Rising Interest Rates, War And…

Monthly Market and Economic Update – March 2022

Peter Flannery Financial Adviser CFP

“If you have one economist on your team,

it’s likely that you have one more than you’ll need.”

Warren Buffett

Key Points:

- The blindingly obvious – volatility is here, now.

- Is volatility a risk or opportunity for you?

- How will war impact markets moving forward?

- Where to with interest rates?

- What is happening with oil?

THE MARKETS

Where to from here for markets?

First, it was inflation and then concerns about rising interest rates over January this year.

Now we have Russians invading Ukraine.

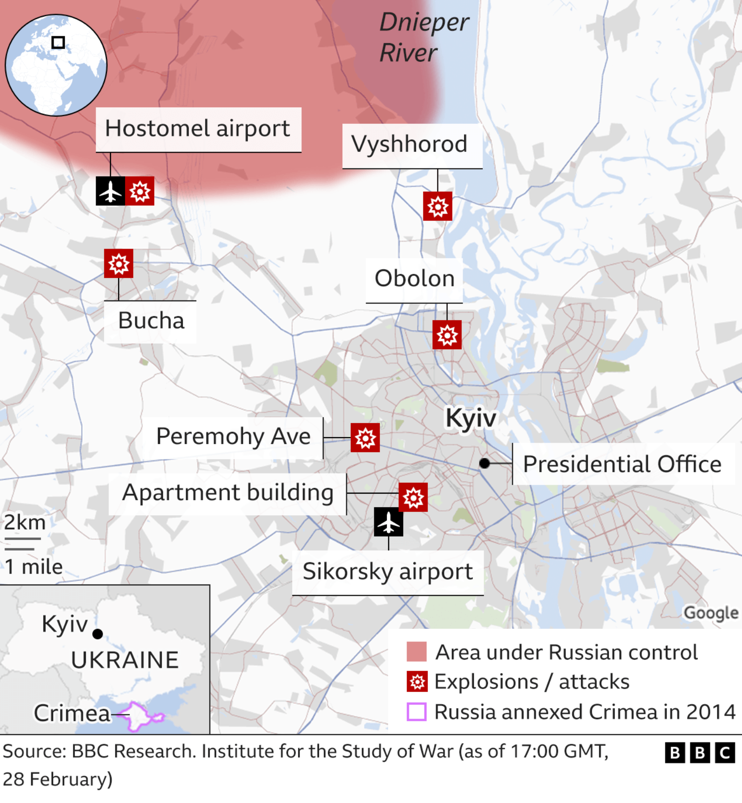

The above map shows areas under Russian control, including Crimea, which was annexed in 2014 by Russia.

So what does this mean for portfolios right now?

We can debate whether Vladimir Putin is a madman. However, he seems determined and probably believes he is right.

He will have thought this through, mapped it out, and is now executing his plan. The Ukrainians though seem at least as determined.

Interestingly, Joe Biden the US President, stated early in the incursion that America would not be getting involved with troops on the ground in Ukraine.

It’s difficult to know, but that might have been a vailed warning to Putin to carry out the incursion keeping humanitarian considerations at the forefront, and America will let them be (aside from, perhaps, some behind-the-scenes support via Europe).

My information suggests that Putin will not want to go to war with America. It would seem unlikely that the incursion into the Ukraine is much more than Vladimir Putin wanting to take back control over what was previously Russian-controlled territory. No guarantees on that; however, that’s how it looks.

The above map highlights key cities in Ukraine, hot points where attacks and explosions have taken place, along with the location of key airports.

Although I won’t take up space showing it here, Russia can strike from the North, the East, and the South, or all of the above.

Ukraine is outmanned, outgunned, out-tanked, and inevitably, depending on how it all unfolds, one would expect Russia, one way or another, to occupy Ukraine. The Ukrainians, however, appear to be putting up a valiant fight so far.

The above photo shows part of a long convoy (actually 65 kilometres by some reports) possibly heading to Hostomel Airport. Hostomel Airport, to the West of the capital, has seen some fierce fighting and appears to have changed hands a few times from one side to the other over the last few days (beginning of March).

So far, Russia appears to be engaging in a surgical operation, taking out key strategic assets with limited loss of civilian life so far, but that could change.

But what about nuclear risks?

As you may know, Vladimir Putin signalled a few days ago that he has placed his nuclear force on high alert. Again, it’s difficult to know what that means as to whether it is definitely part of the strategy (unlikely) or whether it is more sabre-rattling to convince America, NATO, and others that they are deadly serious about their goal of returning Ukraine back to Russian control.

Perhaps the real risk is down the chain of command, if there is a misunderstanding or a misstep that leads to an accidental firing of a nuclear missile. Although again, that would seem unlikely.

Throughout the Cold War, there was a significant intelligence machine watching Russia, and it would be interesting to know how much of this remains in place. I suspect most of it. After all, Russia still has nuclear weapons.

Although again, it’s difficult to know for sure, the consensus appears to be that at this stage, the risk of nuclear missiles being fired is low. America for example, has stated that they have not changed the status of their nuclear arrangements known as DEFCON.

