Is The Global Economy Sliding Into A Bad Place?

Market and Economic Update – Week Ended 5th April 2019

Peter Flannery CFP AFA

“If you have one economist on your team,

it’s likely that you have one more than you’ll need.”

Warren Buffett

The Markets

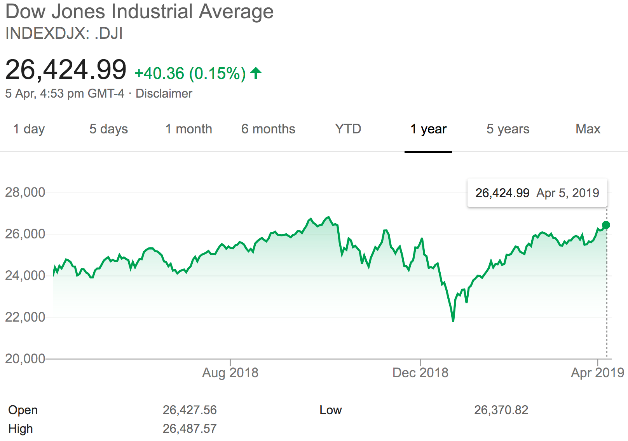

The red chart shows that the Dow Jones index is still below where it was six months ago, however the green chart shows that over the last 12 months, the market is up.

Prices rise and prices fall – same old. Isn’t it interesting how some investors get very jumpy about price movement? What about you?

Many of my clients are quite resilient when it comes to volatility. They have been through a lot over the last 20 years or so, and are well conditioned to prices rising and falling.

Although I still have a handful of clients who worry about markets and appear to listen (too much) to what goes on across the internet, I have an increasing number of clients who truly understand pricing volatility.

They know that the trading price and the intrinsic value are two different things. They know that declining prices means better buying. They are not just putting on a brave face. Indeed, they want to know if I am not recommending that they buy when prices decline – why not !?

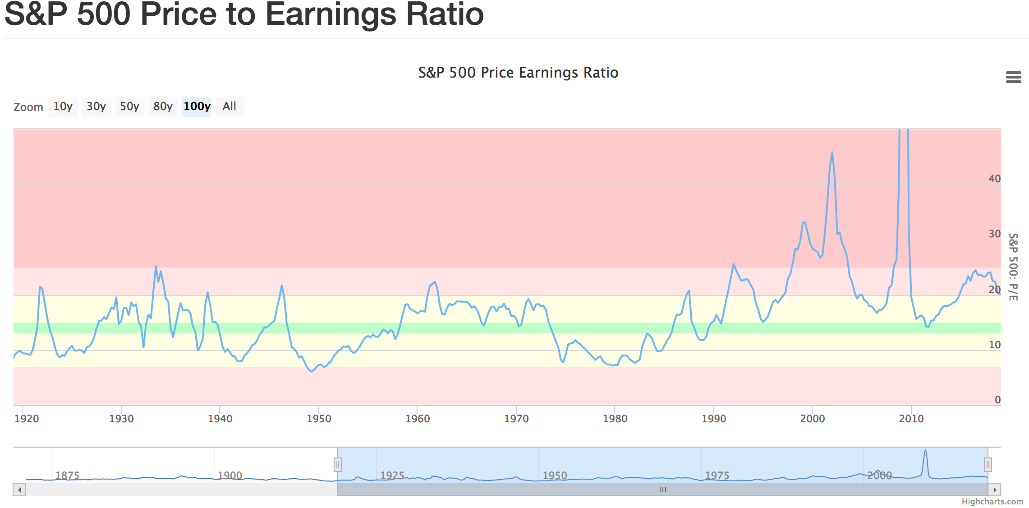

The most recent event was the volatility over the last quarter of 2018. It was noticeable and possibly scary for those that worry about pricing volatility but it did not come to much. The challenge then was that prices were simply less expensive rather than cheap. Still, as the chart below shows, prices are not in bubble territory.

The above chart provides a 100 year look back on the Standard and Poors 500 index in America. Note the spike toward the right side of the chart, which of course was the lead up to the 2008 global financial crisis.

The US market and other markets are generally somewhat expensive but not in bubble territory and certainly not cheap. The light blue line (in the chart above) tracking up and down in a random fashion measures the price to earnings ratio across the S&P 500 index. It provides a general guide as to the relationship between trading prices and the earnings of the businesses in that index.

