China Drops Sanctions Probe into US Sorghum Imports

Market and Economic Update – Week Ending 25th May 2018

Peter Flannery CFP AFA

“If you have one economist on your team,

it’s likely that you have one more than you’ll need.”

Warren Buffett

- Both China and the US appear to be reducing the rhetoric around trade sanctions. China recently stated it is dropping an anti-dumping probe into Sorghum imports from the US. In April this year Beijing introduced high tariffs on imports as part of its tit for tat trade spat with the US.

- But, in an apparent backing off, China’s Commerce Ministry is now saying that this measure affects consumers and is not in the public interest. The bottom line here is that whilst trade sanctions are not off the table, the widely expected trade war between China and the US looks much less likely to emerge. I will keep you posted.

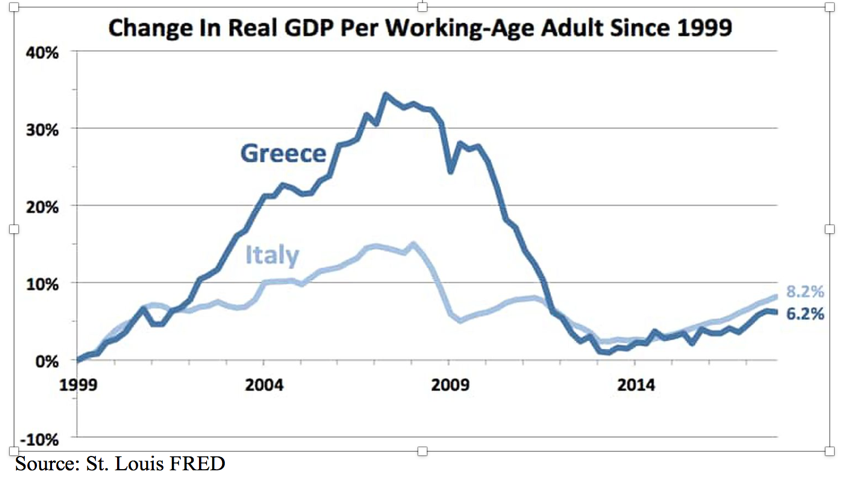

Is Italy turning into Greece?

Like Greece, Italy has made minimal progress.

- Italy’s economy has not performed well over many years however the real problem is that Italy is the eighth largest economy in the world by nominal GDP, but also has a sizeable amount of debt to go with it. Their ever changing government which cycles from centre left through centre right has not been able to get its economy moving again whilst working under the restrictions of the Eurozone policy.

- This brings us then to whether or not Italy might exit the Eurozone? Italy would likely prefer to run bigger deficits (translated that means Italians get to maintain their lifestyle and keep spending more than they make) which of course goes right against the rules of the Eurozone set by the European Union (that is to say Germany).

- Germany of course is concerned that they may need to bail out the Italians at some point. This has been referred to as an extremely unbalanced game of “chicken”. On the one hand, Italy is to some extent at Europe’s mercy because, it depends on the European Central Bank to keep its banks afloat (and its borrowing costs down). In theory then the European Central Bank could crash the Italian economy just by pulling the plug on its financial support (a bit like it did with Greece).

- On the other hand though, this type of action could put Europe at Italy’s mercy. This is because in that type of situation it would leave Italy with little to lose by leaving the Euro. This raises the spectre of the so-called contagion that potentially could involve other European member states. As I said, this is a different situation to Greece because Italy’s economy is much bigger than that of Greece.

- One thing that we can possibly say with some degree of certainty is that, the ever changing populist governments pandering to the wishes of “needy” Italians is unlikely to be a recipe for Italian or European economic stability and growth.

