Will Rising Interest Rates Be A Problem?

Monthly Market and Economic Update – April 2021

Peter Flannery Financial Adviser CFP

“If you have one economist on your team,

it’s likely that you have one more than you’ll need.”

Warren Buffett

MARKETS

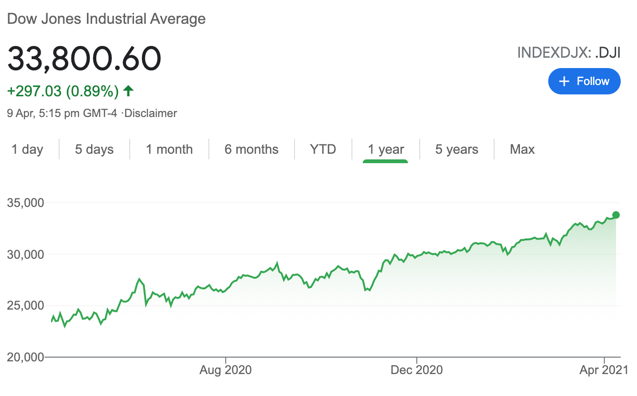

The chart on the left shows the US share market (the Dow Jones) over the last six months. The chart on the right shows the US share market (the Dow Jones) over the last year. The US markets, as measured by the Dow Jones continues to rise to new all-time highs and the Nasdaq representing the tech sector even faster still.

Key Points:

-

Economic growth is coming.

-

But interest rates are rising.

-

What does it mean?

Market Risks

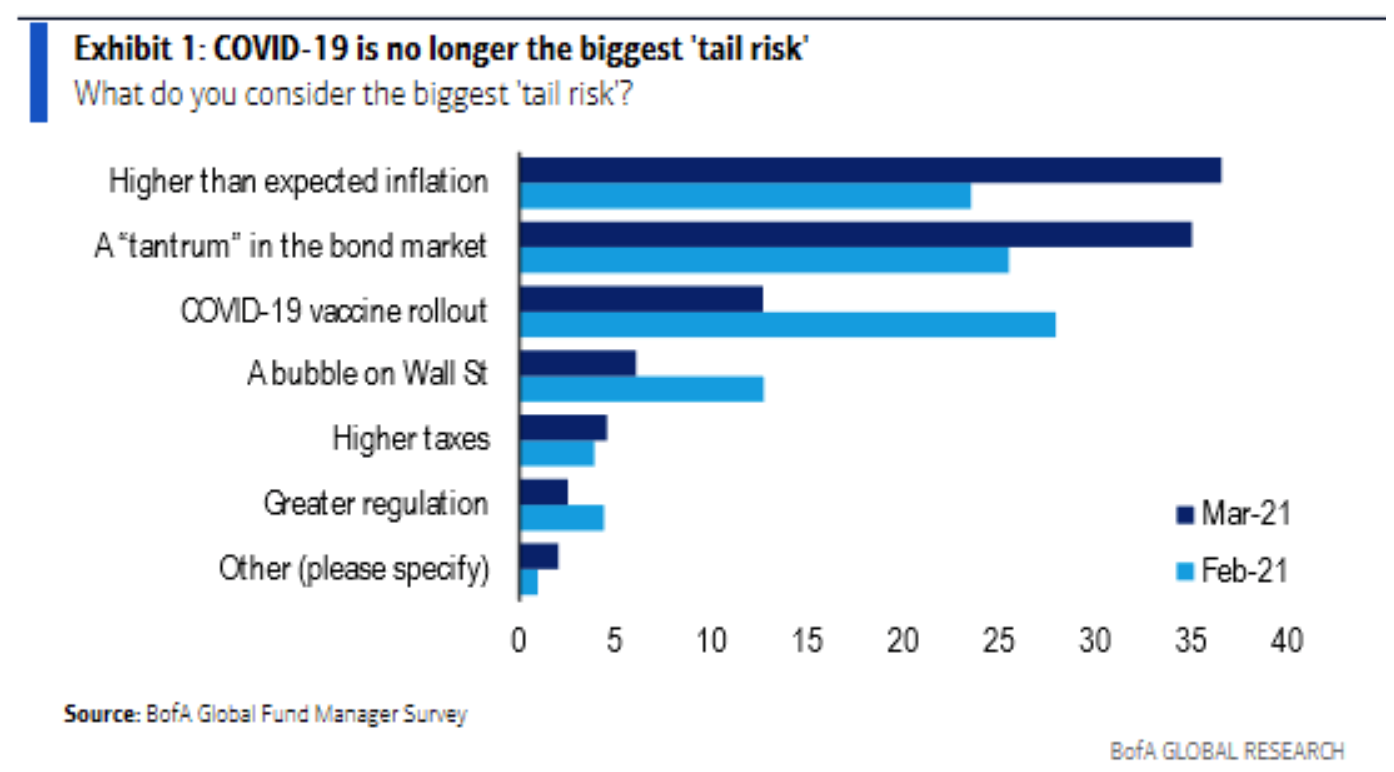

The above chart highlights some important risks, comparing March 2021 with February 2021.

Global markets have undoubtedly recovered from the coronavirus. The control over the virus however is less certain and remains a challenge for a number of countries. Interesting to see the New Zealand government finally stopped importing the virus from India in order to reassess what to do!?

Although there is still a lot that we don’t know about the coronavirus and the increasing number of mutations, so far the vaccination program being rolled out in a number of countries appears to be achieving the desired objective.

Although we don’t know how long those vaccinations will last, they at least are helping to control the spread of the virus currently as more and more people become fully vaccinated.

As some of my clients have mentioned from time to time, this virus may be with us for a long time yet.

However, as I’ve mentioned over the last six months or so, markets have largely looked beyond the coronavirus to the point where I believe now, one of the big risks to market pricing and the cash up value of our portfolios is an unexpected spike in inflation.

In that situation it is possible that the US Fed may respond with an unexpected hike in interest rates which could rattle the markets.

I wouldn’t lose much sleep over it though, even if the market does correct quite a bit. That’s because in general terms, inflation means growth which is a good thing.

No point in becoming distracted by short-term pricing corrections, other than to take advantage of lower prices.

