Trade Tariff Rhetoric Continues

Market and Economic Update – Week Ending 13th April 2018

Peter Flannery CFP AFA

“If you have one economist on your team,

it’s likely that you have one more than you’ll need.”

Warren Buffett

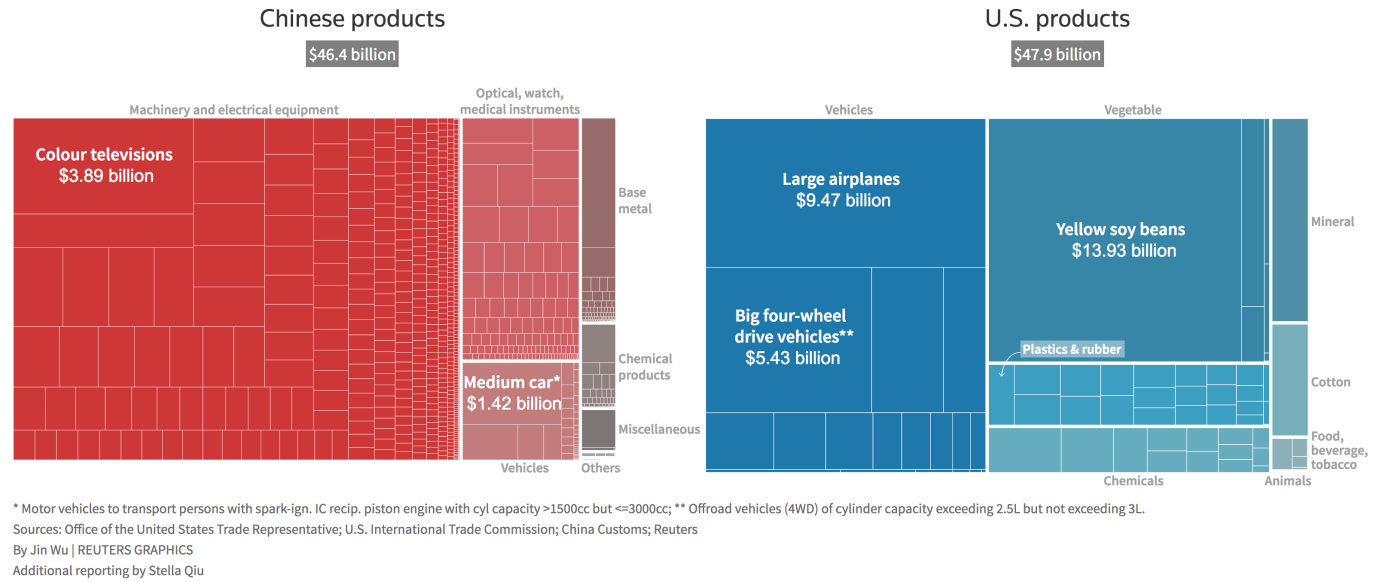

- Eight Chinese industry sectors are being targeted by US tariffs. As the chart above shows, those most affected are electrical equipment, vehicles, optical and medical instruments. On the other side of the coin China appears to be targeting over 100 US based products including aircraft, soya beans and motor vehicles. However, in a recent speech this week Chinese president Xi Jinping mentioned that he is keen to open the country’s economy further and lower import tariffs as he appears to be looking to defuse the growing trade dispute with America.

- Donald Trump responded (on Twitter of course) by saying that he was “thankful” of the Chinese leaders’ words on tariffs as well as his “enlightenment” on the issue of intellectual property. “We will make great progress together!” Trump tweeted.

- More conciliatory tones between the two leaders is likely a step in the right direction although it appears that China’s talk about opening up certain parts of their economy such as the motor vehicle sector are in areas where China already has a distinct advantage. Some analysts have cautioned that concessions made by China on motor vehicles, whilst welcome, would be a relatively easy win for China to offer the United States of America, as plans for opening up that sector have been underway well before Trump took office anyway. Further, China’s vice commerce minister Quin Keming said at a forum this week that China’s economic reforms were driven by domestic factors and not due to external pressures.

