Overcome This To Invest Successfully

The Investment Perspective – May 2021

Peter Flannery Financial Adviser CFP

“Neither the investing method nor the fundamentals of the business are right or wrong because the mood of the market is favourable or unfavourable toward the “stock”. That is because when you really think about it, “stocks” (shares) are all about the financials and the trading price, the share price… the cash up value. What matters more is the economics of the business”

Peter Flannery

The Tricky Dilemma

I am referring to the anxiety that some investors face as they are exposed to the daily slew of populist data (designed to attract attention and sell advertising) from popular media, particularly when markets are uncertain and scared.

Referring to it as news is to me a real stretch. Thinking of it as research or useful investment information is frankly naïve.

What’s interesting about market ‘noise’ is the variety of different responses I see across my clients. Generally, they favour volatility and are keen to take advantage of it.

And whilst I’m generalizing a bit, there are some though that sometimes overthink it. They tend to be those that with a higher level of education and / or high levels of intelligence.

The Validity Trap

You may have heard me talk many times about the validity trap.

This is when we come up with something that on the surface appears to have merit and indeed, can look unarguable.

The challenge though sometimes, is that things that are valid are not always right.

There is a big difference.

For example, it’s valid to paydown debt until you are debt-free and then at that point begin saving and investing.

This has been the popular mantra over decades. It’s almost as though those that say it are espousing real wisdom known by few.

Whilst it is determined significantly by everybody’s individual circumstances, (and I realize generalizations are dangerous) as a general rule, the mix between reducing debt and investing has generated favourable outcomes for those emphasising investing over reducing debt for many years.

Certainly, for those who are more defensive and perhaps highly geared with debt, paying down debt is an obvious emphasis over investing.

For those who have significant scale with their asset base, strong reliable income streams and are perhaps holding moderately low or minimal levels of debt, paying that debt off completely is still valid, however when we look at the interest savings in a low interest rate environment and the compounding effect of money properly invested over time (I don’t mean 1 or 2 years but rather 10 or 20 years) the compounding effect of money invested in growth assets offers a real alternative.

Simplifying it down to the practicalities of the situation, payments on principal and interest loans (otherwise known as table mortgages) eventually see those mortgages paid off anyway.

By compounding what would have been the debt reductions into a growing asset, we can achieve a lump sum of money that otherwise may not have existed at all and the debt has been paid off in the fullness of time anyway.

I know there are all kinds of ifs, buts and variables that surround this particular issue. When we simplify it right down though, the compounding growth on funds invested work well. Practical, simple, effective – but not main stream.

The Investor’s Dilemma

The investor’s dilemma arises when either markets are very uncertain or the opposite, like at the moment when markets are happy and brave.

Again, I’m generalizing somewhat but what I’ve seen over many years is that some investors, when markets become uncertain, they, themselves also become uncertain and scared. They feel a very strong urge to scale back their growth investments and build levels of cash (or pay down debt, buy a new car, travel overseas, help children, go to the dentist, etc., etc …).

They are of course simply caught up in the strong grip of fear of loss.

On the other hand, there are those sometimes, who are somewhat more academic and perhaps, with a higher level of education who, when markets are uncertain, can sometimes rationalize why taking advantage of low prices is an advantage (this can vary from one person to the next).

Then there are others who when markets are happy and brave, take the view that this is the time to take profits and scale back the portfolio by building levels of cash, (paying down debt, help children, etc).

When the markets are unhappy and uncertain, or happy and brave, we can argue both sides of the coin because academically at least, they have merit.

For example, when things are uncertain, we can find all manner of so-called “evidence” to back up our line of thinking.

Also, when markets are happy and brave, particularly for us as value / eco-Investors, it’s not difficult to collect an array of information, evidence and data that supports our line of thinking that suggests markets are expensive, therefore it must be a good idea to take profits and scale back growth investments in favour of cash.

So what?

Firstly, in my experience, we are best to stick with our investing methodology (whatever that might be).

