MARKET VOLATILITY CONTINUES = YIPPEE!

Market and Economic Update – Week Ending 23rd November 2018

Peter Flannery CFP AFA

“If you have one economist on your team,

it’s likely that you have one more than you’ll need.”

Warren Buffett

The Markets

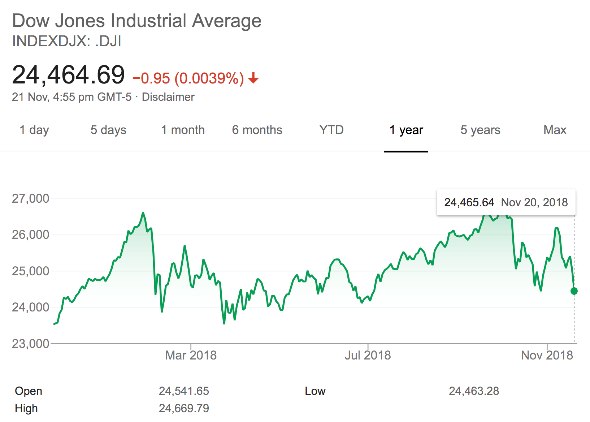

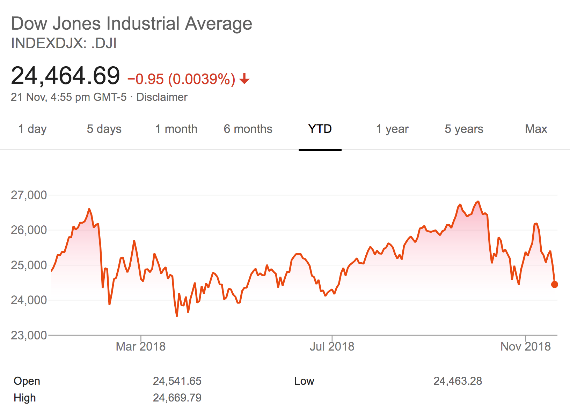

The chart on the left shows the movement of the US share market (as per the Dow Jones) over the last 12 months – still green. The chart on the right shows the movement year to date – red (that means the market is lower than at the beginning of this year).

Markets and the economy are two different things. Markets relate to general market sentiment and the impact on prices, whereas economic indicators relate more to a country’s performance highlighted by changes in such indicators as unemployment, interest rates, economic productivity and a range of other county related measures. A couple of weeks ago, I asked if anyone had any strong views either way about including market information in with the usual weekly economic update and so far, I have seen no strong views either way – perhaps nobody really cares about markets or the economy!

Interestingly, those who focus more on the quality of the businesses within their portfolio rather than the economy or market “news” are actually correct. Long term, whilst markets and economic fluctuations can impact on our investments, the strength and the quality of the underlying businesses within the portfolio inevitably determines how much money we make.

So, the markets remain uncertain and prices somewhat volatile. The market peak for the Dow Jones was 26,829.39 points as at Wednesday, 3 October 2018. That number has declined to 24,465.91 points as at the close of trading Wednesday, 21 November 2018. In real market banter terminology, this represents a decline on the Dow of approximately 9.5% (I will not bore you with how many billions of dollars this has wiped off markets because it is senseless nonsense). You know … since when is the quality of your investment portfolio determined by how unsettled or scared the market as a whole is feeling right now (!)?

Key phrases you will see across the internet and in the popular media go along the lines of, “The market is worried about … markets are unnerved by … XYZ problem looming … and so on.” During those market phases, you will notice that the media overplays any negative data it can locate. Sometimes this data is quite interesting and useful. Sometimes it is obscure data that no one ever cares about. The trick, of course, is to understand the difference.

ECONOMIC BRIEF

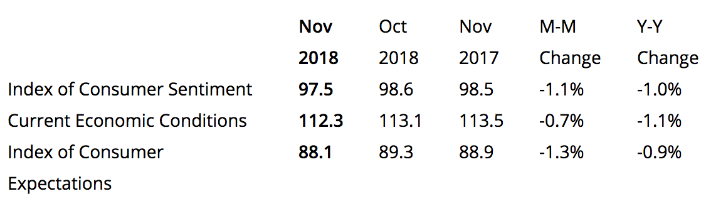

US market sentiment

US Market sentiment has declined of late but still remains solid.

