Coronavirus And The Next Ten Years… (Covid-19 Update #2)

Market and Economic Update – Week Ending 7th February 2020

Peter Flannery CFP AFA

“If you have one economist on your team,

it’s likely that you have one more than you’ll need.”

Warren Buffett

THE MARKETS

WHAT DOES THE NEXT DECADE BRING?

It would be very surprising if, despite unexpected troubles along the way, that the world is not a better place at the beginning of February 2030. Troubles come and go. Progress continues …

The Iran issue that was hot news a matter of weeks ago has now been overtaken by the Coronavirus (which is not to say that the Iran issue has been resolved). It may take time to pass, but in 10 years’ time it will likely be, but a moment in history. Technology advances will undoubtedly continue, probably at such a pace that we might struggle to guess where that will take us.

Although not everyone shares in the wealth that is being created, which brings its own problems as we are seeing around the world now, for many of us though, our lives will be improved in ten years time.

Think back 10 years ago and some of the things that we now take for granted such as Google searching along with many other technologies that are available today and considered mainstream (normal). They were only just getting going 10 years ago or didn’t even exist at all. Self-driving cars, LED light bulbs, gene editing technology (crispr), Spacex’s reusable rocket, the iPad are some other examples. There will be many, many more over the next ten years.

The future looks good. The next 10 years I believe will continue to advance ‘the new normal’ based new systems and processes and of course fast changing technology. With elevated trading prices, markets are bound to be volatile and yet profitable over the next 10 years, especially when you invest in quality assets that grow.

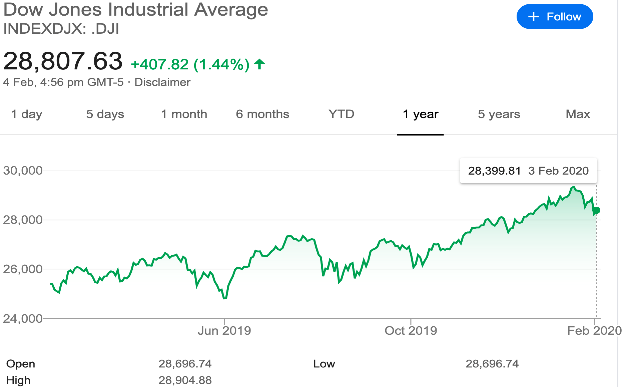

The red chart on the left shows the slight decline in the US share market over the last month. The green chart on the right shows the gain in the US share market over the last 12 months.

Share markets and other assets have boomed over the last 12 months. Will the coronavirus stop it dead in its tracks though? So far, the market has been undecided about just how serious it thinks the coronavirus will be. It would seem that the fallout and the impact will not be immediate but further out into the future. Possibly three to six months out. Then I suspect we may start to see the impact of some of the measures that have been taken to contain the coronavirus over the last month or so.

The coronavirus will likely spread rapidly before it reaches a peak and is ultimately contained. Interestingly, the Chinese government mapped the genome of the virus, sent it out for further analysis and within days a laboratory in America had generated a potential antidote, which normally would have taken months. That’s how advanced technology has become when comparing it to, for example, the SARS virus in 2003. Unfortunately, it may take somewhere between six and eighteen months for proper testing to take place. In the meantime, containment measures appear to be the main weapon against the spread of the coronavirus.

