How to Drive Investing Performance

Investment Perspective – February 2020

Peter Flannery CFP AFA

“Neither the investing method nor the fundamentals of the business are right or wrong because the mood of the market is favourable or unfavourable toward the “stock”. That is because when you really think about it, “stocks” (shares) are all about the financials and the trading price, the share price… the cash up value. What matters more is the economics of the business”

Peter Flannery

Two types of economics – one is critical to your investing success

There are two types of economics.

One is considered to be the branch of knowledge concerned with the production, consumption and transfer of wealth.

It includes the likes of measures of economic growth, unemployment, the rate of money flow throughout the economy, measures of inflation and a variety of other measures.

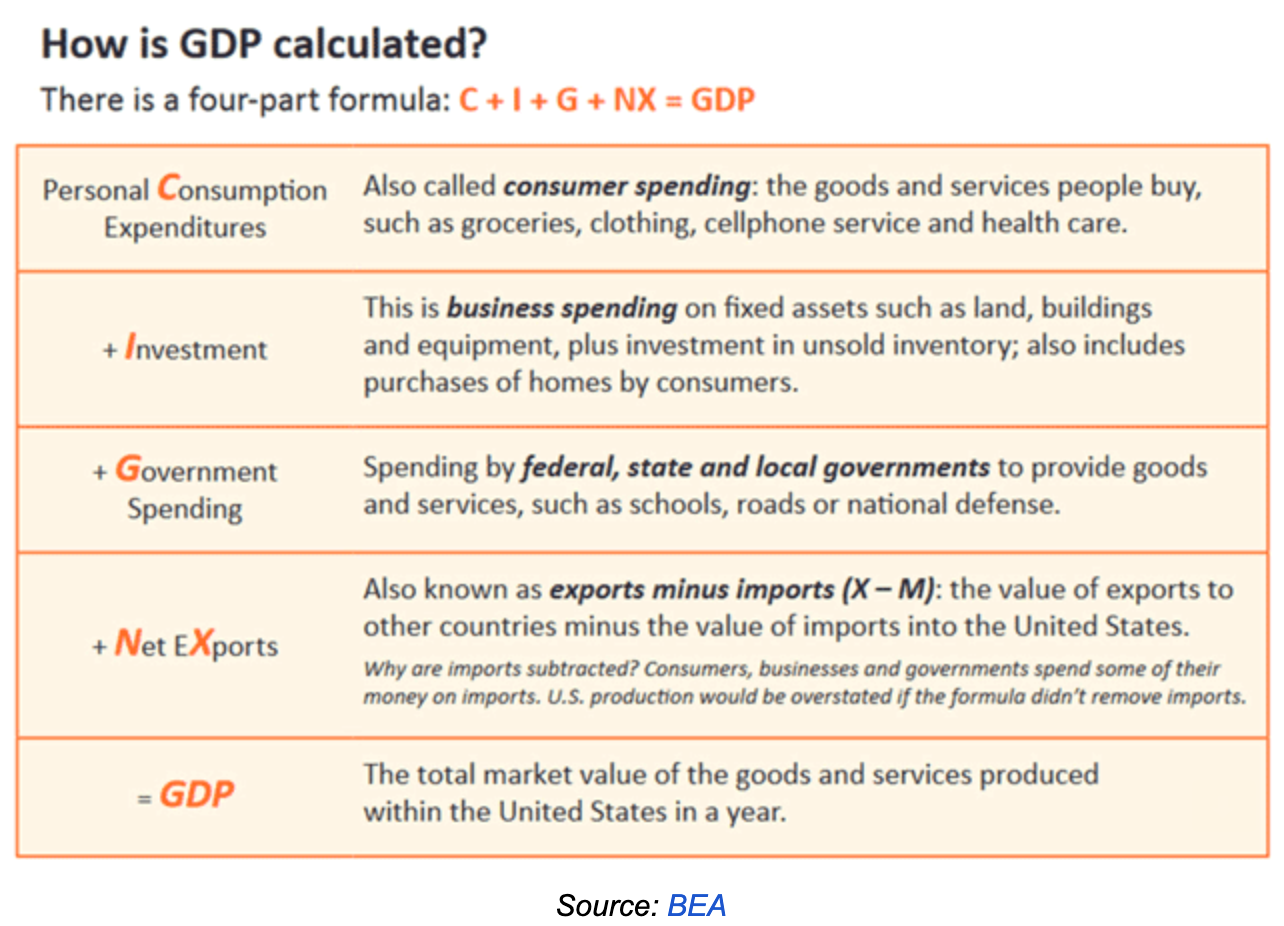

One of those measures of economic growth is gross domestic product (GDP).

