Why Are The Markets So Rattled?

Market and Economic Update – Week Ending 26th October 2018

Peter Flannery CFP AFA

“If you have one economist on your team,

it’s likely that you have one more than you’ll need.”

Warren Buffett

After further declines, markets have bounced back somewhat.

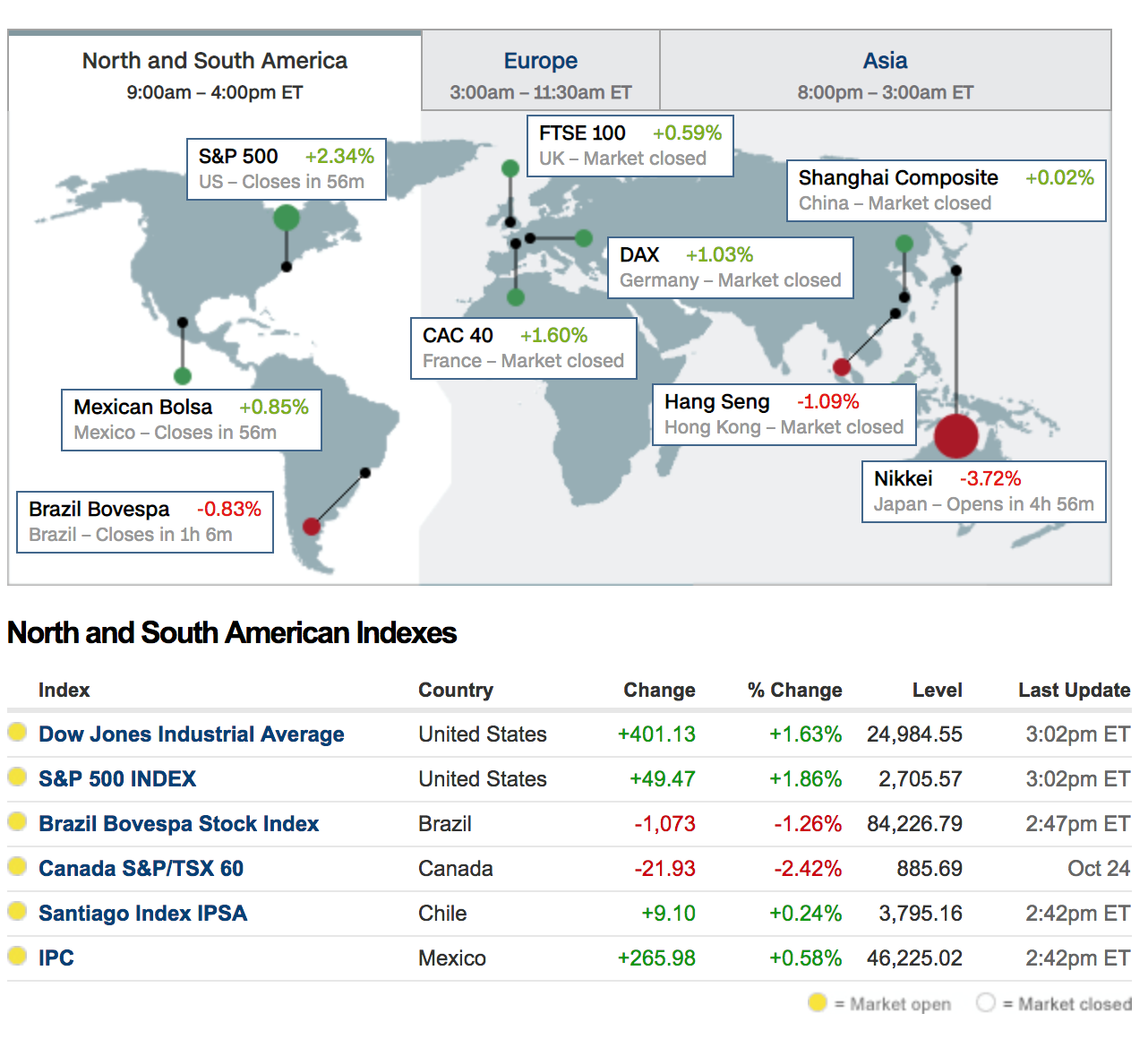

Markets remain rattled and uncertain as evidenced by the decline on the Dow Jones Industrial Average to 24,818 on Tuesday October 23, rebounding to 25,280 on the same day, then slumping once again to 24,586 on Wednesday October 24. Since then the Dow Jones Industrial Average has rebounded to 24,988 as at Thursday October 25 2018. Interestingly, as earnings of large companies are rolled out in the US, the market is very focused on the slightest bit of negative news, selling off specific stocks as any negative news emerges. The point here is that the sell-off is more of a market related issue than anything directly and substantively related to the global economy. Although linked, the markets and the economy are two different things.