Putin can’t have it all his way.

There are some other considerations as well.

For example, many NATO allies are some of the largest importers of Russian gas and oil.

If there was a war with NATO, then Russia would likely lose access to the European market, and this would be a major problem for the Russian economy, already under pressure from sanctions.

This way, America doesn’t need to get involved significantly or even fire one shot. Just cut Russia off from European markets and see how the Russian economy goes from there.

One of Russia’s most important cities is in the Baltic.

America could easily block aid to Russia, cutting off imports and exports from the Western Hemisphere.

I imagine that Vladimir Putin knows all of this, and he will have thought this through as part of his plan.

The question will be whether he has established limitations or points where he won’t go beyond in order to avoid the full force of the world’s anger.

Russia is large by land mass and has significant resources.

Their level of debt is low like New Zealand and so they can run up debt if need be to finance a war. That said, they are not in a position as yet (as much as they would like to be) to be able to trade and function easily without the rest of the world.

As I said, it is not a one-way street, and Vladimir Putin won’t get his own way with everything. The world is watching. It is taking action via sanctions that are already hurting the Russian economy.

Market Volatility (The Vix)

The graphs above (the Vix) measure share market volatility. Sometimes known as the fear factor. The graph to the left tracks market volatility year-to-date. The chart to the right tracks volatility over the last five years. The lines are green because volatility has increased.

When looking at those two Vix graphs above, you can easily see the spike in volatility March 2020 as the coronavirus began to spread. Interesting when you compare the levels of volatility with the coronavirus and Russia invading Ukraine.

In fact, we know that markets declined by around 30% in March 2020, whereas over the month of February, as the invasion became public knowledge, the market declined by only around 10% by comparison.

Anecdotally, I noticed that a number of our portfolios at WISEplanning have been flat over the last 12 months because of the volatility over January and February, with some showing gains over that time.

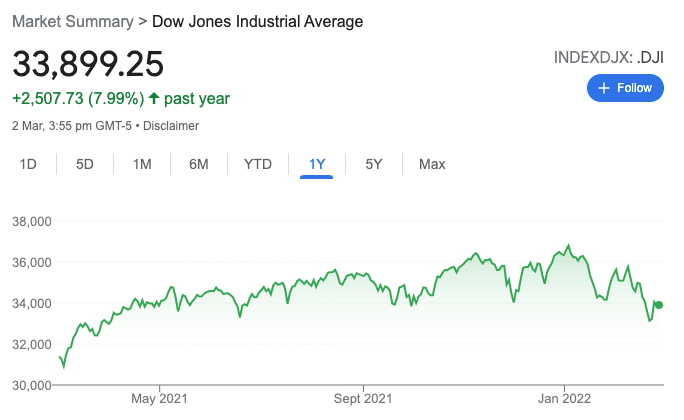

The chart on the left shows the US share market (the Dow Jones) over the last six months. The chart on the right shows the US share market (the Dow Jones) over the last year.

So, markets thought they had plenty to think about with spiking inflation and rising interest rates. The invasion of Ukraine was not on anyone’s mind until very recently.

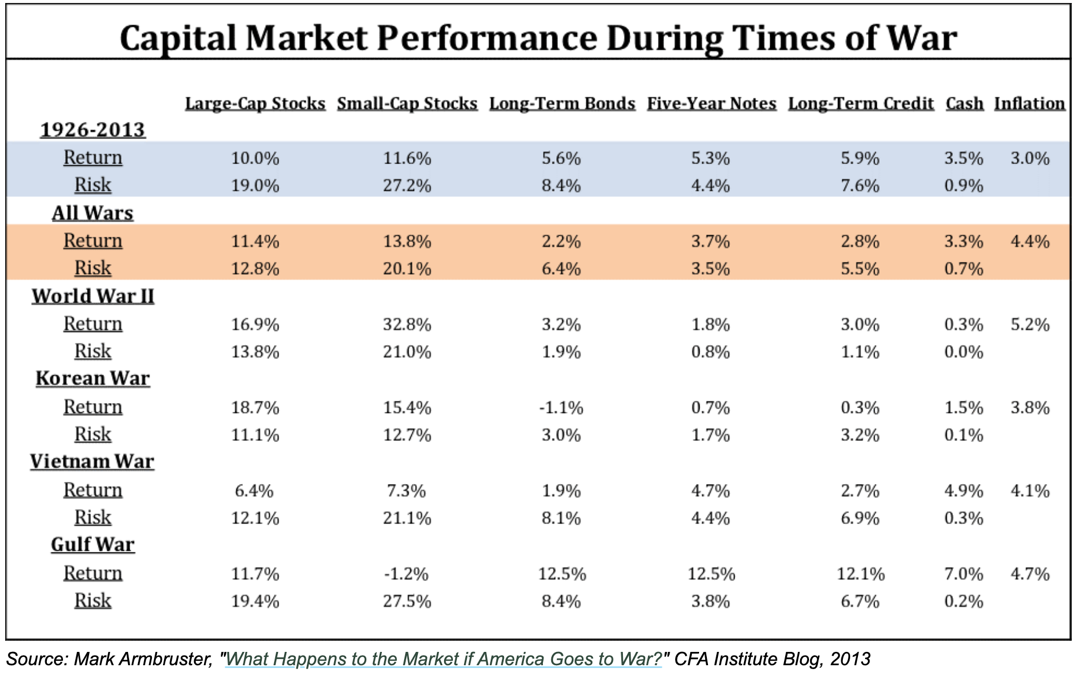

The above table compares different types of shares across the market, long-term and short-term bonds (fixed interest-type investments), cash and inflation.

