Return on Investment (ROI) Improves

Investment Perspective – June 2019

Peter Flannery CFP AFA

“Neither the investing method nor the fundamentals of the business are right or wrong because the mood of the market is favourable or unfavourable toward the “stock”. That is because when you really think about it, “stocks” (shares) are all about the financials and the trading price, the share price…the cash up value. What matters more is the economics of the business”

Peter Flannery

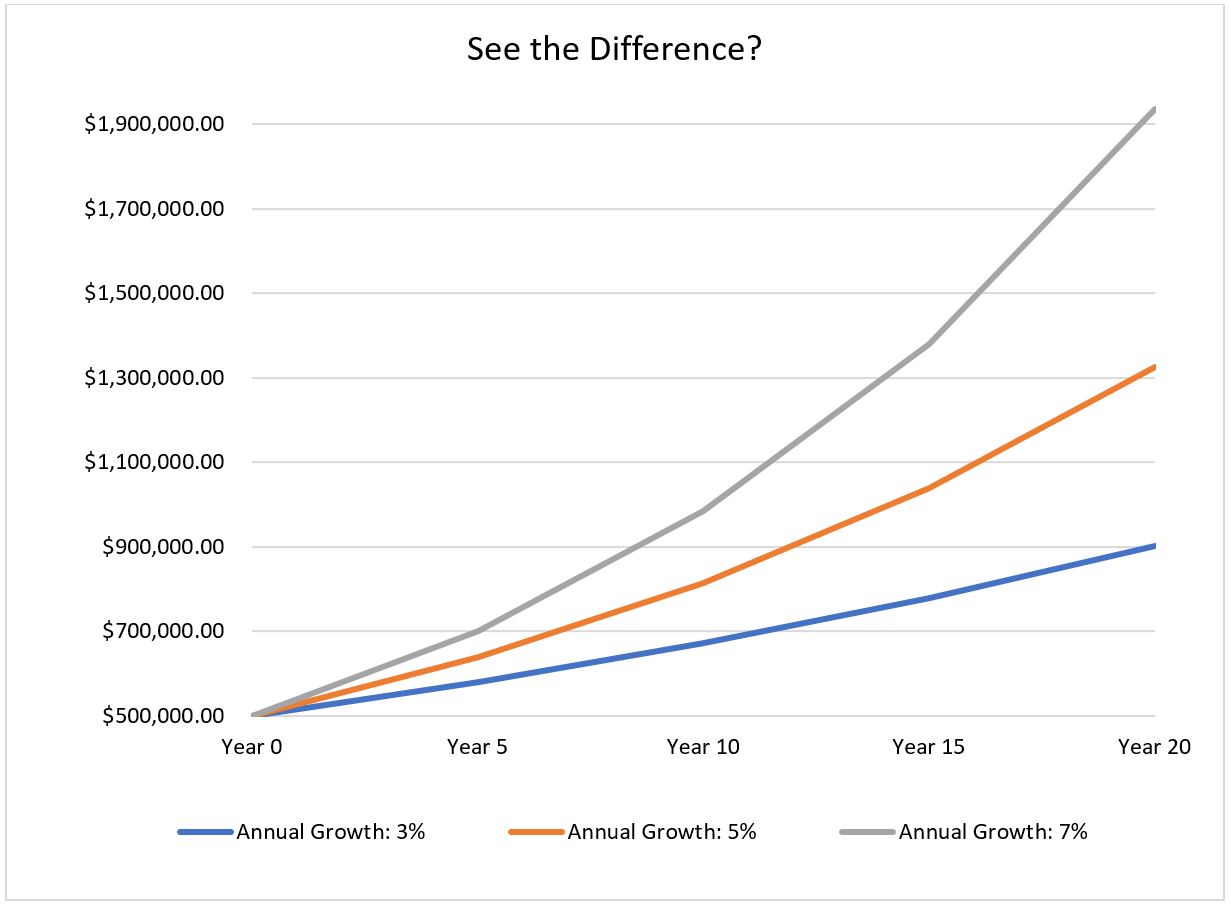

See the difference? …

We are fortunate at WISEplanning that we can improve the return on investment (ROI) without a corresponding increase in risk. How so?

There is a LOT of resource ploughed into the financial analysis of companies across the investing world – massive. I know I allocate a reasonable amount of my life to it as well; however, I also know that financial analysis (‘the financials’) has its limitations.

It is a bit like, no matter how often you add up the household budget, all of those expenses and how many different ways you add them up, those expenses are what they are. Sure, you can then decide to trim back, ‘tighten the belt’; however, that approach to budgeting also has significant limitations.

The real progress to be had with taming and fine tuning the household budget revolves around understanding spending habits and attitudes and identifying those patterns of expenditure.

