What The Markets Are Telling Us

Investment Perspective – February 2018

Peter Flannery CFP AFA

“Neither the investing method nor the fundamentals of the business are right or wrong because the mood of the market is favourable or unfavourable toward the “stock”. That is because when you really think about it, “stocks” (shares) are all about the financials and the trading price, the share price…the cash up value. What matters more is the economics of the business”

Peter Flannery

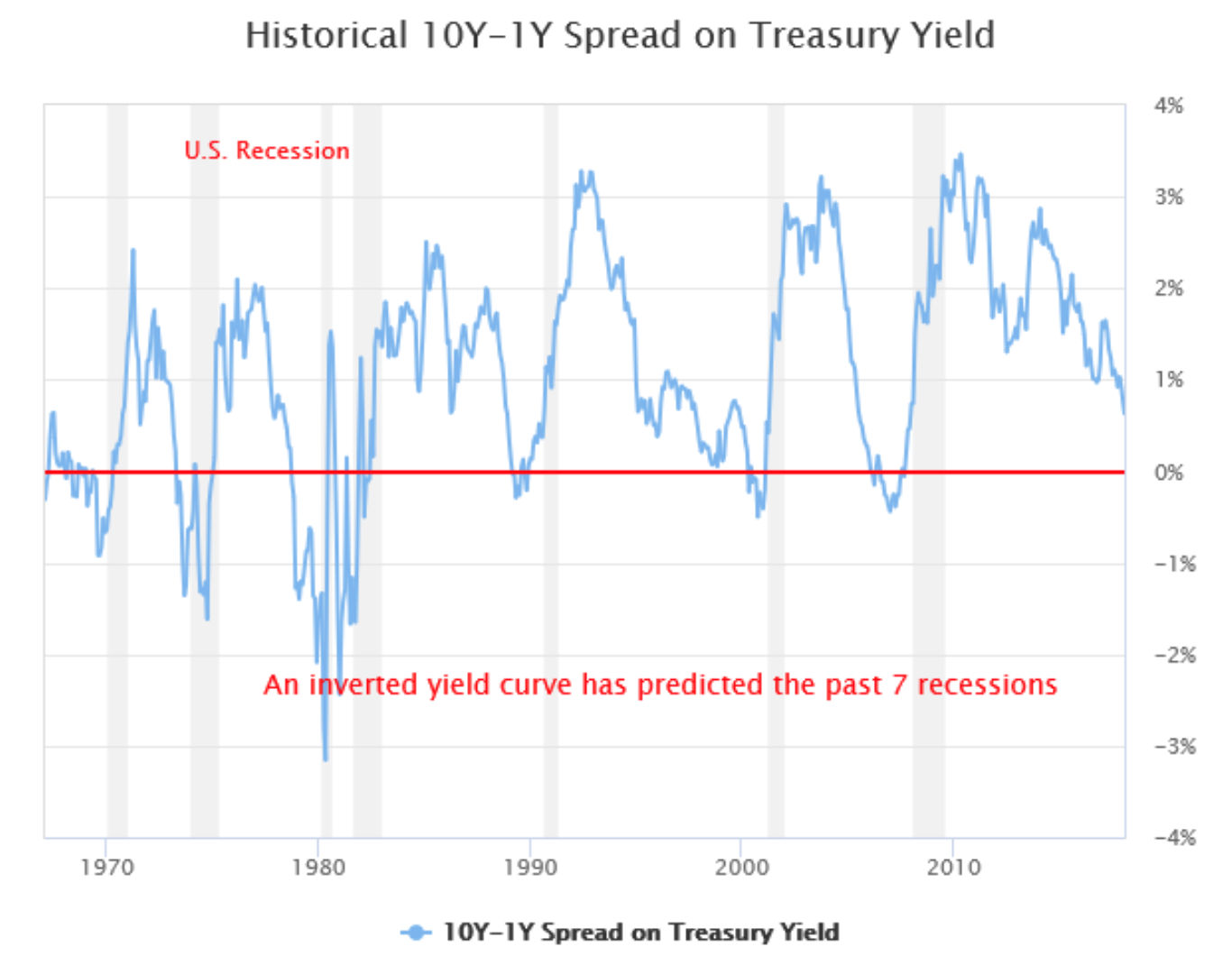

The blue line in the above chart shows the difference between 10 year Treasuries and one year Treasuries.

