Interest Rates are Worth Watching

Market and Economic Update – Week Ending 8th June 2018

Peter Flannery CFP AFA

“If you have one economist on your team,

it’s likely that you have one more than you’ll need.”

Warren Buffett

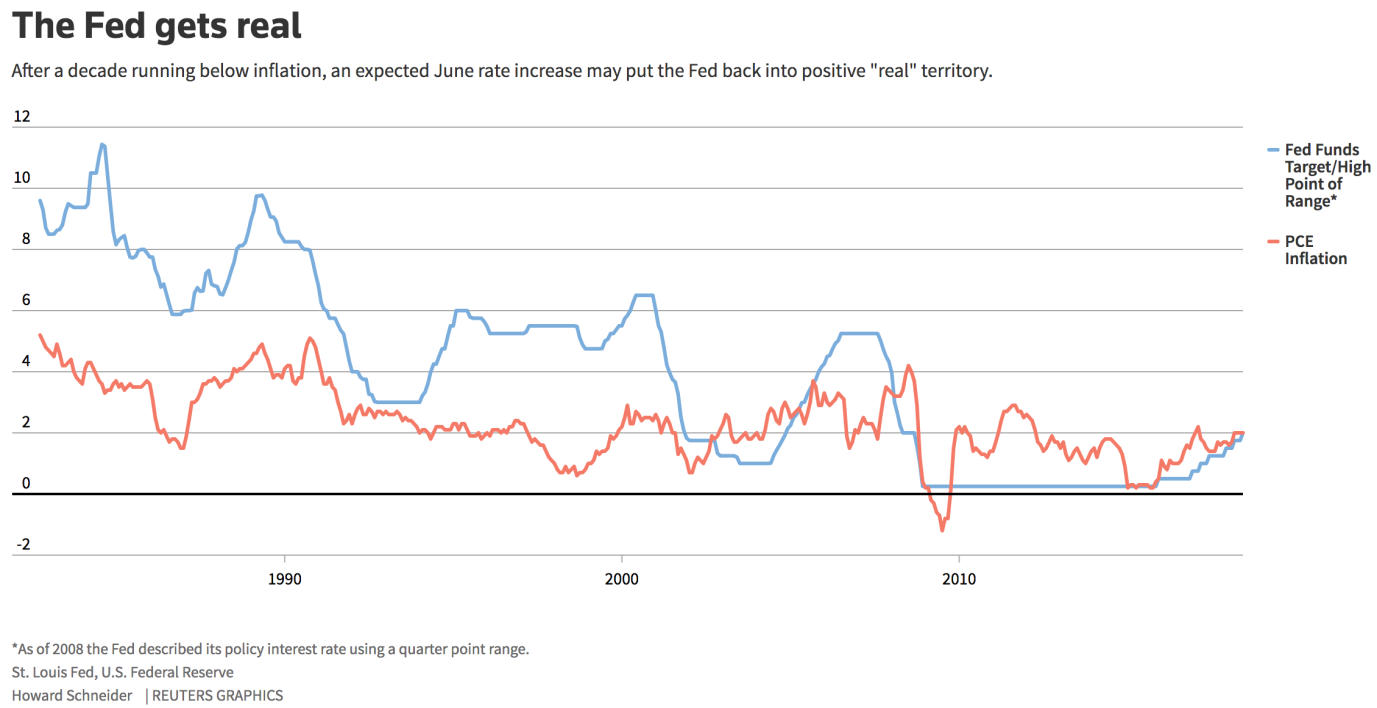

Policy makers in the US are aiming for a “neutral interest rate”.

- Interest rates are important because they can determine asset prices. To be clear, they can impact on the value of your house, the cash up value of your direct share portfolio along with other investments. Apart from market sentiment which at times can be unwieldy and brash, increasing interest rates generally mean higher costs and reduced cashflows. Reduced cashflows on capital assets tend to deflate the capital value or the trading price of that asset. With interest rates in the US continuing to track upwards, some are now questioning just how justifiable further increases are over the next 12 months?

- Increasing interest rates in the US will eventually flow on to New Zealand. Even though at this stage it looks as though the Reserve Bank of New Zealand has the official cash rate on hold until sometime in 2019 at 1.75%, nonetheless the cost of borrowing could still increase. That is because the bank that you and I deal with if we are borrowing money will borrow from the central bank or from offshore sources at a particular rate and then lend it out at a higher rate. The more riskier the banks perceive the environment, the bigger the spread or the margin between the wholesale rate (what the banks pay for their money) and the retail rate (what you and I will pay for money if we borrow).

- So, it is not the official cash rate in New Zealand that will push up interest rates any time soon but rather that spread between the wholesale rate and the retail rate, particularly if global markets become unstable. For example, over the last two or three weeks I have mentioned Italy as a potential source of turbulence in Europe and therefore the global economy (because of Italy’s economic size). In my opinion, the global economy is still caught up in what I have termed “global deflationary funk” which may still see interest rates rise, but the question is, how far and for how long?

- Further evidence of deflationary funk can be seen in Australia where the central bank recently kept interest rates at a record low as it waits for signs of wages growth and price inflation along with a drop in unemployment. The Reserve Bank of Australia has not adjusted interest rates since August 2016 after a series of interest rate cuts from November 2011 that ultimately took interest rates in Australia down to 1.50%.