Portfolios at WISEPlanning are bespoke which means that one portfolio is different from the next. Generally though, we are reducing levels of cash overall in favour of building in more long term growth.

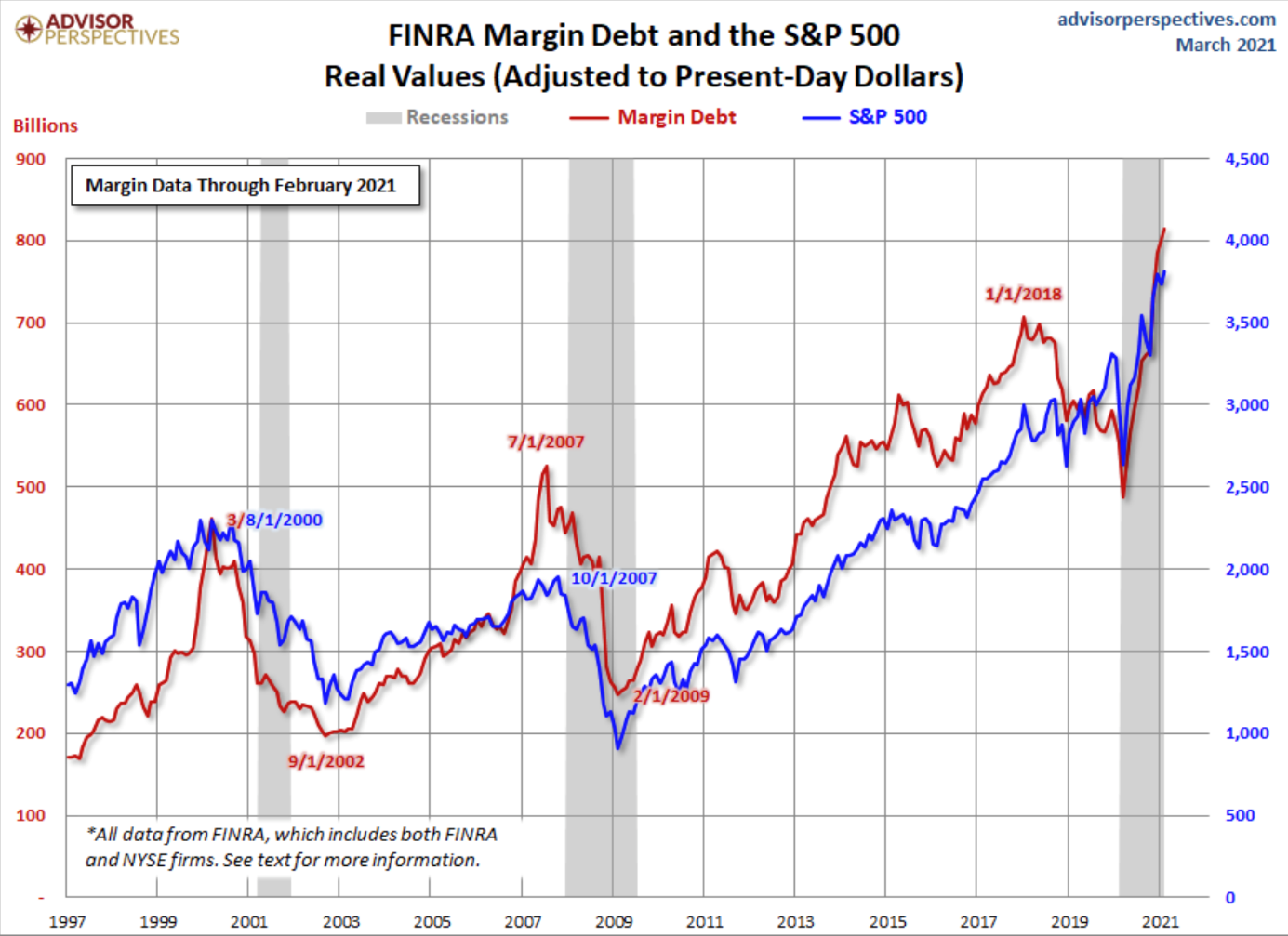

The above graph shows the movement in the S&P 500 Index and compares it to the amount of margin debt at play across the market. The red numbers on the left axis equate to the red margin debt line on the graph and the blue numbers on the right side of the graph equate to the blue line measuring the S&P 500.

At first look, the graph above suggests that margin debt, being at an all-time high means things could crash anytime soon. A closer look shows of course that we are only just coming out of recession which highlights the fact that markets are forward looking, hence the increase in margin debt.

Margin debt put simply is where some fund managers and some investors borrow money to invest in the share market. A good idea when markets rise but not so much when markets decline.

It is also important to remember that the global economy is growing. Sometimes, graphs and charts can paint a picture that is not totally factual.

For example, looking at price-to-earnings ratios as a way to value businesses is something that I’ve often talked about as being an unreliable way to value businesses on the share market. An interesting guide but, sometimes it paints the wrong picture.

That chart above is factually correct but takes no account of the fact that speculators are pushing up that red line on the graph above as they anticipate further growth ahead. As we know from past experience, should a surprise to the negative suddenly emerge, those investors using margin debt can sometimes bail out in a big hurry.

That can cause market prices to decline but the point being that, the increase in margin debt and any subsequent decline in share prices due to an unexpected surprise piece of information may not necessarily reflect the fundamentals of the businesses in which you and I invest, nor the ongoing growth of the economy along wih those businesses in which we invest.

Gilti Tax

Joe Biden, President of the United States of America, is proposing to setup a tax on US companies that receive a substantial amount of their revenue outside of America.

Some of these companies you’ll know such as Alphabet, Facebook, Apple, Amazon, and many others, are potentially paying less tax in the US because they’re paying tax in another jurisdiction.

Other countries might levy tax at a lower rate than what otherwise is the case if the revenue was derived in the US or repatriated back to the US. The idea is to add this so-called GILTI (global intangible low-taxed income) tax which is intended to discourage US companies moving intangible assets and related profits to countries with tax rates lower than the US corporate rate.

The current tax rate is circa 10% whereas the Biden administration is looking to increase that tax up to around 26% or so.

