Is Slowing Global Growth Going To Be Dangerous?

Market and Economic Update – Week Ended 8th March 2019

Peter Flannery CFP AFA

“If you have one economist on your team,

it’s likely that you have one more than you’ll need.”

Warren Buffett

The Markets

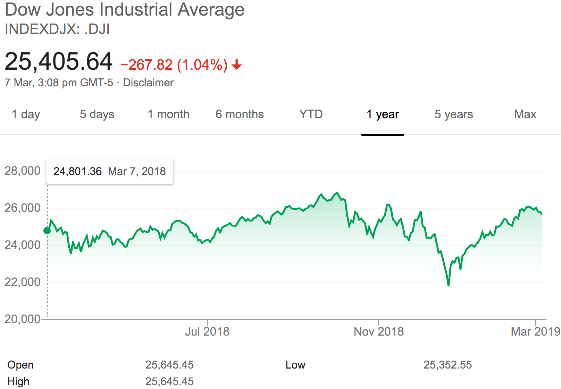

From a market perspective, the US share market is behind over the last six (red chart) months and ahead over the last 12 months.

Generally, markets are alert to indicators of ongoing slowing global economic growth. Since 2003 (yes, that’s 16 years ago!), I have mentioned continually the global economic status that I refer to as ‘deflationary funk.’ The global economy does not follow a set of rules or guidelines and in general terms, waits until difficulties or even crisis erupt before taking action (sounds a bit like climate change). The point here is that the global economy is not currently operating in ideal conditions. There is more debt than is fundamentally sound, interest rates are low (a symptom of deflation) and economic growth, whilst okay, is not stellar. Anyway, global economic growth is largely propped up by monetary stimulus, one way or another, from central banks.

Still, I am looking as closely as I can and I do not see global economic Armageddon anytime soon. As you know, we refer to those events as “black swans”. There are plenty of ‘grey swan’ events. For example, the default of a large global bank and indeed the global banking system, along the lines of what we had over 2008 on three occasions, is what I would call a ‘grey swan’ event. They can become ‘black swan’ events, depending on how they are managed. Anyway, we have had a period of reasonable economic growth over the last few years, which appears to be slowing down now. Of course, this is an opportunity for the scaremongers to point to a potential black swan just around the corner. Again, I cannot see it. What about you?

Markets did incur a notable but not significant amount of turbulence over the last quarter of 2018. As we travel through March 2019, most of the decline in markets (but not quite all, as the red chart above shows) has been recovered. It is business as usual it seems – steady as we go.

Annoyingly, prices remain expensive and I did not get too excited over the last quarter of 2018, recommending lots of buys whilst markets were down. That is because the decline meant prices were less expensive rather than cheap. Also, I am aware that interest rate rises, up until very recently, have been a potential threat to market prices, not to mention the slowing global economy. In other words, whilst I am not pretending I can predict the future, there is a real possibility of more turbulence ahead. In the immediate future through, with interest rates, it seems in many countries around the world, remaining at all time lows or close to all time lows, that interest rate threat appears to be further into the future than it was just a couple of months ago.

ECONOMIC UPDATE

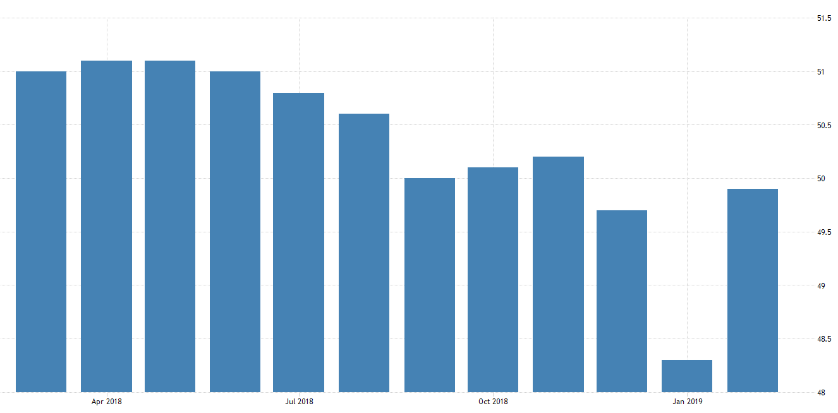

The Caixin China General Manufacturing PMI

Manufacturing in China is slowing down.

The recent Purchasing Managers’ Index (PMI), shows China’s manufacturing sector continues its downward trend. The latest Purchasing Managers’ Index (PMI) delivered a 49.2% number for last month. This is down on the 49.5% number in January and below the all important 50.0% threshold that distinguishes expansion from contraction. This is not a number that highlights a so-called ‘black swan’ event but it is an indication that the Chinese Government is continuing to battle with slowing economic activity in China.

