Oil Prices Are Up

Market and Economic Update – Week Ending 5th October 2018

Peter Flannery CFP AFA

“If you have one economist on your team,

it’s likely that you have one more than you’ll need.”

Warren Buffett

Oil Prices Are Up

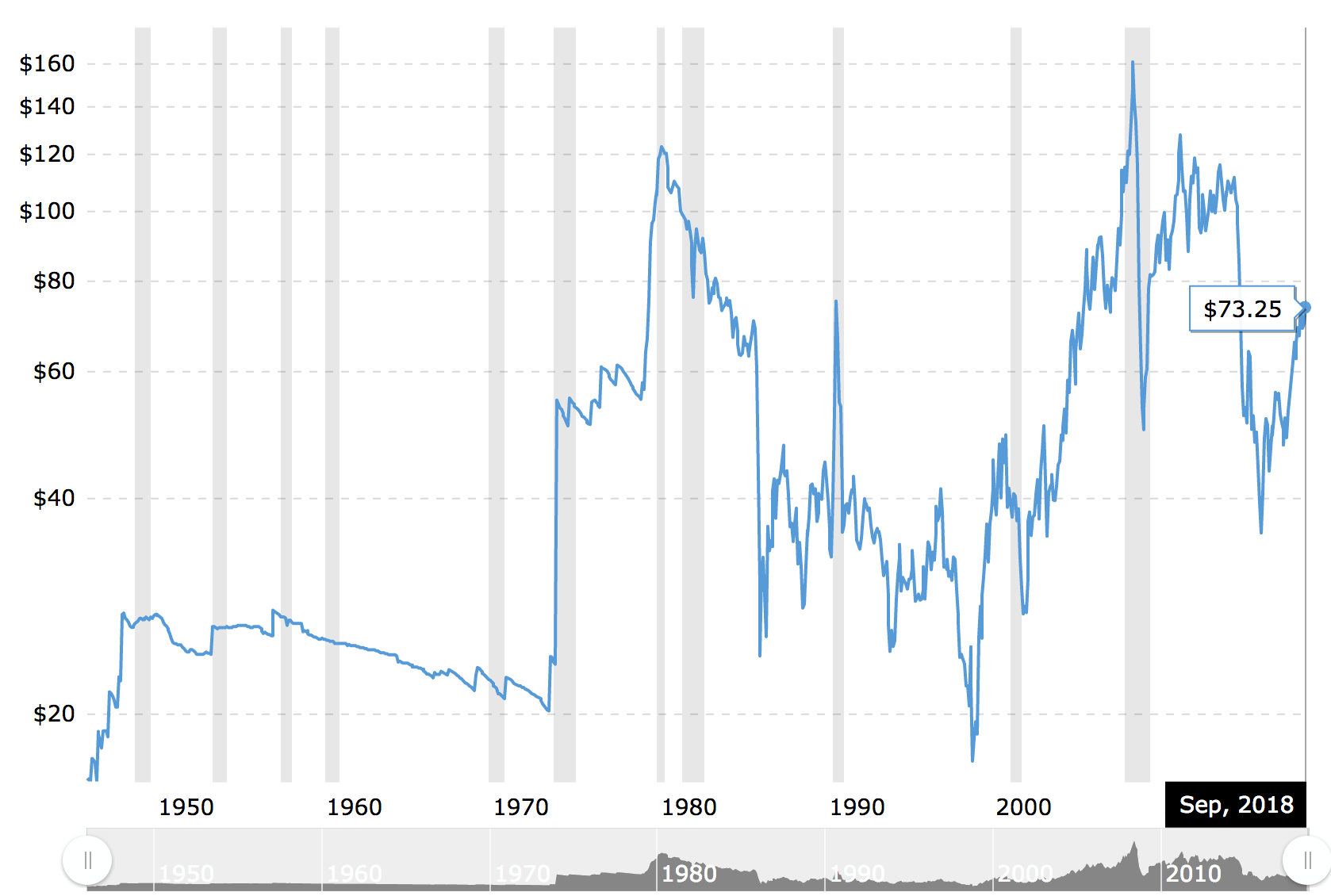

Oil prices continue to rise.

Oil prices appear to be continuing their upward trajectory with the benchmark Brent crude rising 1.1% to $82.28 per barrel recently. West Texas Intermediate is up to $72.48.

Oil prices remain on a so-called bull run, with concerns that US sanctions on Iranian crude oil exports could result in much tighter conditions once they take effect in November – that is not far away.

The Russian President, Vladimir Putin, recently agreed with President Trump, that he thinks oil prices are too high but in the same breath, blamed Trump for those high prices. Obviously, he is referring to the sanctions on Iran and Venezuela, putting pressure on oil prices with markets fearing a shortfall in global supply. The question is, is the fear of short term short supply of oil the same thing as peak oil? What do you think?