This could have an impact on the profitability of those companies and the markets, if they don’t like the idea could react by scaling back the holdings ( selling down) in these businesses, although at WISEPlanning, we would regard that as a transactional approach to investing. There are many other factors to consider.

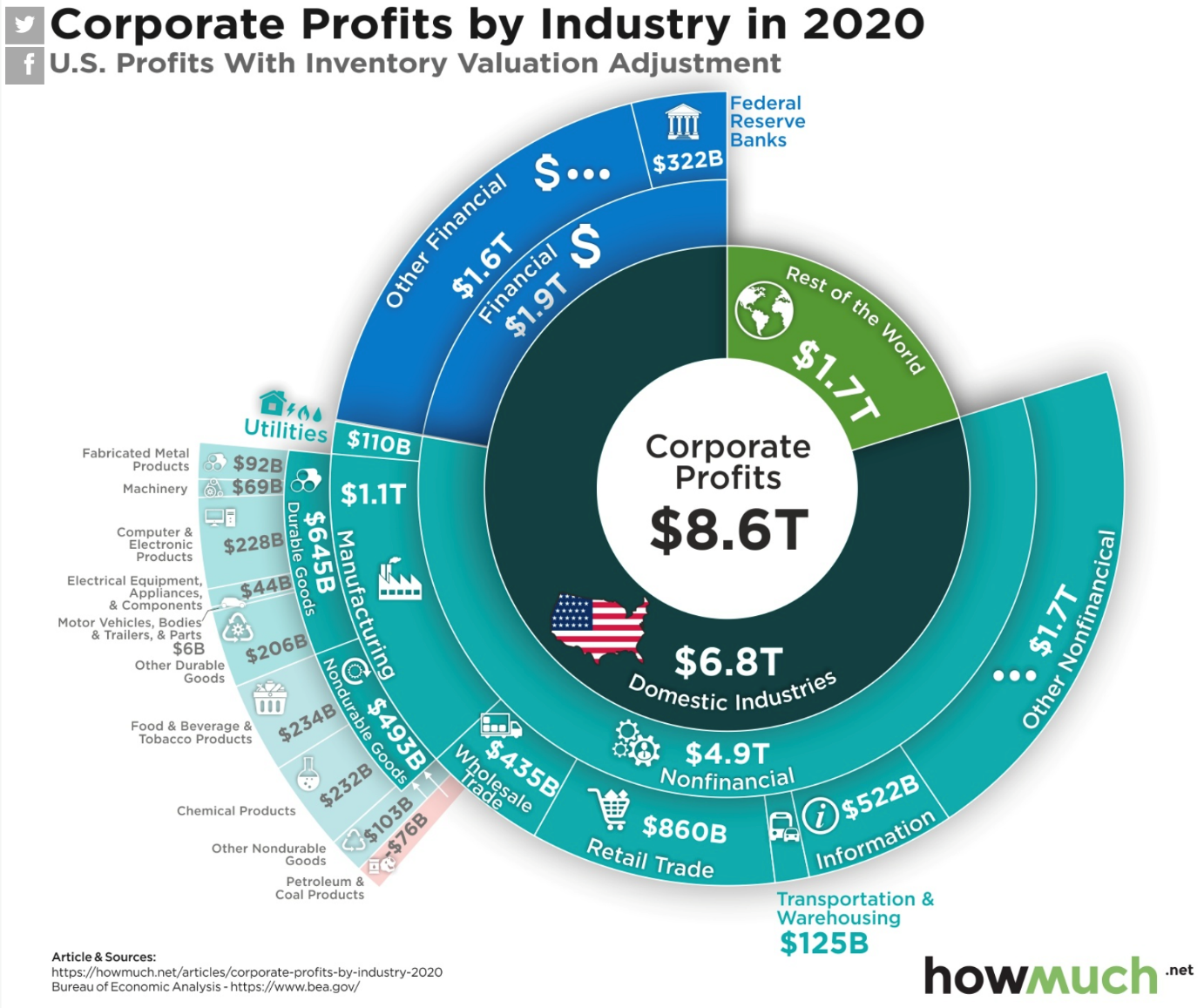

The above diagram compares the level of profits generated in the US by US companies compared to those more global US companies in the rest of the world.

As the above diagram shows, by the far the majority of corporate profits are from US corporations in America as distinct from companies operating globally. Therefore an increase in corporate tax might affect those specific businesses operating globally to some degree but would appear unlikely to create a serious speedbump for economic growth in the US and therefore this tax would not appear to be a major problem for markets.

So, there are some risks but then that’s nothing new.

What I haven’t highlighted this time around is the potential growth that lies ahead for markets all things equal.

Although I’m cautious about pent up demand, it is nonetheless a fact that may drive markets to some degree, at least in the short term. There is also significant support from central banks around the world as well as interest rates remaining low, even though the long end of interest rates has increased a bit.

Although we’re always watching a number of indicators, the inflation rate in America is a key indicator worth watching. That’s because it could mean a sharp increase in interest rates which the market would probably not be happy about.

Again though, nothing to lose any sleep about providing we are focused on quality businesses with sound underlying economics. Trading prices remember, don’t rise in an upward direction in a straight line. ?