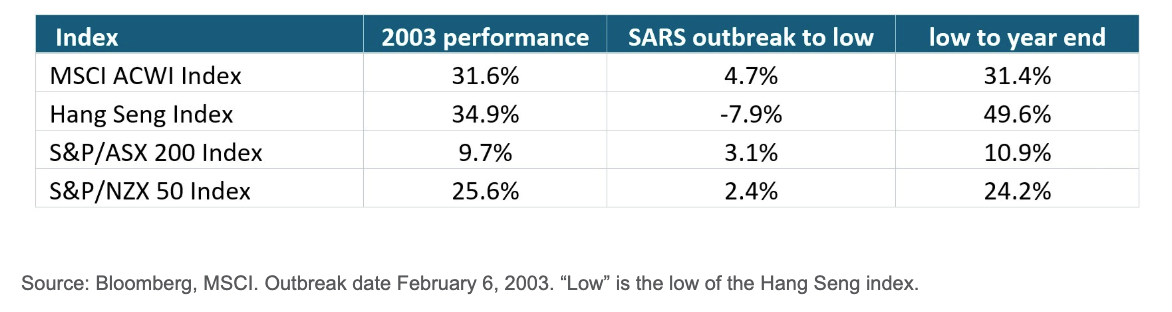

Market Movements During the SAR’s virus 2003

The above chart shows market movements at the time of the SARS virus back in 2003

Although I would not place too much weight on the above chart and how it may correlate with the coronavirus, it does provide some idea though around how markets respond to this type of event. Basically, some volatility but nothing significant. Frankly, I am hoping for more with the coronavirus, so that we can have at least some opportunity for some better buying, be it with existing businesses already in your portfolio or other businesses outside your portfolio that could be included if we can secure the right pricing.

The Warren Buffet Market Indicator

The above chart shows markets remain expensive based on the Buffet Indicator.

So, markets remain expensive. The little bit of volatility right now because of the coronavirus (as I said before, the Iran scenario was short lived and almost forgotten about!) has not been much, although it is probably not over yet.

Remember, the share market is a leading indicator. It tends to be forward looking. Looking, that is, for the danger and the opportunity out into the future. When it sees it either way it reacts, at times, strongly.

Expensive prices however are not in themselves a problem. Markets and investments can remain expensive for longer than we may think. Take, for example, residential property prices in New Zealand that have been expensive for decades. Just because they were expensive seven or eight years ago does not mean that they still cannot be expensive today.

The same holds true for share markets around the world. When the environment is supportive, the market generally takes this as a signal of good times and behaves accordingly, pushing prices up. It is only when there is an unexpected event to the negative that the market changes its mind, and sometimes in a hurry. That, by the way, should not worry you and I providing we have invested in quality assets.

So, What Are the Dangers?

Looking ahead right now, whilst it is always difficult to predict what may actually unfold, one risk that would definitely upset the markets would be US companies missing their profit targets. Profit misses are hated by the market because the market thinks this means less opportunity in the future.

Perhaps another risk is unexpected inflation. Whilst central bankers around the world are doing their best to generate inflation, too much inflation would be a signal for central bankers and others to raise interest rates, which would have an immediate negative impact on share markets around the world.

That is when the value may start to appear. Bear in mind of course, that market prices are elevated, so they will need to fall by around 20-30% before that value will start to emerge across the market. Of course, for us there will be isolated opportunity as Value / e-Biz Investors that will present itself anyway in that situation. That is because we are not playing the markets, nor are we investing across markets but rather inside the market, in businesses rather than stocks.