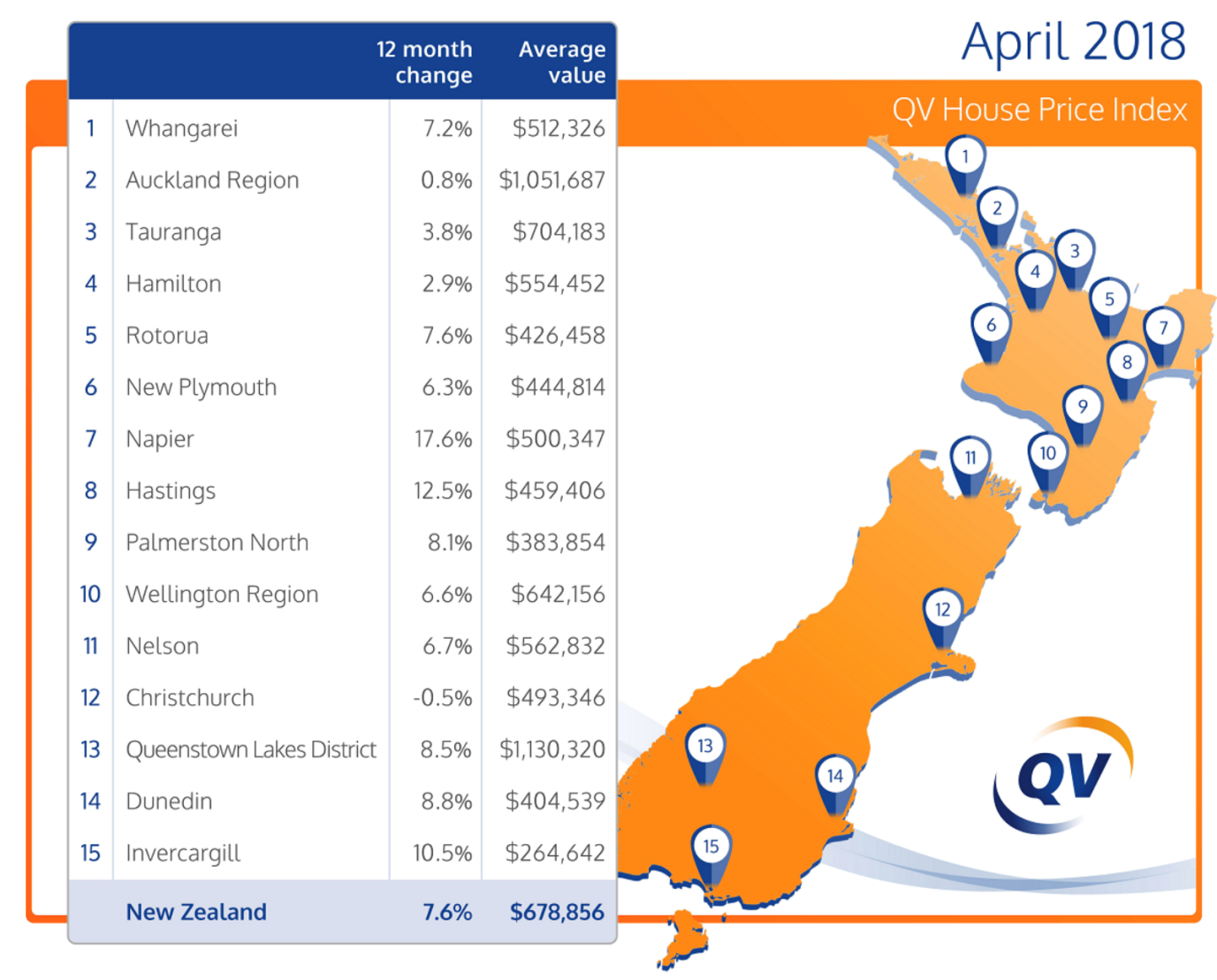

NZ House prices still rise but mixed

- The recent monthly QV house price index shows residential property values for April increased 7.6% over the last 12 months and 1.1% over the last three months.

Generally prices continue to increase apart from Christchurch.

- Meanwhile though, residential property prices over the Auckland region increased only slightly by 0.8% over the last 12 months although values dropped by 0.3% over the last quarter. There appears to be no property crash in sight and property price rises appear to be moderating – particularly in Christchurch city.

- Christchurch has been described as one of the few fully functional property markets in New Zealand where house prices remain flat with some areas showing slight increases and other areas showing slight decreases in price. Over the last 12 months Christchurch property prices declined by 0.5% and by 0.2% over the last three months. The average value of property in Christchurch city is now $493,346.