The Markets and Where to From Here? (Covid-19 Update #9)

Market and Economic Update – 26th March 2020

Peter Flannery CFP AFA

“If you have one economist on your team,

it’s likely that you have one more than you’ll need.”

Warren Buffett

THE MARKETS

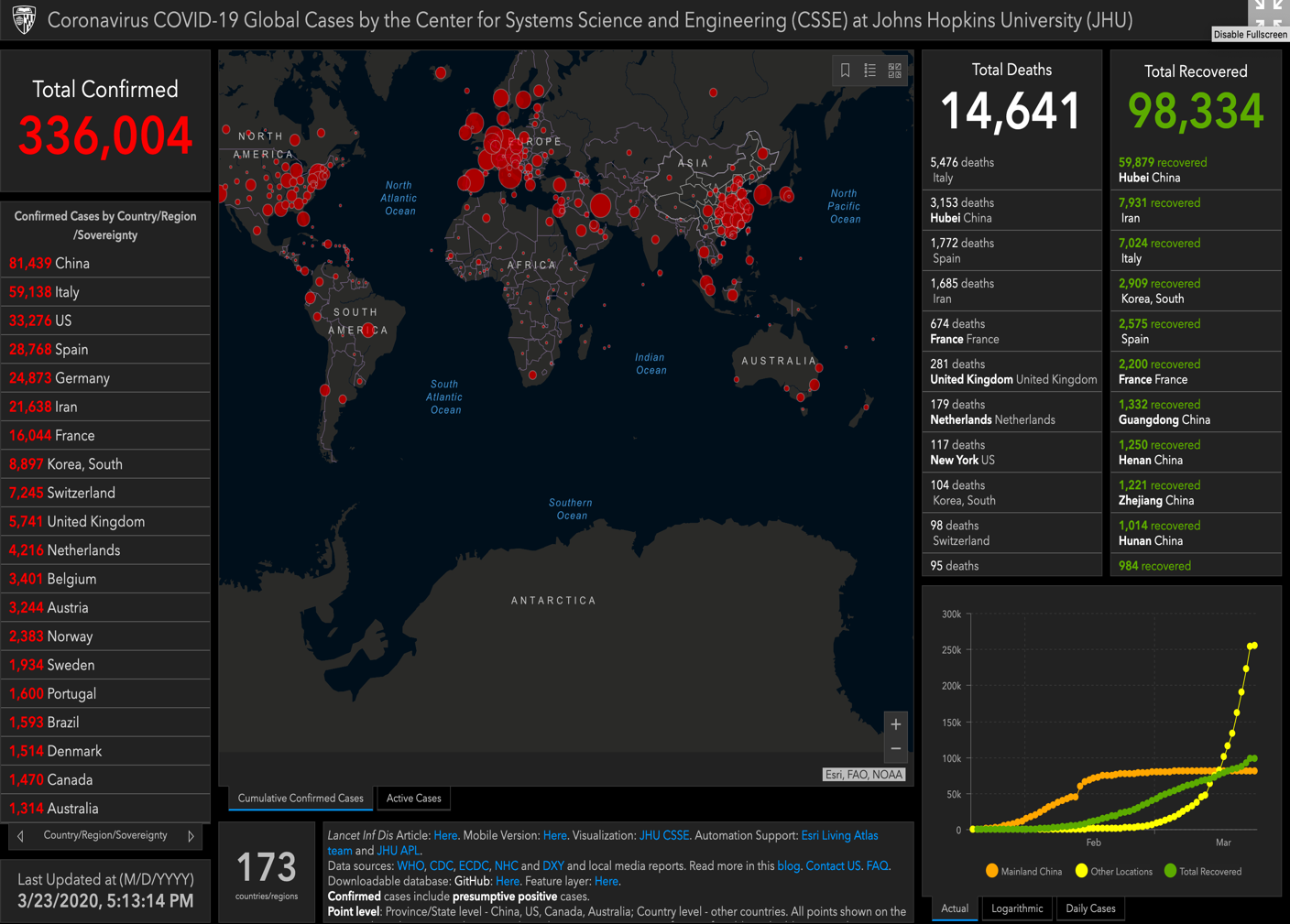

COVID-19!

The above chart provides a graphic overview of the rapidly increasing spread of the Coronavirus.