The Global Economy

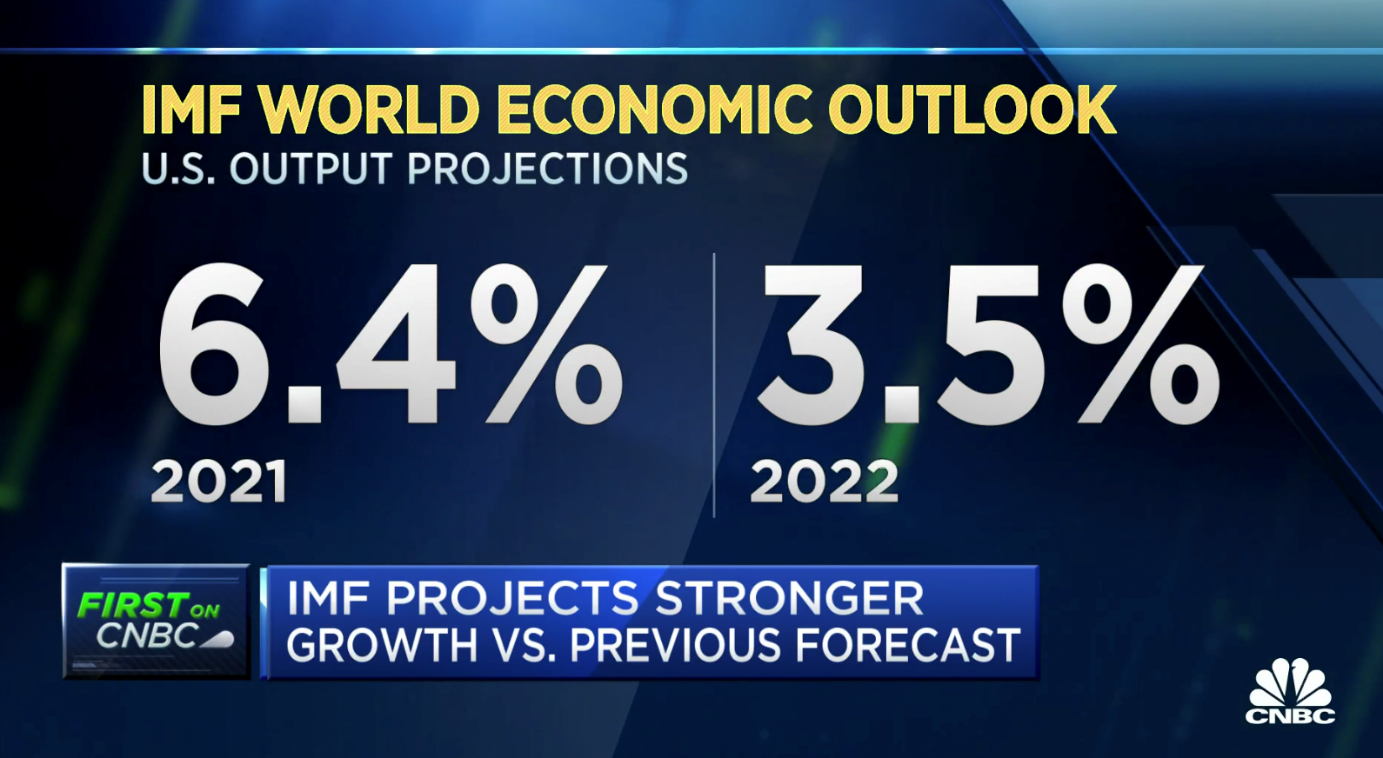

The International Monetary Fund (IMF) recently upgraded its global forecast for economic growth to 6.4% for 2021 and 3.5% for 2022.

The outlook for the global economy generally looks promising. Of course, there’s always trouble one way or another but that’s normal.

Anyway, the IMF suggests improved economic growth at around 6% for 2021 which is up from its previous forecast in January of 5.5%. The IMF also suggests advanced economies may grow by 5.1% with the United States of America potentially set to grow by 6.4%.

Although the rollout of vaccines remains a significant challenge for many countries around the world, an increasingly vaccinated population appears to be helping reduce the spread of the coronavirus. As we’ve mentioned previously, we’ll need third world countries to be vaccinated before we can say that we have successfully halted the spread of the virus.

Low interest rates, the rollout of the vaccines, and the stimulus packages implemented by central banks around the world is helping support future growth. Further, there will also be infrastructure spending as well.

In America, President Joe Biden’s $1.9 Trillion coronavirus stimulus package is also helping support economic growth. Growth in America can also help support growth in other economies too.

The United States of America

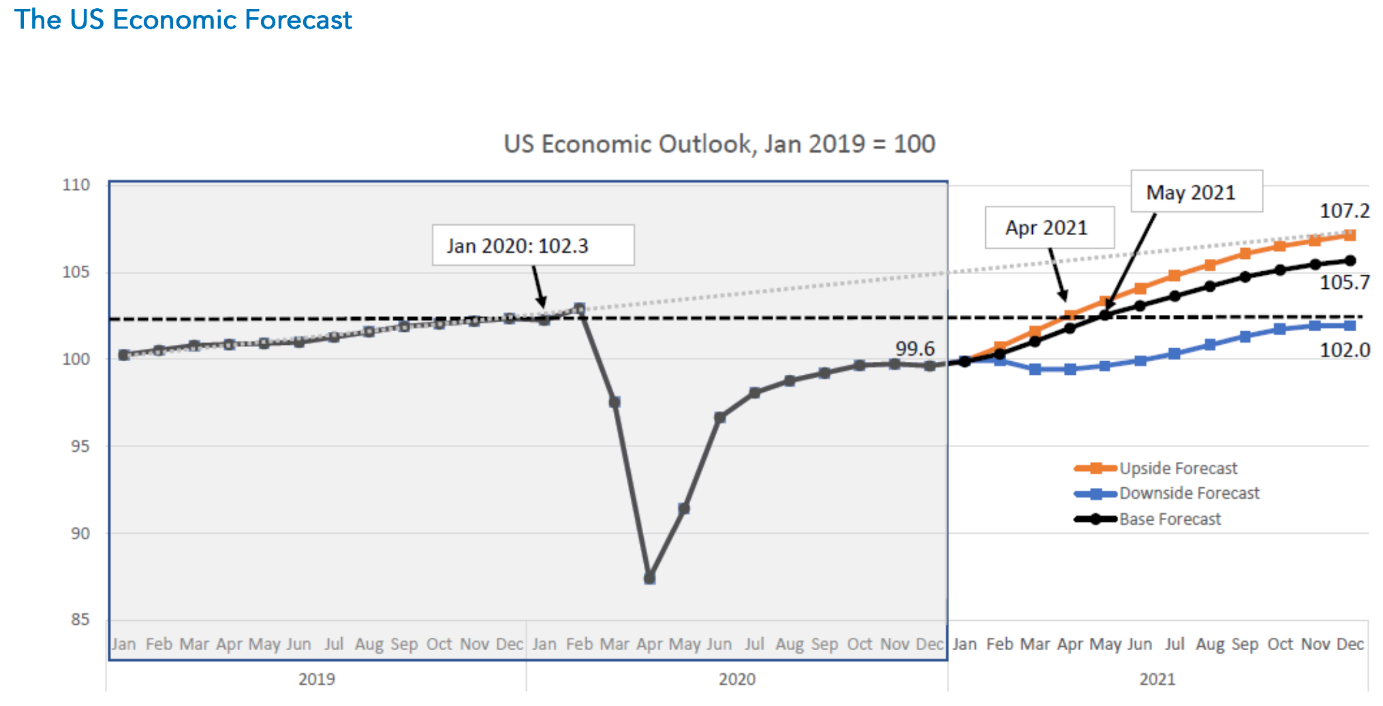

The above chart shows projected economic growth over 2021.

