Trade ‘War’ Update

Market and Economic Update – Week Ending 28th September 2018

Peter Flannery CFP AFA

“If you have one economist on your team,

it’s likely that you have one more than you’ll need.”

Warren Buffett

Trade ‘War’ Update

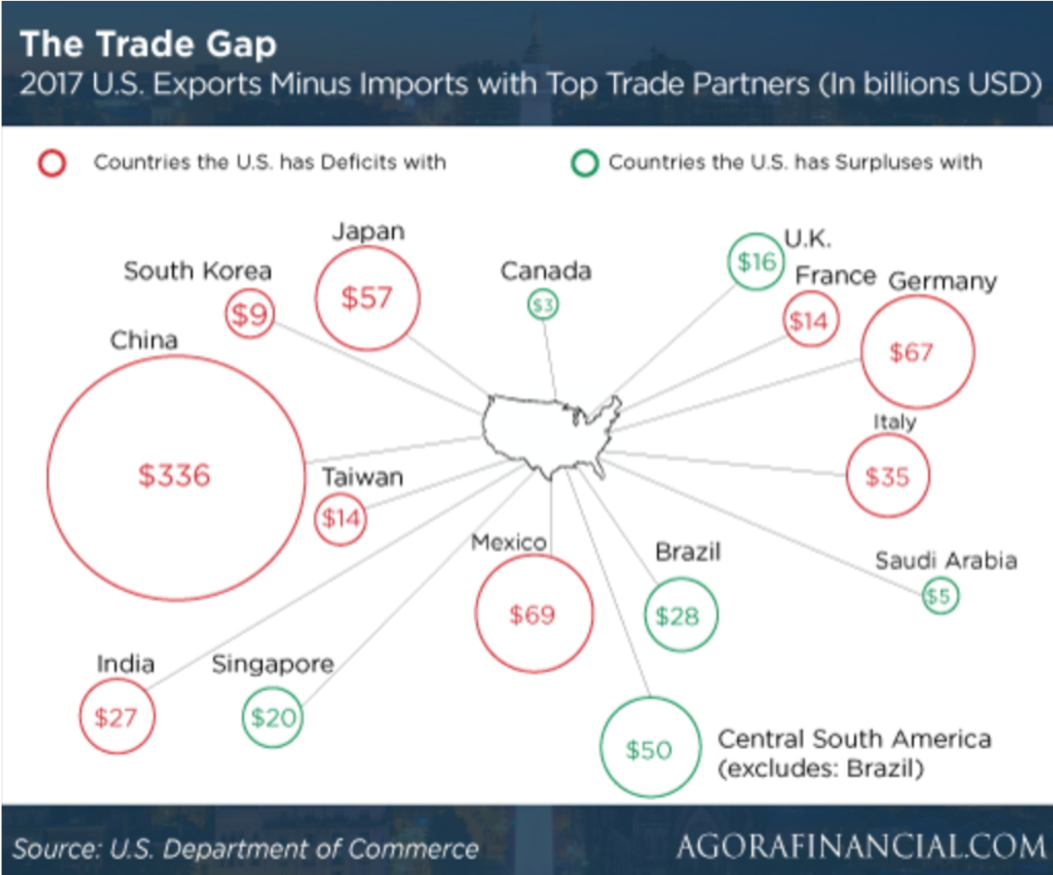

The above chart shows why Donald Trump is unhappy about the trade imbalance with China.

Who will win the trade war between China and America? The answer, in my opinion, is America. Whilst it will not be straightforward and there may even be some ‘blood on the streets’ as it were, America I believe, will win because China exports more to America than America exports to China. That means America can apply a lot more tariffs to Chinese exports than China, by comparison, can apply to American exports into China. This does not mean that there will be no pain for Americans, however the logic of this situation is difficult to overlook.

The US trade deficit, as the chart above shows, is mostly due to the four trading partners; China, Mexico, Japan and Germany. As you can see, China is over 60% of the total. No wonder that Donald Trump has China in his sights. As you know, President Trump also just concluded a new deal with Mexico, that will help reduce the deficit that currently exists between the US and Mexico.

By some counts, the US and Japan currently maintain good relationships and have agreements in place already. This then basically suggests that China and Germany will continue to be the target of President Trump. What will be interesting is to see how Germany and China respond, as Donald Trump continues to press forward with trade tariffs. A declining renminbi or deutschmark is one option that exists for both China and Germany, however too much action in this area, I imagine, would provoke a strong reaction from Donald Trump – let’s face it, he is not known as one to back down easily.

So, the trade tariff ‘tit for tat’ between China and the US started out with two tranches of US$16 billion and US$34 billion. Then came a second round at US$200 billion, looking for the Chinese to cave in. We now have an additional US$267 billion strike, which takes the game to a total of US$517 billion, which is greater than the total Chinese imports of US$505 billion in 2017. Interesting!