The above chart is the market (analysts) looking for market driven patterns from the past that provide indicators about what may happen in the future.

The above chart is quite compelling. The short of it is that the blue line declining is suggesting that another recession is imminent.

If that’s true then we can expect the trading prices of shares to decline from current levels.

For those who prefer a more defensive approach, be it only temporarily, they may consider reweighting some of the growth assets in their portfolio towards defensive cash to some degree.

For others who are happy to ride through the volatility, they will likely make no adjustments on the basis of what may or may not happen to prices because of what the mindless market may dictate.

Either way, I would argue it’s not a bad time to have a reasonable level of cash.

How much cash?

The amount of cash will depend on your own circumstances which is something we can discuss if you like. An amount of cash somewhere between 7.5% and 30% of your portfolio could be prudent if that blue line continues in a downward direction and if the market responds as it has in the past.

What is an inverted yield curve anyway?

An inverted yield curve is when the yields or the coupons on bonds with a shorter duration are higher than the yields on bonds that have a longer duration.

This typically relates to six month or one year Treasury Bills in the US where the yield is higher than say 10 year or 30 year Treasuries.

Normally short term bills yield less than long term bonds.

So what?

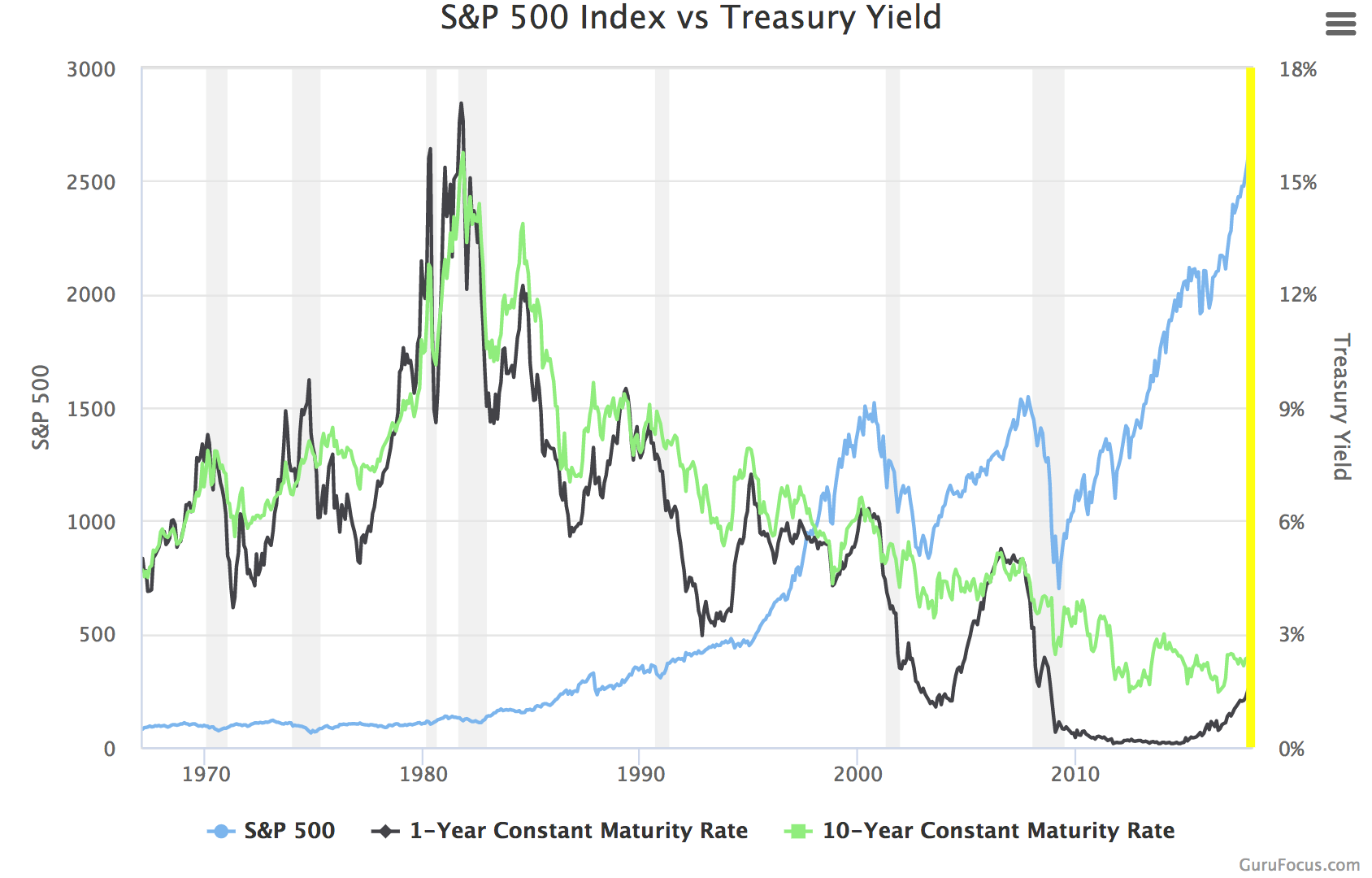

The above chart shows the relationship between the US sharemarket as measured by the S&P 500 when compared to the yield on one year bond maturities and the yield on 10 year bond maturities.

The so-called inverted yield curve means that investors have little confidence in the economy generally or that confidence is fragile (note the word confidence). Simply, the market has the belief that they will make more money by holding onto longer term bonds than if they buy short term Treasury bills in this situation.

When the market believes a recession is coming, the expectation is that the value of short term bills will plummet sometime over the next 12 months or so. This can happen because the Federal Reserve may lower the Fed funds rate when economic growth slows. Short term Treasury bill yields tend to track the Fed funds rate. (This is the interest rate banks charge each other to lend Federal Reserve funds over night. The Federal Reserve uses the Fed funds rate as a tool to control economic growth. This means the Fed funds rate can be an important indicator to watch.)

