Markets Recover But For How Long?

Monthly Market and Economic Update – February 2022

Peter Flannery Financial Adviser CFP

“If you have one economist on your team,

it’s likely that you have one more than you’ll need.”

Warren Buffett

Key Points:

- Uncertainty for the market on a number of fronts.

- Inflation spiking, what it means.

- Interest rates rising.

- Coronavirus – are we there yet?

THE MARKETS

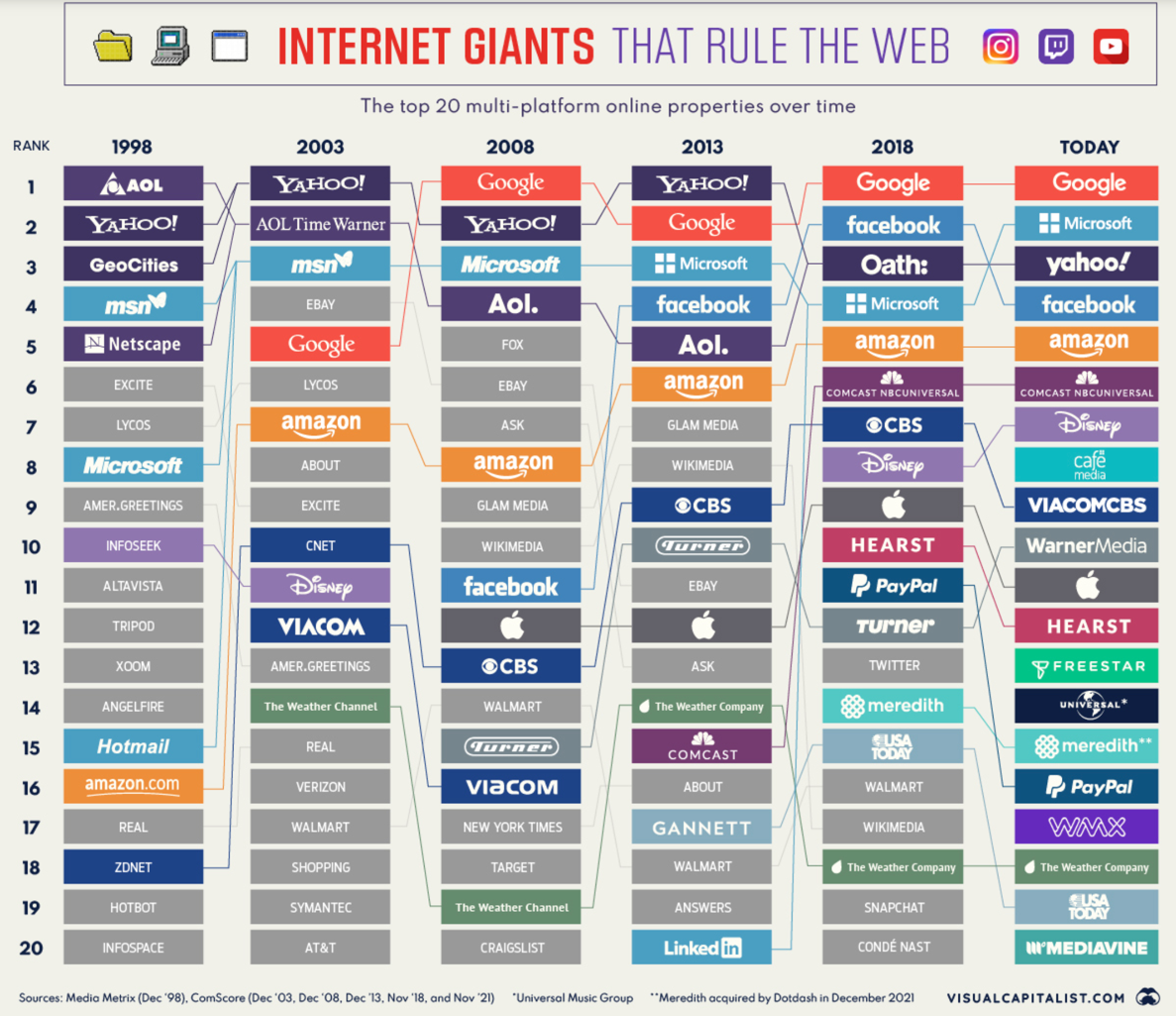

The image above captures its data mostly from comScore U.S. Multi-Platform Properties Ranking. It looks at which of the large internet organisations have evolved to stay on top and which have faded into so-called internet lore.

As people around the world moved online, the iconic AOL compact disk was the key that opened the door to the world wide web. Back in the day, there was an estimated 35 million people accessing the internet using a compact disk.

