Does a good dividend mean a good investment?

Investment Perspective – May 2017

Peter Flannery CFP AFA

“Neither the investing method nor the fundamentals of the business are right or wrong because the mood of the market is favourable or unfavourable toward the “stock”. That is because when you really think about it, “stocks” (shares) are all about the financials and the trading price, the share price… the cash up value. What matters more is the economics of the business”

Peter Flannery

It almost sounds lame to say that we should invest only in quality investments. However what is obvious to some is not to others.

I have heard many a sharemarket investor confidently declare that if a business is paying out a good yield compared to the bank and has done so for a few years, then it must be a good business. The theory is that the business is earning enough money and is profitable enough that it can afford to pay dividends.

Sometimes this is true. Sometimes it is true that the business is consistently profitable and therefore able to pay out a dividend. However, sometimes it is not quite true. This is when for investors things can get a bit tricky.

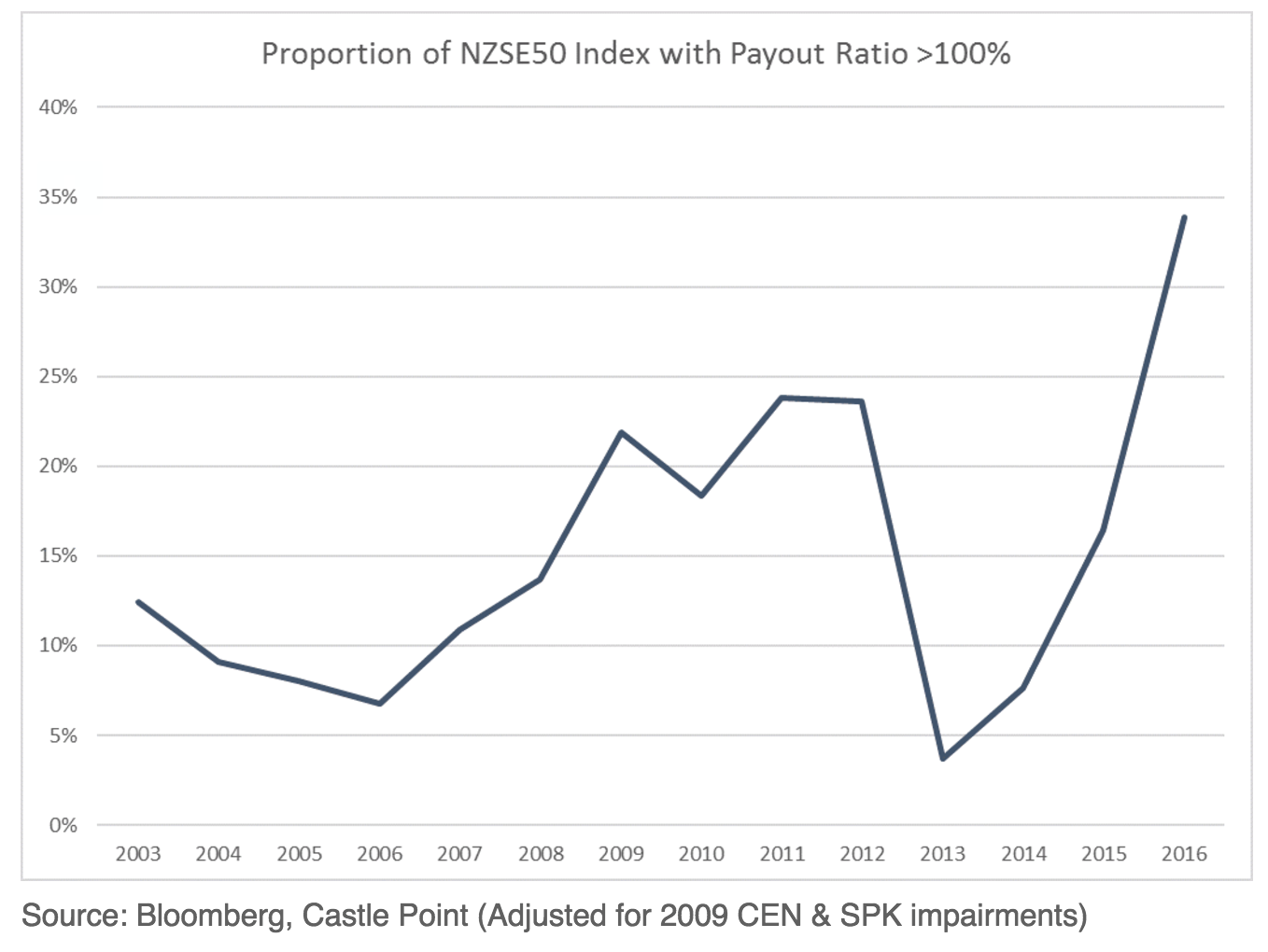

An increasing number of companies of late are paying out dividends at an unsustainable level.

What do you think about a business that pays out more than it makes each year? Once you cut through all the “shenanigans” around why they do it, you wind up pretty much in the same place every time.

Unless turnover and profit are steadily increasing, businesses and investors set themselves up for a day of reckoning. Either due to an external event or something troubling inside the company, the announcement is made that they can no longer sustain the dividend at that level with a variety of reasons given. They cut the dividend forthwith which usually immediately results in those investors who were only there in the first place for the dividend, bailing out and running off. The result of course is a sharp decline in the trading price. Then, because some investors are bound by “play the market” type mandates or are just plain scared of declining prices, they bail out too. The result is the share price declining even further. Of course, for those who bought in late, they now have a lower dividend and also less money than when they started in that particular investment.

Why are you investing anyway?

At WISEplanning we look at your investment “purpose”. We cover it off once every year. Why are you investing and what are you trying to achieve? Investment purpose of course revolves around your goals as an investor. Simplistically, you might be looking to grow your capital or to receive an income off it, or a combination of the two.

TIP: NEVER invest for income only. Always invest either for growth or growth and income.

