Do Trade Tariffs Equal Trade Wars?

Market and Economic Update – Week Ending 6th April 2018

Peter Flannery CFP AFA

“If you have one economist on your team,

it’s likely that you have one more than you’ll need.”

Warren Buffett

China responds to America.

- After Donald Trump initiated his first round of tariffs, China has come back with an increase in the tariff rate on pork products and aluminium scrap by up to 25%. China is also imposing a new 15% tariff on around 120 other imported US commodities. Interestingly, these tariffs mirror Donald Trump’s 25% tariff on imported steel and 15% on aluminium.

- US farmers exported nearly $20bln of goods to China in 2017. China is the number three market for US pork and I suspect US farmers will be starting to worry.

- Does “tit for tat” trade tariffs mean that we have a trade war? I suspect that it depends how you define a war. Without doubt though, the game is on between the US and China. No point in speculating at this point as to what it means for you and I. It is too early to say yet.

- With China having mirrored the US’s initial thrust into trade tariff brinksmanship, it will be interesting to see how China responds longer term and ultimately, how it all plays out. China will have thought this through, thoroughly. Neither country will win, and certain industry sectors will be affected, should it continue to play out on the current path. Not only that, jobs in those sectors, could also be affected.

- Of course, for us as investors, this means volatility, which we like. The more the better.

- Still in the United States of America, the ISM manufacturing index, came in slightly weaker the other day than expected but remains at a high level. Interestingly, there is increasing anecdotal data suggesting increased cost pressures from the steel and aluminium tariffs, including some panic buying, which of course in turn has depleted some stocks. This is notable because it may lead to some further inflationary pressures. In the current economic climate, not only in the US but globally, that would be a good thing. However, it can become a problem if it gets out of control.

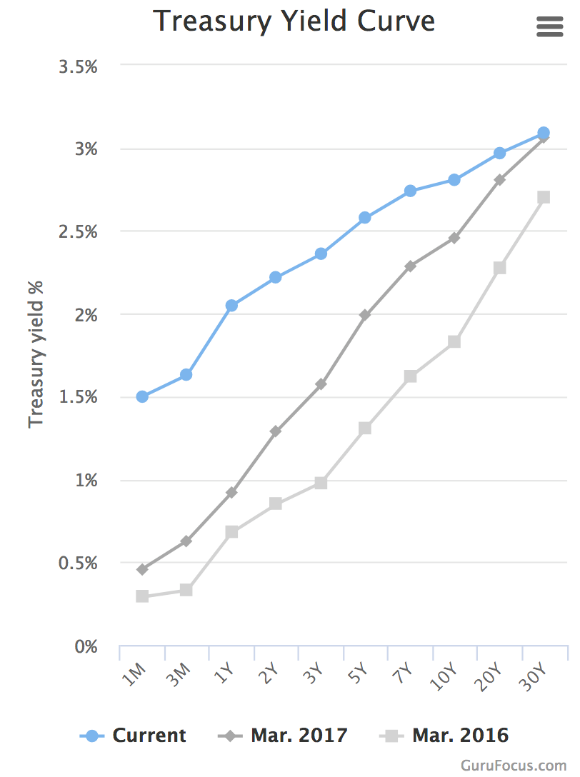

Interest rates continue to rise in the US.

- The above chart shows that over the last three years, interest rates in the US have continued to rise. In my view, this is a critical factor to watch moving forward and will impact on asset prices globally at some point. The timing is always difficult to pick in advance; however, I would regard it as inevitable. I am not suggesting, as investors, we start to worry but rather, ‘keep our powder dry’ so to speak and wait for the markets to react and then progressively look to increase our exposure to growth assets. Interest rates therefore look as though they will continue to rise, although at a slow pace for now.

- The proposed US Federal Reserve interest rate increase in June is widely expected. The US overnight rate will be higher than our official cash rate (OCR) in NZ for the first time in more than 17 years. This will ultimately lead to pressure on interest rates here in New Zealand.

- The US Treasury 10-year yield is tracking at around 2.78%. The Chinese 10-year rate is 3.75% and the New Zealand 10-year rate is at 2.75%.

- Interest rates remain on hold here in New Zealand. At this stage, rates in New Zealand look to be on hold until at least mid-2019. This has seen some shorter-term mortgage interest rates decline slightly over the last few weeks. Interesting, because this is in direct contrast to what is happening in the US. Indeed, some interest rates in the US are now higher than New Zealand, which is not impossible but certainly unusual. Generally, we would expect interest rates in New Zealand to be higher than the US because the New Zealand economy is a smaller, narrower and theoretically more risky economy, than the larger, broader and significantly more powerful US economy. Therefore, something has got to give at some point. With interest rates rising in the US, it is more likely that at some point, interest rates will rise here in New Zealand.

- Property prices across NZ, in some areas, continue to flatten or decline. This is interesting because this is without the impact of rising interest rates. It appears that there may be some minor reduction in demand but moreover, the changes to lending conditions over the last couple of years have definitely had an impact. So too will, perhaps to a lesser extent, the extension of the Bright-Line test, whereby those investors who sell investment properties within five years (currently it is two years), will be up for tax on the gains. This type of change will not cause a market collapse but does take the edge off property price rises. That is because it takes some of the players out of the market, reducing demand. Having had ideal conditions for nearly three decades, residential property in New Zealand, could be facing a different time ahead.

- In Australia, interest rates remain on hold at 1.5%. The Australian economy grew by 2.4% over 2017. The Australian Central Banks forecast is for faster growth over 2018, with business conditions positive and non-mining business investment increasing.

- Inflation in Australia remains low, with both the CPI and the underlying inflation rate tracking at just below 2%. It appears that inflation in Australia is likely to remain low for some time. The Central Bank in Australia is forecasting CPI inflation to run at just a bit over 2% in 2018.