THE GLOBAL ECONOMY

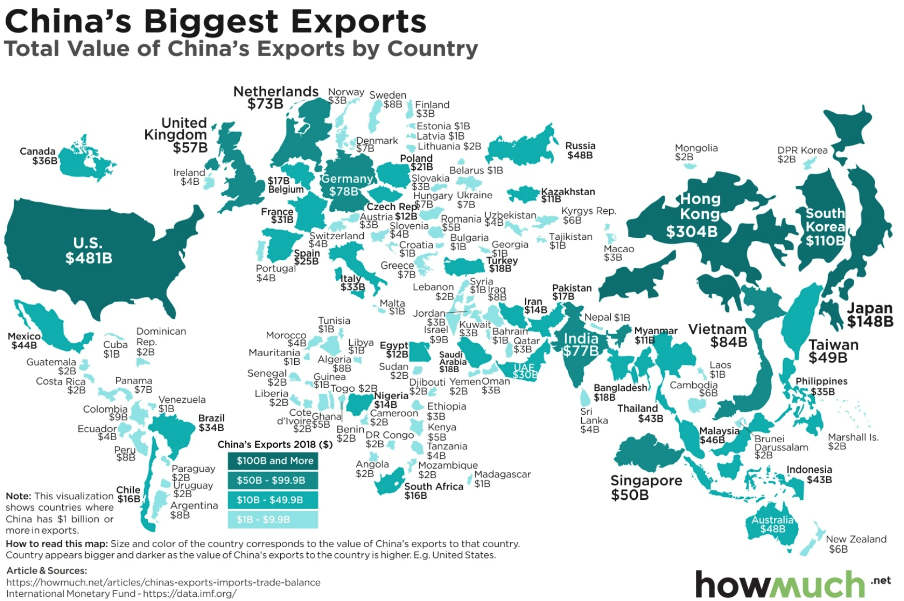

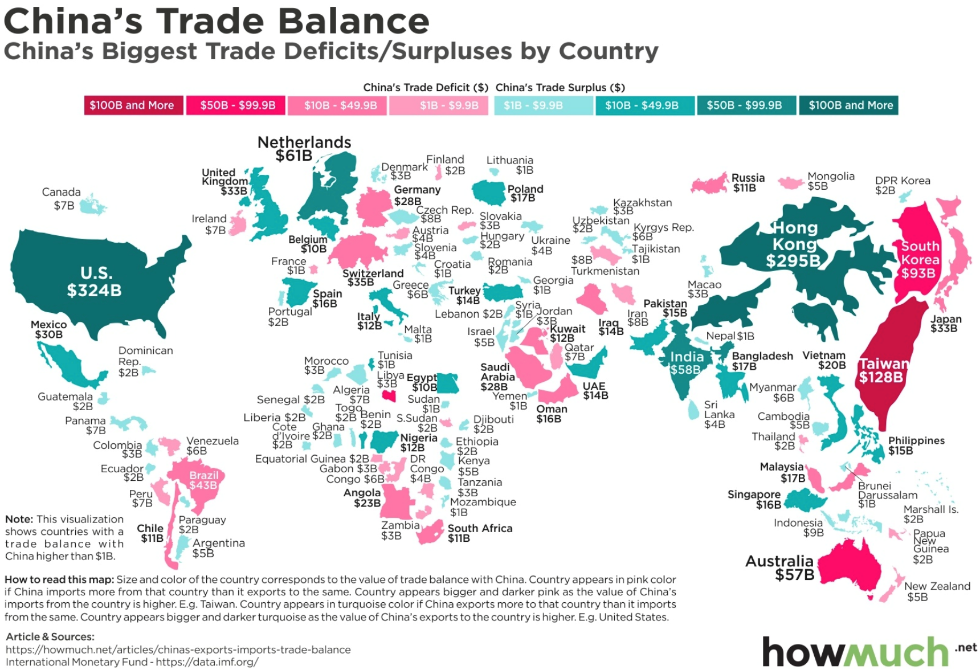

The above chart shows how much China exports to countries around the world. Bear in mind the size of countries in this diagram reflect the amount of imports from China (not the physical size of the actual country).

China’s economy continues to grow at a fast pace. Last year it grew at a little over 6%, which is a lot when compared to most other countries around the world. The question on everyone’s minds is about what impact the coronavirus might have on the Chinese economy over the next 12 months. By some estimates, whilst I believe the Chinese government will attempt to keep its economic growth (as measured by GDP) as close as possible to the 6% mark, it could be as low as 4%. Difficult to predict and time will tell. Anyway, that is still a significant rate of growth, particularly for an economy like China.

Let us not forget though that urbanisation in China is still underway with somewhere around 50% of the population living in cities and arguably another 30% or so to go. That ongoing process will help boost the growing Chinese middle class and the consumption based economy (as distinct from the export led economy). The Americans would be happy for this to happen because it means less tension around trade as the Chinese economy progresses its internal consumption based economic growth.