- Donald Trump still maintains that China continues to steal US intellectual property from US companies which does have some merit when all’s said and done. Chinese officials of course deny such charges however I understand that, behind the scenes they have, for quite some time, been looking to tidy up some long standing unsavoury practises including corruption so that they can become a member of “the club” so to speak. In other words a respected member of the international trade community long term. Indeed, they even see China becoming the favoured global currency over and above the US dollar. The might be a “long shot” so to speak.

- Basically, trade tariffs and trade wars are two different things and at this stage I doubt we have a trade war in full swing. It is still too early to say how this might play out however the recent conciliatory tones are supported by the long term logic of two large economies that rely on each other for trade to a significant extent, getting on with each other rather than arguing. Debate and negotiation will likely achieve much more for both economies than what has been going on over the last couple of months.

US interest rates

Interest rates are tracking in an upward direction for sure.

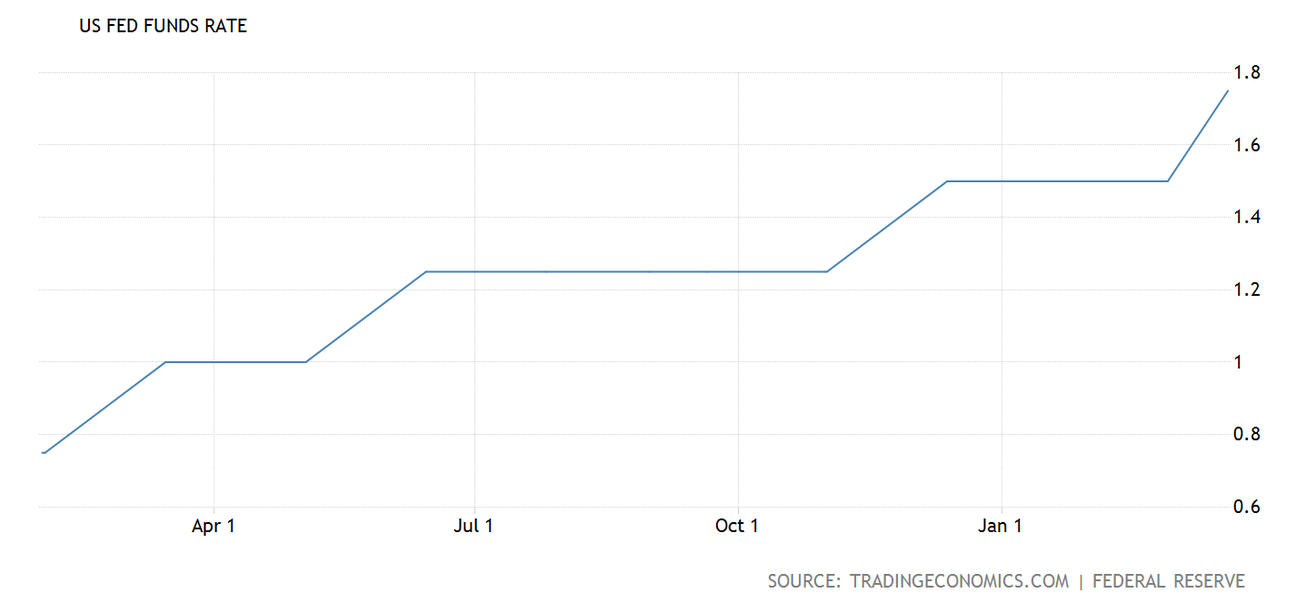

- The US Federal Reserve raised the target range for the Federal funds rate by a quarter of a percent from 1.5% to 1.75% during its March meeting. This was in line with market expectations and what the Fed sees as strengthening indicators that support economic growth in the US. Just for good measure, the Fed threw in an additional rate rise for 2019.

- I mention this because interest rates at some point will bite and impact on asset prices. Not yet though. I will keep you posted …

- As you may know, in New Zealand, interest rates remain on hold, in theory until around mid-2019. As I have mentioned of late, the market is focused on US data including wages growth (we await the next update), rising inflation and rising interest rates. As these numbers show increases, expect certain players across the market to unwind their positions, occasionally in a big hurry. That’s an example of economic data driving markets one way or another.