The company size was increasing, reaching a valuation of around $222 billion in 1999. Fast forward to 2013, about.com, ask.com, and answers.com were among the largest websites in America. Of course, Google has taken over that space largely due to its superior algorithms and smart business management.

The point here is that businesses come and go. The trick for us is to identify those that not only survive, but stay around and can grow to become successful, making us as investors wealthy along the way. Investing in the business is what it’s all about (not playing the share market).

The chart on the left shows the US share market (the Dow Jones) over the last six months. The chart on the right shows the US share market (the Dow Jones) over the last year.

Volatility at last. Although not enough to get us excited. We need more. We’ve seen volatility of around 20% for the NASDAQ and circa 15% on the Dow Jones.

Basically, that makes trading prices generally less expensive but not cheap. Within that, though, there is some emerging opportunity. Specifically for us as e-Biz Investors, because we invest inside the market rather than across it, we can select isolated opportunities within the market.

The e-Biz opportunity

There are a couple of ways to look at investing opportunity as e-Biz investors.

The obvious way that we all know and love is to buy businesses where the trading price is depressed and cheap.

It sounds logical and simple, although we need to be sure that the business is sound to know that we’ll get our money back, and indeed, as the business pushes through the market dilemma or the internal challenge that emerged, that the business will grow. That way, the trading price should spring back up again, although it won’t do so immediately and certainly not to any calendar that you and I might refer to. In this situation, the trading price recovery will be based on market sentiment and can take time.

The second way that is perhaps less obvious, is to look for quality businesses that will grow and compound long-term.

Some of these businesses actually don’t look that exciting. For example, Heico is a good example of a business that has been unspectacular but, over the long-term it has grown successfully, helping to build an investors’ net worth along the way.

Back here in New Zealand, Ebos is another good example of an unspectacular but sound business that has grown over many years.

So looking for opportunities where quality businesses see their trading price decline sharply is a great way of capturing this opportunity without taking undue risk. It’s a different thing though, to speculating on shares hoping that the trading price will recover or continue to rise because everybody likes it (popular).

So what’s bothering the market, and why the volatility?

There are a number of items that the market has been thinking about of late.

But the main ones are rising inflation, the talk of rate hikes out of America over 2022, and the omicron virus coming back on the scene again, causing concern across the market.

There’s also been some geopolitical tensions, specifically along the border of Ukraine, with the build-up of Russian troops and America sending troops in that direction in an apparent show of force. Early days yet, however, something to keep an eye on. Expect quite a bit of sabre-rattling in the not-too-distant future.

Looking ahead over 2022, my expectation is that, whilst the market seems to have come to terms with its worries from January this year, I expect that there may be further volatility ahead as those rate hikes unfold and possibly as more jawboning around those rate hikes takes place along the way.

There is also tapering (the opposite of quantitative easing) as monetary conditions become tighter.

In my view, it’s one thing for the market to know that interest rates are rising and to react accordingly, knowing what it means. It’s another thing in my view for the market to actually cope with it when it becomes real.

The reality is that rising interest rates mean debt servicing costs increase. For some participants, that will be a reality that is too much to bear at some point – guarantee it.

That’s why I believe we may see further volatility ahead. I think it’s important to remember too that markets can send trading prices any which way, for reasons that tomorrow may not even be on the radar today.

The important point I’m getting to is that even though markets might be volatile, we may still see market indexes over 2022 and 2023, along with the cash up the value of your portfolio increase over that time, despite the volatility along the way.

It’s important, therefore, not to confuse volatility with declining markets. You know the old classic…

“In the early years when we invest, the voting machine determines how much money we make (market sentiment). The longer we invest, the more the weighing machine (underlying business fundamentals) determines how much money we make.”

Warren Buffett

The above diagram outlines a variety of risks over the next ten years. They are estimated future projections and as such may or may not materialise. Perhaps a useful starting point for further consideration.

As Warren Buffett once said, “There is always something to worry about”.

What he meant by that was that the markets are lurching from one problem to the next, and between times what it sees is one big opportunity to the next.

In short, the market can be all over the place from time to time.

That is why it’s important to be careful about listening too intently to daily market noise.

This is not to suggest that we should ignore the market. Rather, we should listen to what the market is saying and then read between the lines knowing what we know about investing in the business.

