Is The Global Economy About To Crack?

Market and Economic Update – Week Ended 12th April 2019

Peter Flannery CFP AFA

“If you have one economist on your team,

it’s likely that you have one more than you’ll need.”

Warren Buffett

The Markets

As those who rely on term deposits to live will know, interest rates have dropped significantly over the last five years.

Are reducing interest rates good or bad? It depends what side of the equation you sit, I suppose. If you are investing in growth assets, then low interest rates are possibly an advantage. If you are relying on term deposits or other forms of fixed interest income, then I suspect lowering interest rates are a bad thing. Actually, interest rates have been in decline for almost 30 years. Whether we agreed with it or not, it has helped push asset prices in an upward direction like we have not seen for some time. But where to next?

Over the last week, there has been a raft of cuts in rates everywhere we look across New Zealand. Interestingly, it is not only New Zealand that we are seeing this type of effect. Last year, surprisingly, the US Federal Reserve Governor, Jerome Powell, stated that interest rates “are near normal”. As you know, I think this is somewhat odd given that the long term interest rate in the US over 100 years averaged 5.1%, whereas the Fed rate is approximately 2.5%. It does not sound like near normal to me, however he may have a different definition. A sceptic might start thinking that pressure from Donald Trump has caused him to halt rate hikes. Further, only a few weeks ago, Jerome Powell also suggested that the US Federal Reserve may halt quantitative tightening. This just means that the money that they “printed” by expanding their balance sheet (approximately US$4.5 trillion) is being removed slowly but surely. Jerome Powell is now saying that he is going to stop doing that. What this means, I believe, is that there is some concern around economic growth, not only in New Zealand, but more likely when looking more widely around the world.

Although I would not lose much sleep over it, the outlook is for slowing global economic growth. We know that the Chinese economy is slowing down. Again, I am not too concerned about it because it is a tightly managed slowdown. Partly as a consequence, the European economy remains fragile. China and Europe are strong trading partners. Then, there is the US, which appears to be tracking okay with regards to economic growth, although the US Fed must have some concerns to be stopping quantitative tightening and halting interest rate hikes. Again, a cynic might argue that it is simply caving in to Donald Trump, who might like the idea of being re-elected at the upcoming elections in the US next year.

The bottom line with all of this is that I believe the global economy remains caught in the grip of “deflationary funk”. I do not mean that the global economy is shrinking. I am more thinking that growth is fragile, limited and is likely to slow down further over the next 12 months or so. This, of course, could create some concern across the markets, which in turn could see volatility suddenly erupt if the market senses that fear is starting to emerge. This, of course, may not occur. On the other hand, it could be a bit like that scenario where everyone heads for the exit through the same narrow door but of course, not everyone can fit through. When the market starts running scared, prices decline and if panic selling creeps in, then irrational decisions are made in the midst of market hysteria. I do not know about you but should this eventuate, I suggest we keep our powder dry so to speak and look for opportunities to buy. That said, there is always the opportunity that we might be disappointed and this type of volatility fails to show. Well, patience …