The American economy is poised for economic growth over 2021 and beyond. The combination of low interest rates, the US Federal Reserve bank intervention, the recent $1.9 Trillion stimulus package, reducing unemployment, and of course the rollout of vaccines to help contain the coronavirus, all come together to support growth.

Increasing interest rates and inflation are a couple of things to watch although I suspect Jerome Powell, the US Fed Chairman will be cautious about snuffing out growth by raising interest rates too much too soon.

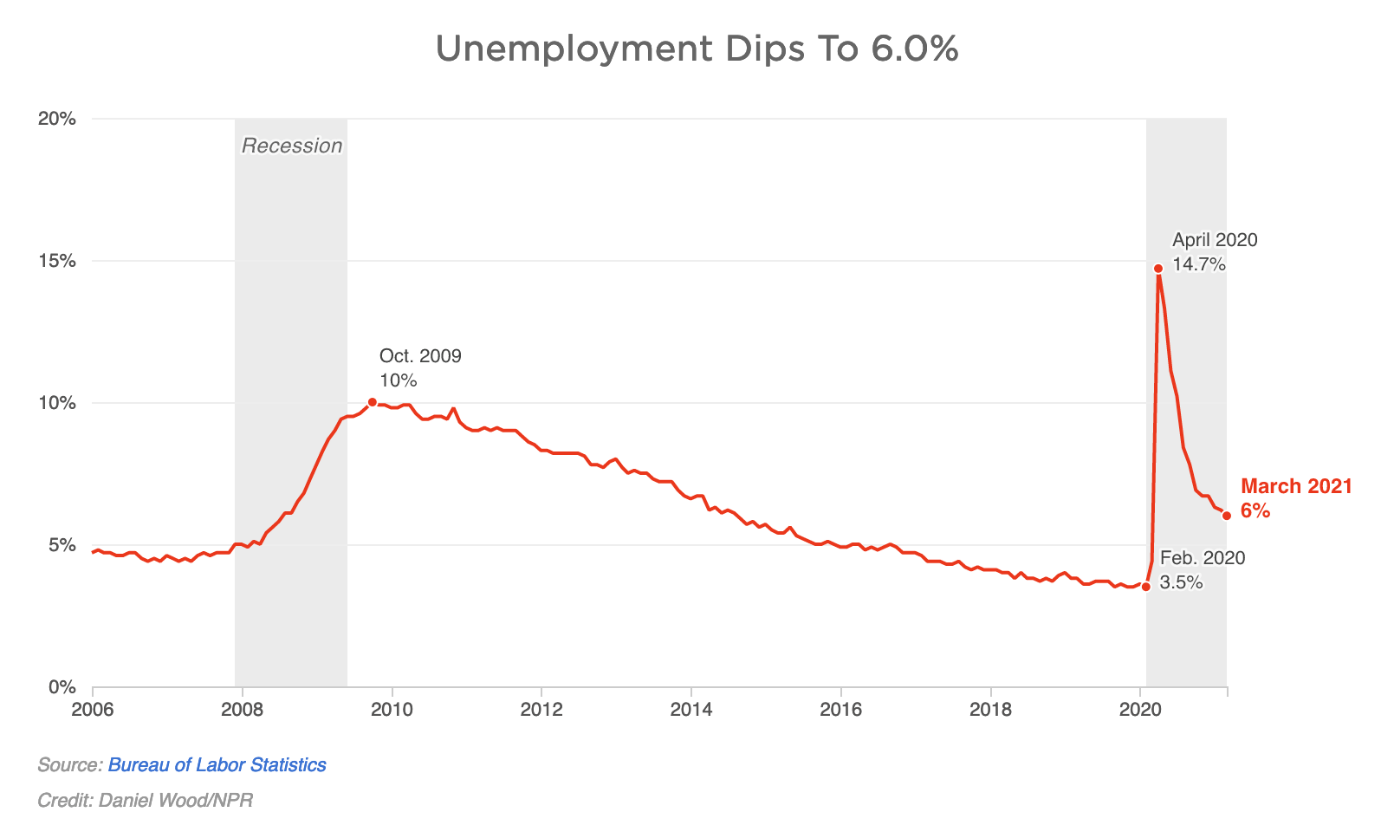

The above graph shows movement in the unemployment rate in America.

Unemployment in the US continues to decline. Although there’s still a long way to go yet before we get near full employment, the trends in the data around unemployment in the US are encouraging. Still there are 8.4 million fewer payroll jobs in America now than there were before the coronavirus took hold 12 months ago.

By some measures, even if the recent economy can add 1 million jobs each month, this still takes us into 2022 before we get back to pre-pandemic levels of employment. It appears that workers related to hospitality are gradually returning to work whereas those involved in manufacturing were less impacted by the coronavirus and have returned to work at a faster pace.

The above graph tracks the movement in the 10-year treasury yield.

The trend in the rising 10-year treasury rate continues. It will be more interesting to see where it gets to next. The 10-year treasury yield is a well-known interest rate indicator followed by markets around the world. Rising interest rates in America could lead to rising interest rates elsewhere.