Although the above table is a simplistic outline, and I wouldn’t necessarily rely on it as a guide to future performance, nonetheless, it is quite interesting when you look at it.

Note, for example, levels of inflation. At the moment, inflation is spiking globally due to supply chain constraints as a result of the coronavirus. There is though, an element of sticky inflation remaining. In short, inflation seems to line up with war it would seem.

What you’ll notice as you scan across the table above, is that markets generally finish higher at war’s end compared to when the war started. There is, of course, volatility in the middle.

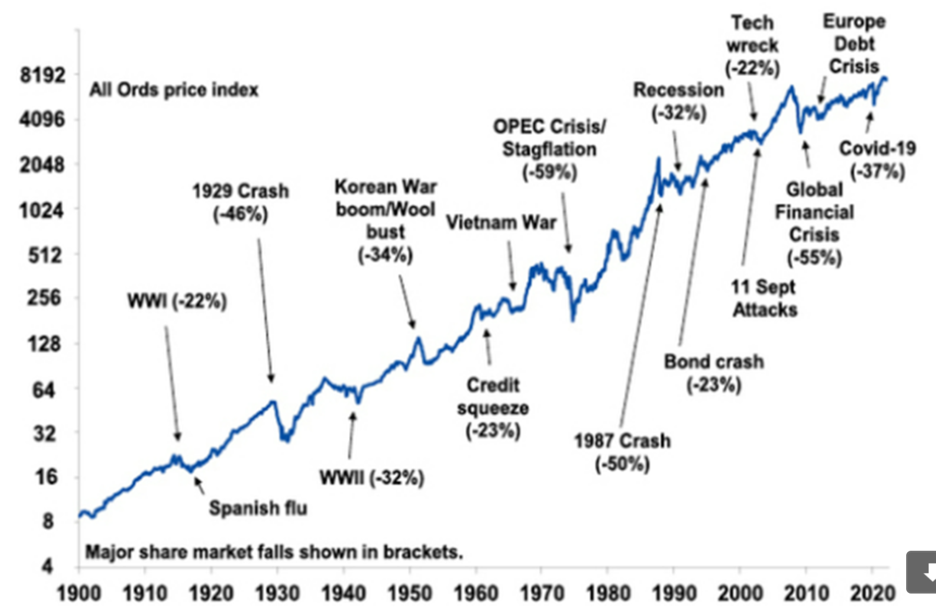

The All Ords Index (Australia) 1900 – 2020

The above graph tracks the Australian share market from 1900 through 2020.

This time, looking at the Australian Ords price index (the graph above), we can see the extent of trading price declines across the Australian share market as various wars unfolded since 1900.

So, where to for markets then?

It is difficult to predict market direction because it’s based on sentiment, and the market itself does not even know the answer to that question.

Stepping back though with some perspective, my view would be that if the Russian incursion takes its natural course, Putin gets his way with Ukraine, and there are minimal casualties, then it will be business as usual to some degree in due course. It’s difficult to know how long that might take.

In some ways, the better the Ukrainians are at warding off the Russians, and indeed the more stubborn they become, the longer it may drag on. Also too, I fear, the greater the risk that Vladimir Putin will become impatient and apply measures that will start to look ugly very quick. A challenging position for Ukrainians and I must admit, not easy to observe.

So as the battle reaches its conclusion at some point, markets may refocus on inflation and rising interest rates which, of course, won’t have gone away.

However, some argue that this may make the US Federal Reserve Governor Jerome Powell think twice before raising rates at the pace that was being considered prior to the invasion. On the other hand, a shortage of gas from Russia could push inflation upwards in Europe and possibly in other parts of the world.

It’s difficult to see a major share market correction if what’s going on at the moment continues down on the same path.

Expect more volatility though, as the market ebbs and flows from one day to the next and becomes somewhat directionless, particularly in the short term. Once some sort of direction starts to emerge, then the market I imagine, would be all over it and we may see trading prices rise in a more solid fashion as those uncertainties dissipate.