The Eurozone

- Deutsche Bank troubles continue. You may remember over the last couple of years Deutsche Bank created quite a fuss as it fell into serious difficulty and looked at one point as though it was going to topple over. Long story short, the bank was rescued but this year worse than expected losses of €2.2 billion have emerged for the fourth quarter of 2017. A €497 million loss has emerged for the full year. As one commentator quite rightly said, “It’s difficult to fix decades of mismanagement in a couple of years”.

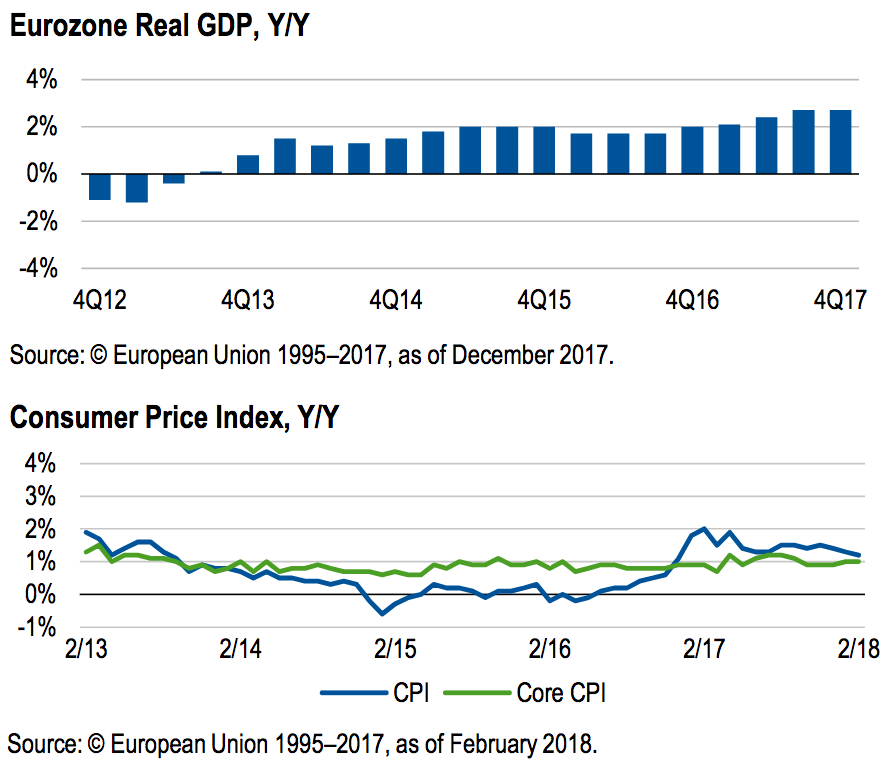

- As for the Eurozone economy, it continues to press forward with steady economic growth and stable inflation.

The Eurozone economy looks fragile but stable.

- It is possible that further central bank stimulus will be required to prop up the Eurozone economy in the future. This just highlights the fragile nature of the Eurozone economy and confirms that this economy still has a long way to go before fundamental economic growth supports the economy. However for now, we will take stability over the less preferable option of out of controll deflation!