The chart on the left shows the upward movement in the American share market (the Dow Jones Industrial Average) over the last five days, and the chart on the right shows the downward movement of the Dow Jones over the last 12 months.

So, what is going on?! Well, pretty much the usual actually. If something changes or goes wrong, markets react. Of course, the human toll is very sad and almost does not bear thinking about.

Expensive asset prices

To cut right to it, asset prices have been expensive for quite some time. We would need to go back to the global financial crisis in 2008, when asset prices, whilst not very cheap, were not overly expensive. Since then, there has been a real challenge locating well priced opportunity. Investments have been expensive.

Debt levels

With asset prices high, we have had increased borrowing levels, with corporate debt in America reaching all-time highs, although I am not as concerned about this as some other commentators. That is because WISEplanning are not investing across the market but rather in specific businesses.

Debt quality(?)

Another concern worth mentioning perhaps is the high concentration now of poor quality debt. The amount of US corporate debt sits at a total of US$10 trillion, with $2.5 trillion in the financial sector and the remaining $7.5 trillion in the non-financial sector. By one measure, this adds up to around 47% of GDP, which is not a dangerous, eye-watering level, but significant nonetheless.

Where this conversation gets to is that those corporates in the US and elsewhere that have high debt levels could see their cashflow being squeezed as bond holders demand a higher interest rate for the risk that they, as (bond) investors, take. We have not seen this type of risk for many years. An event like the Coronavirus outbreak can be a potential trigger for interest rates to rise, particularly when we think about low quality debt (BBB rated debt).

Aside from that, we have a rather acute situation with supply chains suddenly disrupted and just as suddenly cashflows being seriously choked.

To the rescue …

That is why central banks around the world, including here in New Zealand, are looking at fiscal stimulus, otherwise known as quantitative easing (printing money so to speak). Interest rates are low and can go lower still but not by much. The next step then is quantitative easing.

We have even seen the US Federal Reserve signal to the New Zealand Government, that it will provide funding to help keep the economy ticking over here in New Zealand.

So, one of the problems, is the issuance of poor quality debt, which has been strongly sought after as interest rates have continued to decline over the last several years. Poor quality debt can sometimes default and that, if it is of significant scale across the market, can create a credit crunch.

The acute nature of the disruption to supply chains has choked business profits to the extent that some organisations are in danger of collapse without support.

The reality is that central bankers around the world do not have the luxury to sit around overthinking the situation as the Coronavirus, and the impact in its wake, continues to grow like a tidal wave, at pace. They have no choice. They are responding and they will continue to respond.

You may have noticed in the media that the US Federal Reserve is a key player amongst all central banks because the US Dollar remains the favoured currency around the globe.

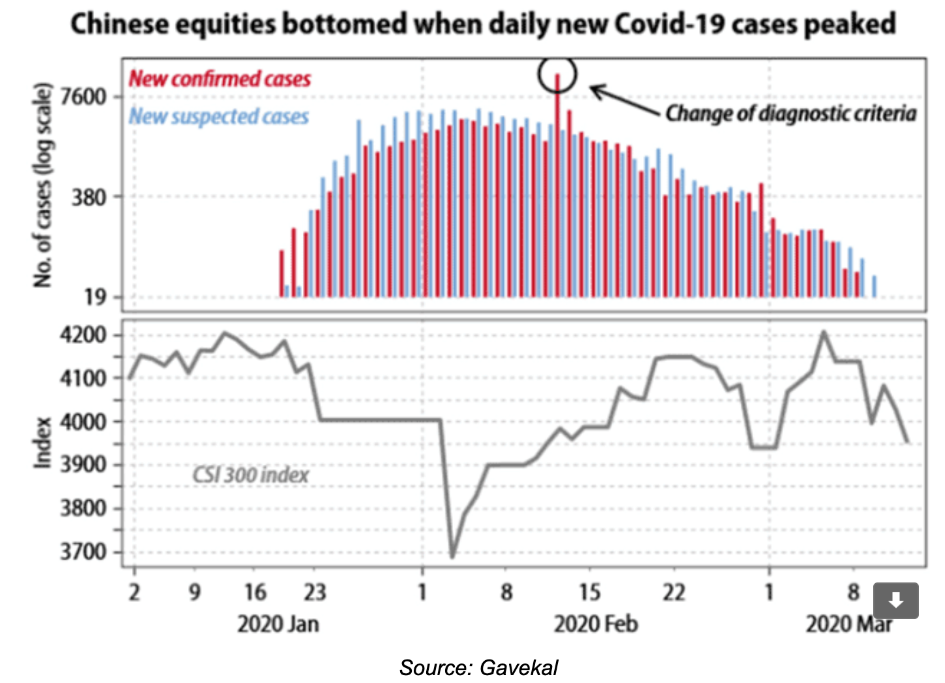

The Chinese share market bottomed out pretty much as soon as news emerged that the Coronavirus infection rate had peaked.