I am not saying that adding it up or even cutting back is without merit. I am suggesting though that you can only go so far by adding things up and cutting back.

Budgeting by behaviour rather than by the numbers is a much more effective approach to household budgeting.

So too with investing

Investing is not just about the numbers. I identified many years ago the limitations of focusing on where to invest as distinct from how to invest.

Many people are always looking where the good investments are. The secret is, ‘how’ you invest because, that will enable you to maximise returns and easily manage risk. So, with regard to investing, it is not where you invest but rather, how.

How, how and how?

The first how revolves around establishing your investing goals and accepting the fact that making your money grow (rather than just receiving income off term deposits) is the key to helping you achieve your goals. Nothing complicated about that – OK?

The second ‘how’ is about ensuring that you have the right investing methodology. To put this another way, it is about having a system for investing and one that is fundamental.

A common approach to investing on the so-called share market is to try and pick winners based on a good idea or to chase rising share prices. This approach works until it doesn’t.

It is not reliable. It is certainly not readily replicable.

That is because, for every good idea that works and turns into real money, there are hundreds, if not thousands of ideas, that sounded good but were never going to turn into real money. Similarly, with chasing rising share prices.

The second ‘how’ then is about the value investing methodology as per Warren Buffett and Charlie Munger. By the way, there have been numerous iterations of Value Investing that have emerged in recent times. I am sticking with Buffett and Munger’s approach.

Indeed, there are thousands of analysts around the world who reckon that value investing is old hat and that investing in technology based companies is all you need to do (another discussion for another day). The bottom line is that we invest in the business and do not play the stock market.

Good businesses are those that offer value. Intrinsic value is driven by the underlying performance of the business and not the share price. The share price provides the score card, if you like. It gauges market sentiment. It is an unreliable (silly) way to gauge intrinsic value.

Good businesses, it turns out, are not those with last year’s fastest rising share price but those that have strong economics. For example, they have a competitive advantage that allows them to price (charge for their goods and services) strongly. Strong pricing means higher profits. We can see this when we look at the return on equity (ROE) – sometimes referred to as return on shareholders’ funds – and return on capital (ROC).

Return on capital or return on shareholders’ funds is a much more reliable way of establishing the intrinsic value of a business (it is not how you calculate it though) because it is based on how well management uses shareholders’ funds and total capital.

The profit the company made last quarter or last year is interesting but not that useful. How well the business is using its capital is much more valuable.

Profit is a different thing to profitability.

Profit is how much money they made.

Profitability is how well the business uses its resources and includes activity in the income statement and across the balance sheet too. Profit only looks at the income statement.

The rising share price is sometimes linked to last quarter or last year’s profit (the income statement). It excludes the balanced sheet. Do you see what I mean?

eBiz Investing

By the way, at WISEplanning, we have taken Warren Buffett and Charlie Munger’s investing methodology and developed it further into what we call e-Biz Investing.

Simply, this means investing in businesses (not playing the stock market – clever sounding ideas and chasing rising prices) that have identifiable and hopefully strong underlying economics. They are strongly positioned in their niche and have pricing power. They may have an eco-system (eg Apple) and will likely have strong branding (the short cut to the decision making process for consumers) e.g. Google.

We are obviously carrying out financial analysis however e-Biz Investing differs from the usual approach because it includes the underlying economics of the business. Share brokers and other analysts do not always analyse the business and in my view, are therefore at a disadvantage when it comes to locating investments that protect capital and grow it long term – regardless of economic conditions.

The third how

The third ‘how’ is about improving returns without a corresponding increase in risk by concentrating the portfolio (more money in fewer investments within the portfolio) and building in more small caps (businesses with a market capitalisation of less than US$2 billion). To be clear, picking even large businesses that make sustainable profits long term is not easy (Warren Buffett has made this comment more than once). Picking small businesses is much more difficult.

Concentrating the portfolio and adding small caps does increase risk. The point is that, because of the strength of the methodology, the increase in risk is small compared to the additional money generated long term.

For example, some simple analysis easily tells us whether or not a small cap has any debt. Debt is not necessarily the wrong thing but needs to be considered in the context of a number of other factors.

A small business that has grown substantially without any debt like, for example dotDigital, indicates not only a good business model but also prudent management. This is not a reason for investing in a small cap but an example of how we can limit risk by looking at the level of debt. More importantly as I just pointed out, why a small business can grow without debt might mean a sound business model and prudent business management.

Small businesses generally grow faster than larger ones, understandably. The point here is that a controlled and methodical approach that helps you as an investor to improve your return on investment (ROI), on purpose, by design, is superior to a more ad hoc approach where you look for shining stars and attempt to secure those investing “king hits” that make you rich quick without time and effort. What do you think?