When trading prices rise too far above their underlying earnings, it is only a matter of time before prices correct, which is perfectly natural and normal – nothing to be concerned about. Indeed, lower prices are good, not bad. Referring to the chart above, it is clear that the P/E ratio shows that markets are not cheap, sitting at around a little over 21, which is not too bad against the long run average of around 17. What this means is that, as an investor, we need to be investing in quality businesses because most businesses trading across the market will be at prices that embellish and exaggerate their underlying earnings. That is because the market is happy for reasons that likely have little to do with each and every business in the market.

Now that the first quarter of 2019 is behind us, we will soon see how the earnings of companies across the US fared. Some estimates suggest that earnings may have declined over the first three months, which is not something that the market likes to hear. Anyway, the S&P 500 has surged 15% year to date, while the NASDAQ is up nearly 20%. This is where we need to be a bit careful.

Should news suddenly emerge that earnings are worse than previously thought and markets have been too excited and become disappointed, expect a sharp decline in trading prices. Of course, it is difficult to predict. As you know, greed and fear have little to do with intrinsic value and business.

Still, the chatter across the markets is for slowing global economic growth and potentially tough times ahead. At this stage, markets appear to be shrugging it off. To be sure, when the market is disappointed, it reacts suddenly and sharply. That is why we have cash in our portfolios, so we can take advantage of those opportunities.

So, markets appear to be somewhat expensive and not cheap but not wildly expensive either.

I suspect a contributing factor to market buoyancy over the last couple of months is the US Federal Reserve, not only signalling that rate hikes are on hold, but also advising that they will pause quantitative tightening (QT) at the end of 2019.

That, in my opinion, is a very surprising move, suggesting that the US Fed may be quite concerned about where things could be heading. This is not to say that the US Fed is looking to predict where things will go but rather to anticipate and attempt to head off tough times before they become entrenched. The global economic slowdown I imagine is likely on their mind right now.

ECONOMIC UPDATE

The new NAFTA deal is looking fragile.

We are now more than six months down the track after America, Mexico and Canada agreed to a new deal to govern more than $1 trillion in regional trade. Things are starting to look a bit uncertain. Back in September, US President, Donald Trump, demanded that the previous trade pact be renegotiated or scrapped. The process has been dragging on. The point here is that American presidential elections are coming up in 2020 and also Canada holds its federal elections in October. The delay means that businesses are uncertain about the environment that they will be operating in. Whilst many commentators believe the deal will eventually be approved, the longer it takes to get it all across the line, the more likely it will not.

Brexit continues to struggle – limited progress here. Theresa May recently asked for an extension until 30 June 2019 and also agreed to make contingency plans to take part in European Parliament elections on 23-26 May 2019, if need be. Mr Tusk of the European Council proposed a longer timeframe. He suggests that the remaining 27 European Union nations offer Britain a flexible extension of up to one year to ensure that a potentially chaotic exit by Britain is less likely. Everyone knows that a no deal Brexit is difficult to calculate and could see some potentially damaging effects, not only in Britain but also Europe.

Not unsurprisingly, there is some notable banter flying across social media. For example, a top Siemens executive said on Monday that the chaos over Brexit is wrecking the United Kingdom’s reputation as a place to do business and turning it into a laughing stock. “Enough is enough. We are all running out of patience” said the CEO of Siemens in the UK.

EasyJet, the discount carrier, warned recently also that continued uncertainty over Brexit was reducing demand for flights to Europe. That means damage to bottom line profits and puts jobs at risk. The CitiGroup CEO, Michael Corbat, recently said that CitiGroup would be forced to move European assets out of London if banks in Britain lost the ability to sell their services in Europe. By some estimates, financial services companies have announced plans to shift assets worth £1 trillion into the European Union according to consultancy Ernst & Young. This could mean that circa 7,000 jobs could also be expected to move. I wonder what that might do to property prices in London!

Airbus CEO, Tom Enders, said in January that a disorderly split from the European Union would cause Airbus to redirect future investment away from Britain. Airbus employs approximately 14,000 people in Britain and said it could not guarantee its factories would survive. These are just a few comments. There are many more.

The point here is that this type of banter is damaging for market sentiment because it is difficult for business owners to make decisions around their future and commit to investing. It is a bit like the proposed capital gains tax here in New Zealand and the impact it will definitely have on small business owners if implemented as proposed. Industrious business owners want to see some reward for their hard work over many years and the risks they take. The mere threat of the CGT is already a disincentive for some.

Anyway, the uncertainty around Brexit is impacting now and will continue to flow through to the economy in the months to come. At the risk of stating the obvious, an orderly agreement to exit the European Union (unless they want to stay) is required – soon. Unfortunately, the politics of it will not allow that to happen easily.

