Inflation, Interest Rates, Oil Prices, Geopolitical Issues, The Changing Credit Cycle…

Monthly Market and Economic Update – January 2022

Peter Flannery Financial Adviser CFP

“If you have one economist on your team,

it’s likely that you have one more than you’ll need.”

Warren Buffett

Key Points:

-

There are plenty of Grey Swans (problems that usually go away) swimming about, so…

-

Are any of them going to turn into Black Swans (BIG problems that have significant impact)?

THE MARKETS

We have volatility!

The volatility admittedly is not significant. The real question though, is whether or not it’s the beginning of something bigger?

The above graph is the vix index that tracks share market volatility.

Volatility has returned to the markets as investors and analysts are starting to wonder about ongoing inflation and rising interest rates.

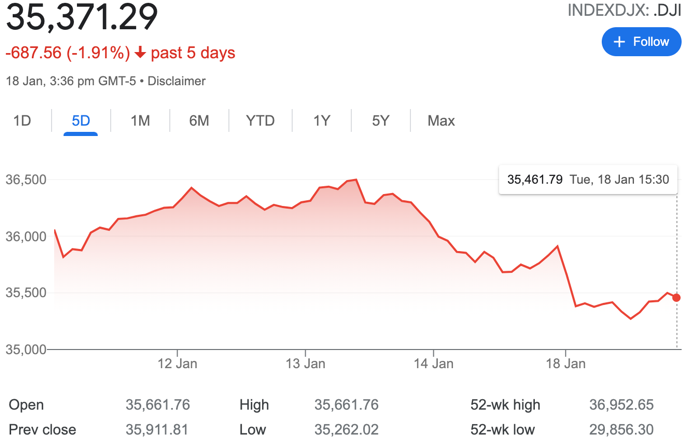

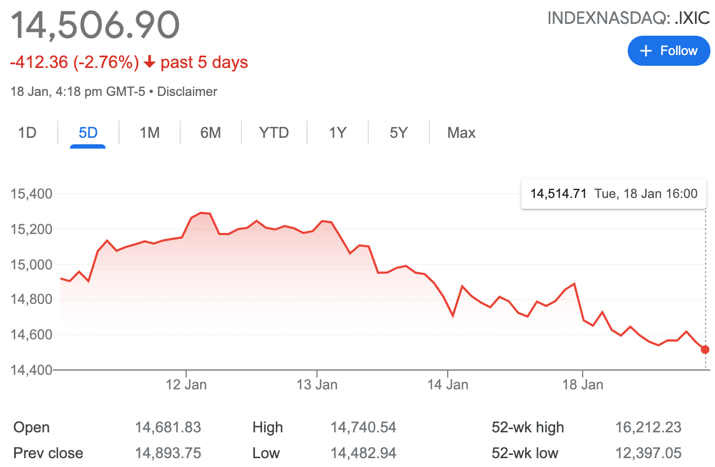

The chart on the left tracks the Dow Jones Industrial Index (US Share Markets) over a recent 5-day period. The chart to the right tracks the NASDAQ, which tracks technology stock prices, again over a recent 5-day period.

Obviously, five days’ worth of data tells us very little. That’s because price movement reflects market sentiment and has little to do with operational profitability… Yes, I know you’ve heard it all before.

I repeat it here, though, because investors can sometimes be overly focused on the moment, overlooking business, logic, and getting caught up in the market noise.

Anyway, the theme that has been running across the markets for the last 12 months or so is the rotation out of tech stocks into value stocks. So, therefore, is it not natural that WISEplanning would be at the forefront of this movement, given that we based our methodology on value investing?

The short answer is that we don’t follow market trends. I don’t mean that we ignore them. We simply don’t follow them blindly because everyone else is or because the noise around them is loud.

Simply, some of our tech holdings, including Alphabet and PayPal, for example, are fundamentally sound businesses that offer long-term growth. Even though the trading price of PayPal has declined quite a bit over the last few months, the business remains sound. It continues to offer growth on the back of ongoing innovation and an expanding ecosystem.

The point here is that in this environment, it is possible that those sexy new upstarts (e.g. Roku, Peloton Interactive, DocuSign, Datadog, and the likes), whilst offering significant upside opportunity in the long run, can at times be significantly overpriced by the market in the short term. Some of these types of operations don’t survive.

Larger, more well-established tech stocks, the likes of which WISEplanning has been recommending for many years, may well get caught up in the so-called rotation should the move become sharp and swift. However, with ongoing profits and sound economics, we can relax when it comes to the trading price recovery at some point and indeed, probably use the opportunity to build on our positions.

Investors at WISEplanning are not all the same regarding their investment risk preferences; therefore, how that’s approached is something I will talk to you about from time to time as I review your investment portfolio.