This highlights the point about markets being difficult to predict. The second point worth noting is that, just as markets declined sharply on the downside, they spring upwards just as quick sometimes.

That is why those with a more measured approach sometimes get left behind as they await all the graphs to turn green, markets to rise consistently day in, month out, and the bad news, whatever it was, to pretty much disappear before they put their toe back in the water with ongoing investment.

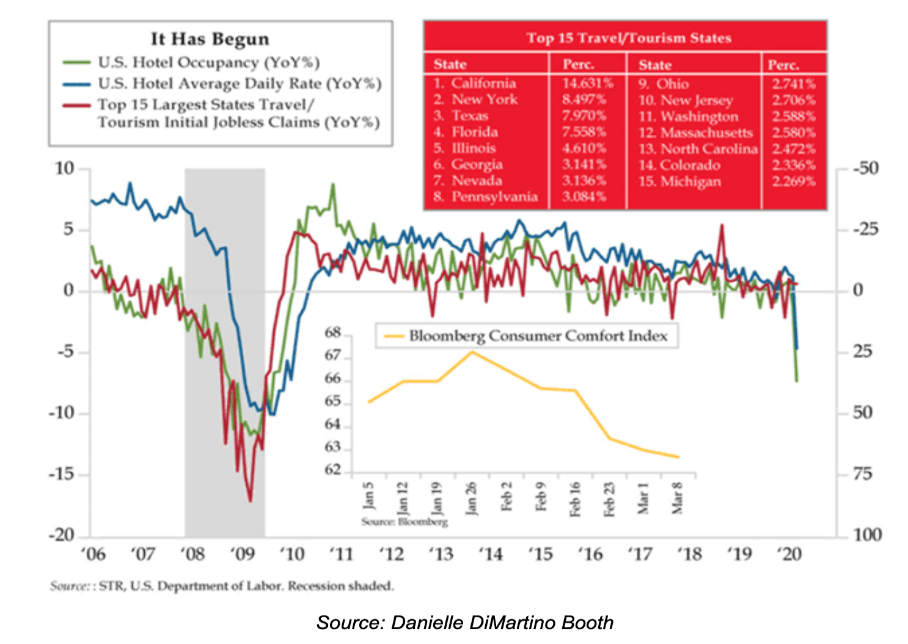

The Economy

The above graph, among other things, shows some potential indicators of recession in America.

So, we have the supply side issues where supply chains are, in some cases, seriously disrupted. For example, supplies of hand cleaner disinfectant have run low and have become like so-called ‘hens teeth’.

Then, there is the demand side of things, where people are not getting out and about and most importantly, for economies that are based on consumption, people are not spending money. That actually is quite a serious problem for most western developed economies, including New Zealand.

The financial shock is well underway, as markets react strongly to what appears to be fear of the unknown. Indeed, markets have undoubtedly become irrational. This appears to be down to those ‘unknown unknowns.’ If the market is unsure, it does not understand the depth of a problem or how long it might go on for, the response is simply to bail out. Luckily for us, of course, that means lower prices and buying opportunity.