Global debt

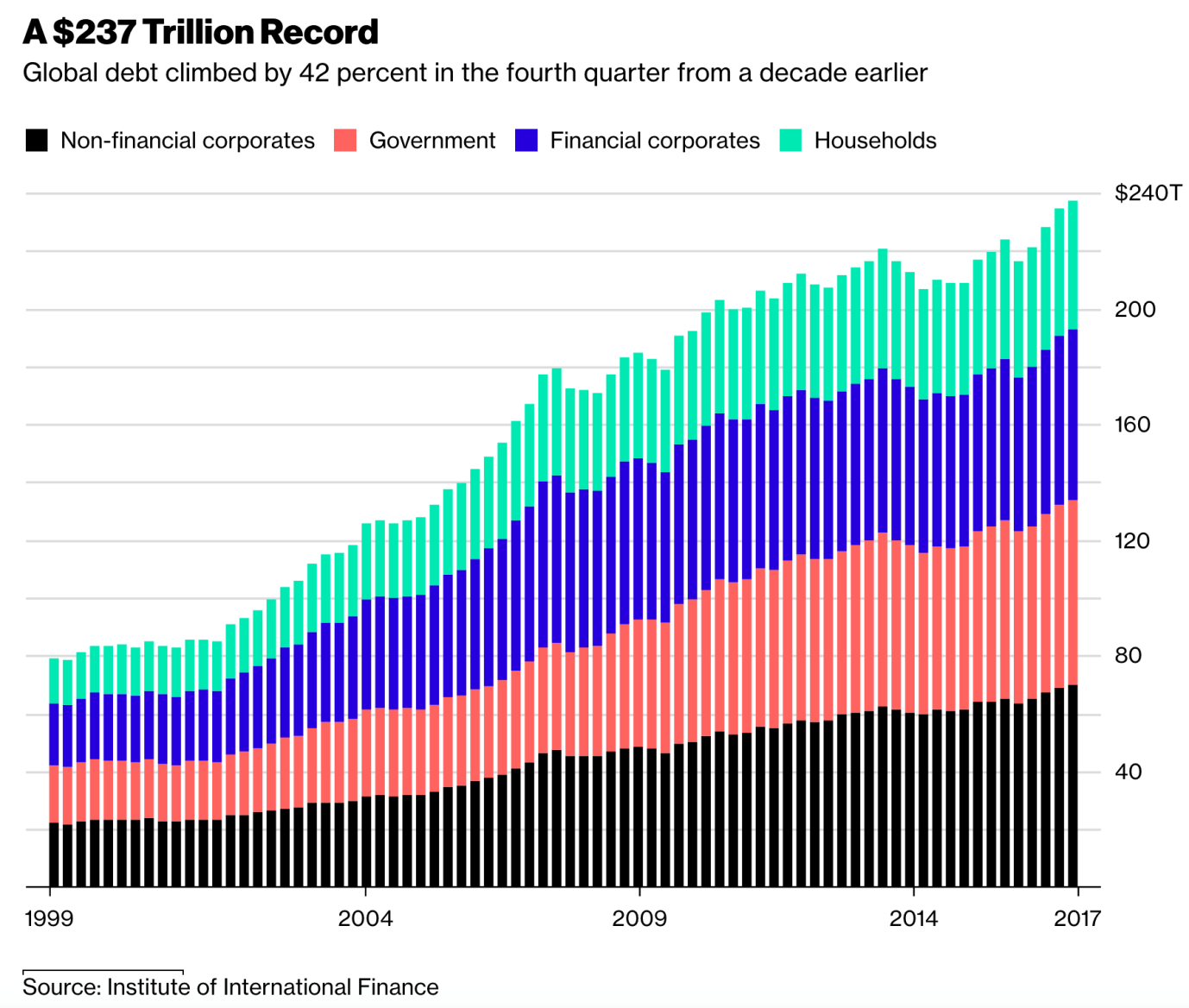

Global debt in nominal terms continues to grow.

- Debt as a percentage of GDP is a useful measure because it compares debt to economic growth (and to a lesser extent productivity). While this is a bit simplistic, it’s a bit like comparing how much you might pay for a rental property with how much rental income you might receive or how much you might pay for a direct share on the share market compared to its earnings. A bit simplistic I realise, but you get the idea. Long story short, rising debt is potentially a problem long term and not ideal. For now though it is manageable and despite what some internet jockeys like to proclaim (remember though there’s a healthy dose of self-interest behind those claims), the debt is manageable and appears unlikely to cause an economic Armageddon scenario any time soon.

- I am not suggesting that we just bury our heads in the sand and ignore it. I am suggesting that we focus on what we can do and keep an eye on the debt, but more importantly focus on our big picture goals. We can’t control the global economy however we can position ourselves within it quite effectively. Whilst global debt could be an issue long term, at the moment it’s not. For example, the ratio of global debt to GDP fell for the fifth consecutive quarter as the world’s global economic growth accelerated. That ratio is now around 317% of GDP or 4% below the high in the third quarter of 2016.

- Global debt is high and growing, but not worth worrying about just yet. I will keep you posted …