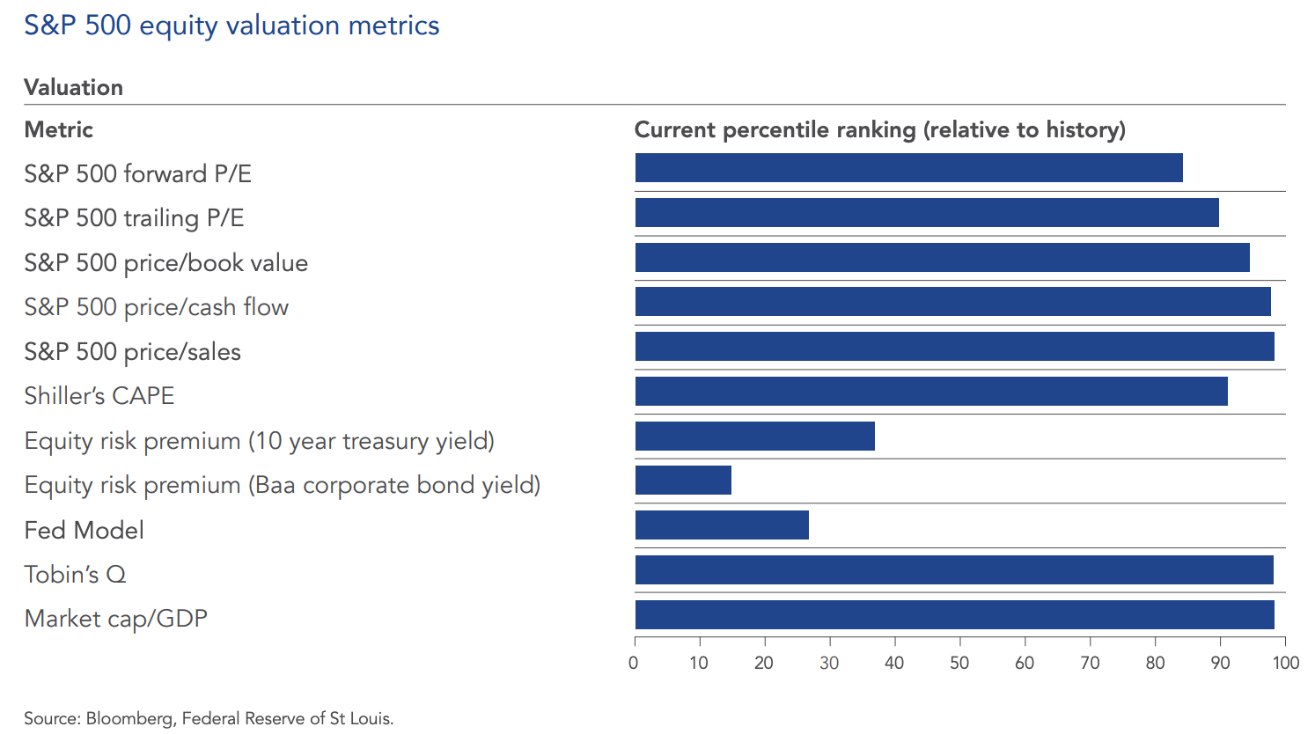

The above graph simply looks at a number of share market valuation indicators commonly used across the markets (Jan. 2022). These are not necessarily metrics that WISEplanning would focus on.

In the chart above, in simple terms, we can see that markets are expensive by a number of measures, except that is for the current level of interest rates.

In other words, if you look at how much of a return you can expect from bonds or term deposits compared to what has been achieved on share markets, it’s not difficult to see the disparity in returns.

Amusingly, when markets become unsettled, those simply playing the markets and chasing returns (rising trading prices) will sell what it deems to be risky assets in favour of so-called safe assets such as bonds and term deposits or even cash.

I say amusingly because long-term, we all know that ongoing inflation makes the real return in cash, bonds, and term deposits a poor comparison to good businesses that grow long-term, be they listed or unlisted.

It needs to be the right track!

That’s why it’s important to be careful about trusting what the market is saying.

For example, part of the market noise is simply journalists expressing their view or the view of the publication for whom they work (and who pays their salary). Good on them for keeping us informed I suppose!

However, you and I, the investors, the business owners should be selective about what we listen to and what we believe. That’s because what we listen to and believe takes us down a certain track.

Inflation

So, inflation continues to worry the markets. Not only that, we have the Omicron virus spreading swiftly around the world, although so far, New Zealand has managed to keep it at bay. For how long is the question?

We know that share markets are expensive. This is nothing new. However, what has changed more recently is persistent inflation (the combination of transitory and more permanent inflation), rising interest rates, and what I believe will be an increasingly fragile market which means more volatility ahead.

That’s why it is not time to be pushing money into markets, chasing prices as though that’s the way to get the best results.

It doesn’t mean that we sell down or bail out or don’t do anything. Sitting tight, though, might be something worth considering and what we might be doing more of just in the short term as we let the market come to us by way of volatility and lower trading prices.