Although we will have to wait and see how it plays out, we know that whilst in some ways, America does have the upper hand here, China on the other hand are comfortable playing the long game. They do not need to win now, especially if they can come up with a long-term game that hurts Americans enough that inevitably, Donald Trump is either removed or simply gets to his ‘use by date’ and there is a change in policy. Although you never know, I doubt the trade tariff game will be over anytime soon. If not, it then becomes a question of what damage is inflicted on the parties involved (mainly US, China and Germany, along with any hapless bystanders caught in the crossfire).

One of the longstanding advantages that America has enjoyed has been innovation. China has been a country of copycats, although with Beijing’s plans to integrate China’s burgeoning Shenzhen and Guangzhou areas with Hong Kong and Macau, there is likely to be a push toward innovation and growth. The more resources are allocated to innovation and innovative technology, America’s longstanding innovation lead could be under threat by the political will of the Chinese Government and the sheer scale of the Chinese economy. Peter Warnes, from Morningstar, made the point recently that the worm may turn and it might be the Chinese who accuse America of Intellectual Property theft! Anyway, China is a large economy continuing to develop and does have ‘long term’ ingrained in its philosophy. China will play the long game.

Anyway, what is going on in America? Recent numbers out of the US show consumer CPI inflation in the US has slipped slightly, coming in at a bit lower than expected at 2.7% per annum for August. It was 2.9% in July. That slight easing in inflation meant that real earnings in America actually made some ground for a change but the gain was only 0.2% over the whole year. So, wages in the US are rising, however inflation is pretty much keeping pace. That means real wages growth in the US in minimal. Citizens are not much better off.

The federal budget deficit came in at US$214 billion for the month of August, which is more than most were expecting and takes the 11 month year to date total to US$900 billion. By comparison, the deficit reached US$1.4 trillion in 2009, which was in the midst of the global financial crisis (the GFC). By some estimates, the 2018 deficit will be 4.5% of GDP, less than ideal. The American economy is growing and this is the time to rein in these budget deficits.

Small business America is feeling good.

The National Federation of Independent Business (NFIB) keeps an eye on small business sentiment in America. The monthly index clocked in at 108.8, which is better than the previous high set in 1983. That is the best reading in 35 years. This is important, because small business is the back bone of most economies and a healthy vibe from small businesses can be a positive indicator for what lies ahead. The index takes into account such variables as expected credit conditions, getting rid of inventory easily, expected business conditions, a good time to expand and so on. Currently, the index appears to be dominated by real business activity that contributes to economic growth. That is things like strong capital spending plans, investment in inventory, job creation plans and strong capital spending plans. Small business in America is doing its fair share of contributing to economic growth across the country. Tax cuts, of course, have not heart either.

Meanwhile over in Europe, the European Central Bank (ECB) kept rates on hold and is looking to do so into 2019 or for as long as necessary. They are concerned about the implications of Brexit and a possible trade war between the US and the likes of China and Germany. Anyway, things are stable in Europe, which all things considered is not bad, although there is no real light at the end of the tunnel, so to speak, in terms of sustainable economic growth – at least not yet.

Turkey’s Central Bank raised its main short-term rate from 17.5% to 24% in a dramatic effort to try and control raging inflation and to also prevent a currency crisis going from bad to worse. Global markets are becoming increasingly concerned that Turkey is another emerging market economy that may need rescuing by the International Monetary Fund (The IMF).

The Turkish President, however, will not be keen on that idea and I suspect will only go to the IMF as a last resort. That is because any bail out from the IMF means austerity measures and controls that would ultimately cramp his style.

Argentina, as you may recall, recently agreed to a loan from the IMF. Other countries, such as Indonesia, Mexico and South Africa are in that group of emerging market economies that have seen their currencies tumble, as investors flee those economies that have grown using large amounts of debt. The problem then of course becomes that debt growing bigger as the currency declines, along with the debt servicing making things more difficult for those economies. The real impact of that situation falls back on everyday citizens in those countries ultimately. Governments come and go. Inflation, by the way, in Turkey, is tracking at around 18%, which is a 15 year high for Turkey. It is likely that Turkey’s tight monetary policy will be maintained until the inflation outlook improves.

The Reserve Bank of Australia kept interest rates on hold at 1.5% a couple of weeks ago, although there are some expectations that a change in interest rates might be on the horizon. Certainly, we know that those borrowing money to buy residential property are seeing some interest rates increase as banks in Australia seek funding from offshore, which is becoming more expensive. One would expect this to flow on to New Zealand as well at some point, although we are not seeing much evidence of it just yet. Indeed, as I mentioned last week the 2-year lock in rate here in NZ has declined slightly.

Meanwhile, back here in New Zealand, the spread between New Zealand and US 10 year bonds is now at its widest point, at 43 basis points. The five year spread though is wider at 97 basis points, with the market assessing the differing outlooks for New Zealand and America. One outcome has seen the New Zealand dollar decline against the US dollar, as the US dollar strengthens and the New Zealand dollar weakens. The cross rate looks as though it could head to below 0.65c. Also, as NZ imports become more expensive, the question will be around whether New Zealand companies can pass these increases on. Petrol is an obvious example. The next question then is what impact the rising price of petrol will have on both economic growth and inflation here in New Zealand?