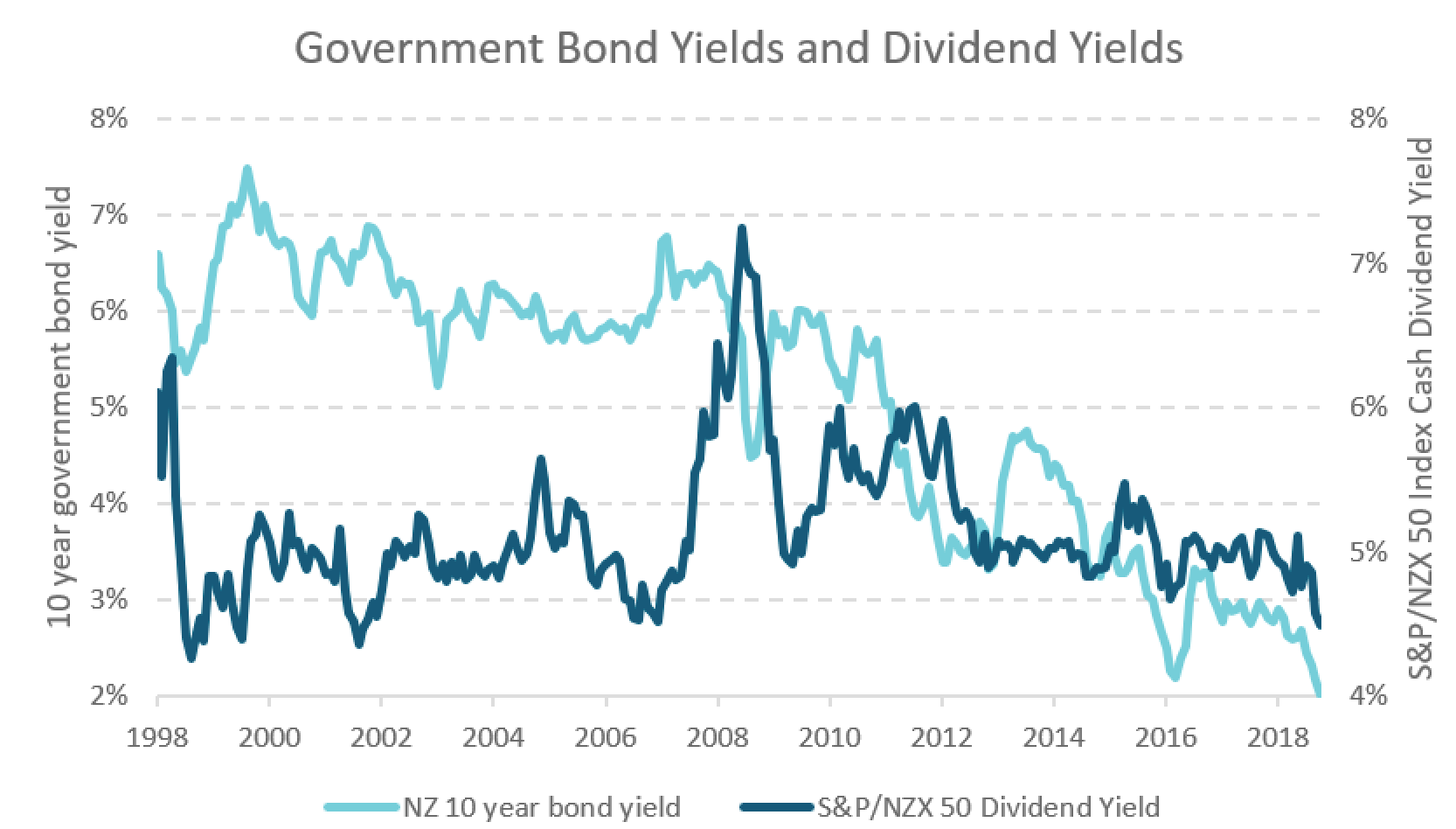

The above chart shows New Zealand 10 year bond yields compared to dividends from the share market.

Shares are just large businesses that happen to be listed on a market. The market provides the mechanism for trading. It makes it easy for us to buy bits of large businesses (shares). The stock exchanges provide rules around which the stakeholders must adhere. It is not perfect but it does provide transparency and safety for investors. At the same time, there is nothing like not having any clue about shares and dabbling as a way to burn good money.

Anyway, one of the funniest things I have seen is the number of accountants who look at a client’s dividend statement and then complain what a low return a particular portfolio is returning for the client (and wouldn’t they be better off in the bank or in property!?) They are overlooking, of course, the fact that the dividend statement does not show the capital growth – I kid you not. Similarly, the chart above shows dividends but does not show the growth.