One opportunity

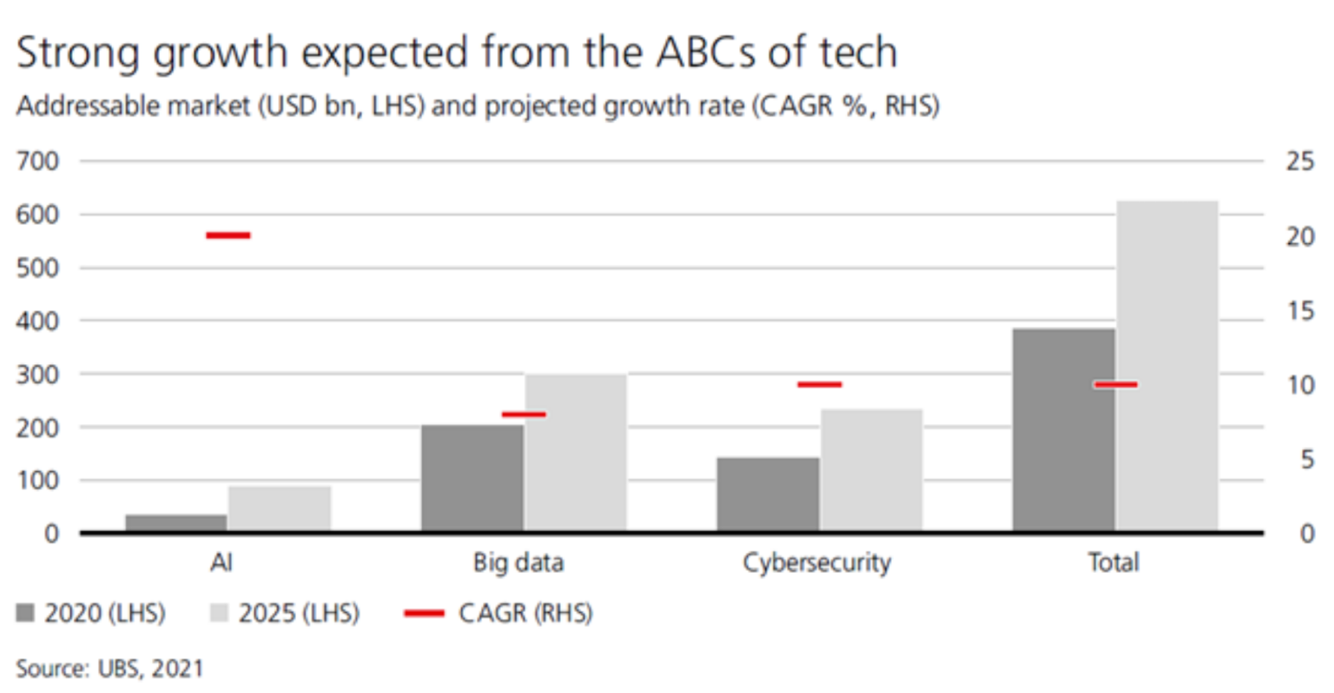

One opportunity could be the growth in Artificial Intelligence (AI), big data and cyber security.

The key point here is that whilst these areas are looking to grow, our mission is to select those businesses that will indeed survive, not to mention make profits for us as investors.

Advanced investors may want to participate in this area, whereas investors looking more for stability and to minimize volatility might be best to avoid this area, at least until some of these businesses are well-established.

Of course, the best money to be made is by getting in early. Everyone knows that. However, the challenge is that some of these businesses simply won’t survive, no matter how good their idea looks today.

One example that comes to mind is Palantir (NYSE:PLTR) – they have a strong balance sheet and should at least survive. Just take a look at the share price, and you’ll see what I mean about volatility. This company is definitely at the sharp end of innovation, developing new tools and services globally, for the US government and corporate organizations.

One challenge they face is the fact that, whilst attracting the cleverest minds from around the world, they have set themselves a mandate of remunerating their employees well to the point where comments have been made that there’s not much left for shareholders.

The potential here is massive. The question remains whether this opportunity is something that shareholders will be able to monetize anytime soon.

The above graph projects growth across artificial intelligence, big data, and cybersecurity over the next four years or so.

The bottom line appears to be, given persistent inflation, rising interest rates, tapering in the US, along with expensive trading prices, we can expect further volatility right ahead. You know what that means, though… more opportunity as well.

