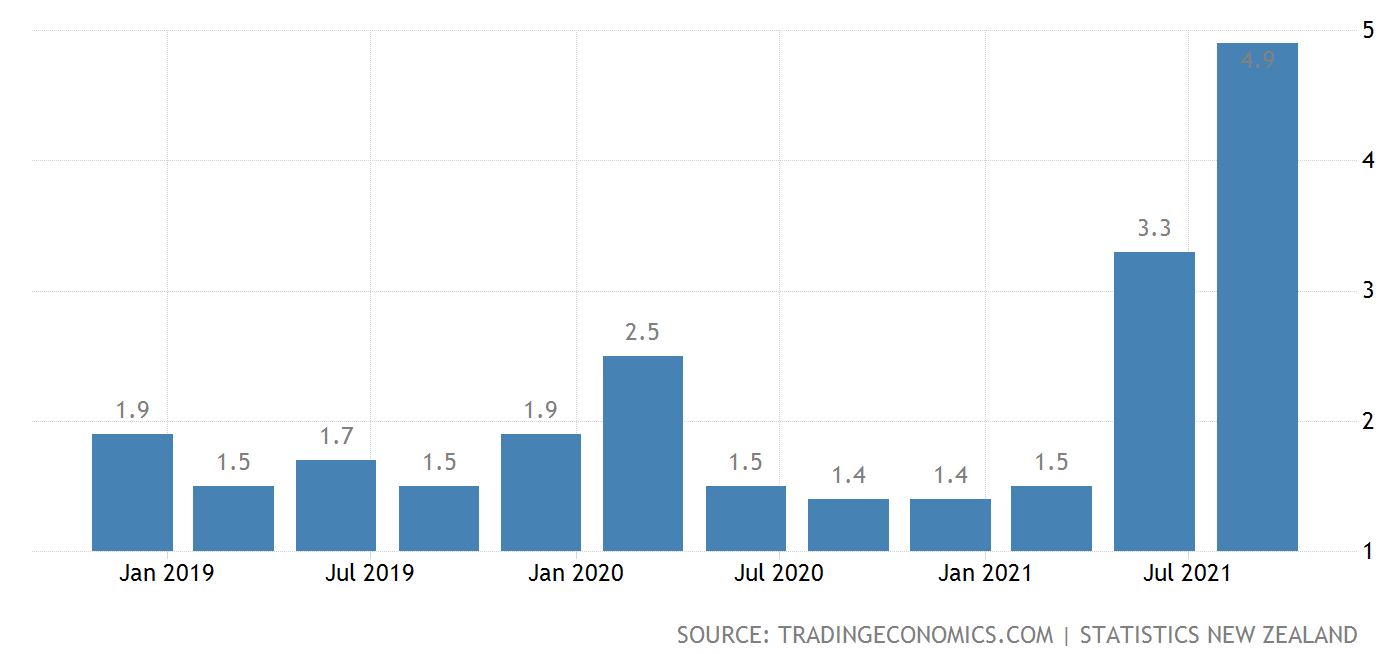

Inflation – New Zealand

The above graph tracks the annual inflation rate in New Zealand.

I included the inflation rate graph above, so you could easily see term deposit rates and the inflation rate, one on top of the other for easy comparison.

In short, by the time you take tax off your interest rate from term deposits, then deduct inflation (the rise and cost of goods and services), there isn’t much left for you, the investor.

Indeed, with inflation spiking, it’s quite possible that if you have term deposits and you’re relying on them for income, you may well receive a dollar amount of income from your term deposit. Be careful, though in thinking that interest payment is real money.

To be clear, it’s fake money because the cost of goods and services is increasing as we speak.

The moral of the story is, invest for growth and income – not just income, when you are looking for passive income.

No need to invest for income if you’re just looking for growth. That’s where we focus on quality businesses and possibly Small Caps that may offer faster growth in the overall market longer term, providing you are comfortable with a more advanced investing strategy.

To Summarise …

The global economy continues to grow as it emerges from the pandemic recession.

We’re not there yet. Indeed, there’s quite a long way to go, particularly when you take into account emerging and developing economies that are much less well-positioned than more developed Western economies to rollout vaccines in order to help control the virus.

Likely, those without the vaccination tool will see the virus flush through the population to inevitably, hopefully, build herd immunity.

Markets and trading prices remain expensive. This doesn’t mean automatically that we’re in for a share market crash.

It does mean that when an event emerges, particularly one that is unexpected, we could see potentially, a sizeable decline in trading prices.

Over September, the volatility that we saw was around 5%, as measured by the Dow Jones and other share market indexes – not enough to get us excited.

That said, interest rates will likely continue to increase, although possibly at a measured pace. The US Fed, for example, has continued to confirm that interest rates won’t be rising until the latter part of 2022 and over 2023.

Without being too boring about it, quality businesses are the key to sustainable, secure investing over time. The smaller the business and the lower the quality, the greater the risk.

As a final note, when carrying out my analysis from day-to-day, looking for good businesses in which to invest, there is a clear trend showing that some of those smaller fledgling businesses that fly below the surface offer potentially spectacular returns in the long run.

However, their financials and their economics look, well, straight out ugly. They are a game of chance—a bit like Bitcoin.

I am neither for nor against Bitcoin. It may well prove to be a spectacular investment for investors. However, it remains a game of chance. As one of my clients recently mentioned, it shows all the signs of the so-called “mousetrap”. Time will tell.

In the meantime, though, I suspect the noise around Bitcoin, and other cryptocurrencies will become ever louder as the trading prices continue to soar to lofty new heights creating real FOMO for those sitting on the side lines.

I’m not sure about you; however, whilst a little bit of dabbling is something that I know some of my clients love to do (they can’t help themselves), I prefer certainty and to allocate my time and my life to things more important than playing the markets.

Speculators sometimes make huge amounts of money, which is why we read about them across the popular media and on the internet.

Again though, whilst you can make your own decisions around Bitcoin and other speculative investments, when we look over time, it’s increasingly obvious that it’s not that simple to just jump on the bandwagon of the latest fad and readily achieve investing success.

It could happen, and maybe Bitcoin or some other cryptocurrency is just the vehicle. On the other hand…