At our recent roadshow I reminded us all that economic recessions and depressions can be caused by lack of demand. With a lack of demand prices decline causing problems throughout the economy. Oil prices have been falling over the last two weeks as the markets declined. Obviously, the market becomes concerned with declining sharemarket prices, that there is an upcoming slowdown in the economy on its way. That in turn can indicate lower demand for oil – hence the price of oil declining. On the other hand the bounce in the sharemarket the other day gave rise to increasing oil prices as some market participants feel a bit more confident. Markets and the economy are different … and are linked.

“Trade drag” is becoming evident in the US as companies such as Caterpillar and Ford Motor Company complain about rising manufacturing costs as a result of duties on imported steel and other raw materials. The US Federal Reserve is obviously watching the impact of trade tariffs, highlighting in a recent report that “manufacturers reported rising prices of finished goods out of necessity as costs of raw materials such as metals rose, which is attributable to tariffs”.

The US Commerce Department in another report said that the goods trade deficit increased 0.8% to $76 billion in September. Exports of goods rose $2.5 billion to $141 billion last month, boosted by shipments of industrial supplies, motor vehicles, consumer and other capital goods. However, food exports continued to decline, possibly pulled back by shipments of soya beans, which have effectively borne the brunt of Donald Trump’s trade fight with Beijing. The anticipated drag on economic growth in the US (GDP) from a deteriorating trade deficit is expected to be offset somewhat by an increase in inventory investment inside the US (Donald Trump making America great again?).

Europe’s economy performed well over 2017 particularly compared to many years prior, however there are some doubts about where the European economy is heading in the future. Growth is expected to slow down over the next 12 to 18 months as Europe deals with new trade barriers, uncertainty over Brexit and ongoing political differences that continue to undermine confidence in the Euro and keeping many banks under real pressure.

The European Central Bank estimates that Eurozone growth will slow to 2% over the coming year which is actually not that bad when you consider the challenges that the global economy has faced over the last 10 years or so. There are some reports that global trade conflicts are impacting on demand for European exports. The uncertainty of course has an impact on sentiment which in turn flows onto potential delays of investment decisions across the economy. Businesses generally do not like risk and will delay investment decisions where there is significant uncertainty. So what we have is what looks like weaker growth momentum in Europe but I would not go so far as to suggest that there is in fact a downturn in the European economy at this point.

America has hit Europe with a new round of tariffs on steel and aluminium. Germany of course being a significant exporter to the US is at the centre of Donald Trump’s efforts to make America great again. We are seeing a reasonably sharp decline in activity with Germany exports as those tariffs start to impact. The German Chamber of Industry and Commerce has downgraded its forecast for economic growth to 1.8% in 2018, down from an earlier estimate of 2.7%. Some German car makers are being hit hard by global trade tensions and some fall out from diesel scandals along with other delays sparked by a new vehicle certification system in Europe. Interestingly, BMW issued a profit warning in September, blaming continuing international trade conflicts. Also, recently Mercedes Benz who owns Daimler reported a decline in third quarter profits in what they say is a very challenging environment. Further, President Donald Trump has more than once threatened tariffs on cars assembled in Europe if the European Union does not make moves to reduce the trade imbalances with the US.

Brexit is looming with Britain scheduled to leave the European Union in March 2019. There still remains significant confusion about what this all means for businesses which is an unhealthy situation. Businesses and markets do not operate well under a cloud of uncertainty which is what Brexit apparently means for businesses. For example, BMW says it will shut its Mini factory in England for one month of maintenance immediately after Brexit because it cannot be sure of getting parts. Also, Jaguar has cited uncertainty over Brexit as one reason for putting 1,000 workers on a three day work week until Christmas. Although longer term the situation will work its way through, in the short to medium term though, the uncertainty is only growing and although it is difficult to gauge right now, it will impact on economic growth and activity in both Britain and Europe.

The European Commission rebuked Italy last week over a draft budget presented by Italy. The European Union is calling for a significant decline in spending by Italy however Italy is refusing to go along with it. Indeed, Italy claims that it has no “plan B” since the draft budget was rejected by the European Commission last week. The concern here is that ongoing friction between Rome and the European Union could place Italy’s fragile banking sector under more pressure. This in turn would be another “head wind” on Italy’s already struggling economy. This is important because Italy is the third largest economy in the Eurozone so its financial fate is important for everyone.