Modern Portfolio Theory is all about dampening down pricing volatility through diversification.

Momentum investing, driven mainly by sharebrokers, is generally about following the trend and the sector. Half the time this works pretty well, whilst half the time – not so much.

Value investing has been around long enough to now become more mainstream. One problem is the resulting confusion in terms of what it actually means.

For some, it is about buying assets cheap.

Charlie Munger taught Warren Buffett decades ago that this approach alone is too simplistic.

Eco-Investing at WISEplanning is about investing in the business (thank you Charlie Munger and Warren Buffett).

Further, it is about undertaking proper analysis of the financials but also looking at the economics of the business.

This helps us to both manage risk and support long term performance.

It’s not always easy but it’s not too complicated and certainly avoids the need for complexity.

With a low turnover mandate (where we minimise trading existing investment for new ones), we keep costs to a minimum. We can also drive improved performance by concentrating our portfolios overtime at a pace that suits the investor.

Anyway, my point here is that, when we look to scale back productive assets and increase levels of cash, we are rebalancing, which is a clever name for timing the markets.

Whilst this is a bit simplistic, when we ‘chop the head off a fast growing investment’ (take profits or scale back), we can also slow down future growth for that investment and damage the longer term compounding return of that investment and the overall portfolio.

Anyway, investing in good businesses is about investing in good businesses – not second-guessing where markets and trading prices may or may not go.

Still, you and I as investors are free to choose with our money. If we feel more comfortable with half or say 20% of our portfolio sitting in cash for flexibility, then that might be okay too.

The final word on this is that, good businesses tend to be resilient, so should their trading price decline then our one job is to buy more at a lower price (not worry about where markets may or may not head to in the future (that’s immeasurably more difficult).

