Improving Investment Returns

Investment Perspective – March 2019

Peter Flannery CFP AFA

“Neither the investing method nor the fundamentals of the business are right or wrong because the mood of the market is favourable or unfavourable toward the “stock”. That is because when you really think about it, “stocks” (shares) are all about the financials and the trading price, the share price… the cash up value. What matters more is the economics of the business”

Peter Flannery

How to invest is at least as important as where to invest.

Many people are keen to consider ways to improve investment returns. We refer to this as Return On Investment (ROI).

The Plan

The plan shown on the chart above does not refer to the investment plan but rather your holistic and all encompassing plan for your future life right up until ‘beam up date.’ It will include obvious financial planning, such as the household budget, how you own your assets (estate planning), risk management and of course, building up sufficient investment assets, so that you have passive income for as long as you need it – and enough of it.

Retirement planning is also another component of our life plan, with the idea being that one day most of us strive to “retire”. Retirement is a relatively recent concept that developed over the last couple of hundred years ago out of “the smoke stack economy”, with people working in factories six and seven days a week to the point where they physically wore themselves out.

They needed to ‘retire.’ These days, at least at WISEplanning anyway, we differentiate “retirement” from financial independence. Retirement seems to be stopping work when we are old, with anxiety, without enough money and hoping it all works out. The newspapers and the popular media appear to suggest that around $700,000 in your Kiwisaver scheme is all you will need (good luck with that!!).

Each to their own so to speak, however, it is more like $3 million once we take into account how long we might live and the special healthcare considerations that may emerge as the aging process continues to advance. Some of the help we may need is not available in New Zealand and we may need to put our hands in our own pockets and travel elsewhere for a solution. You may never need to do that, however the chances are increasingly likely that some of us will. The problem is that we just don’t know who.

Where to invest

Where to invest is the most common approach for those who wonder what to do with their money. The most popular option in New Zealand is the bank. Then, it is residential property and it would seem Kiwisaver schemes and company super schemes are next in line. Investing directly in productive assets, such as direct shares, it seems, is something not many people ever do. The educated academics argue that they are investing in productive assets by investing in Kiwisaver and other managed funds. Valid – but is that the the best way?”

I don’t know about you but when talking to many people, they do not rate methodology (how to invest) highly.

They still think in terms of property, the share market or the bank – where to invest.

How to invest

How to invest, in my experience, once we have our life plan sorted out, is at least as important as where to invest. There is a real difference from one method to another.

For example modern portfolio theory, encompasses diversification and dampening down volatility. Momentum investing through share brokers, is about following or even chasing rising prices across different sectors, also clinging to the idea that diversification is a great idea. Then there is good old Value Investing, which remains an obscure approach that few practise and even fewer understand, it would seem. The idea with that one, of course, is simply to buy quality businesses at favourable prices, holding them long term. The idea is to only invest in a few good ones rather than a lot of average ones who compete with each other (!).

This does not mean that we as Value Investors would never sell. It means that we may trade one investment for another as our investing strategy progresses and becomes more advanced.

In my experience too, there is no reason for an investing strategy to become more defensive as we get older – I know … that is not the widely held belief.

For sure, when we stop work, our money needs to keep working and by all accounts, probably work harder than it has ever done in the past. That just means investing slightly differently – not taking on lots of risk.

The importance of methodology

It is difficult to maximise investment returns if we are adhering to an investing methodology that slows down and stifles that very thing we are trying to achieve.

Portfolio governance versus portfolio management

Your role as investors (clients of WISEplanning) is to take charge of the governance process.

Simply, this deals with setting benchmarks for performance, deciding on the appropriate investing methodology, selecting advisers and managers to carry out the day to day operational activity of actually investing and holding the managers/advisers to account on a regular basis.

Success is almost inevitable when those undertaking the governance role work harmoniously alongside and are on the same page as the advisers/managers. Indeed, the governance role is to help and support managers, so that they do their best work.

The advisers/managers, on the other hand, are responsible for the day to day operations of investing, making sure that everything is done that should be, in a timely manner. The short of it is that, the advisers/managers will have the back of the board of governance (this could be just yourself and your partner).

The advisers/managers will highlight adjustments that need to be made and will always make sure that those adjustments are in line with the agreed investing strategy. They will also help “the board” to design strategy that supports long term investing objectives.

It is not the role of governance to manage the portfolio. It is not the role of the managers/advisors to deviate from agreed strategy and methodology. Indeed, they must stick to the plan (or be removed).

Improving investment returns (ROI)

Adjusting your investing strategy is an effective way to increase the ROI. The more advanced the strategy, the greater the level of pricing volatility along the way and the greater the ROI long term too.

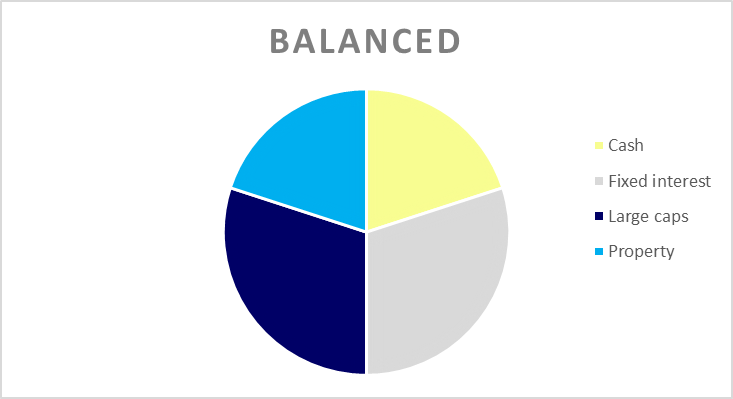

The Balanced investment strategy

Starting off with a balanced investment portfolio, we have 50% of the portfolio in cash and fixed interest type investments, generating income but no growth. The other 50% of the portfolio will be in a variety of growth assets and probably widely diversified, in order to dampen down pricing volatility (the cash up value in the portfolio moving up and down too much).