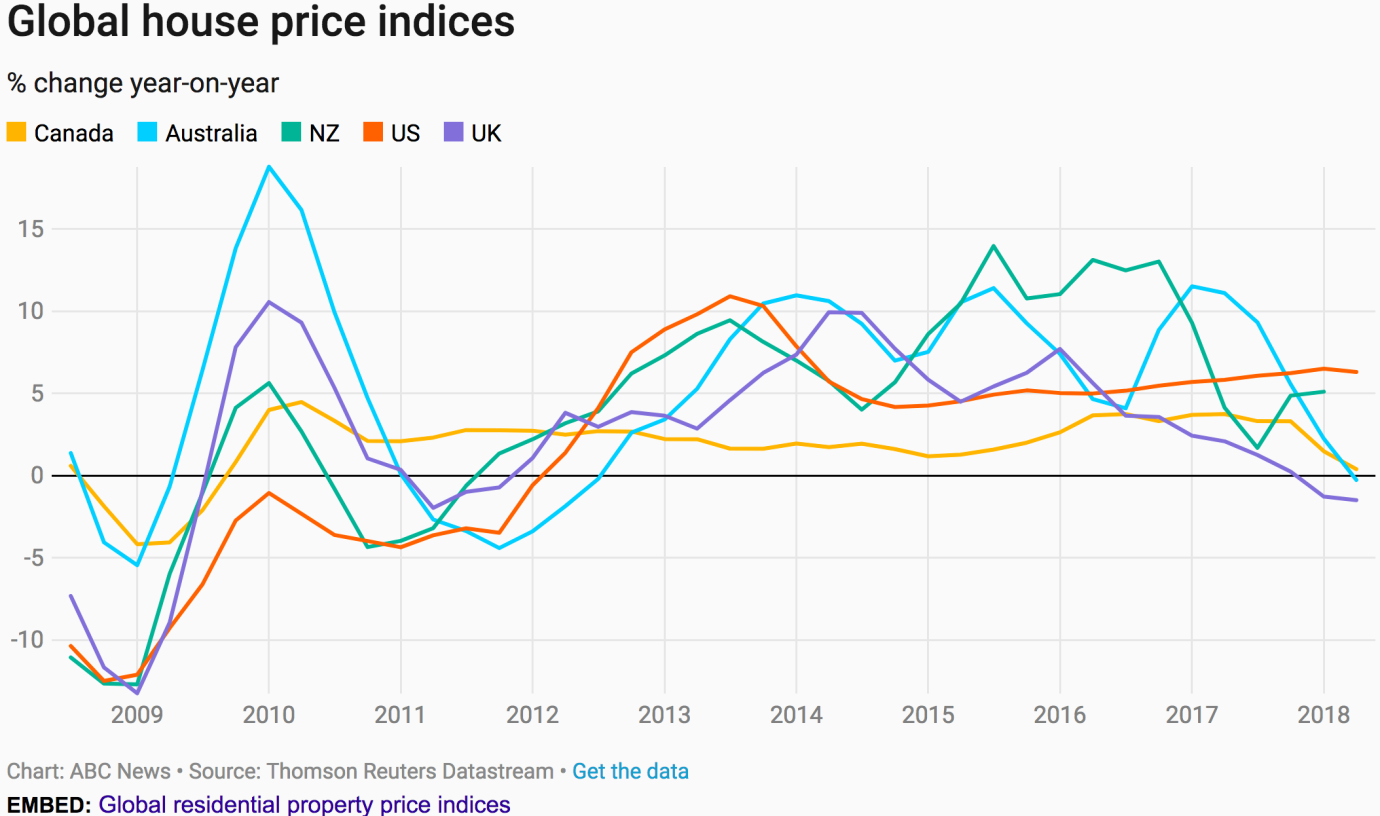

Property prices around the world are starting to moderate and decline.

The liquidity bubble has been alive and well for well over 30 years and is not over yet. The liquidity bubble is about easy money conditions, the increased use of debt pushing up asset prices and declining interest rates since around 1980 to now. An obvious challenge for property prices in the future is the normalisation of interest rates that is led by the US Federal Reserve in the US. Although long term interest rates are less of an impact, “short to medium term” can go on for many years (even decades as we have seen in the case of declining interest rates since the early 1980’s).

