Share Markets Decline, Decline And…

Market and Economic Update – Week Ending 12th October 2018

Peter Flannery CFP AFA

“If you have one economist on your team,

it’s likely that you have one more than you’ll need.”

Warren Buffett

US Treasuries

US treasuries are on the rise.

The People’s Bank of China cut the reserve ratio for the country’s major bank by 1% because of slowing growth. This effectively frees up more money for the state-controlled banks to lend out, which in turn helps stimulate economic activity. Of interest is that this is their fourth such cut in 2018 and by some measures, a large and broad policy manoeuvre. We then had the sharp rise in US treasuries (as shown on the chart above). The amount of the increase was notable but what was more interesting was the speed of the increase. This suggests that some players in the market are becoming somewhat nervous and looking to retreat, as they adopt a more defensive approach.

What followed from there, over the last few days, has been a correction across markets around the world.

The above chart shows a notable, one day market decline of 3.11%.

The tech sector has seen some good declines, with the likes of Amazon, Netflix, Facebook and Apple, among others, seeing their trading prices drop. Of course, this stands to reason because those are popular investments, followed strongly by the market. Therefore, we would expect those popular, strongly-followed businesses to be seeing strong selling, as some of those investors “run for cover”, so to speak. Whether it be mum and dad investors, who cannot bear the thought of watching the cash up value of their investments decline, even a little bit, or fund managers, who worry that when they next report to their investors, any negative numbers could see their funds under management decline, or other investors who are not sure what to do (because they play the markets like most) and therefore are watching what other participants in the market are doing with the view to following them out of the markets. Value investors find this type of behaviour highly amusing, as you can imagine.

US producer prices increased 0.2% in September, reversing an unexpected decline in August and pretty much in line with expectation. This means that producer prices are up 2.8% year over year. This index is often followed as an indicator of inflation, which is why the market is currently watching it closely. So, those treasury yields, rising from 3.05% up to 3.22% at one point (their highest point since 2011), along with a resurgence of inflationary fears, as well as low unemployment has conspired together to spook the markets, hence this sharp decline across markets (over the last few days). Rising interest rates also, from an analyst’s perspective, makes share prices look a bit more expensive, relative to fixed income alternatives. Once yields rise to a certain level, some fickle share market investors begin to feel attracted to so called low risk defensive assets, like term deposits and prefer to avoid what they consider to be high risk investments, like shares.

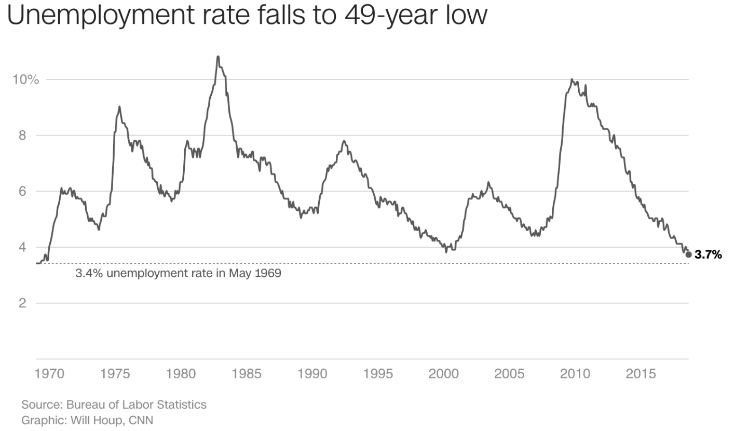

Unemployment in the US continues to decline.

Unemployment in the US, having dropped to a 49 year low, at 3.7%, as mentioned earlier, is a potential trigger for increasing inflation, ( driven in part by wages growth) which can spook markets because they know that what follows is interest rate rises. Interestingly, the labour force participation rate, which measures the percentage of the population that is either working or looking for work, has remained basically unchanged over the last few months. Professional and business services remain the economy’s strongest sector, with a cumulative 560,000 jobs added over the past year. Also, healthcare and transportation, along with warehousing, have continued their strong gains, adding 26,000 and 24,000 jobs respectively in September.

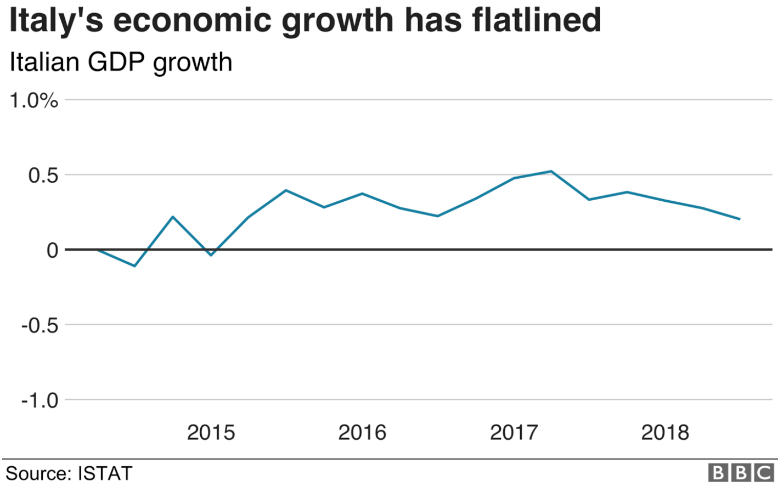

Economic growth in Italy remains sluggish.