Of course, for us as value investors, we know that in the short term, price movement is a function of the voting machine or market sentiment and is of little consequence other than if it drops far enough, we will buy. Longer term, good businesses grow. Some of them choose to pay out dividends, which ultimately is not such a good idea because they cannot grow as fast as other businesses who decide to keep some or all of it back as retained earnings. That way, they can grow faster long term.

Small caps are at the heart of retained earnings and growth – that is the sweet spot for investors looking to maximise returns long term. To be clear, chasing dividends looks intelligent when markets decline sharply. Those dividends just keep rolling out. Longer term though, the compounding growth of retained earnings inside good businesses that use capital effectively has been proven to be the most effective way to generate wealth. As Warren Buffett would put it, that is a real productive asset.

ECONOMIC UPDATE

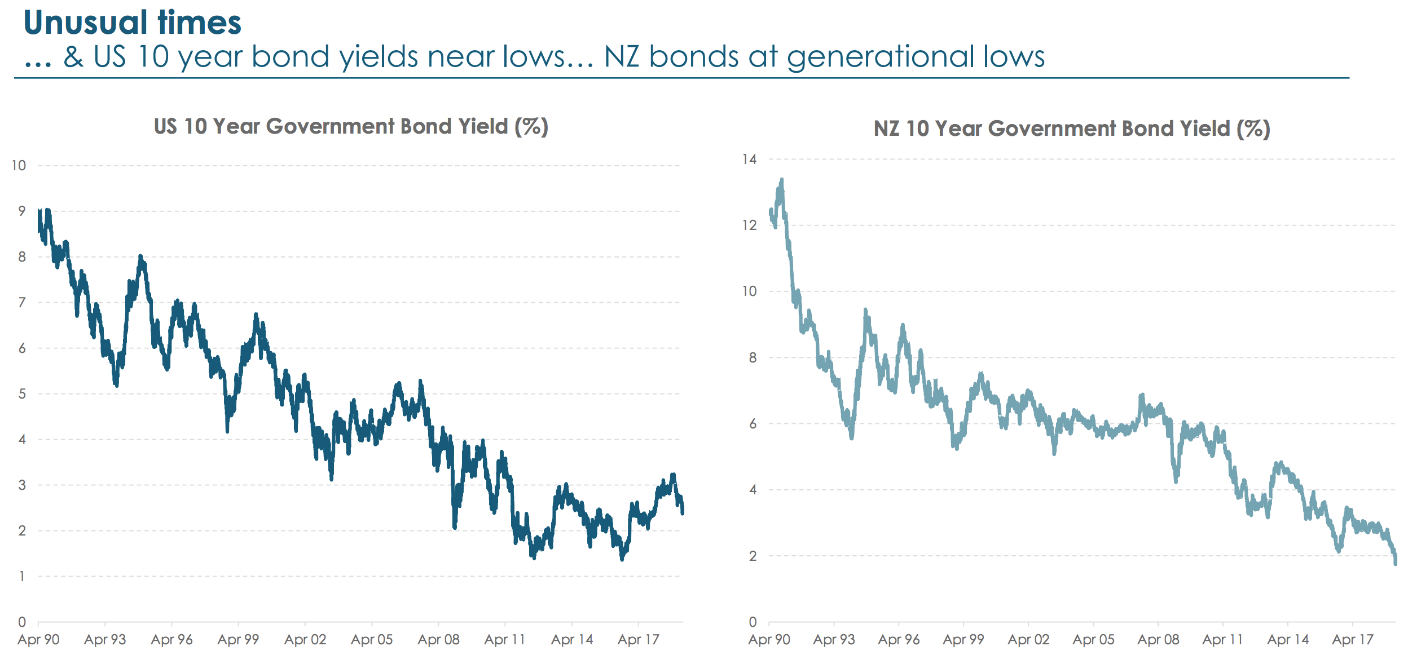

The above chart shows US 10 year government bond yields (left side chart) and New Zealand 10 year government bond yields (right side chart).