Although others may have a different view, I (and many of my clients) regard this as playing safe rather than investing. It is about protecting capital at the expense of making money (we can do both).

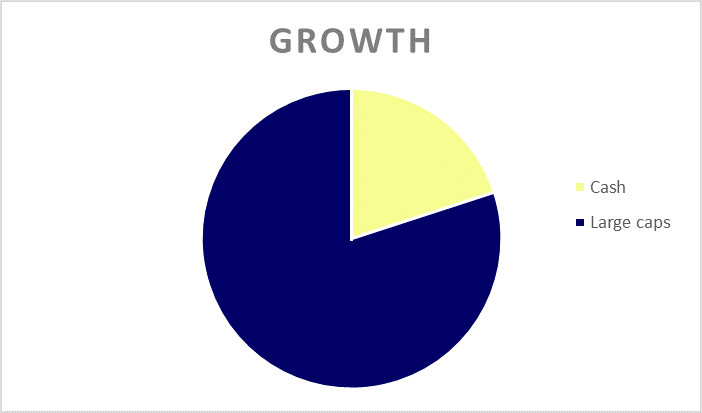

The Growth investing strategy

Then, we come to the Growth Strategy, which at WISEplanning involves eliminating fixed interest, maintaining cash for flexibility and investing in larger businesses, although still with a diverse mix. What we have here is the potential for another 1% – 1.50% per annum in additional returns (best guess, no guarantees), which does not sound like much. On a $500,000 portfolio, 1% amounts to $5,000. Multiply $5,000 by 10 years (not a long time, let’s face it) and we have an additional $50,000 in round numbers. This is not a bad gain just for making a decision around investing strategy.

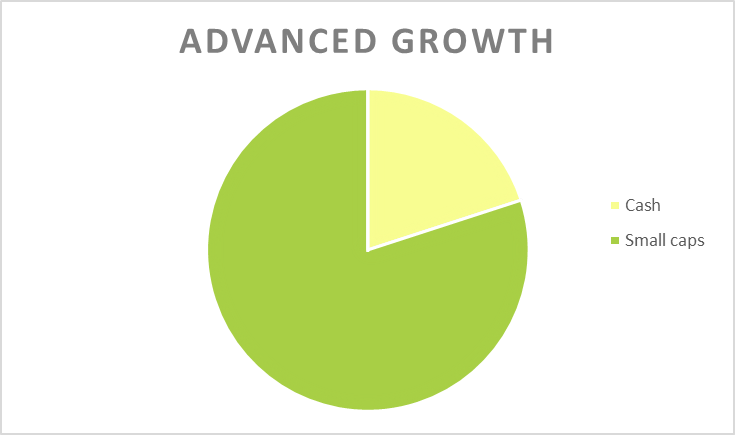

The Advanced Growth investing strategy

At WISEplanning (we are different, remember), we then have the Advanced Growth Strategy, which involves greater concentration of the portfolio as well as the inclusion of smaller businesses. They can be more volatile and more risky but of course, they offer faster growth over time. At the extreme end of an advanced growth strategy, we have only a few investments concentrated in small caps, with enough cash to maintain flexibility.

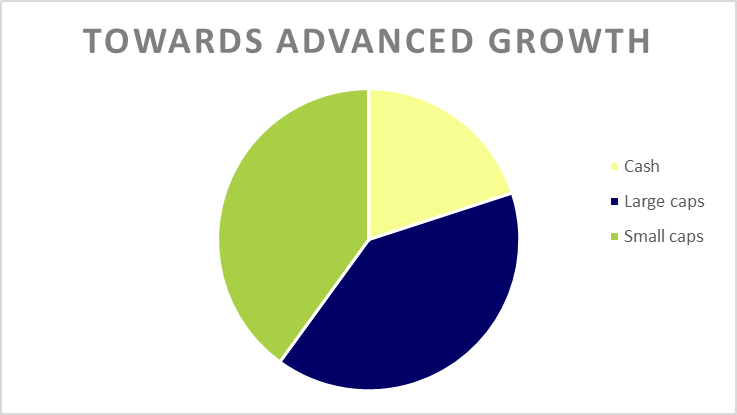

The Towards Advanced Growth investing strategy

Then, in between the Growth Strategy and the Advanced Growth Strategy we have an interim Strategy, which we refer to as Towards Advanced Growth. Basically, this just means slowly moving the portfolio from a Growth Strategy to an Advanced Growth Strategy over a period of time in an iterative and controlled manner (as opposed to a sharp transition made immediately).

And so …

So, investing and growing our assets is an important part of generating passive income. Before we invest though, if we have not done so already, it is important to prepare and set up a proper strategy (framework) for our future lives right up until ‘beam up date’ and then put together a supporting plan, with the list of actions that need to be taken to drive the success of our strategy for life (beyond investing).

Investing is an important component of the plan for life, as is the right investing methodology when we invest. The right investing methodology will ensure that capital is protected and that our assets grow as much as possible, regardless of market and economic conditions.

By progressing your investment portfolio to a more advanced investing strategy, you can improve the performance of your investment portfolio over time and increase your return on investment (ROI).

“Beware the investment activity that produces applause; the great moves are usually greeted by yawns.”

Warren Buffett