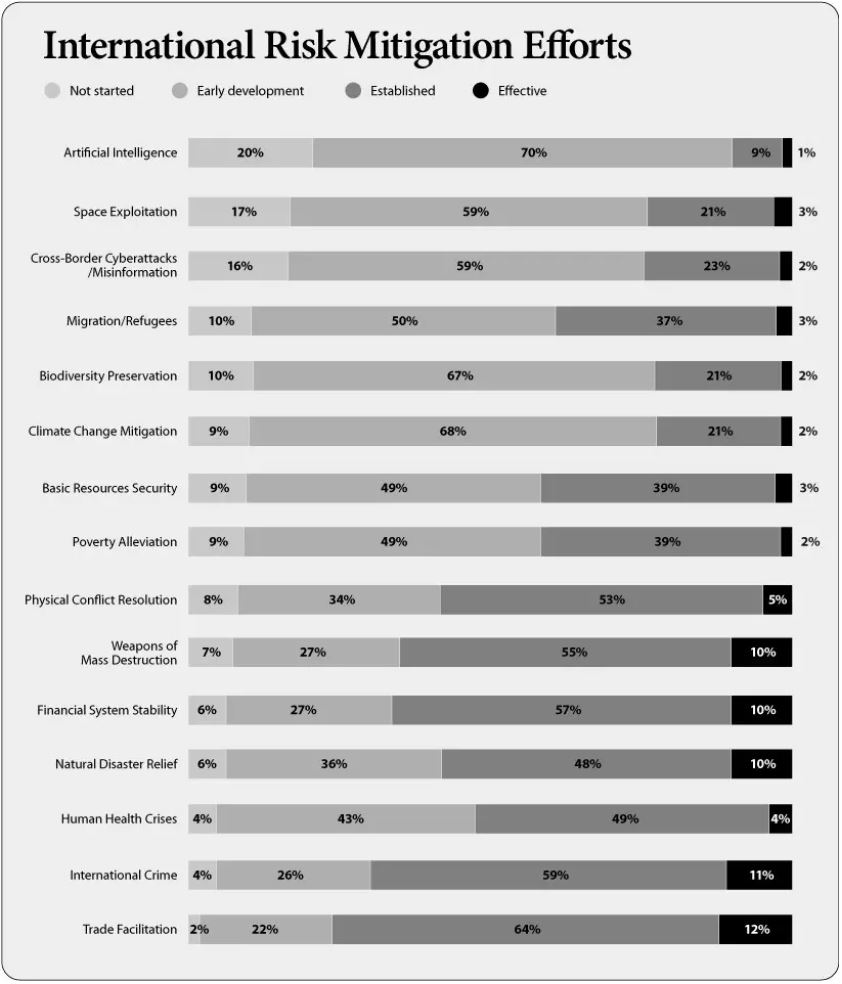

The above table demonstrates and estimates risk mitigation efforts and the progress currently underway.

Risks tend to come and go. Back in the day, international crime and weapons of mass destruction were real risks that some people today believe we’ve effectively implemented plans for mitigation.

Looking ahead, cross-border cyberattacks, misinformation, and the misuse of artificial intelligence are new areas that some people are now more concerned about. Humans can be stupid, but they can be resilient and innovative!

The above diagram shows in descending order the largest listings of businesses over 2021.

The point of the above diagram is that, even though there were risks over 2021, innovation, productivity, and progress continued.

Let’s continue to focus on that, especially when markets become volatile, which they surely will…