Sentiment surveys are carried out around the world as a way to gauge the pulse of the market and a possible indicator of where things might be heading. Of course, they are subject to rapid change for all kinds of reasons. The above chart is November 2018 data, showing that sentiment across the US declined from October with a 1.1% change from one month to the next and interestingly, a 1% change over the last 12 months. The short of it is that market sentiment remains basically unchanged and favourable. Consumers and business owners in the US will be aware that the US Fed has been increasing interest rates and this, I imagine, will be increasingly factoring into their feelings about their expectations of the future.

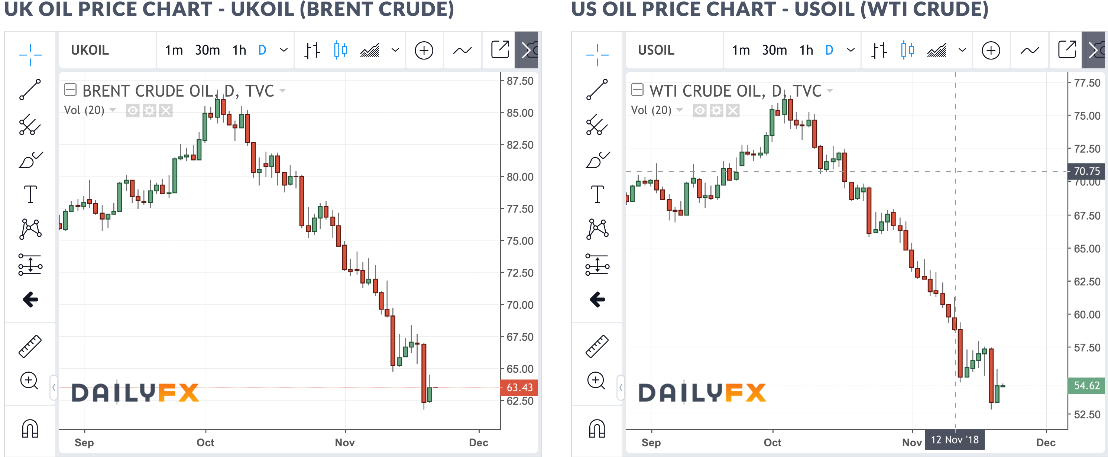

Oil prices have declined, along with general market sentiment, over the last month to six weeks.

US crude oil production was unchanged over the last week, at 11.7mln barrels per day. There have been some concerns floating around the markets of late, about a potential oil glut, although recent US Government data showed still strong demand for refined fuel. However, the market remains somewhat concerned over rising global crude supply. Oil, like any other commodity, will see its price rise and fall on the back of supply and demand.

The US Federal Reserve has been raising interest rates over the last 18 months or so and is expected to raise interest rates yet again next month and three times next year. However, any real change in economic growth (GDP) may see the US Fed Governor, Jerome Powell, slow down the pace of those hikes.

The probability of a US recession in the next two years, whilst still reasonably low, increased by one measure up to a median 35% from 30% in the latest monthly Reuters survey of economics, taken in 13 November through 19 November in the US. The chance of a recession over the next 12 months is rated at 15%. You will need to look elsewhere for doom and gloom, it would appear. Although a number of developed economies around the world are showing signs of slowing down somewhat, growth in the US continues to remain solid, with unemployment official at the lowest rate in around 50 years. There is ongoing support for the economy through debt and riding the tail end of the $1.5 trillion tax cut boost, which is still impacting positively on the US economy.

Then, there is any number of forecasts showing the slowdown for the US economy over the next one or two quarters, driven in part by the stimulus of tax cuts wearing thin and the trade standoff with China continuing. Also, the strong US dollar will not be helping exporters either.

Economic growth in the US, as measured by GDP, will likely expand at an annualised rate of 2.7% this quarter, down from 4.2% in the second quarter of this year and 3.5% in the third. By some estimates, economic growth in the US is forecast to then slow to 2% to 2.5% throughout 2019 and then down to around 1.8% by mid-2020.