The movement in the S&P 500 (share market index). Are you happy or unhappy after looking at this chart?

It is all a matter of perspective really – isn’t it? We know the US economy is reasonably strong. Not only that, over 80% of companies have announced their profits as earning season is now well underway. Indeed, this whole earnings season thing is strongly followed by most participants in the markets, all around the world. Quarterly profit announcements are considered appropriate in order to keep investors informed of what is going on with companies.

That has led to analysts, share brokers and other investors to focus strongly on these quarterly announcements, which are taken very seriously. Indeed, good businesses with sound economics can see their trading prices decline sharply if the market becomes uncomfortable even with a near miss (e.g. actual earnings coming in lower than expected). Sometimes these near misses (earnings miss or revenue miss) can signal troubling times ahead for a particular business. More often than not though, they are just reporting a period of time that was less favourable than expected – there is nothing actually wrong with the business. Of course, the media would not have us let the underlying truth get in the way of a good story though!

ECONOMIC UPDATE

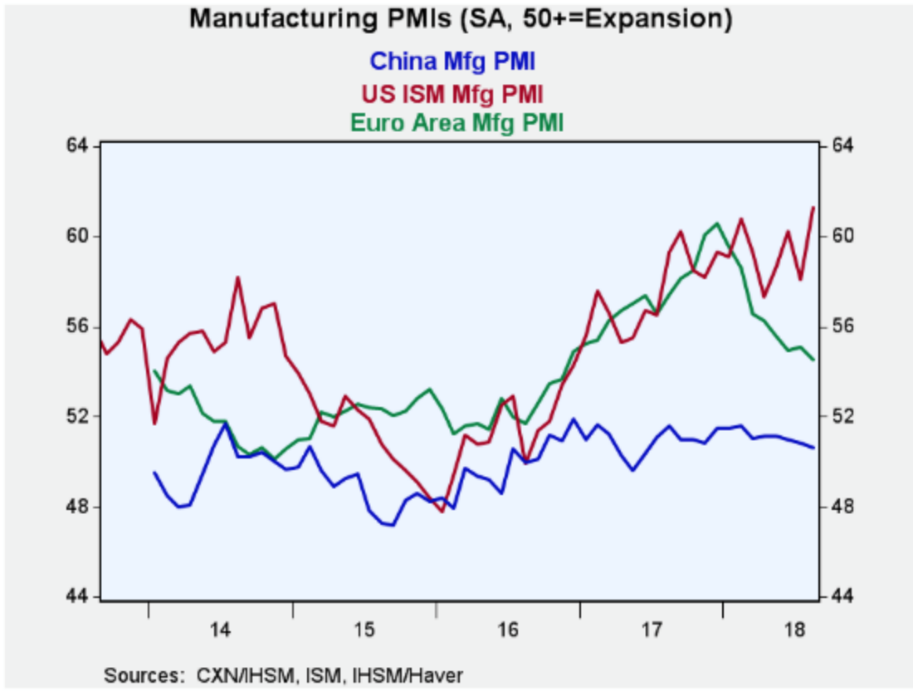

Despite trade tariffs, the US economy looks to be doing okay.

Around the world, manufacturing and production expansion is evident almost everywhere. That synchronised, global economic expansion still looks to be underway. Interestingly though, manufacturing and production expansion appears to be slowing in China, whilst the US is on a roll!

The chart above appears to suggest that the US economy was actually doing fine without imposing tariffs on Chinese imports, however the trade deficit between the US and China recently hit $50 billion for the month, up from $47 billion in June. What is important about this number is that the deficit was determined by import growth because US exports declined by 1% over the previous month. The actual trade deficit with China rose to $31 billion (65% of the deficit) and the European deficit was $17 billion. China and Europe represent the largest deficit, hence Donald Trump’s focus on China and Europe.

At the end of August, Chinese financial reserves were estimated at US$3.1 trillion. This suggests that China has significant foreign exchange power to influence its growth and the engagement in its partners’ capital markets and trade. Anyway, China has other trading options apart from the US, so trade sanctions will impact China but it is not the end of the world for China nonetheless. Cutting to the chase, China will likely play the long term game anyway.