From an economic perspective, reducing interest rates can be the symptom of a bigger movement below the surface. Simply, a variety of factors are coming together to create the aforementioned deflationary funk. Notice the left side chart above that shows interest rates increasing over the last couple of years in the US but now on the decline again.

The question sometimes asked is, “What happens when interest rates get down to zero? What will the central banks do then !?” The short answer is, as we already know (eg Japan), they just continue to expand the balance sheet (the central bank prints money). That is not the only macro prudential tool at their disposal though. In short, there are a variety of ways that central banks can stimulate an economy. Increasing their balance sheet is one way. Another way is to loosen bank lending restrictions, allowing banks to lend money more freely. As I said, they have a number of tools and China, off the top of my head, would be the most prolific user of macro prudential tools.

I know some worry about a “day of reckoning”. it is not as simple as building debt around the world and one day it all blows up and it is the end of everything. No one can predict the future. When we step back, take a breath and look intelligently at what is going on, whilst the cynics will argue it is all one big experiment and who would know where it is all going to wind up, in my opinion, the global economy has a developing and increasingly sustainable eco-system which continues to progress.

Of course, progress is not a straight line in an upward direction. There are bumps along the way. At times, these can be significant and appear insurmountable … and yet they are always resolved. Hysteria does not make them any worse or any better, so why bother with it? I am not suggesting bravado or head in the sand or she’ll be right.

The fact is that the goods and services that most people around the world enjoy is not something that the world will give up without a fight (e.g. are you ready to say goodbye to the internet – seriously, can you imagine what the implications would be…). The businesses that provide all these goods and services need to stick around so we can maintain our current lifestyle. I imagine that everyday citizens of the world could care less about Alphabet (Google) or Apple, for example, and yet if a government decree decided that the internet was to be no more or that iPhones / smartphones were to be banned and could not be replaced with anything else, there would likely be an uprising.

Let’s face it, we do not like giving up things that we like.

So, deflationary funk, I believe, is alive and well. This does not mean that economic Armageddon is just around the corner.