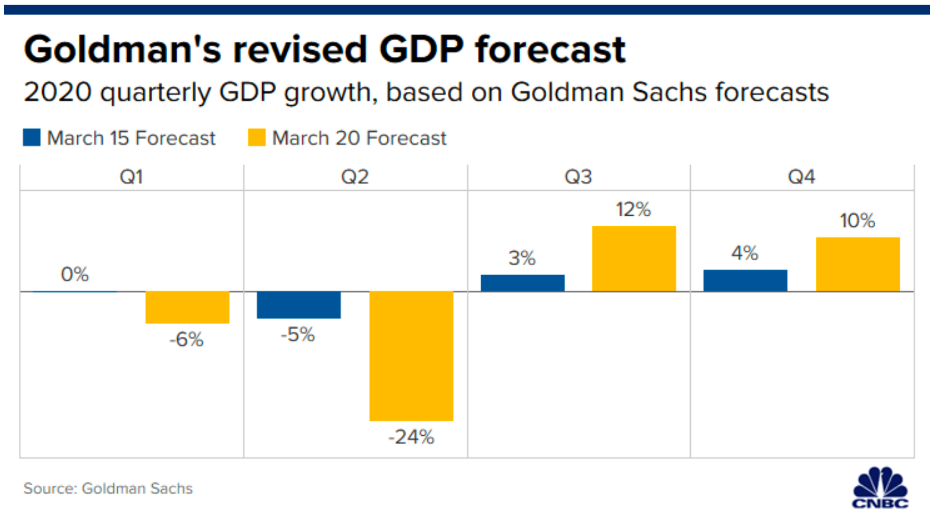

The United States of America

The above graph shows the impact of Coronavirus on economic growth in America to the end of 2020.

Economic growth in America looks likely to contract (not grow) over the first two quarters of 2020. To me, this projection seems feasible and a possible/likely outcome.

Of course, what is less predictable is how the markets will react. What we have seen so far though is swift action by the US Federal Reserve, alongside other central banks around the world. Although many a commentator is quick to point out that reducing interest rates down to zero will not solve any problems and anyway, they are ‘running out of bullets’ so to speak, with this approach.

The reality is that, as valid as this comment may be, low interest rates do help support any struggling economy. It keeps an economy moving, whereas at higher levels, economies struggle. So, whilst it is not a panacea or silver bullet, as it were, it helps.

Central bankers have a number of tools in their tool bag. Without going into the depth of each one, quantitative easing has been a well used tool over the last 10 years and longer. Basically, central banks undertake an asset purchase programme, which effectively allows money to be injected into the economy, to keep things ticking over. Of course, it is not ideal and we would all rather we did not have to resort to these measures, but this is where we are.

If there is a risk here, to me, it is the fact that ‘America Inc’ has been slow to respond to covid-19. This will allow the spread of the Coronavirus to be greater than may have otherwise been the case. America is swiftly moving to lockdown right across the country. That, of course, is huge for America and also big for the rest of the world too.

Possibly not helping things, in terms of international trade, is the fact that Europe is also behind the Coronavirus curve.