The above diagram outlines an explanation of economic growth as measured by GDP.

Gross domestic product or GDP is a widely used measure of economic productivity around the world.

When we take it at face value, it is a simple measure that is easy to understand; however, when we explore in more depth, we start to realise that it is a complex combination of data that may or may not be actually giving us a real measure of economic productivity and growth across an economy (in this case, the US economy).

The above diagram explains how GDP is calculated (in the US).

When we start to drill down and explore what production really means, economists start to come up with different views.

Back in the day, prior to the technology revolution and digital technology, GDP was more a measure of farming and factory production, whereas now we have things like social networks and other technologies that contribute to economic growth and prosperity.

As John Mauldin reported recently, the Nobel prize winning economist, Robert Solow, quipped in the late 1980s, that “You can see the computer age everywhere but in the productivity statistics.”

The short of it is that, getting good data to be able to generate reliable analysis is one issue. Another problem is whether or not central bankers and government statisticians would use this data anyway!

The point I am looking to make here is that there is a significant amount of attention given to economics as it relates to a country’s state of health but precious little given to what comes next …

The Economics of Investing

Investors pay lots of attention to economic data that relates to the health of an economy.

This data can be useful, but only really for the pricing of an investment (the trading price). In other words, economic data impacts on the mood of the market. The mood of the market determines the trading price of an asset, particularly direct shares that bob up and down pretty much on the basis of market sentiment from one day to the next.

To be clear, the fundamentals of the underlying business are not usually reflected in the trading price in the short term.

Value investing, as per Warren Buffett and Charlie Munger (leading on from the teachings of Ben Graham) is focused almost entirely on the fundamentals of the business in which they invest and in particular, taking into account the economics of the business (as distinct from the financials).

Of course, we analyse the financials of a business in order to get the full picture. The financials though tend to be historical.

The economics of the business tend to be intrinsic and indeed drive the financials.

To be clear, an increase or decrease in business profit (earnings) is worth knowing about. That may impact on the trading price of a business. If the profit is up, the trading price may move up. If the profit is below expectations, then the trading price may move down, sharply if the disappointment is significant.

At the moment, Synlait Milk comes to mind. The underlying economics of the business remain ‘intact’, to speak, despite the fact that profit has declined by a reasonable amount (nothing that I see any need to be concerned about). Indeed, it looks like an opportunity for us to buy more.

Anyway, value investing has been successful for decades (notwithstanding the skillset of Warren Buffett and Charlie Munger as well as the underlying methodology) which as I mentioned earlier, is intrinsic to the underlying business.

We do not play the stock market. We invest in the underlying business. Most others, of course, play the share market. They cannot help it. They are infatuated with the trading price.

The More Important Economics

The more important economics relate to the asset, not the state of health of a country’s economy.

Apart from some impact on the trading price, the state of a country’s economy will have limited impact on the underlying economics of a business.

Trading conditions can be tough however those businesses with strong economics (eg the competitive advantage, brand strength, the eco-system) will be resilient and continue to perform long term.

As you know, when everybody is happy, those fundamentals can be overlooked as the trading price reaches toward the sky!

Can you trust the market?

For example, over the last 12 months, Apple’s trading price has increased over 100%. Apple is a great business; however, I very much doubt that the economics of Apple have improved by 100%!

So, why do we not sell Apple then?

For those who are more defensive investors, that indeed, is what we might consider.

For more advanced investors, however, we are investing in the business. We see volatility as our friend, not our enemy. When we invest in the underlying business, we take a long term view, wanting to participate in the long term growth of our business.

The compounding long term growth of a business with strong economics is a very acceptable investment, particularly when compared to many other options.

“The trading price of a stock tells you exactly nothing about the underlying business.”

Warren Buffett