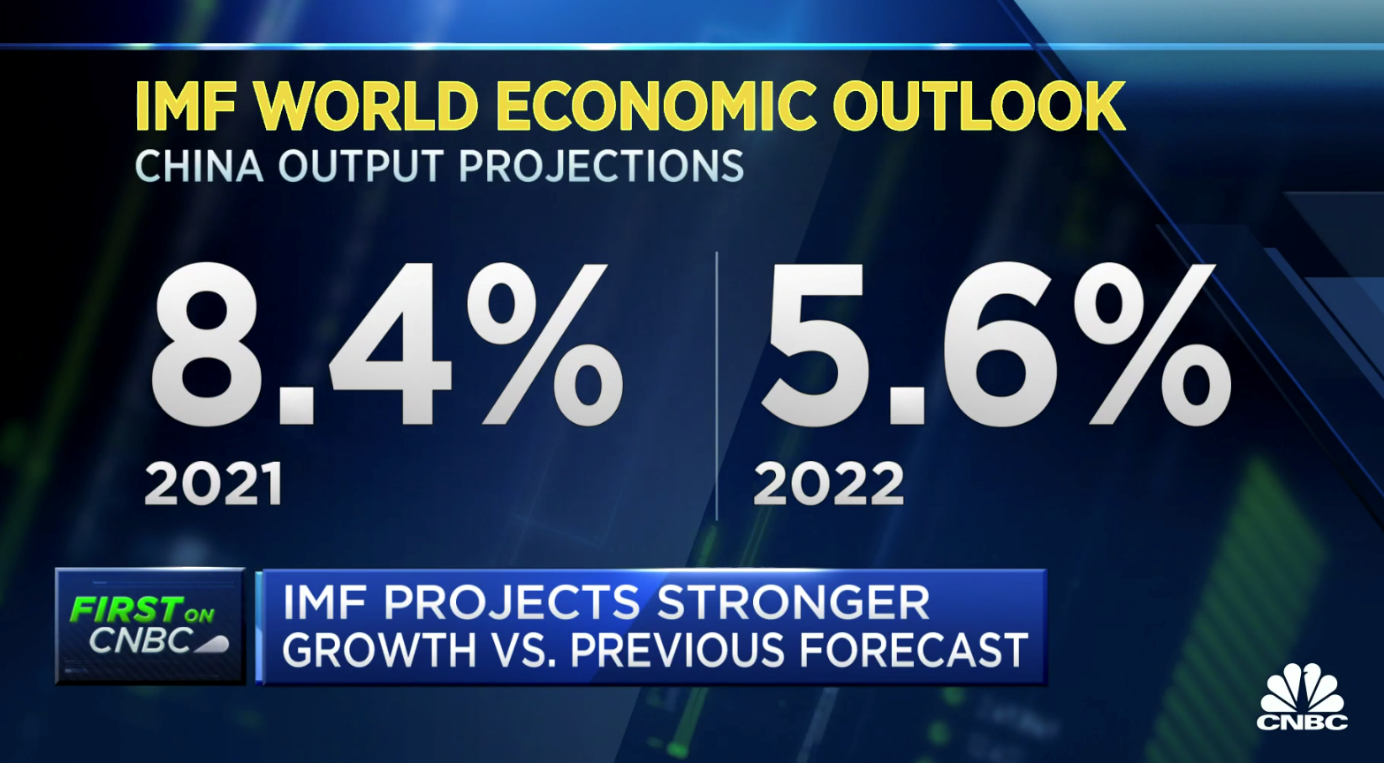

China

The IMF upgraded its recent economic growth outlook for China to 8.4%.

China’s economy continues to grow, supported by central bank stimulus, low interest rates, and of course strong containment of the coronavirus. China is well-placed for growth over 2021.

This is at the same time as ongoing tensions between China, the US, Australia… who will be next?

China of course is a superpower and my expectation moving forward is that they may be more forceful in their dealings with other countries in the future.

The IMF is predicting ongoing fiscal and monetary support with the possibility of a mild interest rate tightening this year as a result of the significant fiscal expansion over 2020.