The Global Economy

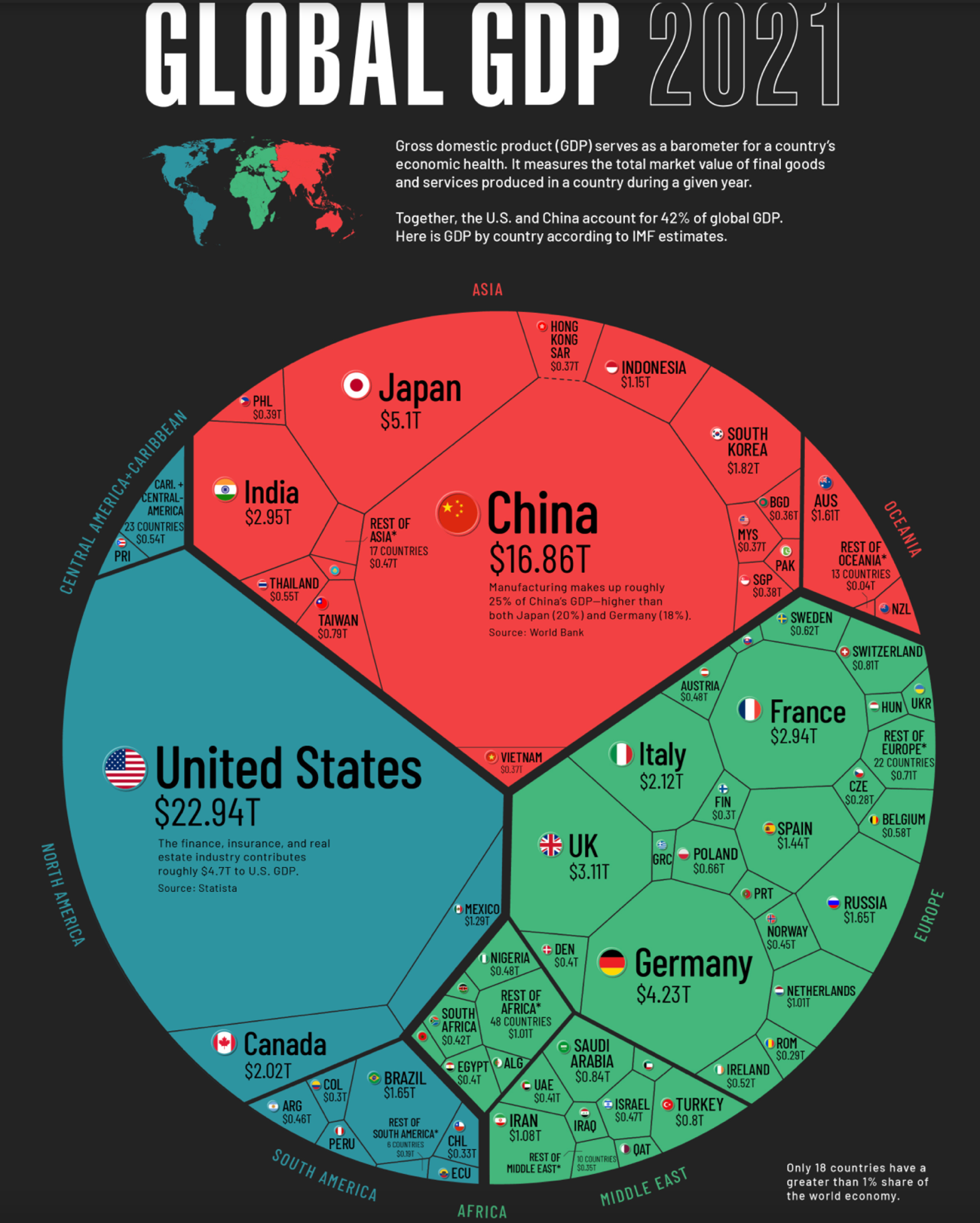

The above graph shows the largest economies around the world as measured by Gross Domestic Product (GDP).

Although somewhat of a blunt measure, economic productivity can be measured by Gross Domestic Product (GDP), or Gross National Product (GNP). But either way, we can see that productivity continues, as demonstrated by the above diagram. Countries continue to grow and prosper, albeit at different paces and at different levels.

More recently, what has emerged is that Western economies appear to be handling the coronavirus more effectively than a number of developing and emerging economies.

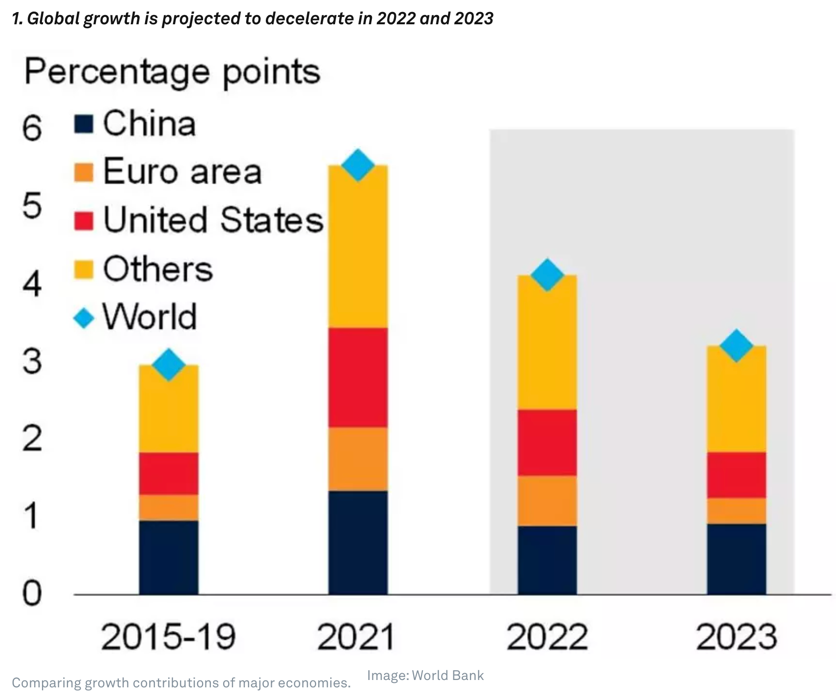

The above graph tracks historical and projected economic growth in the main economies around the world.

The graph above from the World Economic Forum shows economic growth declining from 2021 through 2023. This is a modest decline though over 2022 from 5.5% to 4.1% growth according to the World Bank. This reflects the ongoing disruption caused by Covid 19 as well as supply bottlenecks.