Anyway, the general idea is that, as investors flock to long term Treasury bonds, the yield on those bonds can decline. That’s because they are in demand so they don’t trade at such a high yield in order to attract investors (simply supply versus demand). The demand for short term Treasury bills falls, so Treasury bills need to offer a higher yield to attract investors.

At some point the yield on short term bonds rises higher than the yield on long term bonds and therefore the yield curve inverts.

In a so-called “normal” growth environment, the yield on a 30 year bond in the US might be approximately three percent (e.g. short term bills say 2.00%pa compared to long term treasuries at say 5.00% pa) higher than three month bill.

However, if investors believe that the economy might be slowing in the short to medium term and then possibly speeding up again in the medium to long term, the market might prefer to tie their money up until then, rather than have to reinvest it sooner at a much lower rate.

That might be too much information however it does provide some detail around the inverted yield curve which the market is focusing on at the moment (and how to complicate our lives!). Of course, because the market is focusing on it now, it could important at some point from a pricing perspective.

The business of investing in business

Investing in a business is very different to investing in the stock market.

For example, Microsoft and Apple provide products and services that to the uninitiated look pretty much the same. However to those who understand the difference, that difference is significant.

Investing in the sharemarket probably looks and sounds not too much different to the way one might invest in a business.

However, once we understand the difference we realise that difference is huge.

An unarguable fundamental of business

For example, the quality of owner earnings of a business is not a financial that many sharemarket investors would consider. However, for us as Value Investors it is very important because it provides information about the strength of the business and good growth ahead for investors long term, regardless of an inverted yeild curve or resulting sharemarket crashes.