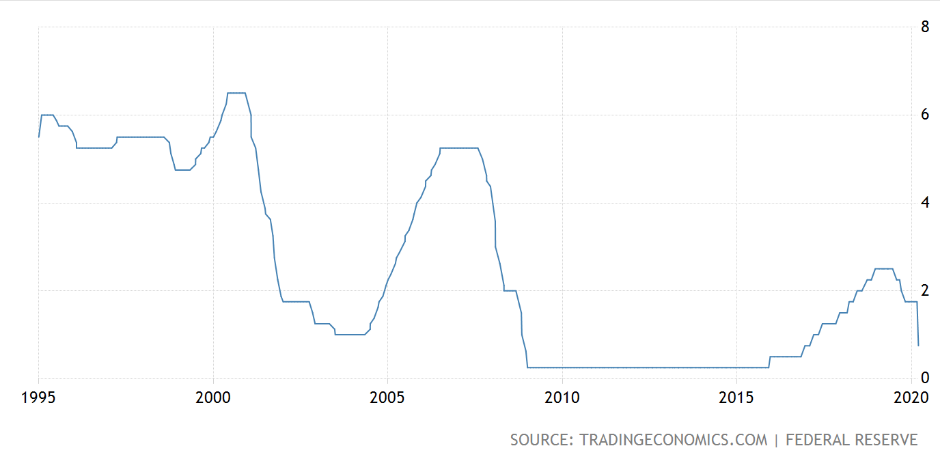

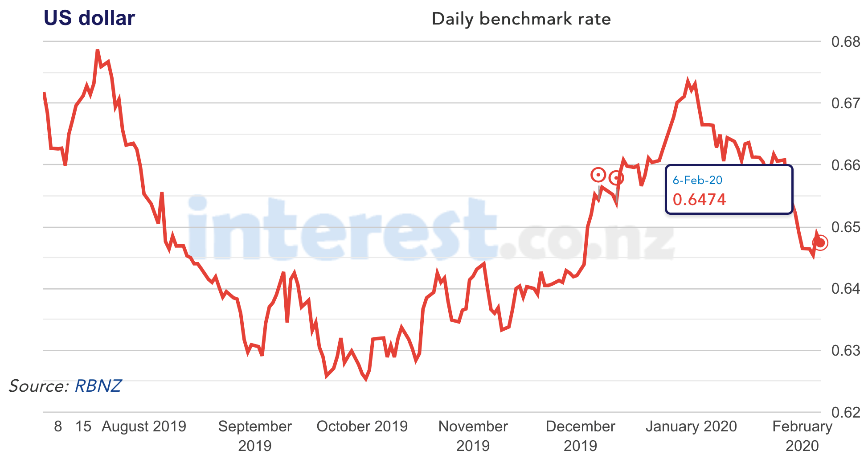

Interest Rates – United States of America

The graph above shows the movement in interest rates in the US since around 1995.

The short of it is the US Federal Reserve has taken strong moves by lowering interest rates (monetary policy), as well as undertaking a new round of quantitative easing (fiscal policy), which is euphemistically known as printing money.

The bottom line is that the US Federal Reserve will do what it takes (the reality is they have no choice) to support the US economy and the global economy through the Coronavirus pandemic. This has included, by the way, a line of credit to the New Zealand Government to help them support New Zealand’s economy.

Although I have not shown it here (sorry, I have kept this reasonably brief because we are investors rather than economists – busy investing!), other central banks around the world are taking similar measures to support the respective economies.

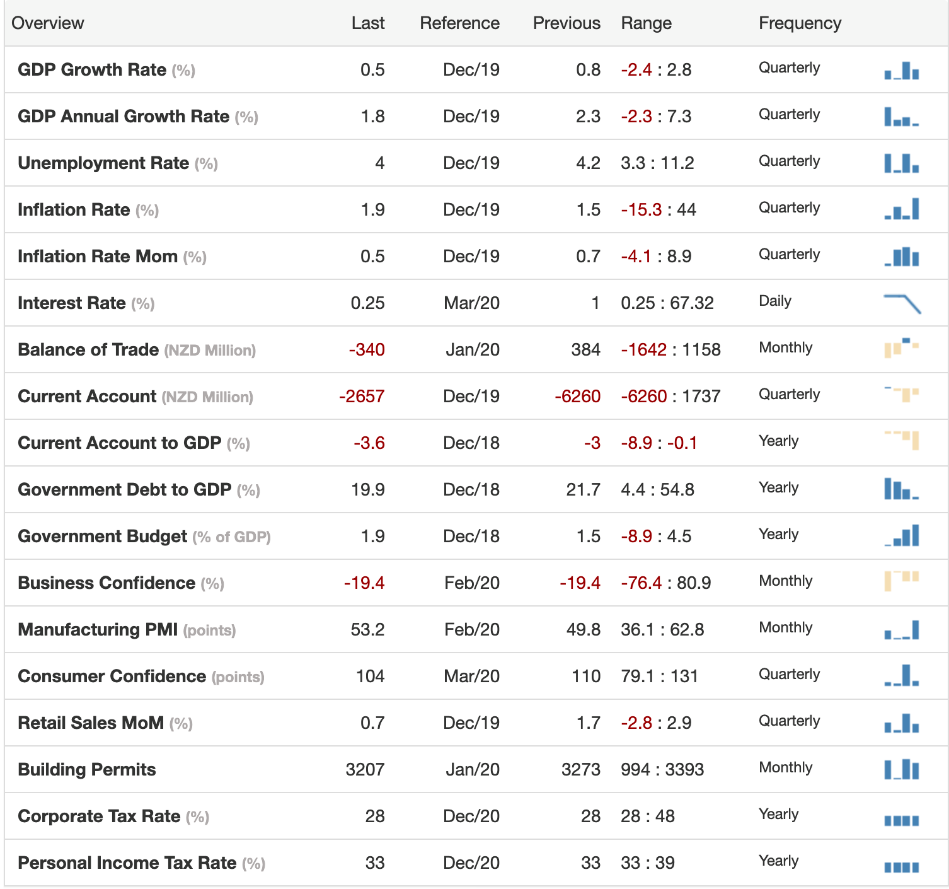

New Zealand

The above shows a variety of economic indicators across the New Zealand economy.

As I mentioned earlier, the New Zealand Government is adopting strong measures right across the New Zealand economy to support mums and dads and businesses through the Coronavirus ordeal.