Ongoing downside risks for the global economy would include the likes of ongoing omicron disruption, further supply chain bottlenecks, the possible financial stress for some economies, climate-related disasters for some economies, and a possible weakening of some long term growth drivers.

Generally, a number of emerging markets and developing economies have limited policy space to provide additional support if required. These downside risks may be amplified, increasing the possibility of a potential hard landing for some economies. At this stage, it’s difficult to see a hard landing for the global economy.

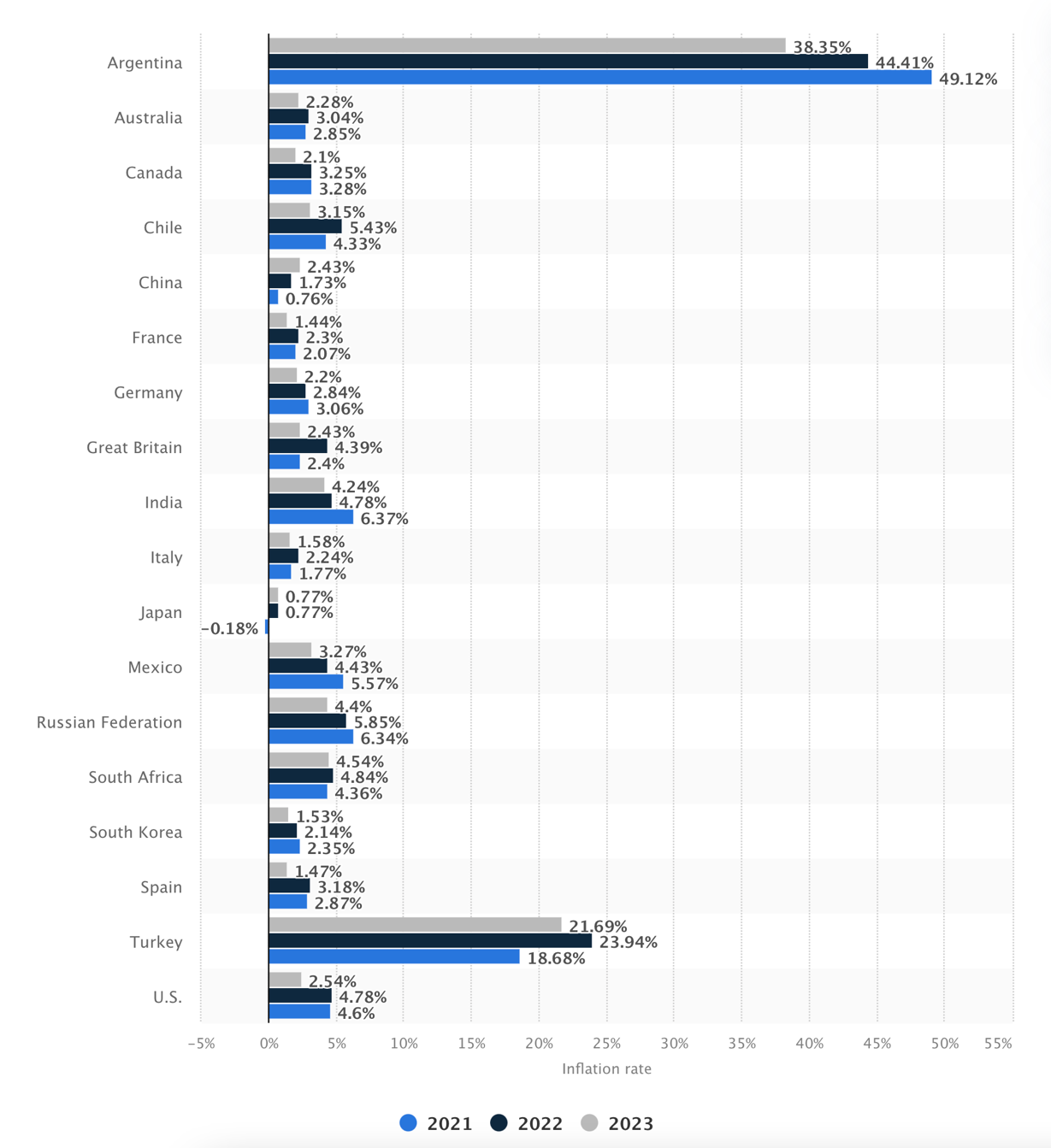

The above graph shows an inflation outlook from 2021 through 2023, country by country.

We all know that bottlenecks and pent up demand has enabled inflation to spike as the global economy recovers from the pandemic recession.

Interestingly, it wasn’t that long ago that the global economy was facing off squarely against serious deflation. Central bank intervention (rightly or wrongly) has helped to stove off imminent deflation and global depression. Here we are now with inflation spiking in a number of countries across the globe.