However, the market is focused on the possibility of recession which is why you will see a lot of information, almost building on itself, promoting the idea of pending economic recession, a sharemarket crash and a so-called “blood bath”.

Sure the trading price of our business with quality owner earnings may also decline as sharemarkets crash generally, however…that is our opportunity to buy more and a better price – not complicated.

Focusing on what works makes the most money

Attempting to “second guess” or outwit the random walk of markets long term is an approach that the market itself believes is not only appropriate and doable but of course it is widely practised.

It can work from time to time but is not something that appears to work well long term.

Because there is an army of traders, speculators, momentum investors (sharebrokers), fund managers and the like, this approach is almost considered standard operating procedure for investing in the share market (wrongly in my view).

Investing in the sharemarket is not the same thing as investing in a business

Humans, being what we are, we tend to follow the herd. Particularly in times of uncertainty, most people look to others for direction.

For example, the citizens of any country will look to the government to sort things out when they don’t think that things are right or when there is an event that is impacting on them financially (e.g. recession). All kinds of intricate and at times complicated financial analysis is carried out by sharebrokers, fund managers, some investment advisors and some investors as though the secret to financial success exists in the complexity of the financials and the calculations around those financials. In case you are wondering, it just isn’t so.

Investing in a business is certainly about considering the financials however the less complicated the better. How well a business uses its capital is a key indication of a good business and good management and can simply be measured by return on equity and return on shareholders’ funds. It’s not the only financial, however it is key.

Investing in shares is not the same as investing in a business

The essential difference is that shares are selected through financial analysis whereas businesses are selected through different financial analysis along with the underlying businesses’ economics.

At the risk of over-simplifying things, other than an entry price, worrying about markets crashing is only very slightly more useful than worrying about meteorites striking planet earth, creating a dust bowl, blocking out the sun and killing off all vegetation.

By the way, if you are wondering what are those all important economics, perhaps the key one is the sustainable competitive advantage. A business’s sustainably strong position inside a market niche ( that niche may be global – e.g. Google (Alphabet) represents better pricing power and ultimately more profits for investors. Grow and compound that over 20 years or so and there you have money working for you, more and more every year.

Sure, markets crashing and “blood baths” sloshing with disaffected and fragile sharemarket hopefuls along with the popular media making a feast of even the slightest bit of negative news around the decline in a sharemarket index will unsettle most people.

That is what separates those people from their money and the significant amount of other money that can be made by investing in good businesses with strong economics and staying the course.

But everyone on the internet is saying that markets are expensive and they’re going to crash

If you worry about prices declining you may benefit from going back and reading all my Investment Perspectives over the last two years to help you reposition your investment perspective so that you avoid mindlessly running with the herd.

If however you like the idea of a market correction because you know that better pricing will be available then and you are pondering whether or not to increase levels of cash, get in touch with me and we can take a look at your portfolio and have a chat.

Reduce Australasian weightings?

I have been suggesting to many of my clients to consider perhaps scaling back some of their Australasian holdings in favour of cash so that when prices decline at some point in the future (it could be soon, it could be a long time away) they have a sufficient level of cash available to take advantage of better buy prices then.

On the other hand you may be happy to remain fully invested if your portfolio has more of a global tilt already and just ride through the volatility.

Buying good businesses at favourable prices has almost become a cliché in investment circles (but amusingly is not widely practiced!).

However if we know how to do that and execute it properly we have a good chance of making money longer term, regardless of sharemarket crashes, media banter, and all manner of other distractions getting in the way.

We will just buy good businesses at fair prices and either hold them long term to enjoy the compounding rewards or kick them out if their economics deteriorate or other options become available that are more favourable.

That by the way has little to do with share prices bobbing up and down, sharemarket crashes and investors worrying about what may or may not happen.

“Everyone wants a fancy sounding story for why the stockmarket goes down, but in most cases it’s as simple as “because it went up a lot””.

Cullen Roche, founder of Orcam Financial Group