The Global Economy

So, what economic indicators give us clues about what may impact markets? Let’s take a closer look at some of the main indicators we can watch…

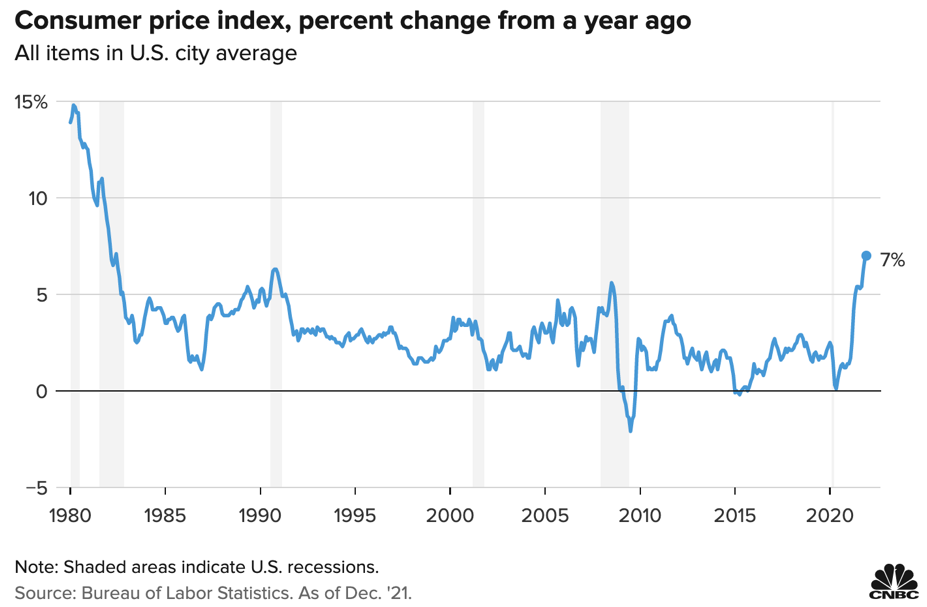

The above graph tracks US Inflation as measured by the Consumer Price Index from 1980 up to just a few days ago.

Okay, the Consumer Price Index (CPI) is a blunt instrument when it comes to measuring real inflation. That’s because it only it includes certain consumables and excludes other items such as property prices and some commodity prices.

Anyway, it does give us some indication as to what’s happening at the moment. Inflation is up, whichever way you measure it. That means rising interest rates, which means worry for investors and volatility. As the popular media likes to tell us, this is the biggest increase in the CPI (US) since June 1982, to be specific.

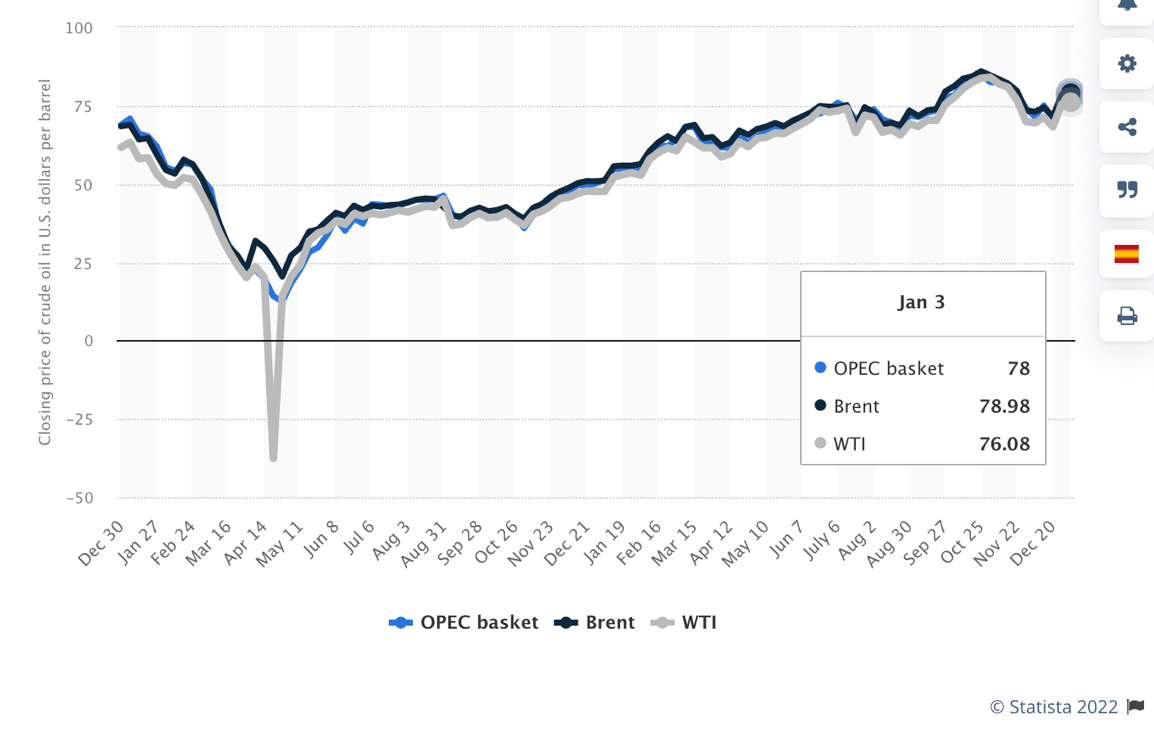

Oil prices rise

The above graph tracks the movement in oil prices.