You may possibly be watching the debate around whether inflation is transitory or more permanent. I’ve argued that it is both. The more sticky types of the inflation will revolve around the likes of rising wages costs.

The reason the global economy watches inflation closely is because it may mean interest rates rise.

4% or 5% interest rates on mortgages doesn’t sound like that much if you’ve lived through the 1980s, 1990s, and the 2000s. However, it’s a lot if you haven’t had a mortgage that long (the last 5-10 years), and you’re currently used to interest rates of around 2-3%.

An interest rate of 5% is possibly close to a doubling in the monthly servicing cost of a mortgage. With asset prices amplified by those low-interest rates, this may prove to be a challenge for those who are possibly overextended with debt servicing. Time will tell…

The above graph shows forecast salary changes for 2022 by world region.

Some inflationary drivers, I believe, are transitory and temporary. However, wages is one of those sticky inflation drivers that may last for longer than expected and therefore provides support for ongoing higher levels of inflation.

Generally, it appears that a number of Western economies will almost certainly see wage increases over 2022, whereas this outlook is more mixed when we start looking at emerging and developing economies.

New Zealand

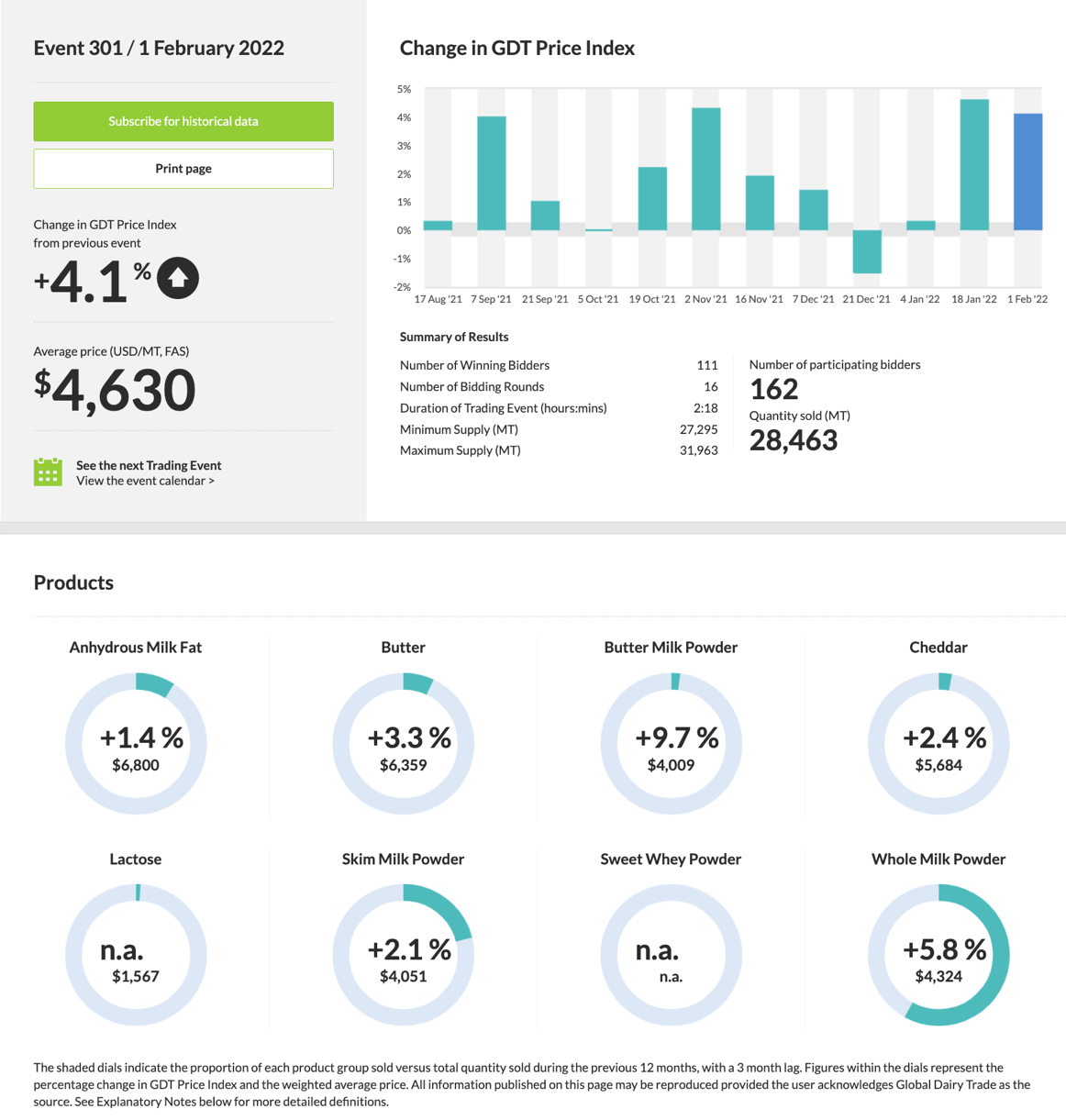

The above info stack shows a variety of information around the dairy auctions rate and milk-fat pricing.