The Global Economy

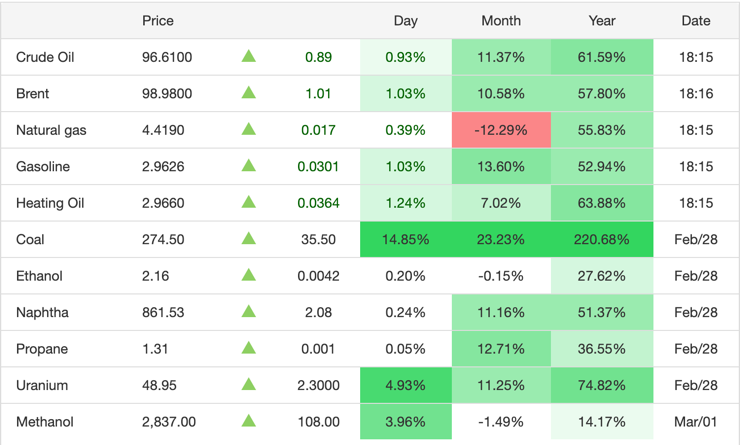

Oil

The graph to the left tracks the movement and the price of Brent crude oil over one year. The table to the right tracks the movement in oil and gas prices by day, month, and year.

Brent crude oil is a major benchmark price for purchases of oil around the world. Although Brent crude oil is actually sourced from the North Sea, oil production out of Europe, Africa, and the Middle East that flows to the West also tends to be priced based on this oil.

As you may know, the price of Brent crude oil has hovered around the $110-mark (as of March 03 2022). Traders are weighing up the possibility of the release of strategic crude reserves by America and its allies to counter the impact of sanctions against Russia on energy supply.

Russia of course, is one of the world’s largest suppliers of oil and gas and sanctions against Russia may have the impact of chopping off a large source of oil and gas. It’s worth noting that if that were the case, then this would also stop income from oil for the Russian economy – not ideal for Russia.

Large oil companies such as BP and Shell have also announced plans to exit Russian operations. In the meantime, OPEC will meet this coming Wednesday (as of March 1 2022) to discuss output policy.

OPEC has been considering sticking to their plan of moderating supply increases despite market turmoil brought on by invasion.

The above graph tracks the trading price of crude oil over the last 50 years.

You may remember back in the day when the media across the world was talking about ‘peak oil’ and the fact that one day, there might be none left. Again, if you’re old enough, you may remember petrol rationing in the 1970s. Back to the future… the reality is that the world needs oil to continue to function.

New forms of energy may well emerge (hopefully). However, right now, the simple fact is that the world needs oil. It also needs gas for heating.

The reason I mention it here is that rising oil prices can support rising inflation which, of course, can lead to pressure on interest rates to rise. Let’s watch this space.

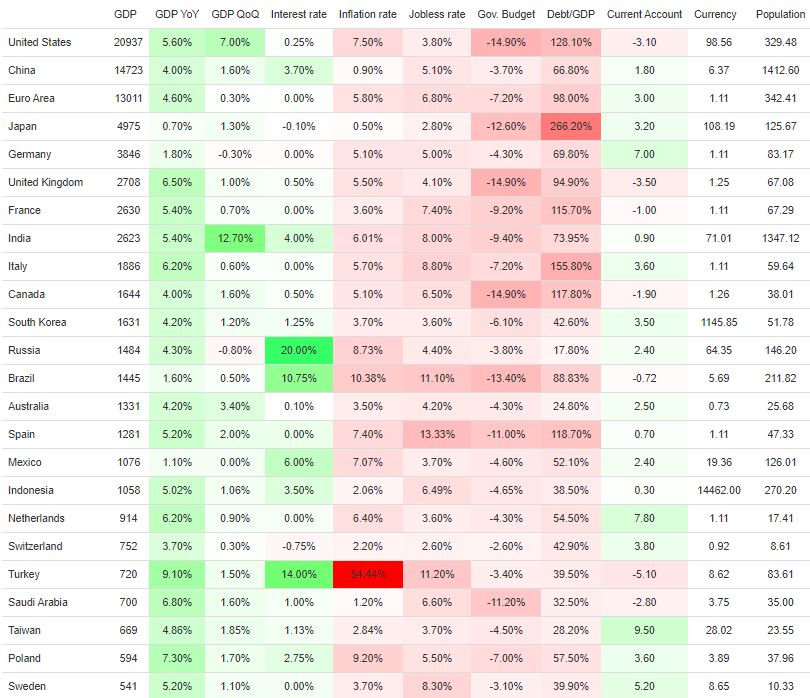

A quick look at the global economy

The above heat map provides a variety of economic data across a number of countries.

A couple of points worth noting (from the above heat map) is interest rates in Russia that have just doubled from around 10-20% (the dark green colour with 20% in it) and also their inflation rate alongside their interest rate at 8.73%. What’s interesting about that is this inflation rate number is before the impact of sanctions, a declining Russian rouble and other consequences of Russia’s decision to invade Ukraine.

They do have over US$600 billion of foreign reserves and relatively low debt at 20% of Gross Domestic Product. However, that strong position will be eroded quite quickly. Russia defaulted on its debt in 1998, by the way.

This brings us to another interesting point, is that one might think that if a large country like Russia defaults on its debt, then why didn’t the global economic system collapse?

You can see the answer when you look at the heat map table above, which shows Russia’s annual economic productivity, which sits at around US$ 1.48 trillion compared to say, the Euro area at $13 trillion, China at $14 trillion and America at a bit over $20 trillion.