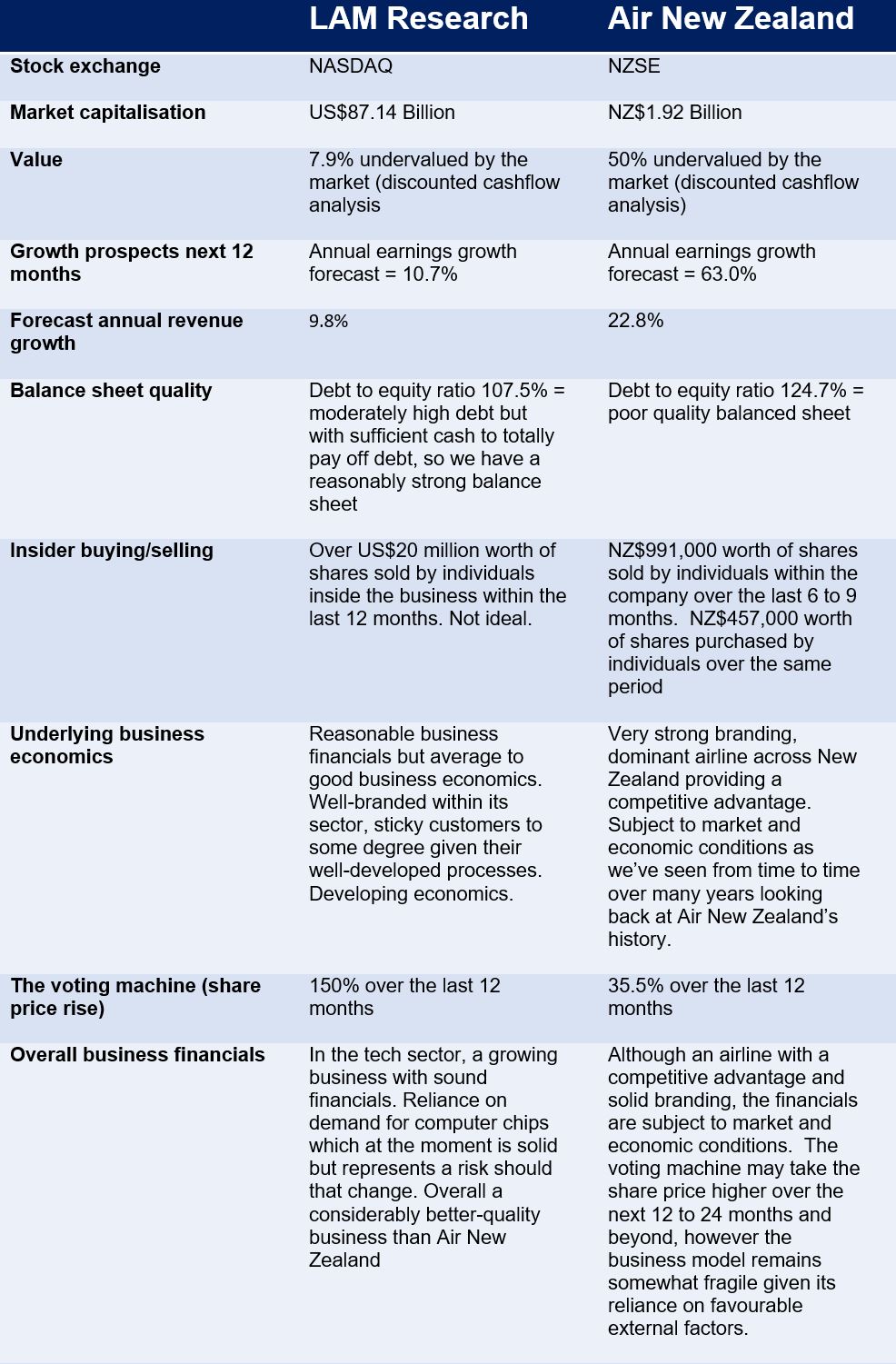

LAM Research and Air New Zealand

Just for fun, let’s take a look at two totally different business models. Neither are recommendations.

The above comparison between LAM Research and Air New Zealand may offer limited clarity around the importance of the underlying economics of each business as it overviews the financials and to a limited degree the underlying economics of each business for comparison purposes. Neither business should be considered a recommendation.

Computer chips and those operating in the semi-conductor sector have been popular and in demand over the last year or so.

LAM Research’s business model is about the design, manufacture and provision of the equipment that chip makers use to make their computer chips. Potentially this makes LAM Research’s customers unusually sticky which of course helps support ongoing profitability and growth. A powerful business economic.

The shortage of computer chips which is underway at the moment obviously makes chipmakers and those that supply the equipment that allows them to make those computer chips in demand and very valuable. Of course, should there be an oversupply of computer chips, then the reverse would be true as well.

Air New Zealand we know and love and as a frequent user or Air New Zealand until 12 months ago, like many other Kiwis, I have been a happy customer of Air New Zealand for decades.

Although they have quite strong economics with regard to brand strength and competitive position in New Zealand, once you look at global travel, their competitive advantage diminishes considerably.

Further, they are subject to market and economic conditions along with other external factors that they have little control over.

If I had the choice between these two businesses, even though we know that the trading price of Air New Zealand is likely trending up over the short to medium term, I would likely favour LAM Research. What do you think?

Valid and / or right?

It’s not difficult to formulate some sort of rationale for almost anything, across both sides of the argument.

Interestingly the rationale of each side of the argument is likely valid.

That doesn’t necessarily mean though that they are right.

As I mentioned earlier, the well-known mantra of paying off all debt before investing it is valid but is not right for everyone.

In the investing world, it can be critical to distinguish between what is valid and what is right.

It’s easy to validate one’s point of view around a particular investment decision. Unfortunately, it is not as easy to be right in the long run.

That’s why an investing methodology, whether it be for property, our own closely held business or direct shares, that is based around the economics of the asset helps to manage risk, support long-term performance and helps us to be right more often than we are valid.

“One of the funny things about the stock market is that every time one person buys, another person sells … they both think that they are astute.”

William Feather