New Zealand relies somewhat on the dairy industry for our standard of living. Tourism has been vying for number one or number two position, although with visitors to New Zealand numbering 350 over the last 12 months or so by the most recent count (a long way from the recent 70,000pa), it’s difficult to see tourism retaining the top spot anytime soon.

The good news is that demand for dairy products continues to remain buoyant, as evidenced by the blue bar to the right of the top graph above.

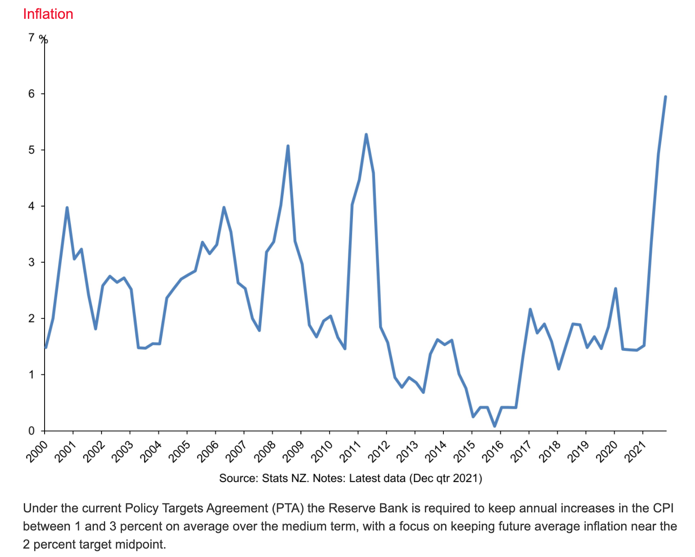

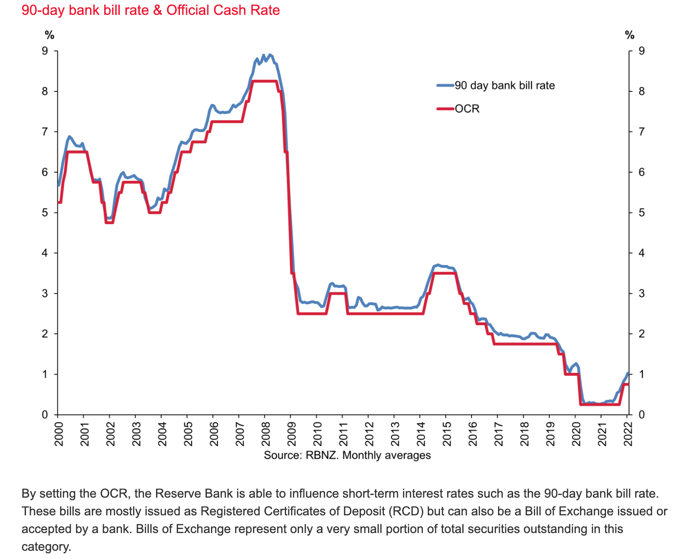

The graph on the left tracks inflation in New Zealand, and the graph to the right tracks the 90-day bill rate here in New Zealand as set by the New Zealand Reserve Bank. The above two graphs go side by side because rising inflation may well mean rising interest rates, which is already underway here in New Zealand.

As I’ve mentioned elsewhere, even though a 5% interest rate doesn’t sound like much, it may be a lot for those servicing debt with interest rates currently at 2.5%. That’s almost a doubling of servicing costs for some.

The real question on everyone’s mind is how far up will interest rates rise.

Difficult to know for sure because, of course, there are a number of moving parts globally that contribute to the answer.

At this stage, my best guess would be somewhere around between 5-6% per annum over the next couple of years or so. There are a number of variables that could change that. However, that’s how things look right now.

For those of us who remember interest rates at 15-20%, 5-6.5% doesn’t sound like much. From the current low base now, that increase is quite a lot and a reasonably serious headwind for some individuals, some business owners (large and small), and generally for the New Zealand economy. Along with that, too, we may have rising wages.