The United States of America

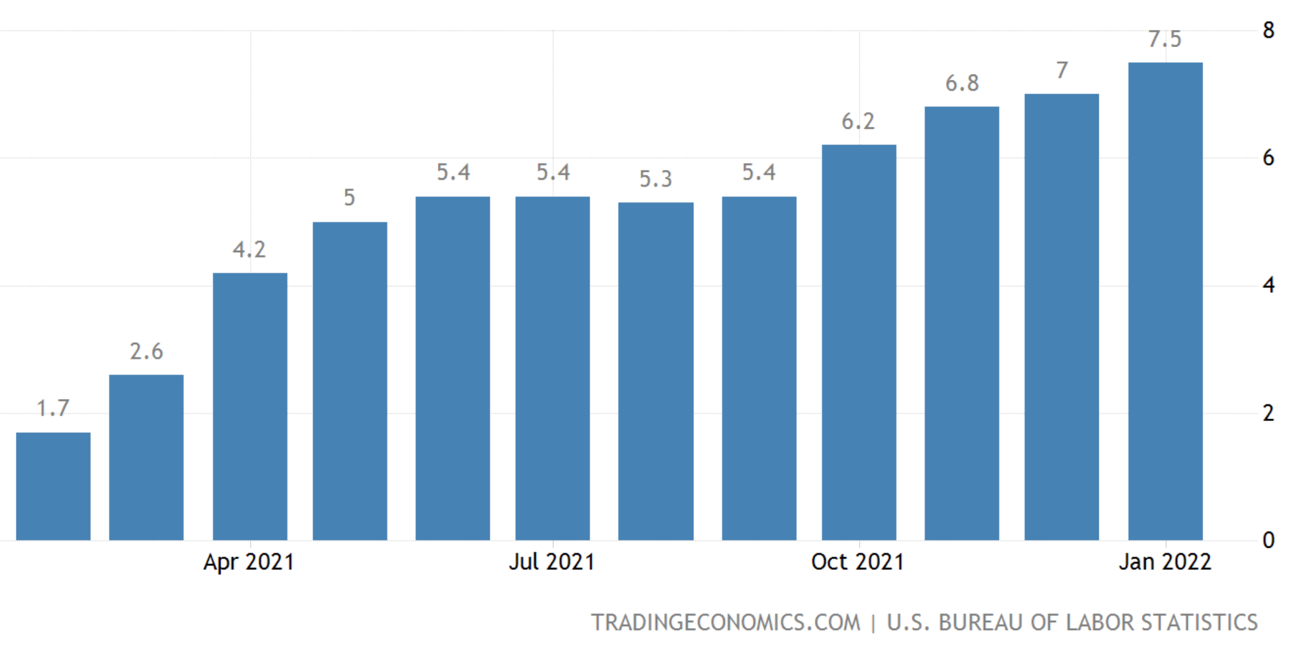

Inflation – USA

The above graph tracks inflation in America.

As the above graph shows, inflation has been steadily rising in America, particularly over the last year or so.

As I’ve mentioned elsewhere, this is partly due to supply-chain constraints and partly due to more permanent sticky inflation. The media are giving the US Fed a hard time by saying that Jerome Powell (Governor of the US Fed) has given up on the transitionary inflation narrative. However, I don’t believe that’s the case as he has commented that he sees the transitory nature of some inflation components as lasting for longer than expected but also the fact that other inflationary components such as wages growth are also emerging.