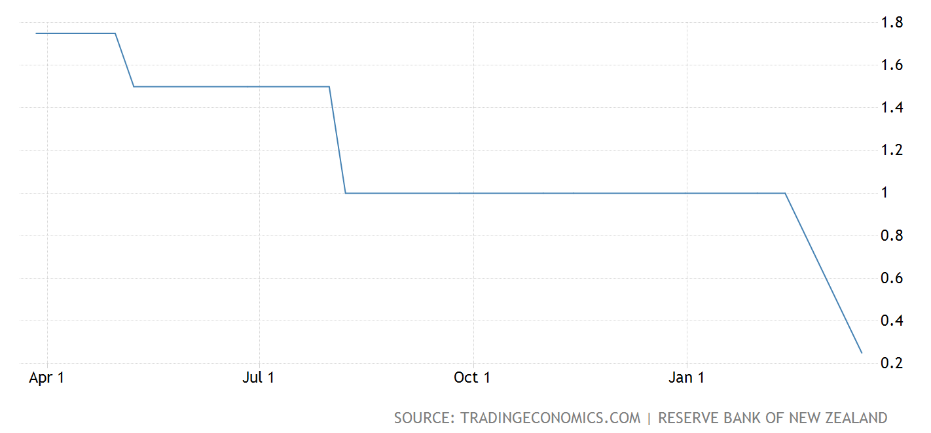

Interest Rates – New Zealand

The above chart shows interest rate movement over the last 12 months.

As you can see, the above graph showing interest rate movement has been in one direction – down. This is a combination of a couple of notable factors. The first one being the ongoing global deflationary funk, which appears to be ongoing and secondly, of course, there is COVID-19. Indeed, that decline in interest rates was huge from around 1% to 0.25%.

I know that some clever people across the internet reckon that central bankers are ‘running out bullets’ because interest rates are near zero. What they overlook is the fact that low interest rates do actually help support economies but more importantly, that fiscal stimulus, which involves quantitative easing and the like, means that central banks have an array of tools that they can use ( in addition to interest rates).

For example, the New Zealand Reserve Bank, as you know, was about to impose an increased level of capital surety (banks needing to hold more money aside for a ‘rainy day’) but has delayed the implementation of that and indeed is looking like reducing that requirement in the short term. This will allow banks to lend to businesses and mums and dads, whereas they otherwise may not have. This truly is banks and those that need the money, working together! It is, of course, a hand up rather than a handout (although there may be some who feel that they are missing out).