Oil prices are rising because demand has begun to outstrip supply in recent times – not ideal.

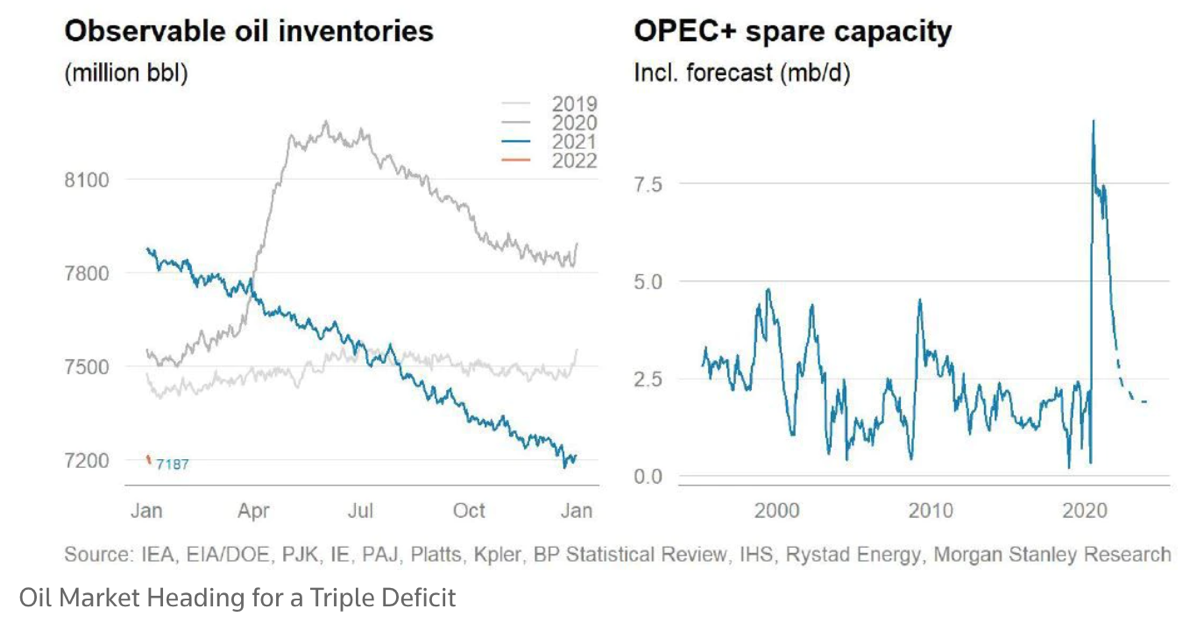

The graph on the left tracks the level of oil inventories from 2019 through January 2022 (note the faint orange dot on the bottom left of that graph). The chart to the right shows OPEC spare oil capacity from back in 2000 to the end of last year. Make what you will of those charts. To me, it suggests that oil is not a thing of the past and that the global economy still needs it to be able to function.

Obviously, the reliance on fossil fuels has been outed, and there is a push to replace this form of energy. It will be interesting to see what forms of energy are adopted over the next 10-15 years and the implications of that new energy source. I’m thinking about electric vehicles and batteries. What happens to those batteries when they are discarded, for example? What is the shelf life of a battery for an electric motor vehicle?

The point about rising oil prices is that they represent a potentially significant speed bump for the global economy. If they see a serious slow down because of rising oil prices, the markets won’t be happy about it – more volatility for us.