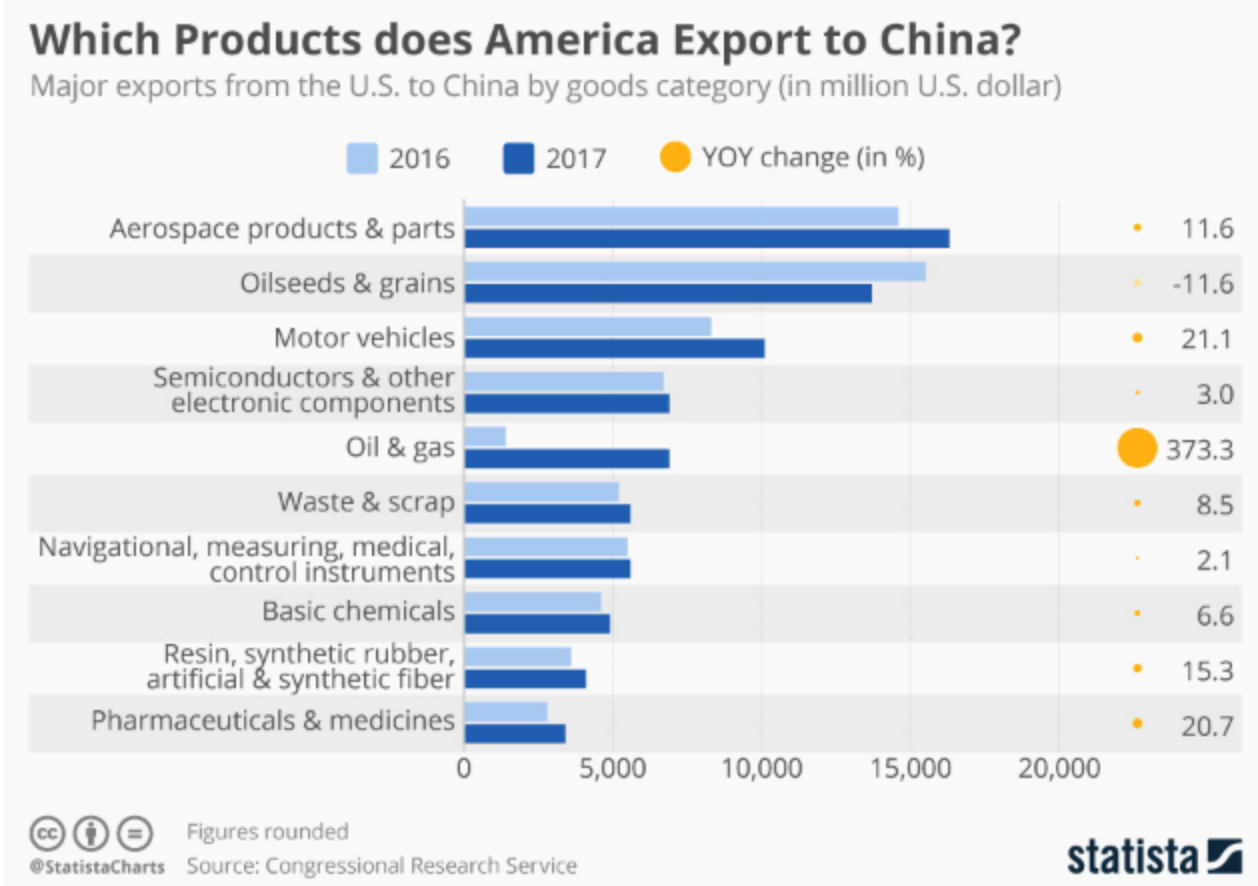

The above chart shows which products America exports to China and the change from 2016 through 2017.

As a point of interest, the US trade account is currently represented by approximately US$3 trillion of imports that exceed the $2.5 trillion worth of exports. This annualised trade deficit of US$0.5 trillion represents 2.5% of US economic growth, as measured by GDP.

As I mentioned before and I will say again, because it is worth repeating, when it comes to trade tariffs and a potential trade war, I suspect, whilst China cannot win the short term game, it will likely play the long game.

Argentina just received a $57 billion loan from the IMF. That is Argentina’s biggest loan ever. About $15 billion has been dispersed already, with the remainder to be dispersed over the next three months or so. However this loan comes with a strict set of restrictions, including Argentina’s commitment to a zero deficit for 2019, along with limits on certain central bank actions.

A new trade deal is born between the US, Canada and Mexico, which replaces the old NAFTA trade deal. It is called USMCA. Donald Trump will be pleased, as in theory, this new trade deal between the US, Canada and Mexico puts China, Japan and the European Union on notice (that America has other options when it comes to trade). However, the deal needs to be approved by congress before it is implemented on 1 January 2020.

The Reserve Bank of Australia kept official interest rates on hold at a record low of 1.5%. However, banks have moved independently of the Reserve Bank of Australia (RBA) recently increasing rates by around 0.25 percentage points due to higher costs of international borrowing. This is not a significant increase, however it is an indication of what may lie ahead in the future (increased offshore funding costs for New Zealand and Australian banks).

Back here in New Zealand, the latest QV house price index nationwide shows that values fell by 0.6% in the three months to September. This leaves the average national value at $676,427. So far, the arrival of spring has not had much of an impact on values. Whilst market prices appear reasonably subdued in some areas, listings have increased quite a bit in some areas. There is some evidence that limited supply in some areas, along with ongoing demand and stable interest rates, is helping keep values around current levels. Growth in residential property prices in the main areas appears to be slowing or flatlining.