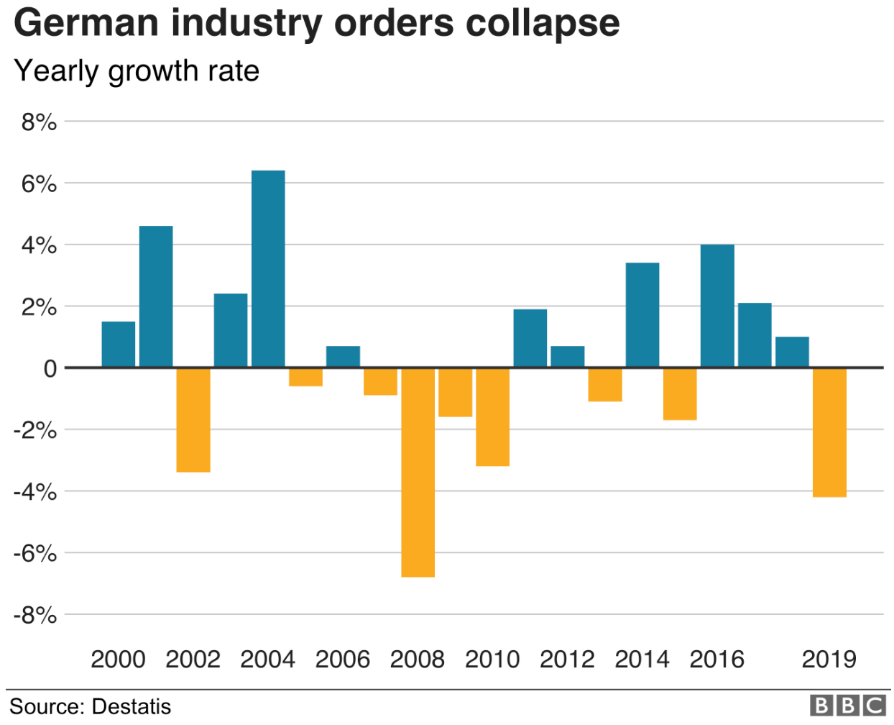

Dramatic headlines aside, the above chart shows industrial orders have hit a very soft patch all of a sudden.

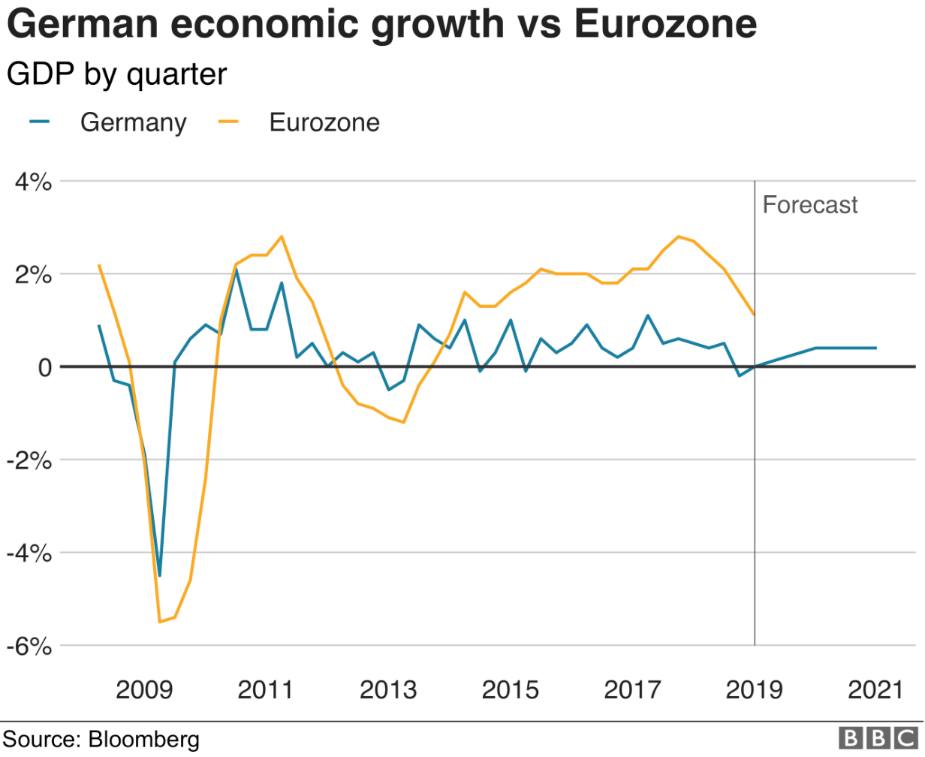

Germany’s economy appears to have hit a difficult patch. Looking at gross domestic product (GDP), we can see this measure shows a decline in the third quarter of last year by 0.2% and failed to show much growth in the following three months thereafter. In theory, a recession is generally defined as two consecutive quarters of contraction, in which case, Germany appeared to have a near miss.