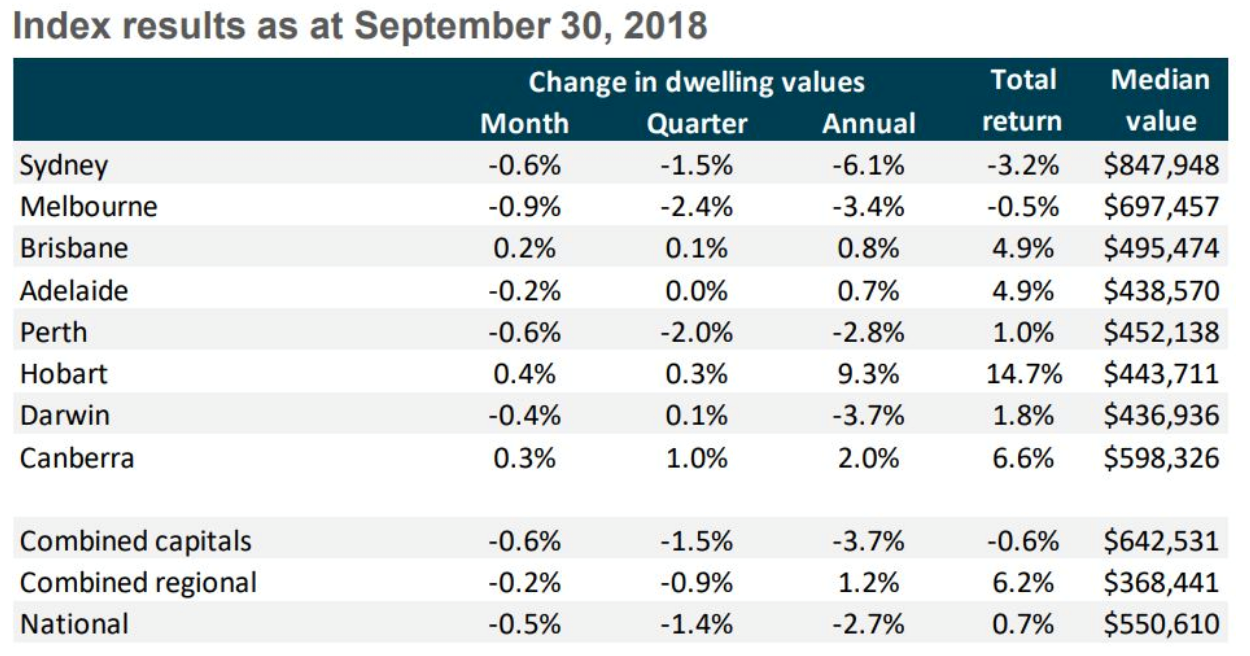

Property prices are generally in decline across Australia.

For those who believe that property prices only ever go up we only have to look at the Australian market now to see that indeed this is just not so. Interestingly, Australia embraces immigration which of course supports property prices however the banks in Australia are taking a somewhat tougher line with borrowers. This makes it more difficult for some Australians to be able to borrow money to continue upgrading or investing in property in Australia. For example, interest only loans are virtually a thing of the past in Australia but as you may know, still available here in New Zealand right now.

Banks in Australia and to some extent in New Zealand too, are now applying much greater scrutiny to borrowers’ cashflows including the types of expenditures that borrowers have in their budgets. Although somewhat anecdotal, a recent article in Australia suggested that subscribing to Netflix did not work in the favour of one borrower a few months ago (although subscribing to Netflix I doubt would be the reason any loan might be declined outright (?)). The short of it is that the borrowing game has changed for Australians and is in the process of changing for New Zealanders too. Money will become increasingly more difficult to obtain. The impact of this of course is a head wind for property prices in the future and for the underlying economy too.

In New Zealand, the Reserve Bank recently released lending figures showing that the numbers were slightly down on the same month in 2017 ($1.04 billion) and $0.5 billion short of September 2016 figures. The report shows that investors borrowed less in September than any month from May through August. This comes as interest only lending slumped to 30% of activity down from a high of around 41% in 2015. These curbs on interest only lending appear to be influenced by Australian banking policy. This, in conjunction with ongoing loan to valuation restrictions (LVR) also continues to dampen investor activity in New Zealand.

Overall however new lending totalled $4.7 billion last month up from $4.56 billion in September last year. This marks the sixth consecutive increase on comparable figures from 2017. Further, first home buyer lending reached $821 million, up from $658 million in September 2017. Core Logic stated recently that their model suggests volumes of house buying and selling will remain stagnant at around 80,000 per annum into 2019. This is interesting given the Reserve Bank’s indication that interest rates may stay at around 1.75% until 2020 which is accommodative. Will there be a relaxation of the LVR policy? Will this be needed to provide some renewed impetus to property sales over the coming year?