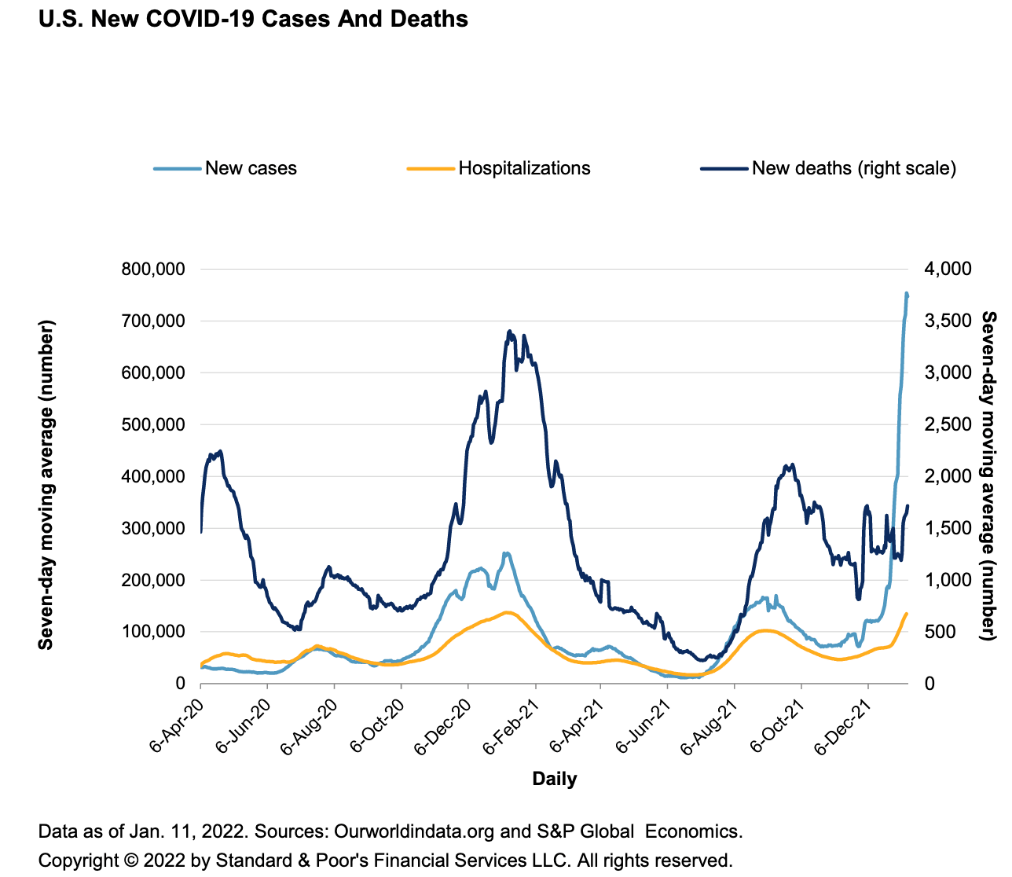

The above graph tracks new cases, hospitalizations and new deaths.

The Omicron strain of the virus, at least anecdotally, appears to be less harmful, and the death rate has not increased significantly even though the infection rate has been fast to increase.

I understand that the Omicron virus’s impact is not over yet, although its impact may be less significant compared to previous outbreaks.

The Flow on effect

The problem is that the rapid spread of Omicron is making an already challenging situation for business owners worse. Some employees have received cheques in the mail and are not that keen to go back to work, and others may be put to the side lines as they become infected with this new strain of the virus.

At this stage, it doesn’t appear to be a major problem for the global economy but will have an impact nonetheless. There have been some reports of businesses having to close their doors on certain days of the week because they simply cannot get staff.

This is the case not only in the US but also in the UK and parts of Europe as well.

There has also been mention of a new strain that may be emerging. Just when some were suggesting that this strain might be the end of the current outbreak.

The new strain has been referred to as IHU. Little is known about it at the moment, and we’ll watch and wait to see what develops.

Geopolitical considerations

China and America are natural competitors. They compete across a number of fronts.

I recently read an article suggesting that China’s military capability would catch up with America by around 2030 (eight years away). It looks like we have a bit of time to think about what that might mean!

Right now, though, Russia appears to be building troops near the Ukrainian border over recent months as tensions have escalated. It appears that Ukraine has become more aligned with Europe and NATO, which doesn’t suit Russia.

In response, they have increased gas prices over winter and allocated more troops along the border. There is nothing to worry about at this stage, although something to keep an eye on.

For many years, the Middle East has been an area of discontent, and that’s nothing new. Currently, there is some concern about the outcome in terms of unprecedented risks that could emerge if the talks between Iran and Israel break down. It won’t be the first time if those talks stall. However, the real risk, which is possibly unlikely, are that missiles are fired once again but this time against nuclear facilities.

I have mentioned in the past the build-up of ships around Taiwan and China’s insistence that Taiwan is part of China. There has been some so-called sabre-rattling over the last 6 to 12 months. However, nothing to be concerned about at the moment but something obviously to watch.

Back here in New Zealand…

The New Zealand economy has been surprisingly resilient.

It hasn’t hurt, of course, the fact that we are basically a large island isolated from most others in the world.

That has helped us to keep the coronavirus at arms-length to some degree.

In short, the coronavirus game is far from over, although the steps in place to combat the virus may be helping to get us to the end. At least to the point where we simply live with it and get on with our lives.