Germany’s economic growth has been flatlining since about 2011 – not good.

The good news is that the European Union has seen economic growth over the last several years, albeit supported by low oil prices, low interest rates and central bank intervention. Still, we will take whatever growth we can get – right? Italy’s economy appears to be in recession and Germany’s economy continues to struggle. One of the reasons, of course, is that China’s economy is slowing down. With China and Europe being significant trading partners, this is having an impact on economic growth across Europe. There is also some local factors, such as new emissions testing procedures, that have been implemented in Germany. This has slowed down car production over the last year. Believe it or not, low water levels on the Rhine, have restricted cargo traffic too. This is important because the river is an important transport route for German industry. The short of it is that the European economy, whilst a sophisticated market with strong management processes in place, remains economically fragile and continues to need everything to go right for the economy to continue to grow.

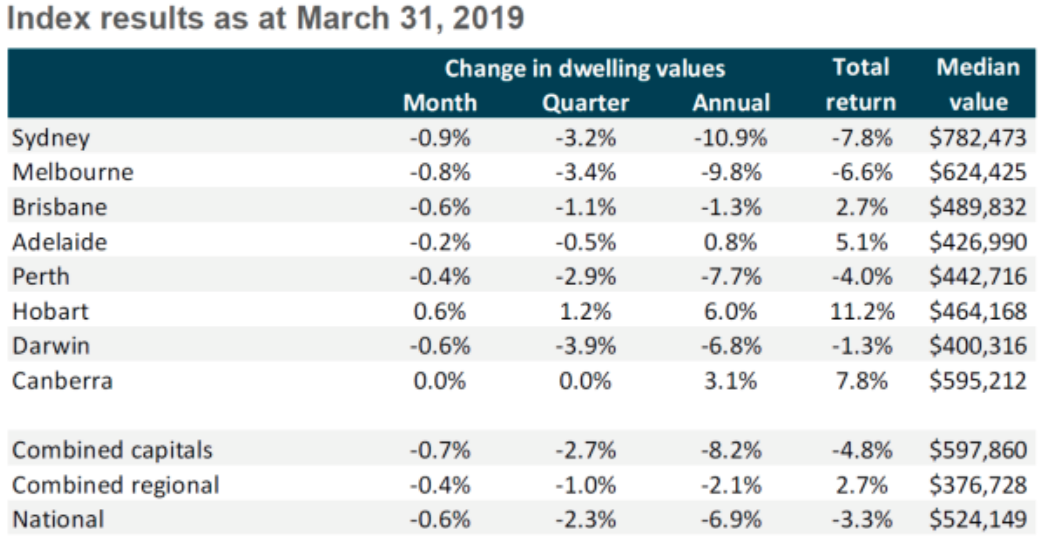

Australian Residential Property

The above chart shows pricing movement across Australia as at 31 March 2019.

As the chart above shows, property prices have been mostly in decline over the last quarter and certainly the last month (apart from Hobart). Whilst many view this as negative and certainly, it does create a drag on economic growth, for investors, price declines are a good thing for investors looking to buy. Price declines are also welcome news to first time homeowners in Australia too. Prices continue to decline and whilst there has been the slightest bit of an indication that the decline might be slowing, the decline remains well underway. The outcome, I suspect, will be that prices will decline to a point where they may remain lower than previous but likely still not cheap compared to fundamental norms. That is for a number of reasons, one of which, of course, is low interest rates. What caused the decline in property prices? Among other things, in 2014 the Reserve Bank of Australia imposed tighter lending conditions on banks throughout Australia, which means that less money was lent. This reduced the strong demand pressure, allowing property prices to flatten out and indeed prices then started to decline. The Governor of the Reserve Bank will not be concerned about declining prices, although will be watching the impact those declining prices have on market confidence and inevitably, economic growth.

Interest Rates

Interest rates remain on hold – why?

The Reserve Bank of Australia kept the cash rate at a record low of 1.5% at its April meeting the other day, as widely expected. This is a record period of policy inaction for the 32nd month in a row. Apart from the local economy, the Australian Reserve Bank, like other central banks, will be keeping an eye on slowing global economic growth. Slowing economic growth affects us all to a greater or lesser extent.

Federal elections in Australia are moving ever closer. Australia’s Labour Party tax proposals include axing their cash refunds of excess franking credits, adjusting the law around negative gearing and increasing capital gains tax. Understandably, non-Labour voters are not too happy about it. However, like New Zealand, there is a fair amount of debate that will take place prior to any tax policy being implemented. Still, it looks as though there will be some increase in taxation on Australians. There is increasing noise around the idea that it seems unfair to penalise those in the community that work hard and are industrious, looking after themselves and paying their fare share of tax. Why should they work hard and be penalised for it?