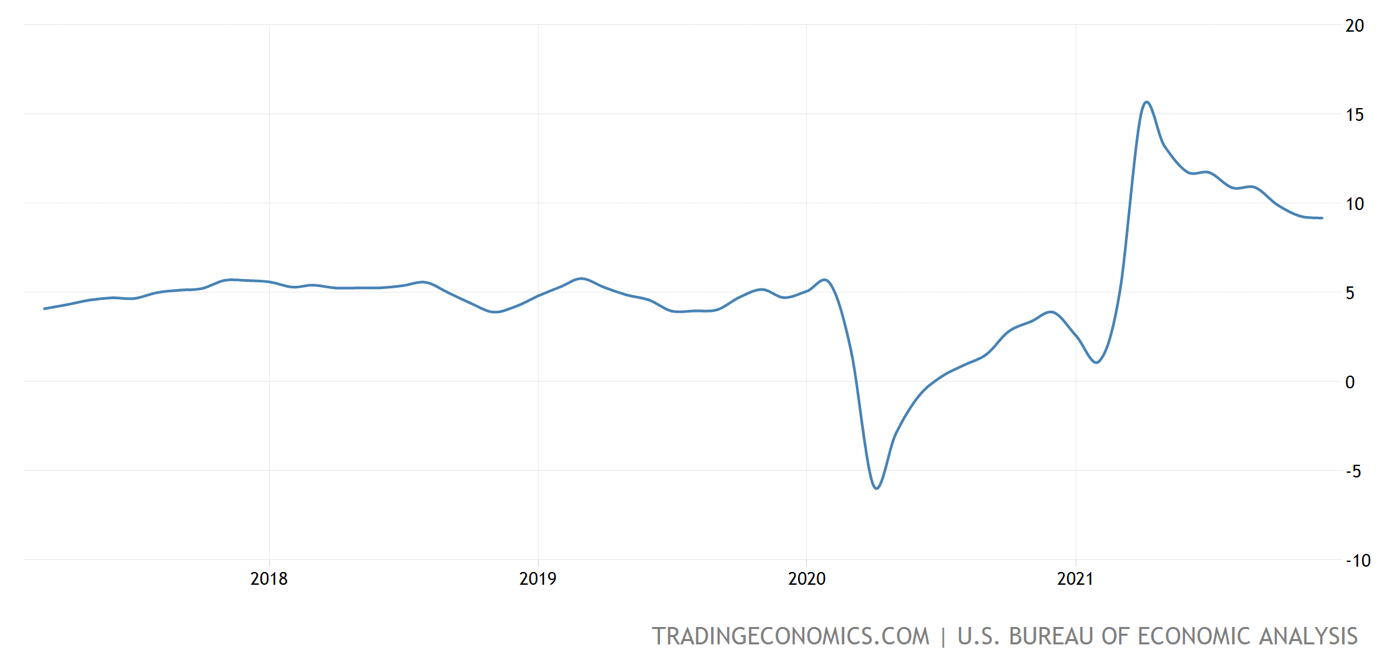

Wages Growth – USA

The above graph tracks wages growth in America over the last 5 years or so.

I mention wages growth here and show the chart to demonstrate that wages growth is tracking at a higher level than it has for some time. If I show you the 10-year graph, it looks surprisingly similar to the 5-year graph with that long flat line to the left (just much longer). The point here is that wages growth is tracking at a faster rate than for much of the last ten years, which signifies higher inflation ahead.

Do you know what that means?

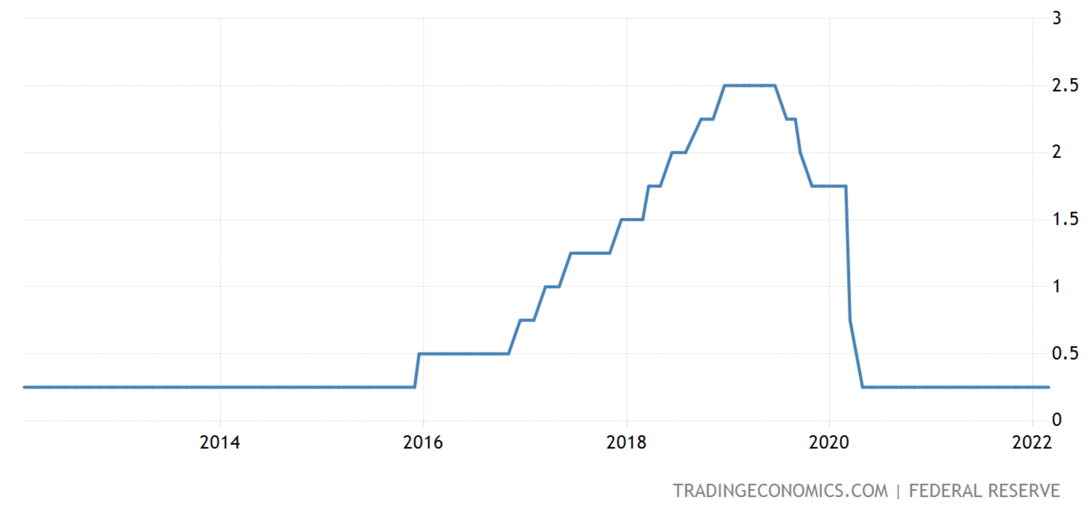

Interest Rates – USA

The above graph tracks the Fed’s funds rate in America.

Note the low flat line since the coronavirus emerged in March 2020. We can expect that flat line to the right of the graph to start sloping upwards.

Without a doubt, the talk around rising interest rates is loud and clear, and if you read my update last month, you would have seen the Fed dot plot showing the trajectory of expected interest rate increases.

There are some question marks now around whether the Ukraine situation may slow that down; however, I believe it could even exacerbate it.

Looking more closely at this, prices for wheat (Russia as the world’s largest producer) recently surged, as did corn. Russia and Ukraine together supply more than 25% of the world’s wheat and nearly 20% of corn exports (as well as 80% of sunflower oil). The point here is that this may cause some commodities to increase, which of course, drives food inflation.

As we’ve already mentioned, oil prices are on the rise, with Brent crude over $100 a barrel. Russia generates 10% of global oil supplies and approximately 30% of Europe’s gas.

Although not clear cut, it is possible that the Ukraine situation may push inflation higher.

The US economy remains quite strong as it continues to emerge from the coronavirus pandemic recession. Inflation is tracking up and indeed spiking at the moment, and that’s why the US Fed has been much more vocal about rising interest rates in America over 2022.