Retired New Zealanders engage in a relentless chase for the best yield they can get from the bank or other fixed interest type investments that are based on first mortgages and/or property in an attempt to outwit the markets by stealing a better return than the banks can offer and of course just trying to make the best use of the limited funds they have available. This can be a dangerous practice which I have advised many retirees to “cease and desist” forthwith.

The point is that they just do not understand that investing for income only is a mistake, particularly in the long run. So why do they do it? You know the answer …

(a) They do not know who to trust;

(b) They worry about losing their money.

Fortunately, investing for growth as it turns out, is not rocket science. Unfortunately though there is a massive industry that would have you believe that rocket science is exactly what it is!

How to get the best out of growth and income investments

Income type investments, or “yield plays” as we call them at WISEplanning, can be useful as part of an investment portfolio mix. I use then as a proxy for cash for those who are looking for growth when suitable growth options are not available, usually due to stretched valuations. We can sit in the likes of ANZ, Westpac, Methven and a number of others, knowing that they may not grow much in the future but while we are waiting for suitable options to emerge, they provide a useful yield by way of income. To me, it is okay to sit in a yield play generating 5% or 7% or 10% whilst we await good pricing to emerge elsewhere.

I know what you are thinking … but what happens if there is a sharemarket crash? How good does it look then when the price of that yield play has dropped like everything else!? Well, that is always a possibility however where we have a mix of different asset types (at least the way I design portfolios), I am always taking that situation into account and including other options. One of those options you may have heard of before … it is called cash. Whilst many of my clients do not care too much for much, it can be quite useful when markets drop significantly in a synchronised manner.

Otherwise, if there is a general sell down across the markets cash is useful but failing that all things equal, as I said about looking for growth options, these can emerge when one company or another stumbles temporarily, the markets of course always react by selling out, providing us with the opportunity to buy in – so long as you and I are patient about the recovery time. The key here is that if our horizon is 20 or 30 years (even if I am aged 60 or 65 the horizon is likely 20 to 30 years still), then there is plenty of time to buy in at a low level and average down if we need to and wait for the markets to rediscover this investment and for the price to rebound. Even if it takes four or five years what does it matter?