- However, in Australia business conditions and the economy are generally positive with recent data showing the Australian economy growing at an annual rate of around 2.8% – not bad. Still, unemployment remains stubbornly high at around 5.5%, wages growth tepid and inflation stubbornly slow. Property prices in Australia are mixed but have certainly come off the boil over the last year or so. Whilst some expect an interest rate hike in Australia by the end of the year, I would be surprised and believe this would be an ambitious move by the Reserve Bank and difficult to deliver any time this year. That’s deflationary funk for you!

- Meanwhile back in Italy, Moodys ratings agency last week placed Italy’s debt rating on a downgrade review. Moodys reckons that the country faces “significant risk of a material weakening” in its fiscal strength because of its new anti-establishment coalition government. The problem here is that the new government could see some of the required economic reforms stalled or even reversed which could have a significant impact on Italy as well as the European Union. Predictably, Moodys are seeking greater clarity from the new government as to its plans – good luck with that! The new government by the way are calling for a flat tax and universal income. I am not sure if that lines up well with EU requirements for members which could be a starting point for further market uncertainty.

- Moodys took action because Italy’s new coalition between the five star movement and the league was granted authority to form a government recently. The parties have vowed to challenge the European Union’s budget rules and are looking to slash taxes whilst at the same time increasing spending. By the way, Moodys Italian debt is currently ranked at Baa2, that is two notches above “junk” status. Global markets are a bit perturbed about what is going on in Italy and it could be interesting. However, I am looking for some volatility …

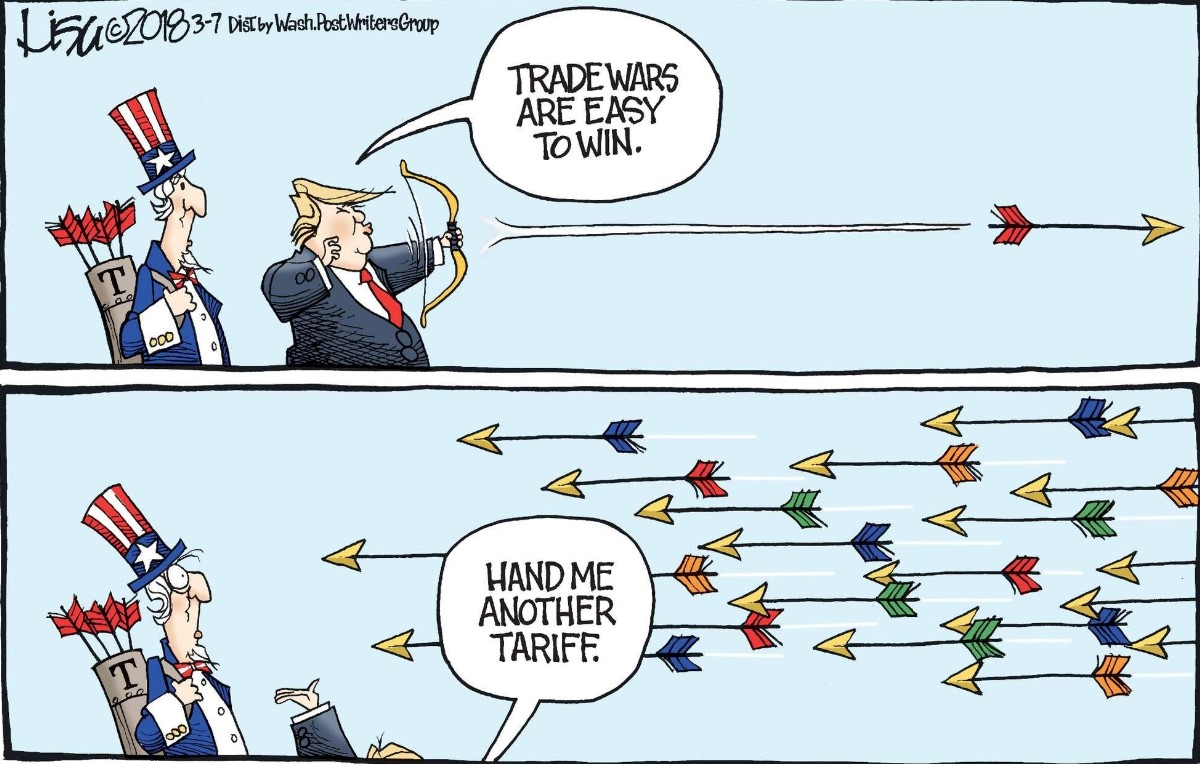

- Trade tariffs remain in the news and indeed are back in fashion once again as Donald Trump recently imposed a new set of heavy tariffs on foreign steel and aluminium imports on its close allies – an interesting move. The other day the Commerce Secretary Wilbur Ross, announced hefty tariffs on aluminium and steel imports from the European Union, Mexico and Canada that will go into effect pretty much immediately. Steel imports from those countries will be taxed at 25% and aluminium imports at 10%. These are significant numbers when you consider that the average tariff rate on US – EU traded goods is under 3%.

- The response was almost immediate. Mexico announced it will impose tariffs on American imports in retaliation. The European Trade Commissioner Cecilia Malmstrom said Europe would impose rebalancing measures and take other necessary steps to protect the European Union market. For example possible targets for Europe could be tariff increases on the likes of American bourbon, jeans and possibly motorcycles.

- This is a relatively big deal because the European Union, Mexico and Canada are among the top four largest trading partners of the US. Whilst it is too early to say and at this stage not worth worrying about, trade tariffs in themselves are really the warning shots and what could unfold into a trade war. Basically that is where two sides become locked in a cycle of retaliatory tariff increases. The result would be an impact on economic growth which would not take long to unsettle markets and cause asset prices to decline (yippee!!).