New Zealand

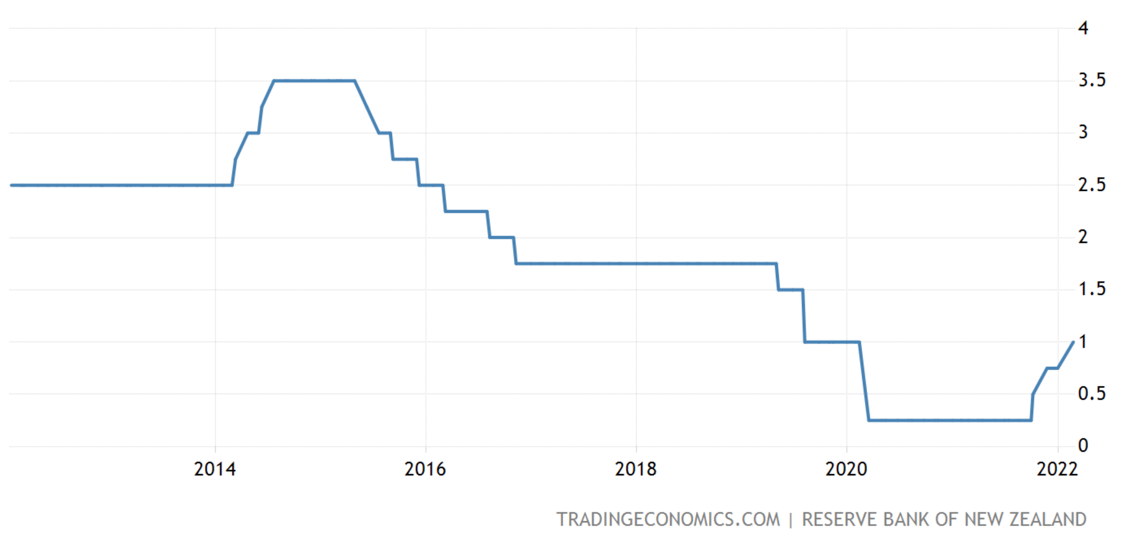

Interest Rates – New Zealand

The above graph the official cash rate here in New Zealand.

Interest rates are on the rise. This may sound like good news for retirees who insist on relying on income off their term deposits in the bank. However so far, the movement hasn’t been much. That said, they might be more encouraged by this time next year if interest rates continue to rise.

Mortgage holders, on the other hand, will be less pleased. In short, an increase in interest rates from 2.5 to 5% is a doubling of interest rates and a doubling of mortgage repayments. 5% doesn’t sound much if you’ve been around for a while, but a doubling of debt servicing is a lot for many people. The impact of that has yet to be felt as many mortgage holders have fixed interest rates that fall due over the next 12 to 18 months.

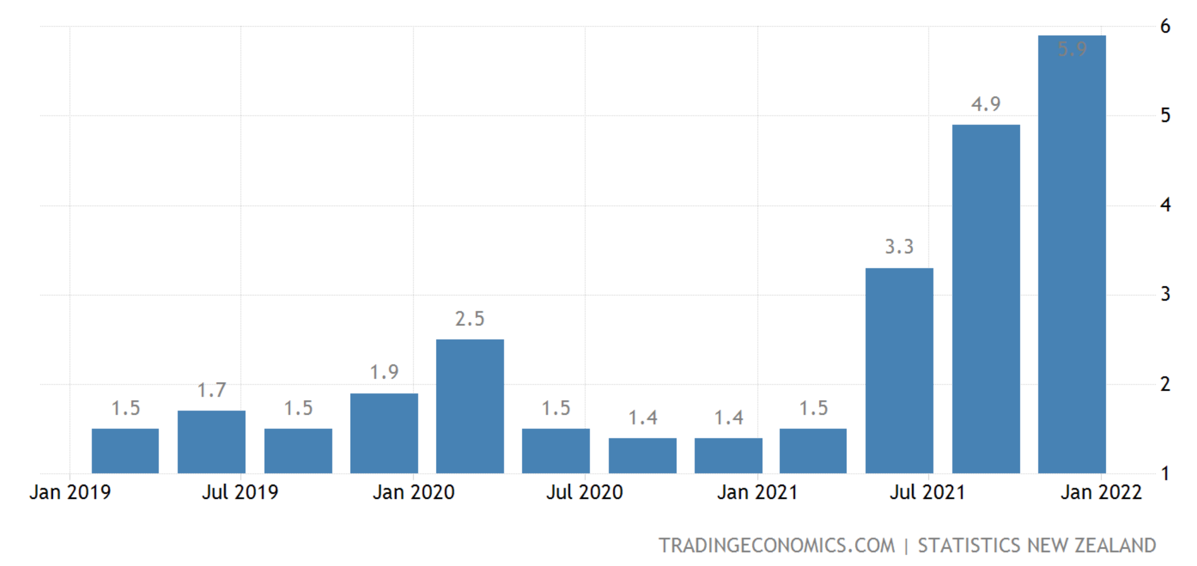

Inflation – New Zealand

As the chart shows, inflation in New Zealand, like a number of other countries around the world, has spiked recently as a result of supply-chain constraints.