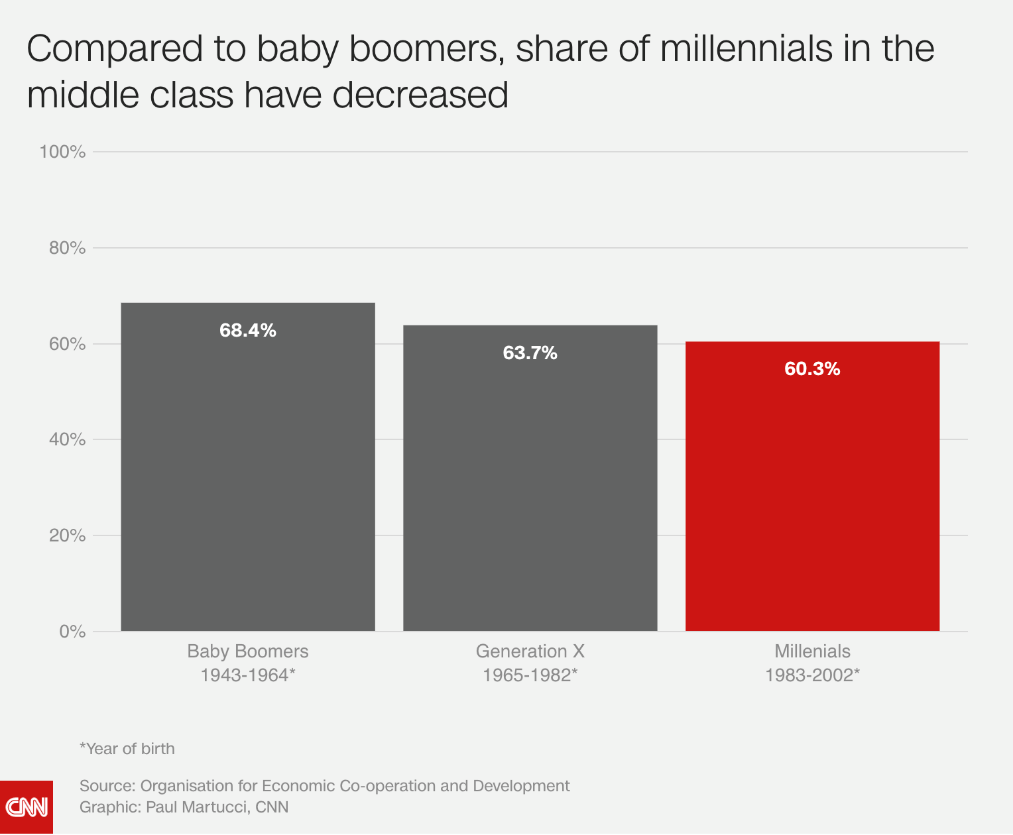

Something we have known for many years, which the chart above clearly demonstrates …

There is a growing divide between the rich and poor. The middle class is gradually disappearing. A few are making it to the top, with the lower half of the middle class sliding off into a life of struggle and anxiety. What is ironic is the fact that the world has never been so well off. Citizens of the world have never had such opportunity and a great lifestyle (I know, there will be naysayers reminding me that there are lots of poor people and even in New Zealand, people are homeless and living in cars). Exactly – the reality is that the middle class continues to shrink. Why do you think that is?

In New Zealand, of course, we have a smaller gap between the rich and the poor but a similar pattern here, whereby the lower half of the middle class are finding things increasingly difficult as their wages and salaries have struggled to keep up with the cost of goods and services (eg housing).

We are not going to know for some time whether or not Brexit is worth it. Things are currently hanging in the balance, as it were, however if you can call it progress, there has just been some. European leaders and the British Prime Minister, Theresa May, have agreed to an extension to Brexit that will allow Britain to delay its departure from the European Union until 31 October 2019. They are looking to have a review in June as the result of the recent plea from Theresa May. This is all about helping the UK to avoid crashing out of the European Union without a deal in place, however the French President, Emmanuel Macron, is remaining tough, suggesting that, “Nothing is decided.” He wants more “Clarity” from Theresa May about exactly what Britain really wants. Meanwhile, Theresa May has suggested that she thinks a 30 June 2019 deadline should be enough time for Britain’s Parliament to ratify a Brexit arrangement and pass legislation needed for a smooth Brexit. I know … British MPs have rejected her deal three times already.

Meanwhile, America prepares to impose US$11 billion in tariffs on the European Union. The World Trade Organisation has recently found that the European Union subsidies to Airbus has adversely impacted the United States of America. Donald Trump, of course, has been saying that the European Union has been taking advantage of the US on trade for many years and it must stop. The World Trade Organisation ruled the European subsidies to Airbus were illegal in May 2018. This then prompted the European Union to announce that it was also readying a list of tariffs to counter American subsidies to Boeing.

By the way, this is not new. Litigation around trade tensions between Europe and the US have been going on for around 14 years. America’s goal is to reach some sort of agreement with the European Union to end all subsidies that are inconsistent with the World Trade Organisation mandate. The short of it is, there has been a fair amount of going back and forward between Europe and America and nothing is in place yet; however, this situation continues to head in the direction of “tit for tat” tariffs. Interestingly, this is right at the moment when Boeing is having its own problems in the midst of the two 737 max jet planes involved in fatal crashes over the last several months.

The US and China have recently agreed to establish trade deal enforcement offices. This does not mean that they have reached an agreement over trade tariffs but that they have made some progress in what have been called productive dialogue between China and the US recently. Basically, they have agreed on an enforcement mechanism and will establish enforcement offices that will deal with ongoing matters around trade. They are still working it all through, as I said, and whilst this is some progress, they have yet to discuss lifting or stopping proposed trade tariffs.