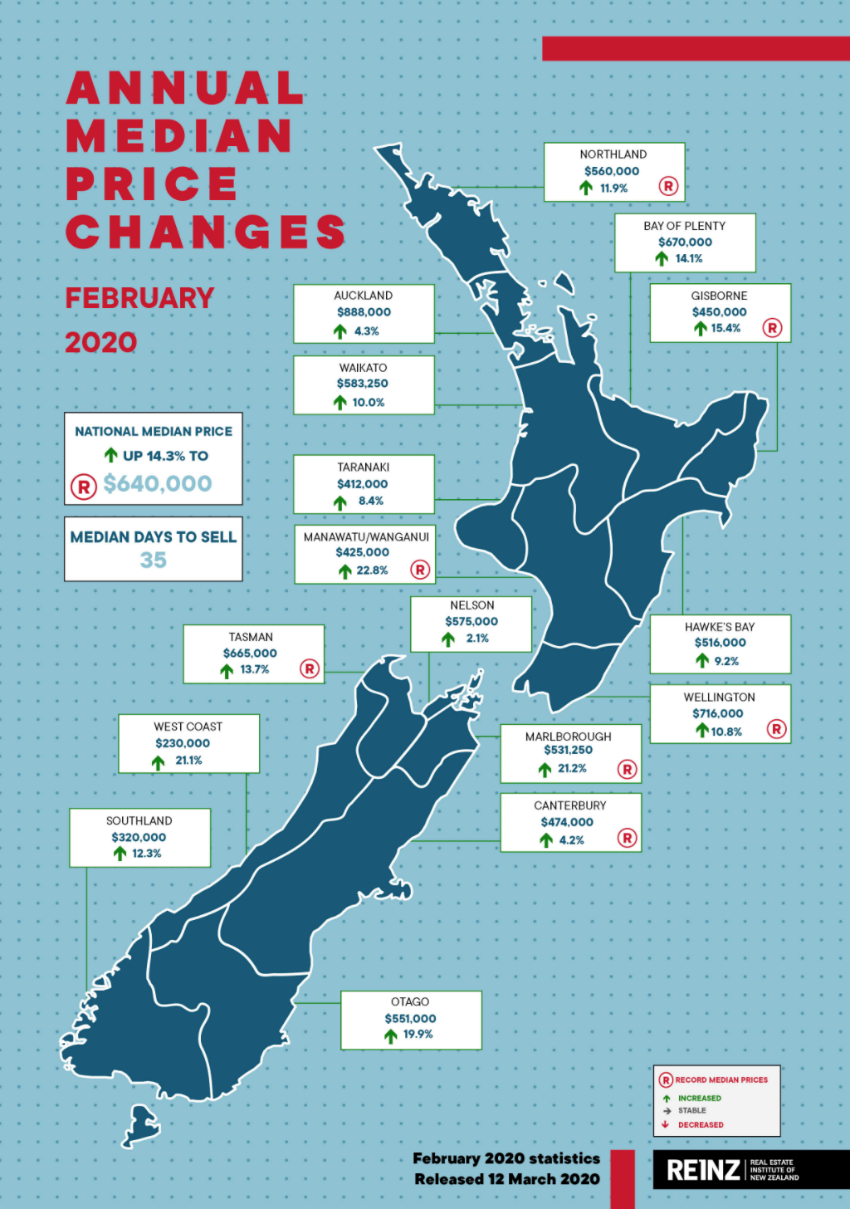

The above diagram shows property price movement across New Zealand.

We all know that the share markets around the world have been highly volatile over the last two or three weeks – fantastic ( lower prices = better buying)!

What is less obvious is the impact of the pandemic on property prices. That is because (except for listed property trusts) residential rental properties are not listed on a market, so pricing is private and not as transparent as easily traded parcels of shares on a stock exchange.

It is difficult to gauge; however, some AirBNB property owners might be feeling uncomfortable with the sudden decline in international visitors. Will some opt to sell? Will some need to sell? On the other hand, interest rates will provide ongoing support to residential property prices across New Zealand.

Let’s not forget that share prices around the world traded expensively for almost a decade. Residential property prices have been trading expensively for likely three decades.

I am not suggesting that the Coronavirus will be the undoing of residential property prices, although one would expect there might be some impact on property prices. It is always difficult to know what the trigger will be for any expensive asset; however, the point here is that whilst residential property is a relatively secure asset, when all is said and done, as normal as expensive prices for property may seem, those prices are at odds with the fundamentals.

Of course, who cares about that?!

As I have often mentioned, residential property in New Zealand is no longer an investment but rather a religion (blind faith).

To Summarise …

Okay, while I am standing on my soap box, I would just like to say that I take issue with the comment around ‘We don’t know how long this pandemic will go for,’ which suggests we should all be scared out of our wits and worry ourselves half to death.

Frankly, unless COVID-19 mutates, which so far has not been the case, then logic suggests that to a greater or lesser extent, we will follow China’s footsteps.

I am not in the medical profession and cannot comment about the virus. As an investor, I certainly think about the impact of this virus on my investments and yours.

There are risks and there is capital dislocation. In many ways, it is not business as usual. Significant disruption is at play.

The central bankers are all stepping up and I believe communities will do the same (I am thinking about Christchurch earthquakes and how people truly stepped up and showed their best then) and how the next four weeks will likely put us further down the track and in a stronger position to deal with COVID-19.

We do not know how long it will go for but we do not need to know. What we need to know is that the appropriate steps and measures are being implemented, which is what we do know and that is all I have got to say about that.

As I mentioned earlier, this report is somewhat briefer than normal perhaps, just because at WISEplanning, we have been very busy helping our clients to invest, taking advantage of the best pricing opportunities that we have seen for about 10 years.

Ironic, isn’t it, how there have been reports that some people in China are seeing the stars for the first time in their lives, how some rivers are seeing pollution levels disappear, with fish starting to repopulate some of those rivers?! It is interesting how we, as humans, are being forced to live ‘in a bubble’ together as one.

I remain very confident that with the support measures in place here in NZ and elsewhere that, the opportunities are there for those who can see them. Steady as we go …