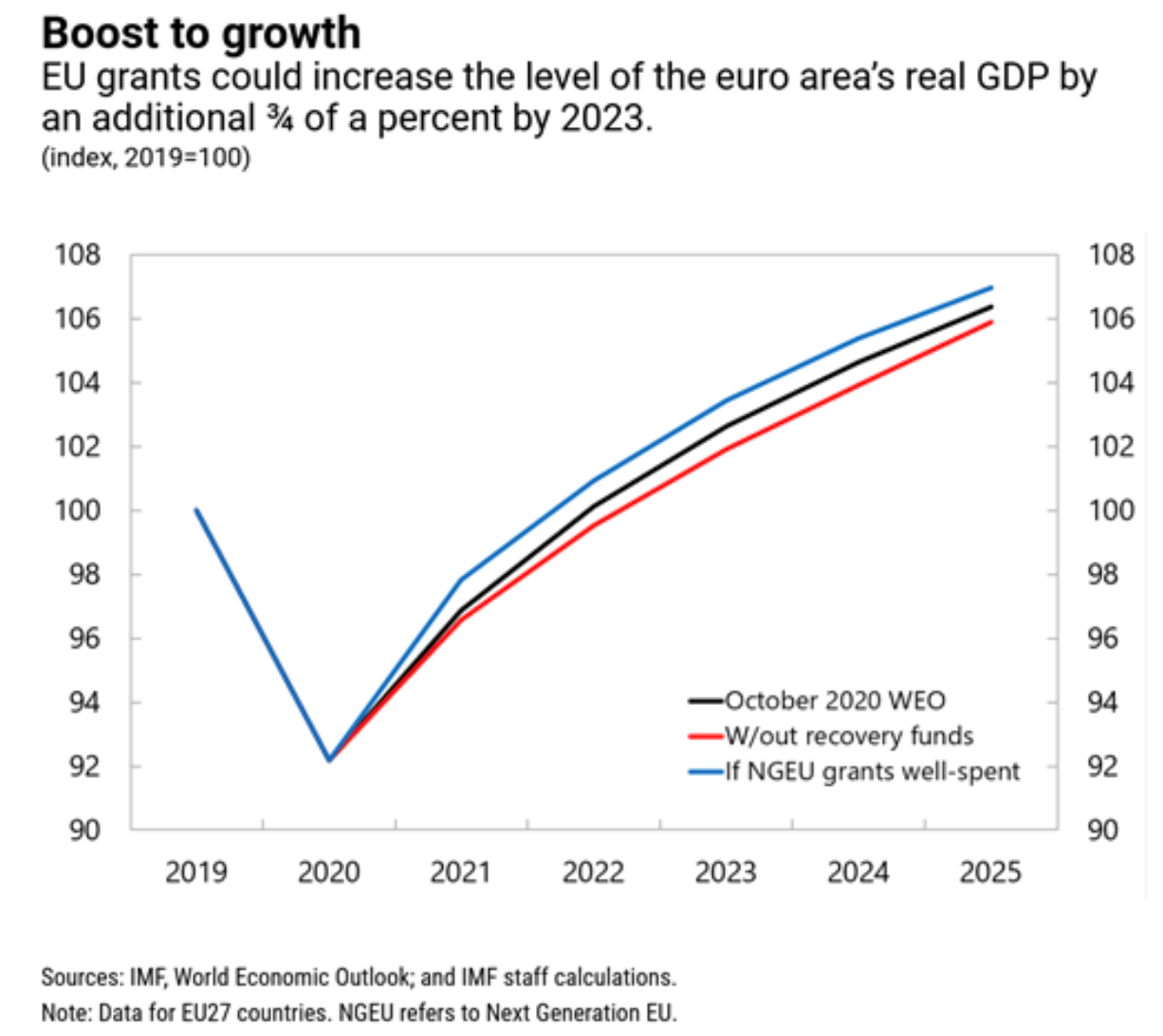

The Euro Area

Using 2019 as the starting point, the above graph shows the economic contraction and recovery through 2025.

Economic growth in the Euro area also looks positive although probably not at the pace of other economies such as China and the US.

Central bank support has been important for the recovery of the global economy and no less so than the Euro area.

European Union recovery funding should play a critical role in helping accelerate the green and digital transitions and also helping boost economic growth. There is the €750 billion next generation EU recovery fund of which €390 billion are grants.

Hopefully this will be used to initiate investment to reduce carbon emissions and improve productivity through increased use of digital technology. By some estimates, these grants are expected to boost real GDP by 3 quarters of a percent by 2023 and more if these grants are well invested.

The European economy has struggled for many years and has never really recovered from the impact of the global financial crisis back in 2008.

The international monetary fund recently suggested that an ambitious approach to implementing key structural reforms should be part of Europe’s economic recovery plans. Time will tell…

New Zealand

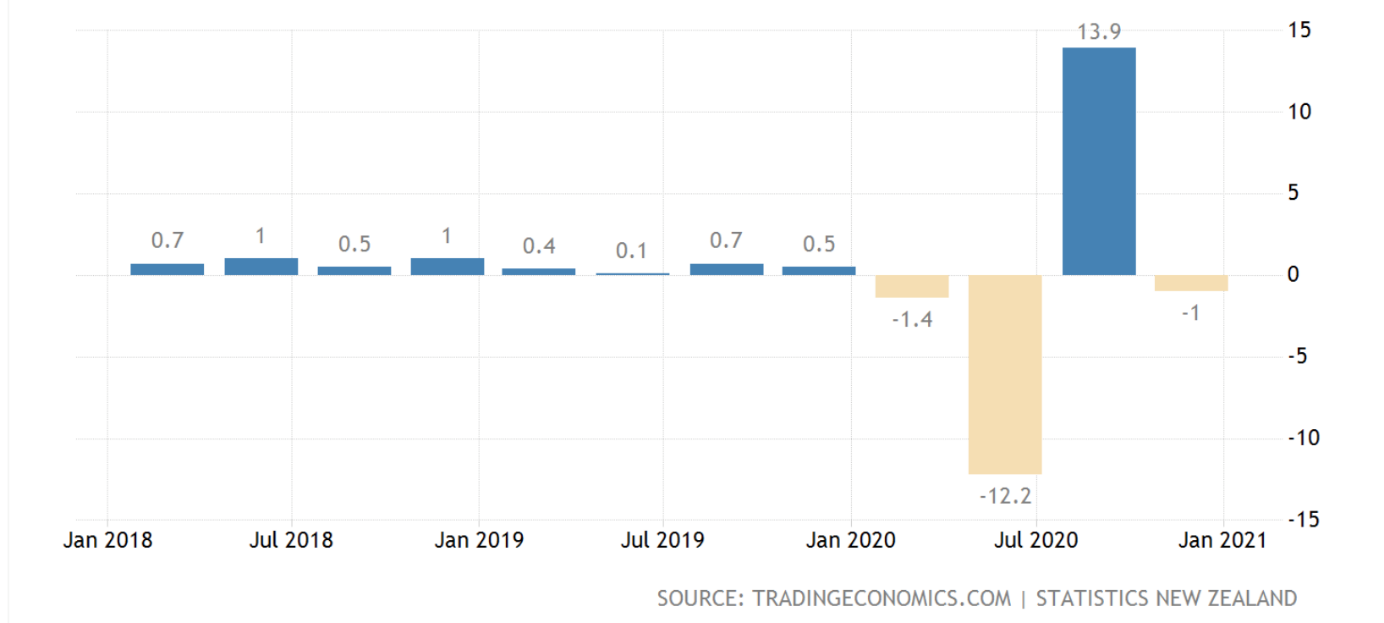

New Zealand GDP

The above graph tracks the economic growth (and contraction) of the New Zealand economy.

The New Zealand economy shrank by 1% over the last quarter of 2020. Drilling down and looking across the economy, primary industries were down by 0.6%, services rose by 0.1%, and goods producing industries fell by 3.2%.

Over the 12 months to the end of December 2020, economic growth shrank by 2.9% over that 12-month period.