Italy has a reasonably large amount of debt to contend with, which is partly why a recent budget set out by the country’s coalition government, that involved greater spending than was previously planned, unsettled markets. Italian share prices dropped and the value of the Euro also declined. The cost for Italy to borrow money (the debt issued by the Italian Government) has been rising of late, which demonstrates that investors are becoming anxious. Markets are becoming concerned that recent government plans may mean that Italy is heading for a standoff with the European Commission.

The government that took office in Italy in March this year is keen to deliver on campaign spending promises (sound familiar?). To do so, it will need to borrow more than was previously planned. Increased borrowing against Italy’s persistent weak economic growth is an incongruent match. Previous plans, sent by the last Italian Government, outlined expenditure at 1.6% of annual national income (GDP), declining to 0.9% and 0.2% over the next two years. This would see the budget almost balanced by the end of the decade.

The current coalition spending however suggests expenditure at 2.4% of annual national income (GDP). Although the European Union limit is 3% of GDP, another rule that impacts on Italy relates to the total accumulated debt, which should be no more than 60% of GDP. Italy has more than twice that amount.

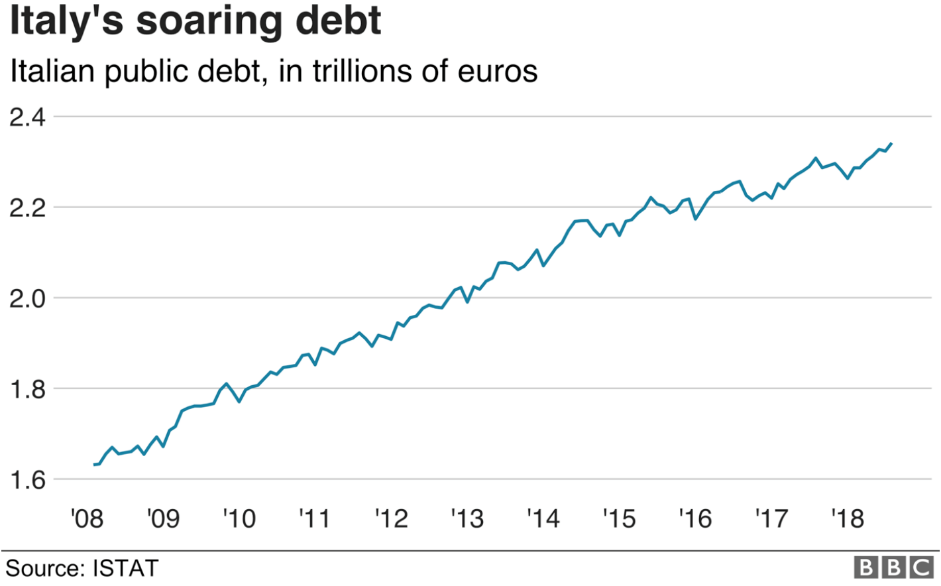

Italy’s debt continues to grow.

Italy’s debt burden, as a percentage of annual economic activity, is second only to Greece in the European Union, at 132%. Further, Italian banks continue to remain what some regard as the country’s ‘weakest link.’

Italy could default on its debt or it could leave the Euro. Whilst these are options, there is quite a way to go before they become real, but that is the general direction currently (!).

UK house prices unexpectedly dropped at the fastest pace in almost six months in September, according to Halifax. The number of homes for sale in 2018 fell to a decade low. According to one of Britain’s biggest mortgage lenders, the average price of a home in Britain dropped to £225,995 last month, which is down 1.4% from August. The price of a home still remains 2.5% higher than 12 months ago. House prices in London appear to be declining for the first time since 2009, however in other parts of Britain, prices are rising still. In New Zealand, we have Auckland property prices declining in some areas and the prices in some provincial areas around New Zealand still rising. I suspect that the combination of rising mortgage rates and economic uncertainty in Britain, eg Brexit, could weigh on demand over the next several months. This will likely keep house price rises reasonably subdued, particularly in London.

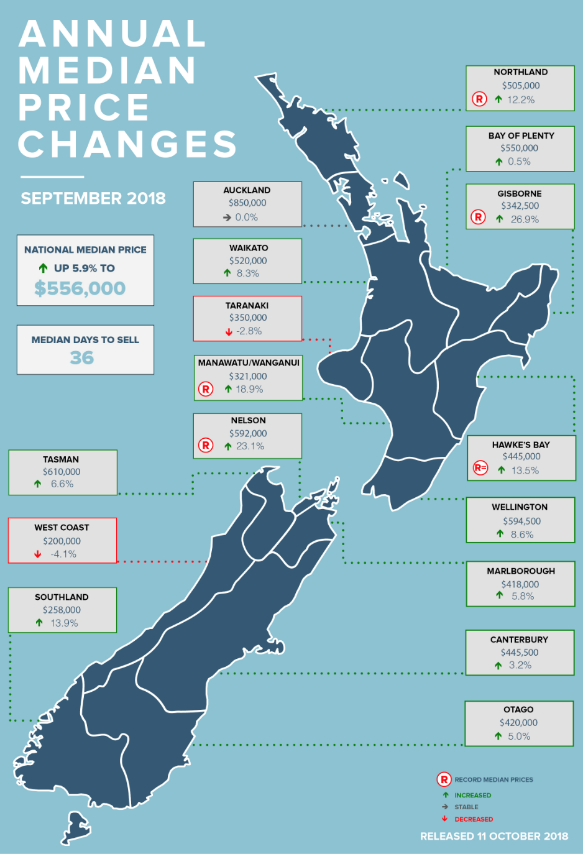

Quite a bit of green, a little bit of grey and some red.

The national media price of a residential property in New Zealand is $556,000, up 5.9%. The median number of days to sell sits at 36 across New Zealand.