The above chart shows the trade balance between China and its trading partners.

China, as we all know, is now an integral component of the global economy. That is why the market is undecided about the coronavirus because, if this virus becomes much worse than expected then it will impact severely on the Chinese economy. Because of its size (and the trade with other countries), the impact would flow on across the rest of the global economy, severely hurting global economic growth. Whilst that is a possibility, to me, a severe hit to the global economy seems unlikely at this stage.

The market (as distinct from the economy) is more inclined to adopt an irrational approach, based perhaps on defensive behaviour and minimising losses rather than much in the way intelligent reasoning – just saying! So, China does matter to the global economy but also China matters to China as well. That is why, in my view, the Chinese government will be, as usual, strongly focused on maintaining economic growth. There were some hints in the New Zealand media recently that China may potentially punish New Zealand for closing its doors to Chinese travellers, however I expect that to be ‘sabre rattling’ rather than a threat to be delivered upon.

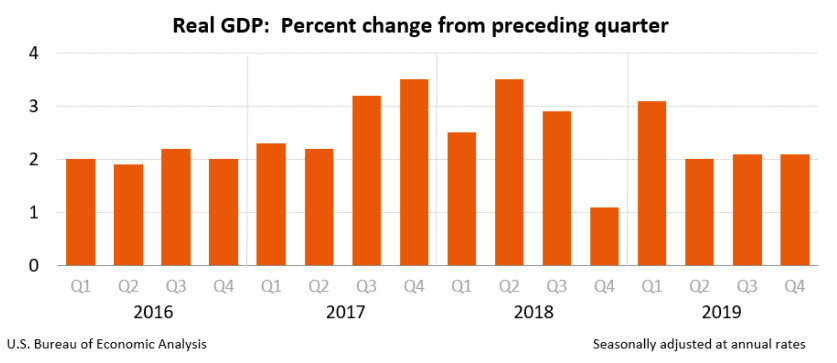

Economic growth – USA

The above chart shows economic growth in the American economy.

Economic growth in America remains stable, although at a modest pace. It is worth mentioning that the above chart shows real (after inflation) gross domestic product (GDP). The increase in annual economic growth was at the rate of 2.1% in real terms in the fourth quarter of 2019. It should be noted that this is an advance estimate as the data is still being collated and it could change.

It is interesting to note also that American economic activity was $US21.73 trillion over 2019 – unmatched by any other economy on earth. By comparison for example, China’s GDP was $US14.3 trillion over 2019. America remains a significant economic power even though China may well be continuing to grow faster than America.

As I have mentioned in the past many times, America has that unique package that no other country possesses. Warren Buffet has been known to suggest that ‘It is a brave man that bets against America Inc’. Yes, they have lots of debt although not as much as some other countries such as Japan, and also, they have a trade deficit with China. That of course is something that Donald Trump is working on right now. In short, America has options because of its size and scale and also that unique package that exists in America only.

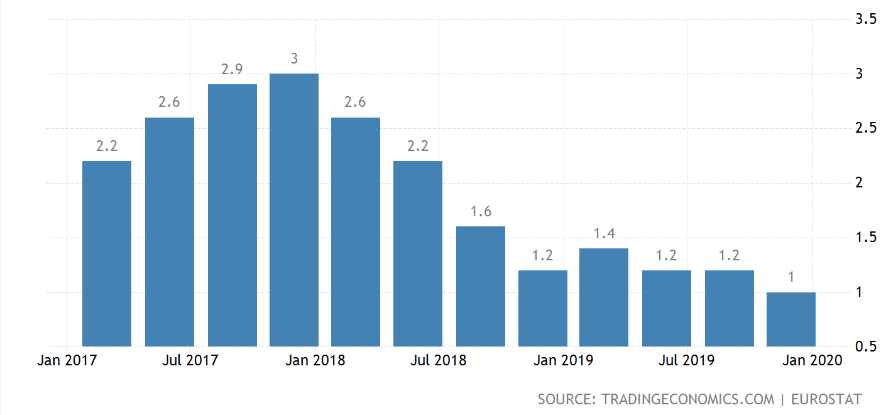

Economic Growth Euro Area

The above chart shows economic growth across the Euro area.