Brexit remains in the news, with the deadline looming. There is around four months before Britain’s supposed departure from the European Union. Theresa May, the British Prime Minister, is in serious talks with European officials in an attempt to iron out the remaining issues of disagreement. In an interesting move, German Chancellor, Angela Merkel, said she was not willing to come to a recent meeting with Theresa May, which apparently meant that Angela Merkel was wanting a documented proposal finalised before any meeting could take place. That, of course, puts a bit more pressure on Theresa May. Another headwind for Theresa May revolves around the disputed Peninsula of Gibraltar. Spain’s Prime Minister is insisting that he would vote against any draft deal, unless he is given real assurances over Gibraltar. Theresa May, on the other hand, remains positive, suggesting that sufficient direction has been given for these issues to be resolved. It appears that the major stumbling block is those issues around Gibraltar, according to some commentators.

Italy, as you know, is in the midst of a disagreement with the European Union over its failure to comply with how it conducts the affairs of its country fiscally. In short, Italy is spending too much money and needs to introduce a range of measures to cut expenditure in order to meet Eurozone membership rules. By one measure, Italy has around US$2.6 trillion of debt and the interest the Italian Government is paying on that debt continues to be driven higher, as foreign investors become more and more reluctant to invest in Italy’s debt, because of the “bun fight” with Europe. Italy’s Deputy Prime Minister has come up with a plan to suggest that everyday Italians could purchase government bonds and they could be rewarded with tax breaks. This would help the government to finance some of its debt, so that it could continue with government spending plans that have actually already been rejected by the European Union because they do not meet the European rules on public debt. The reality is, should everyday Italians decide to invest in those bonds, they would be exposed to significant risk if this fight between Italy and the European Union escalates into a debt crisis

The European Commission initiated disciplinary proceedings against Italy last week, stating that its 2019 draft budget does not comply with the rules. For example, European Union rules require members to reduce debt once it exceeds 60% of GDP, however Italy is planning to raise its budget deficit to 2.4% of GDP, which means its debt will not be falling fast enough. It is interesting to watch this debate and it will be more interesting to see where it gets to in the near future – I will keep you posted.

Back here in New Zealand, residential property prices appear to be on the rise again, with nine out of 15 regions showing new record asking prices for residential property. These include Auckland ($946,400), Canterbury ($481,050), Otago ($567,950), Waikato ($570,900) and Wellington ($602,950). Interestingly, there was a 14% increase in the number of properties for sale in October this year, compared to October 2017. This sometimes indicates more activity and rising prices. Let’s remember though that interest rates in New Zealand have been flat for some time, remain low and according to Adrian Orr, the Governor of the New Zealand Reserve Bank, may not be changing until mid-2019 or even into 2020. This would appear to underpin property prices around New Zealand.

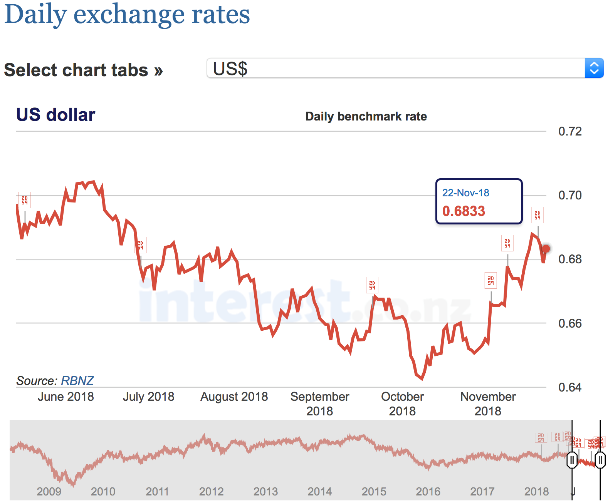

The New Zealand dollar is strengthening against the US dollar.

Although the general trend over the last week or two has been in an upward direction for the New Zealand dollar against the US, a few days ago, the New Zealand dollar declined, along with other risk sensitive assets, as the ongoing US/China trade skirmish continues, keeping investors nervous about the pace of global economic growth.

Also, dairy prices unexpectedly fell at the global dairy trade auction, with the index down 3.5% recently.

If you would like a more in-depth overview of the global economy, please click here to review the latest quarterly economic update.