Although it is difficult to calculate, it could also be partially as a result of the US/China trade negotiations and those tariffs having some impact on the Chinese economy. Recent numbers show that factory activity has dropped to its slowest pace over the last three years. The strong rhetoric around trade tariffs between China and the US appears to have softened, with a truce of sorts underway, although the US chief negotiator suggested recently that there is still much that needs to be done in this area. It is not over.

Interestingly, trade tariffs are a double-edged sword. There was a report recently that Ford Motor Company has been struggling a bit, as they let several thousand of their workers go, on the back of poor sales in China. Still, the Chinese economy generally continues to expand and Chinese banks saw record lending in January, which is an indicator of ongoing strong activity in China.

It would not surprise me, if over the next 12 months, we see reports out of China suggesting their economic growth is dropping below the 6% annual growth threshold for the first time in many years. This is far from game over for the Chinese economy and in my opinion, is not cause for alarm. As I have said many times, the Chinese Government are vigorously managing the Chinese economy. They appear to be doing what ever it takes to maintain economic stability.

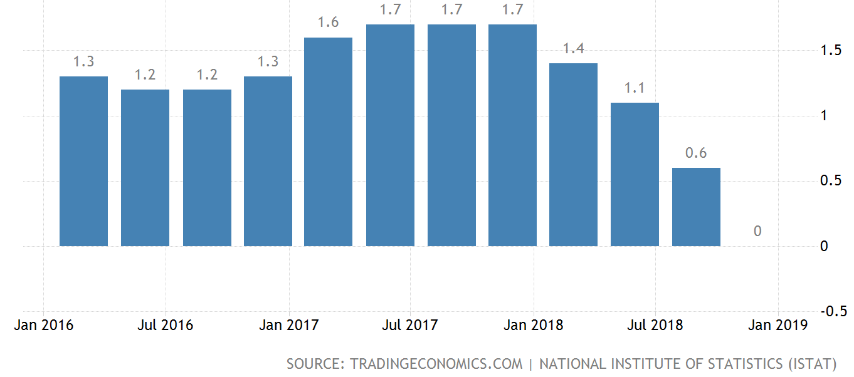

Euro Area Economic Growth (GDP)

Economic expansion in the Euro area remains fragile.

The Euro zone quarterly economic growth number was confirmed at 0.2% in the fourth quarter of 2018. This number came in slightly above the previous period’s revised figure of 0.1%. The expansion appears to be driven by exports, household consumption, along with the usual support from central bank stimulus, including low interest rates, as well as relatively cheap oil prices. The German economy looks to have stalled in the fourth quarter of 2018, after having already contracted in the July to September quarter 2018 for the first time since 2015. Further, Italy’s economy contracted for the second straight period by 0.1%, in theory placing the country into a recession for the third time over the last 10 years.

Italy’s GDP

Economic activity in Italy appears to have slowed more sharply than expected over the second half of 2018. Expansion measured by GDP fell 0.1% in the third quarter of 2018 and has likely contracted again in the fourth quarter of 2018, producing what economists generally define as a ‘technical recession’ or two straight quarters of declining economic growth (as measured by GDP). From what we can tell, businesses appear to be cutting back on some of their investment plans in Italy, which has shown up in recent surveys. A slowdown in global trade is also having some impact on the Italian economy too.

Italy has had its share of non-performing bank loans, however they appear to be under control for now. That means the level of troubled loans is slowly reducing but still at a high level. Restrictions of capital flows globally would still impact severely on Italian banks, creating a ‘grey swan’ event right there. However, the cost of bank credit currently remains relatively low, thanks to central bank intervention keeping things stable for now.

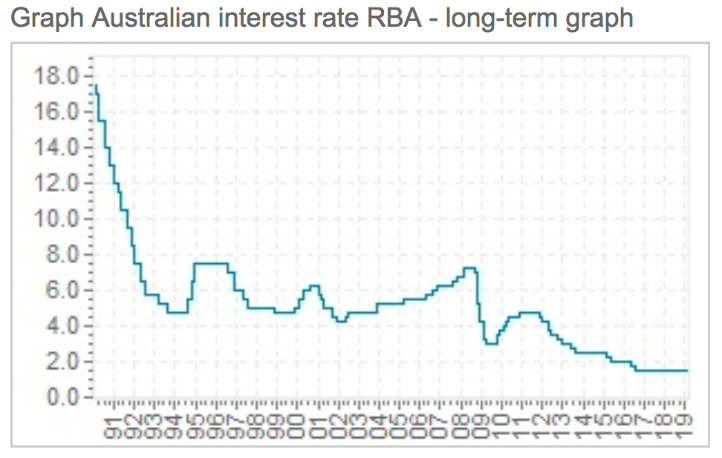

Interest Rates Australia

Note the flat line towards the right hand side of the above graph.