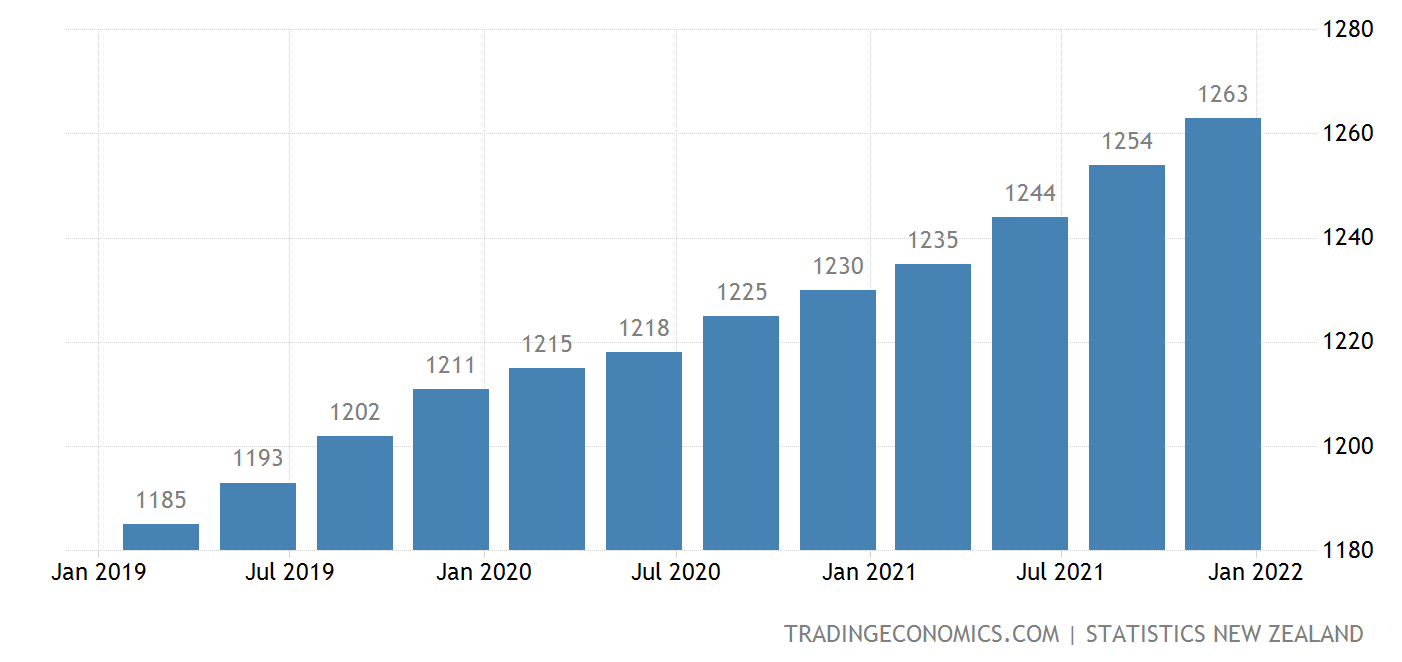

Wages Growth – New Zealand

The above graph shows the growth of wages in New Zealand from January 2019 to January 2022.

New Zealand’s annual wage inflation as measured by the Labour Cost Index rose by 2.8% over the 4th quarter of 2021. This is up from a 2.4% increase over the prior period. It is interesting to note that public sector wages grew 3.1%, a 2.0% gain from the previous quarter, while the private sector wages grew at the slower pace by 2.5%, up from 2.2% in the prior quarter.

Like many other countries around the world, labour shortages are putting pressure on wages costs. Therefore, it is possible, even likely, that we may see wages rise in some countries around the world, including here in New Zealand.

That may help to underpin and indeed put further upward pressure on inflation ( and therefore interest rates).

At this stage, my view is that the transitory inflationary components may dissipate over the next 12-18 months and to some degree, that decline might be offset by the ongoing rise in wages costs. I will keep you posted.

To Summarise …

The global economy continues to grow as it emerges from the global pandemic recession. That is a good thing.

It would appear that by around mid-2022, the omicron virus might have burnt its way through a number of the population in most developed economies, including potentially New Zealand.

It is interesting to know that at the time of preparing this paper, the spread of omicron in New Zealand, whilst it has increased, has still not yet spiking strongly. It might happen soon.

Ironically, the longer it takes to spike, the longer we all have to suffer and tolerate the impediments to our normal lifestyle.

New Zealand as an economy has been quite resilient over the last couple of years and is in reasonably good shape financially, although we all owe a bit more now, given the borrowing that has taken place since March 2020 (coming up for two years ago!).

Although I haven’t mentioned it much in this update, property prices continue to rise throughout New Zealand. However there is some strong evidence now that property prices are flattening out and in some areas, there is some evidence of a lower clearance rate at auctions.

One would expect, with the hype disappearing out of the system and the reality of increased interest rates, along with tighter credit as the credit cycle in New Zealand continues to move on, that ever-rising residential property prices may have finally peaked. We remain of course, among the most expensive in the world still. Crazy!

Elsewhere those geopolitical issues are something to watch, as is inflation, wages growth, and rising interest rates.

Otherwise, in our investing methodology we trust and therefore, steady as we go…