Investing for growth

First let’s get out of the way what does not work. Investing for income only long term can be a real mistake. Whilst a business such as Hallenstein Glasson here in New Zealand has offered good dividends over a couple of decades and has been a worthwhile investment, nonetheless that dividend is assessable for income tax (although there are imputation credits attached I admit). Whilst the growth on that investment from day one probably has been quite good, for those who invested over the last 10 years though, the growth has been minimal, as expected. We really want businesses that will grow as opposed to shares whose prices rise due to market driven sentiment or other influences.

That grow but pay out most or all of their profit as a dividend will either need to raise capital by way of debt which they will need to service or go to the shareholders with a rights’ issue which effectively means investors putting their hands in their pockets and giving that to the company in order for them to grow and pay out more dividends down the track. I am not against rights’ issues however as investors we need to be careful about which ones we choose.

To be clear, there is a substantial difference in the amount of money that you and I will make as investors between a business that pays out most or all of its profits as dividends and one that keeps it all in to reinvest it for growth.

The problem with the New Zealand market

I do not know whether you noticed it or not, but it is difficult on the New Zealand sharemarket and even the Australian sharemarket to find these types of businesses. They tend to be small companies (“small caps” in our lingo) or young start-ups that need every cent to survive in the hope that they can grow and prosper. Britain and the US offer better prospects and over time I suspect will do better as investors with exposure to those markets in the long run. The New Zealand market offers reasonably good yield plays. Long term though if we are looking for growth we will probably need to invest outside New Zealand. I am not suggesting there are no options in New Zealand. Just that it is very difficult to find them. That is because there are not many. How many businesses in New Zealand survive 30 or 40 years or more and are great investments in which to invest?

KNOW THIS …

Warren Buffett did not get to be somewhere near the richest person in the world or thereabouts consistently over the last decade or so, gave us the most obvious example (if you need one that is). Berkshire Hathaway whilst never the number one performing stock on the market ever as far as I am aware, now trades at a share price of around USD$250,000 for each A share. That is because he is a master at picking good businesses and good people who run those businesses. It is also because Berkshire Hathaway looks for businesses that have a low dividend payout ratio. Further, Berkshire Hathaway has never paid a dividend – ever. The compounding effect of investing in good businesses that use capital well, who have a low dividend payout ratio and in turn reinvest those profits for growth can be significant over time. Much more than those businesses that pay out most of their profits or who are unable to use capital at a useful level for the compounding benefit of the business and its shareholders.

But what if I want some income though?

You might be familiar with “The Incomiser” system. Simply, it uses a combination of investments that generate high yields and allows us to scrape off profits from time to time if need be. This is a useful system because it provides investors with maximum control and flexibility. The income rolls in every month, regardless of economic conditions or market prices and the portfolio will continue to grow long term for those who want that.

What is clear is that those who invest for either growth or income and growth are substantially better off financially than those who engage in the unsafe practice of chasing high yielding fixed interest type investments based on property investments or first mortgages. Businesses that are well managed, have a sustainable competitive advantage and who redeploy profits to grow their business can compound substantial wealth for investors over time. This allows for the scraping off of profits that leaves the original capital in place (under The Incomiser system).

High yielding shares in New Zealand can be useful as part of a mix in order to generate some cashflow within the portfolio or to act as a proxy for cash whilst we await other opportunity to emerge. However, those companies who pay out a substantial proportion of their profits to curry favour with the market are unlikely to offer real sustainable growth long term. The opportunity cost by the way can be massive. The growth in Berkshire Hathaway might be an extreme example but it is not the only game in town when it comes to compounding growth. Few are as successful however investing for growth and compounding it over time seems to work, as opposed to investing in businesses that pay out most or all or even more than they make each year in profit is some kind of rocket science that I still do not understand!

“Real knowledge is to know the extent of one’s ignorance.“

Confucius