New Zealand

Confidence across New Zealand continues to wane.

Whilst drilling down into the specific data is not all negative, however 40% of those surveyed expect it to be tougher to get credit, which I agree with. Remember, the New Zealand Reserve Bank is looking to implement reasonably strong demands around increased security in order to make banks safer in the event of another global credit crunch. We know how this worked out in Australia, where similar measures were introduced in 2014, although it did take until 2018/2019 before we saw property prices decline. I would not be surprised if that had a similar impact here in New Zealand. Also, the threat of a possible capital gains tax will be having a real impact, particularly on business owners. Residential property has become very mixed, with Auckland in a reasonably strong decline. Residential construction intentions (Auckland) have basically fallen off the cliff over the last few months. These surveys are somewhat anecdotal but we know that global growth is slowing and therefore this type of survey is worth keeping an eye on.

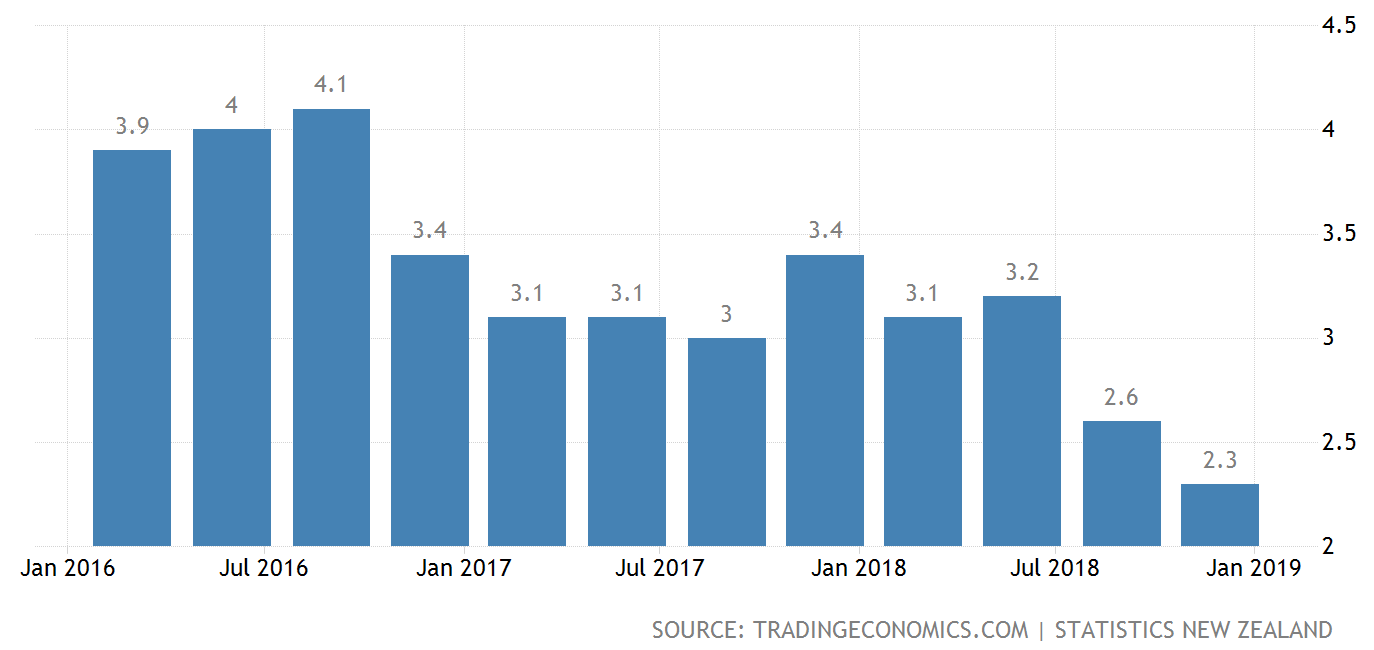

Economic Growth (GDP)

Economic growth in New Zealand is reasonable but definitely slowing down.

Economic growth in New Zealand has been okay over the last few years but is definitely slowing down now. Nothing to worry about just yet, however there are a number of headwinds looming, such as: slowing global economic growth, declining property activity across New Zealand, the threat of capital gains tax impacting not only on sentiment but also on investment intentions to name a few. None of this, of course, concerns us as value investors. Indeed, it may provide some much needed volatility for us, so that we can finally have the opportunity for some better pricing – hopefully!