The IMF (the International Monetary Fund) recently suggested that the global economy is at a, “Delicate moment” and they have downgraded their growth forecast for 2019 again. They now say global growth will be +3.3% rather than their earlier projection of +3.5%. They also have reduced their forecast for the US economy down to +2.3%, the European Union down to +1.3%, Latin America +1.4% and Canada +1.5%. They still see China growing at +6.3% this year and India growing at +7.3%. These, of course, are only projections but interesting to watch.

New Zealand

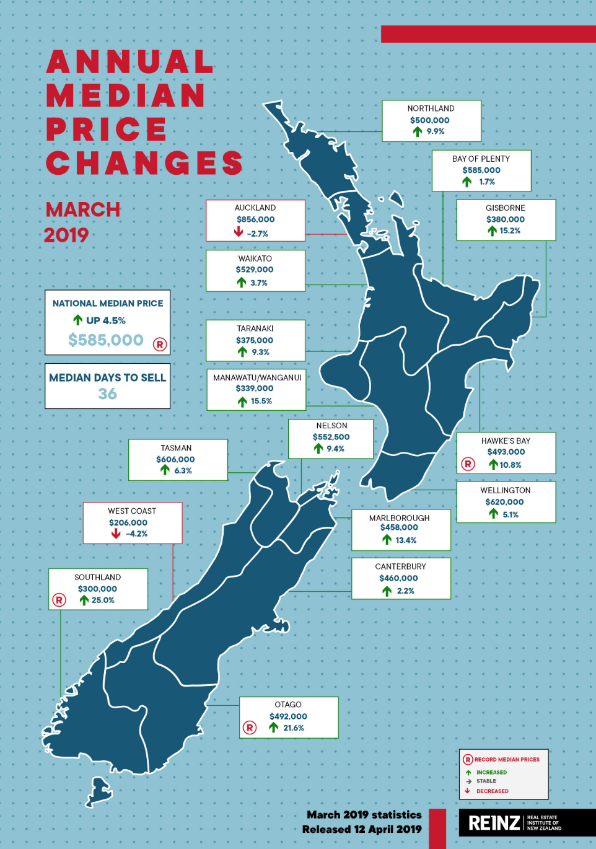

Property price rises and falls remain a mixed bag.

Uncertainty around legislation (eg capital gains tax), increasing compliance costs for landlords, to some extent, and increasing difficulty accessing finance continue to impact on sales volumes and home prices. The latest stats from the Real Estate Institute of New Zealand (REINZ) show the number of houses sold fell from 7,964 last year to 6,938 this year, which is a 12.9% decline. The West Coast saw an increase in houses sold from 47 up to 48 (up 2.1%), however Gisborne is down from 75 houses sold to 50, which is a 33% decline. Marlborough is also down from 121 houses sold to 82, which is a 32.2% decline in house sales. It is very much a mixed bag with Southland, Otago and Hawkes Bay showing increases in the median prices for the year ended March, with Southland up 25%, Otago up 21.1% and Hawkes Bay showing an increase in the median price by 10.8%.

Only Auckland and the West Coast show a decline in the median price, with Auckland being down 2.7% and the West Coast down by 4.2%. Interestingly, the number of days to sell a property increased by two days, from 34 days to 36 days, compared to March last year but actually fell by 11 days from February 2019, where the median number of days to sell was 47.

Another potential headwind facing residential property is Adrian Orr of the Reserve Bank of New Zealand’s recent proposal to increase banking capital in order to shore up the balance sheets of New Zealand banks. The idea is to make New Zealand banks safer in the event of a global credit crunch, however in short, this could see restrictions on lending, which as we have seen in Australia, could eventually mean less demand and pressure on house prices.

As you know, house prices in Australia are mostly declining as you read this now. Further, the extent to which Adrian Orr is suggesting they increase their level of capital looks significant. Time will tell. I will keep you posted.