At its meeting on March 05 2019, the Australian Reserve Bank decided to leave the cash rate unchanged at 1.5%. The Reserve Bank Governor in Australia will be watching the global economy slowdown and watching very closely the back and forward banter between Australia and China, with regards to coal and other matters that potentially could put a strain on Australian/Chinese relations.

That could mean putting trade at risk. This is important because China is Australia’s number one trading partner. Although we will need to see how this plays out, I am not convinced that Australian/Chinese relations are in peril and nor therefore is trade between the two countries at risk. Sure, that could eventuate, however that is not the case right now in my view.

By the way, Japan is Australia’s second largest trading partner and third in line is the United States of America. New Zealand is Australia’s sixth largest trading partner and the United Kingdom is number seven for Australia. I include the above chart on interest rates in Australia as further evidence of ongoing ‘deflationary funk.’

It is a global phenomenon and not one that is isolated to just one or two economies.

It also looks stubborn and protracted, not going away any time soon.

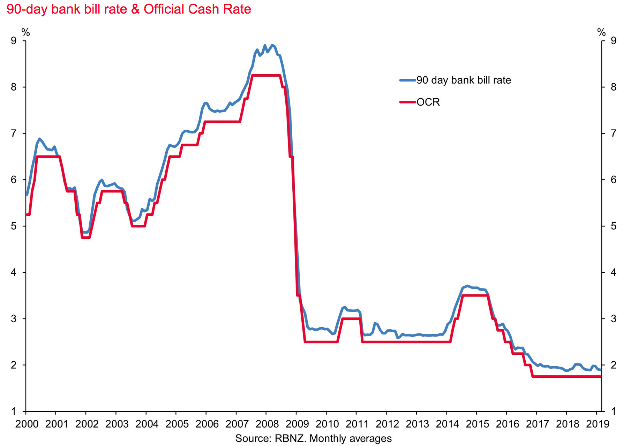

Official Cash Rate New Zealand

Interest rates in New Zealand remain on hold also.

Like other central bankers around the world, the New Zealand Reserve Bank Governor, Adrian Orr, will be watching the global economy, along with a variety of other key variables. He will respond with interest rates, which as he says, will likely either move up or move down or flat line, depending on market conditions. Stating the obvious, we have low interest rates flatlining and on hold until 2020 possibly, more evidence of global deflationary funk.

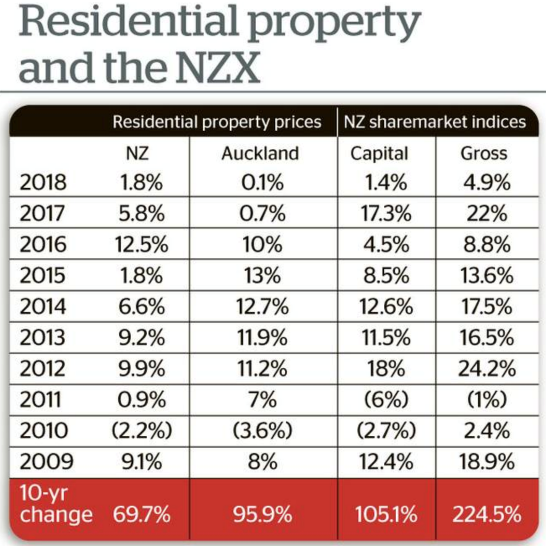

Residential property and the New Zealand share market compared.

From memory, it was Brian Gaynor from Milford Asset Management who generated the above chart a while back. It is quite a good chart because it does highlight the reality of productive assets versus real assets. Sure, we are not getting into leverage and other aspects. The point here is that productive assets, long term, generally outperform other assets.

Capital Gains Tax (!?)

The initial iteration of the tax working group paper outlined a proposal whereby capital gains tax would be applied to New Zealand direct shares, however the foreign investment funds regime (FIF), under which international investments are taxed, would remain in place. The bottom line is that international investments, therefore, would be treated more favourably from a tax point of view than New Zealand direct shares. Although possible, I believe it is unlikely that this will remain unchanged. There is lots of discussion and debate that has yet to take place (probably by around midway through 2020 (?)). After that will we have some idea of how things might look for investors. I will keep you posted …