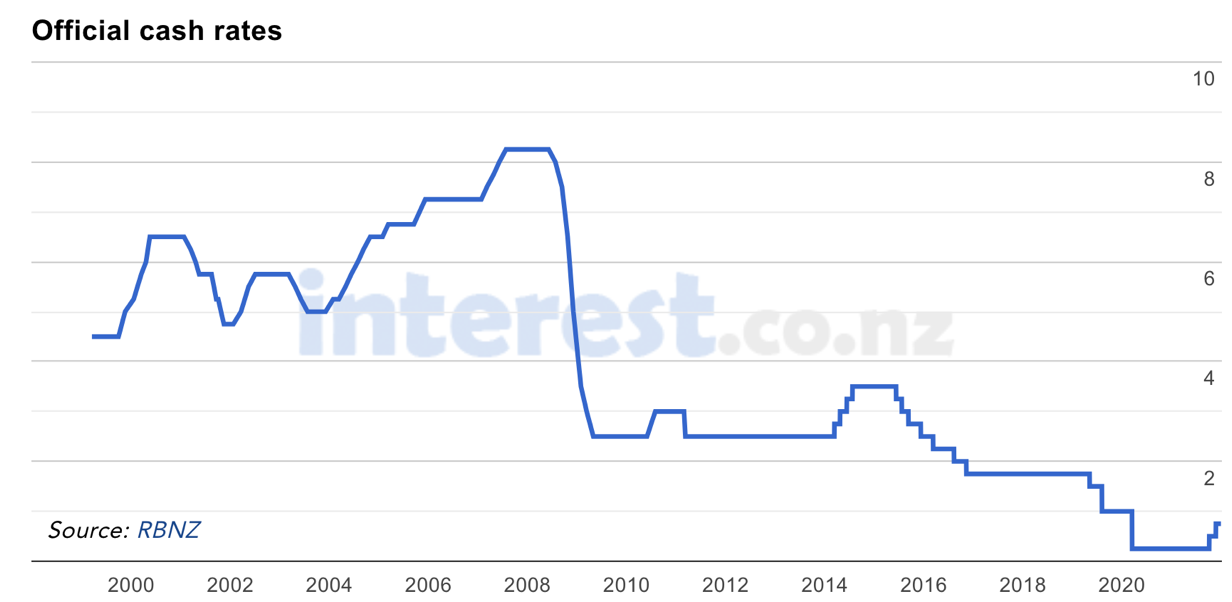

The above graph tracks the official cash rate here in New Zealand from back to 2000 up to date.

So, interest rates have been declining for decades. Nothing new.

Are we seeing interest rates undergo a secular shift towards an upward trajectory?

This matters, of course, because interest rates impact asset prices.

To be clear though, it doesn’t mean that a good asset is no longer good. Quality assets are quality because of their intrinsic characteristics – not interest rates.

Interest rates are more about the pricing of an asset.

What’s important here is that when we invest in an environment like we’ve seen over the last 30 years or so that has been highly liquid, we will probably make money one way or another.

Moving forward though, a higher level of interest rates makes it more difficult for some businesses to raise capital and to grow. Further, some businesses that are not well-financed and whose profitability is weak can become compromised as interest rates rise.

Quality investments may well see their trading price decline. That’s a different thing to their intrinsic value, which of course, is not based on market interest rates but rather the asset’s ability to use capital.

The point here is that we need to be careful if trading prices are re-rated downwards. The market takes a simple view on pricing – declining prices means bail out, sell.

We want to be careful that we don’t bail out of quality investments that in the future, the market will love once again as they report growth. Remember, reliable profits are mostly about the ability of the asset to use capital rather than interest rates. Admittedly, I am simplifying this whole point. However, I trust you get the idea?