With inflation in New Zealand tracking in an upward direction (quite sharply actually), the New Zealand Reserve Bank is taking action already.

Although we’ll see how it all works out, the Reserve Bank governor recently mentioned that some of the rises in mortgage rates have already been priced into rising interest rates, and so it will be interesting to see how much more mortgage rates might rise.

At the same time, it will also be interesting to see where inflation rates get to around the world and in particular, the United States of America.

On another note, business confidence in New Zealand appears to be on the decline as the government fumbles with clear direction on our exit strategy out of the coronavirus. It’s not helped by the public display of a loud minority camping out on the grounds of parliament who were (and still are?) fragrantly flouting the law in full display without consequences.

De-escalation may well be an appropriate strategy. I wonder, though, as part of that strategy, what might have been missing in terms of containing and managing the growth of the escalating lawlessness?

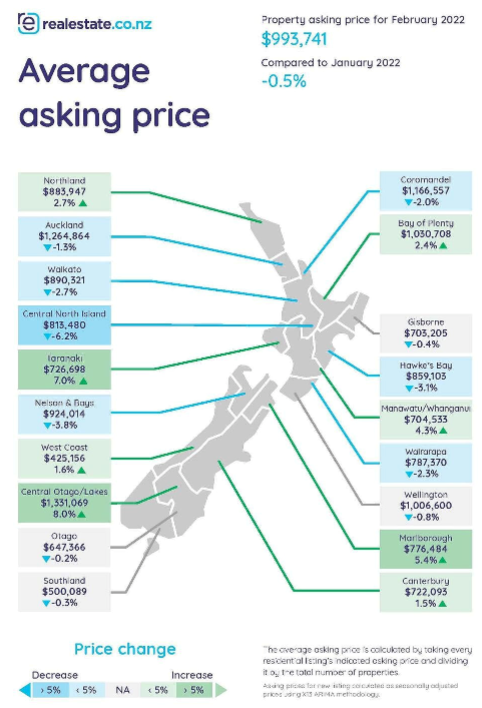

Residential Property Prices

We are now seeing residential property rises showing declines in some areas around New Zealand over the last month or two.

The chart above tracks residential property prices over the last 12 months and the last month.

Obviously, the annual increase is still positive. However, that annual increase may decline quite quickly over the next few months as does negative numbers work their way through the annual results.

It’s difficult to see any crashing of property prices because Kiwis love their property, let’s face it.

We might see though, in some areas, a pullback of, say, 5% or even 10%. That won’t be the end of the world. Banks won’t be worried about it. What matters, not only for banks but also for mortgage holders is their ability to service the loan.

Banks have been stress-testing their own servicing for Kiwi borrowers over the last couple of years on interest rates of around 6-8% as distinct from the 2-3% interest rates that have prevailed across markets.

6% is now becoming very real at the longer end of rates, although it would be interesting to see whether we get to 8%. It’s quite possible but not definite.

The answer to that lies in future inflation, which would be driven to some degree by factors outside New Zealand over which we have little control.

The New Zealand economy continues to have held up pretty well, all things considered over the last couple of years. However, debt levels are a bit higher now than they were previously.

We all look forward to some clarity over the coronavirus exit strategy…

To Summarise …

The Russian invasion of Ukraine has taken headlines across the world by storm.

It is difficult to predict how this will play out. However, if history is anything to go by, then we know that markets may well be trading at a higher level once the war is over compared to when it started. Time will tell.

Worries about nuclear missiles flying seem far-fetched right now. I know anything’s possible, but there is no hardcore evidence that supports this idea that is obvious at the moment.

As for World War III, again, it would appear highly unlikely given what we know about Biden’s response and the precision approach to taking out strategic assets across Ukraine. Of course, this could change, and if so, it could be a change for the worse, unfortunately.

Even then, that doesn’t mean World War III is about to erupt. There is a long way between now and World War III and plenty of reasons why World War III is off the table at the moment. Let’s not get ahead of ourselves.

Of course, we all hope for a speedy end to the Russian invasion of Ukraine and that the fear and suffering for Ukrainians is kept to an absolute minimum.

The impact on NATO-aligned Europe will be noticeable. However much greater on the Russian economy. Although it’s difficult to calculate, I reckon that Russia has a limited timeline for this incursion to work. Otherwise, Vladimir Putin may be pushed, however reluctantly, to the negotiating table.

Inflation might be exacerbated by the Russian invasion of Ukraine, and even if not, it remains a key indicator right now and over the remainder of 2022.

Therefore, interest rates are also a key indicator and one that we watch when thinking about pricing volatility.

Pricing volatility, of course, equals opportunity.

Trading prices are still not cheap even though there’s been some volatility across the markets. However, isolated opportunities within the markets are emerging.

The global economy continues to grow out of the coronavirus, with Europe stable (aside from war). America is growing, and back here in New Zealand, we are also growing with inflation and interest rates’ key items to be watched moving forward.