As the chart above shows, economic growth across the Euro area remains stubbornly low. No change here. Interesting when you think that debt levels have increased, interest rates are at all time lows and oil prices are also low. More central bank support will be required.

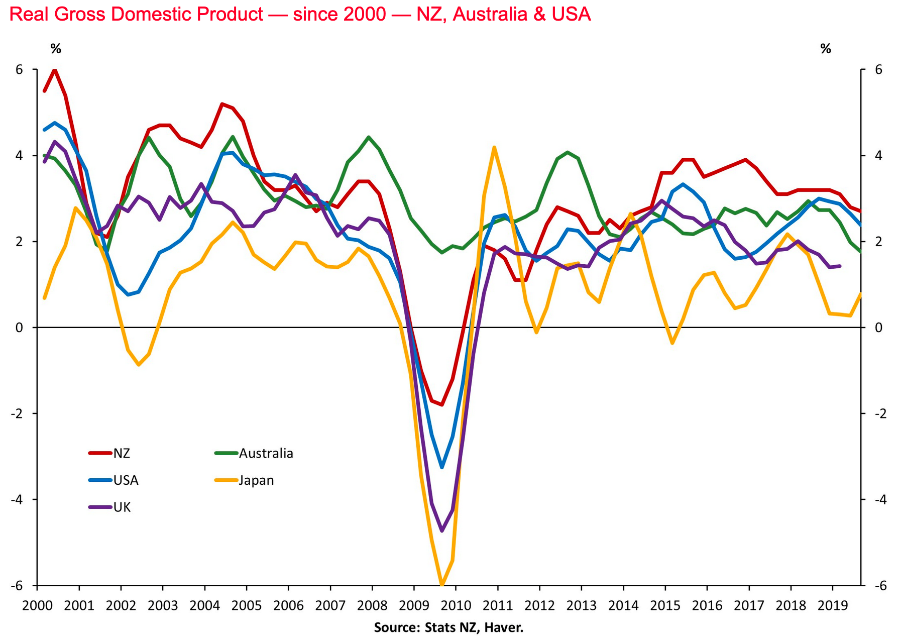

Economic Growth – New Zealand

The above chart shows economic growth in New Zealand, compared to other countries, since the year 2000.

Despite New Zealand’s narrow and high-risk economy, we continue to ‘punch above our weight’ so to speak with regards to economic growth. We are vulnerable to global shocks however we continue to grow at a decent pace, particularly when compared to most other developed countries around the world