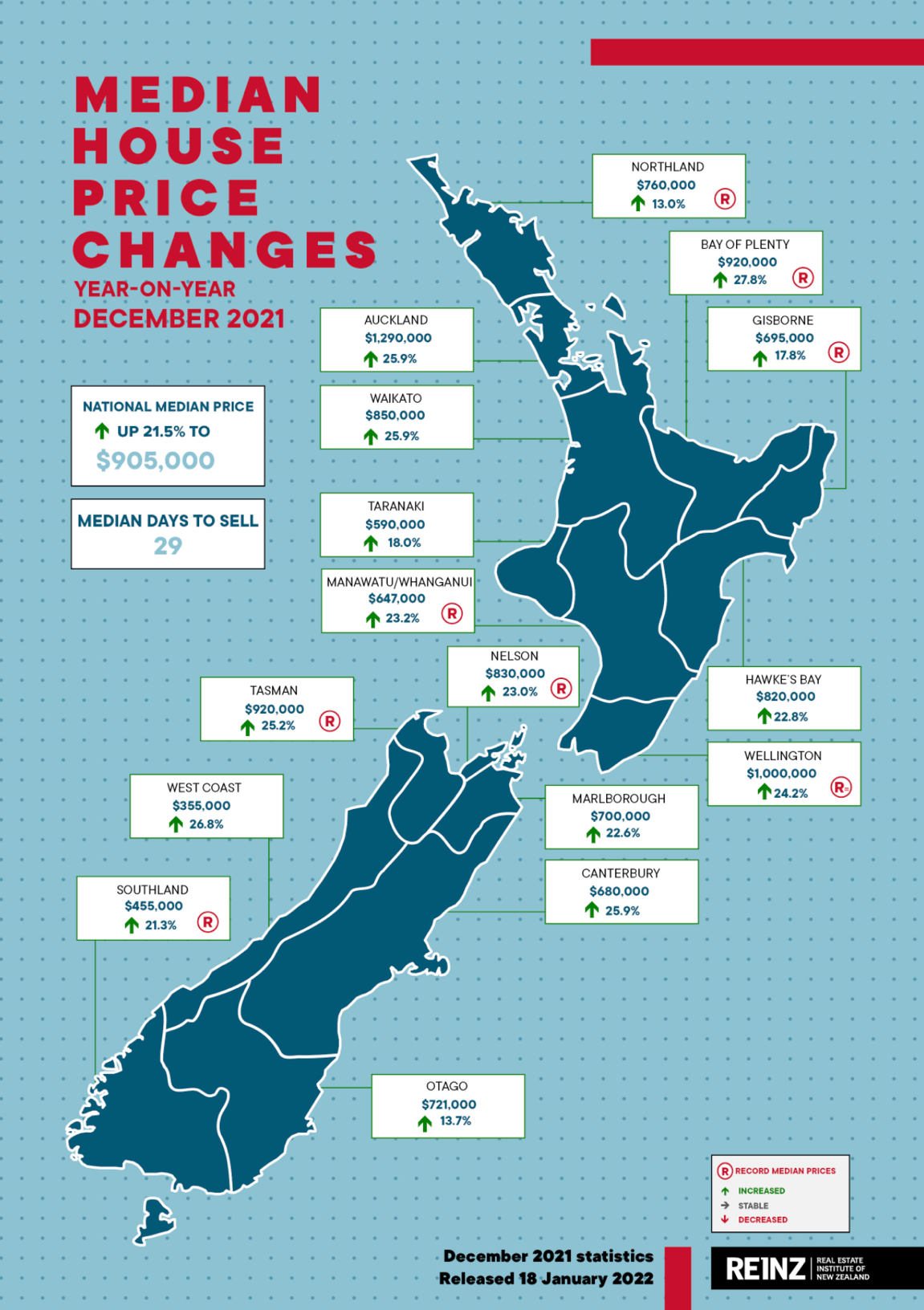

As you can see from the image above, most areas have seen significant lifts in property prices – why is that?

In my view, there are a few forces at play.

Firstly, interest rates have been declining for decades, and the mechanics of this simply means that it’s easy for asset prices to rise in that environment. In addition to that, we have had easy money conditions where getting a loan or raising capital has not been too difficult (increasing credit across the economy – see the latest Investment Perspective) until recently.

In New Zealand, banks are now faced with new legislation that makes them more accountable for the loans they provide to their customers. This means that the banks are scrutinizing customers’ balance sheets and particularly cash flows and spending habits. You may have read in the media about how some would-be borrowers have been turned away because of a shopping event at K-Mart or a Netflix subscription and the like.

Of course, the New Zealand Reserve Bank is behind it all, wanting to ensure that we have stable capital markets and that banks don’t let those who cannot service and repay their loans become compromised, creating problems.

As always, it’s not when everything’s going well but rather when there is an event that creates serious capital and cash flow problems for an economy that impacts those who can afford it the least.

It’s not the millionaire with no debt that’s likely to be compromised, but rather the hundreds of thousands of mums and dads who have loans and children at school, modest incomes, and are getting by from week to week. Members of the so called ‘disappearing middle class’ here in NZ.

Of course, at WISEplanning, we have two programs that help everyday Kiwis to escape that situation – another story for another day, perhaps, but let us know if you have family who might like to know more…

Whilst we’re on the subject of fast-rising property prices, we should also include New Zealand’s love affair with property as another contributing factor. Some have done very well from property over the years and simply believed in it because of their experience.

I wonder what they think about the changing credit cycle underway globally along with the implications of tougher banking scrutiny enforced by new legislation and the Reserve Bank of New Zealand?

In short, the environment is shifting. We’re moving into an environment that will not be the same as it was over the last 30 years or even the last five years.

The question though, is whether it hurts the very people it’s trying to protect by depriving them of capital in the form of loans that help them to get ahead long term?

Still, with potentially tougher times ahead for some, the New Zealand Reserve Bank will want to make sure its ducks are in the row properly, should an unexpected event emerge from offshore.

I don’t believe the game is over for property as an investment. Clearly, though, conditions are now different.

To Summarise…

My market and economic updates are designed for investors, specifically. In this update, I have pointed out some of the main items that may impact markets over the next 12 months. It may sound a tad negative, especially if you like to see prices rising every day.

The credit cycle is indeed a cycle, although not a nice neat wavy line that you’ll often see on your computer screen or other written material. It is an ad-hoc line that’s a bit more jagged and surprisingly unpredictable.

Conditions are changing, so prices will reflect the markets’ fears and concerns as that takes place.

I am not being negative. Instead, I am simply reporting the facts as I see them.

I trust that whether you’re a seasoned investor, having seen it all before or whether this is relatively new to you, you can see the benefit of uncertain markets and the advantage that lower prices offer?

“People can foresee the future but only when it coincides with their own wishes.”

George Orwell – British Writer