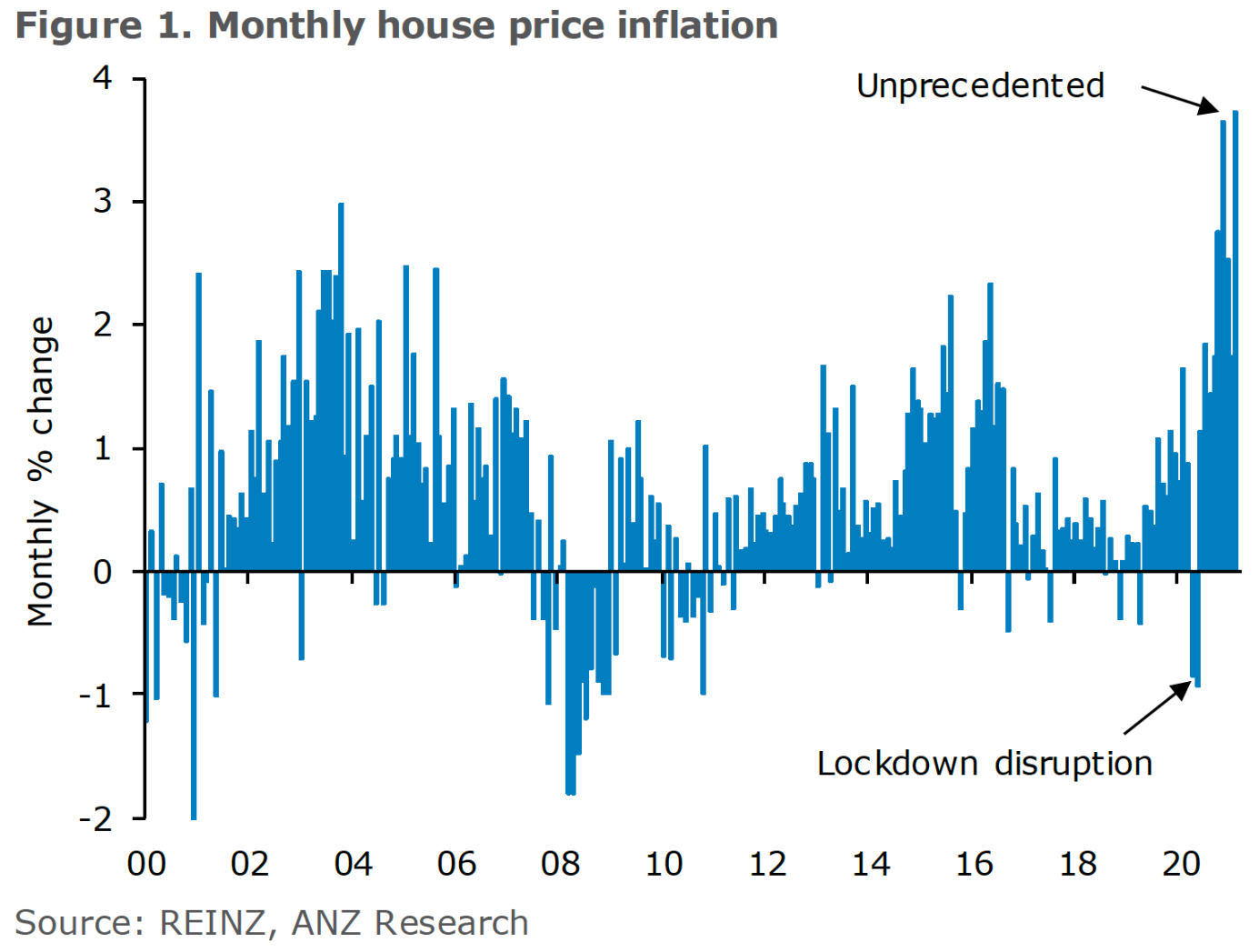

The above graph tracks the movement in residential property prices.

The above graph confirms the strong rise in residential property price inflation which has now become political. Hence the introduction of strong measures that many landlords will not be unhappy about.

Specifically, the increase in the 5-year bright line test to 10 years will be a speed bump for those turning properties over in order to benefit from short term gains. For longer term property investors, it’s likely to be less of an issue.

For property investors that are highly geared with debt, the loss of tax deductibility on the interest expense does seem somewhat Draconian and will be disincentive for some.

Whilst I doubt this would see the property market crashing as a result, it may remove a layer of investors which, as intended by the government, may help to slow the rise of property prices.

Landlords of course are also dealing with the recently introduced healthy homes legislation, making property ownership more troublesome for some landlords that are less prepared to meet those compliance requirements.

The above graph tracks the world commodity index, the New Zealand index, and export prices.

As the above graph shows, commodity prices have surged. This is sometimes considered an indicator of better times ahead. Hopefully this will translate into economic growth in the year ahead for New Zealand.

To Summarise …

Simply, the global economy looks set for a period of growth as it emerges from the clutches of the coronavirus. We’re not there yet and the coronavirus continues to mutate, but so far has been increasingly contained in some countries. The ongoing rollout of vaccines will help.

Also ongoing central bank support, low interest rates, and reductions in unemployment will help to deliver increased economic growth over 2021.

Rising interest rates and inflation, particularly in the US are worth watching.

Back here in New Zealand, the surge in residential property prices has forced the labour government to take action and it will be interesting to see how this helps housing affordability for first time buyers.

I cannot resist making the point again that many New Zealanders approach to getting ahead in life generally remains based on buying and selling property to each other, hoping that the price of housing will continue to rise. After all they say, that’s what is done for the last 30 years so therefore it must be locked into the genetic fabric of property behaviour and investing, right?!

What we know is that when the set of conditions and circumstances surrounding a particular outcome change, so too does the outcome.

With New Zealand residential property prices among the most expensive in the world by several measures, this does not mean that house prices may not still continue to rise. Indeed, if we see borders freeing up in the future, and people immigrating to New Zealand, the current demand pressures will remain strong, possibly continuing to place upward pressure on house prices.

The point here is that expensive house prices are not a guarantee of future rising house prices.

Indeed, they are a signal to be careful. Further, I like to point out the fact that deductibility for borrowed funding for existing property is being phased out whereas owning one’s own business still entitles the business owner to deduct interest costs.

That’s not a reason to get into business but one of the many reasons that being a business owner can be superior to investing and residential property.

I’m not suggesting that residential property is not a worthy investment. I am strongly promoting the idea that business is about productivity and innovation, not leveraging debt against property because that’s what everyone’s done in the past and it’s simple to understand. What do you think?

The sooner we invest in productive assets like business, or even building new housing, the more productive we as a nation will be.

The New Zealand economy and those of us that live in it will also be all the better for it in the future.