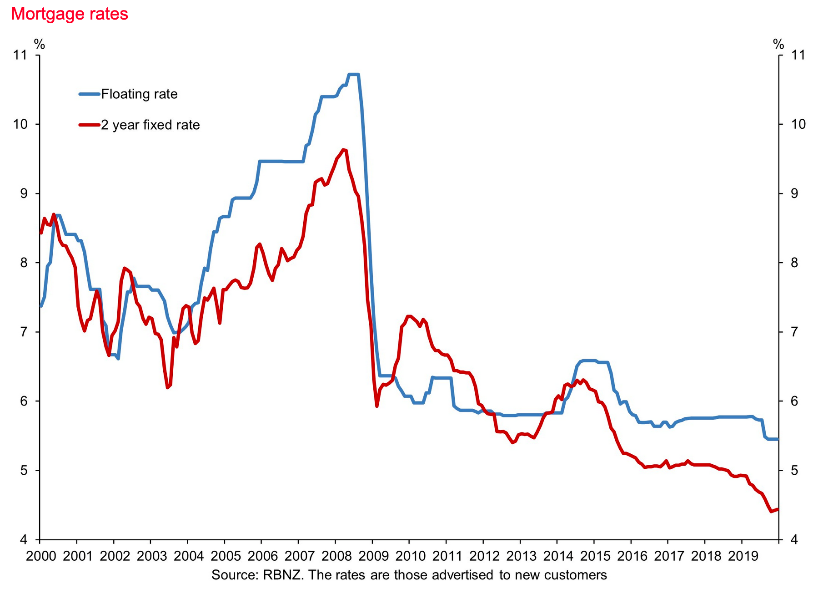

The above chart shows floating and two-year mortgage rates since 2000.

As the chart above shows, mortgage interest rates have generally tracked downwards for at least 20 years. As I have mentioned in the past, this is symptomatic of what I term ‘global deflationary funk’. The liquidity bubble has expanded and as result, central banks have responded with the use of tools within their tool kit, one of which is reducing interest rates.

The idea is to stabilise the economy, support growth, reduce unemployment and then engineer employment growth. So far employment growth has been stubbornly absent around the world. Economies however are stable and global growth continues at a modest 2.5%. Interestingly, the ANZ bank lifted some of its mortgage rates recently although it was only by around 10 basis points, but it is a reversal of ever declining interest rates over the last several years. There is an argument that ongoing strong housing data, along with the governments newly announced infrastructure plan, may provide support to the New Zealand economy and this may in turn lead to the abandonment of a negative outlook for the Reserve Bank of New Zealand and a more stable outlook in the future. The change in interest rate direction by the ANZ, the first of the banks to move, is an interesting one and whilst you never know, I do not see it leading to significant increases in interest rates anytime soon.

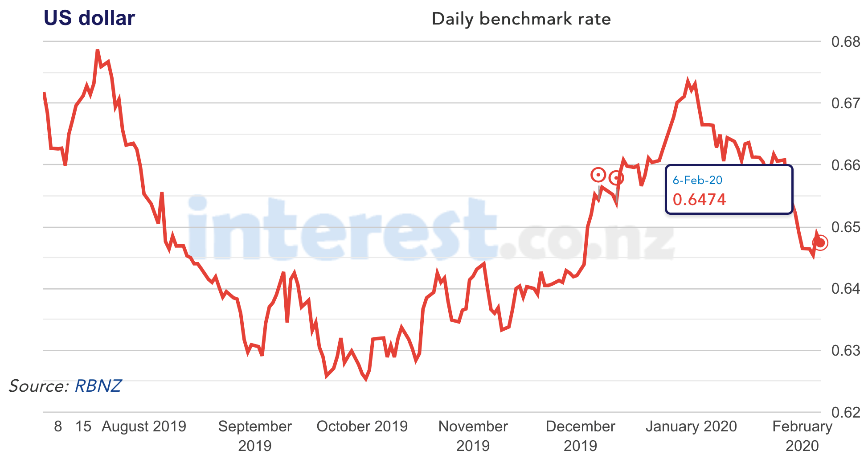

The chart above tracks the New Zealand dollar / US dollar cross rate over the last few months.

To Summarise …

The coronavirus has captured significant media attention, which in some ways is understandable given the potentially serious nature of the virus. I must say, when it gets down to watching a plane landing on the television, I have to check myself against what other uses I might allocate my time to!

The impact of the virus is yet to be felt – look out for that over the next six to twelve months. I do not see it becoming a serious global economic threat. In terms of the impact on markets and prices, at this stage the market appears undecided. I am hopeful for some real volatility to come out of it – at least that is something positive.

Interestingly, on the New Zealand front, residential property price rises have re-emerged again, no doubt supported by continuing low interest rates and a slowing but nonetheless growing population.

There are elections in New Zealand and in America this year which should prove interesting, although I do not see either as somehow a major market catastrophe that we need to watch out for. At best, we can hope for some volatility with regard to the American elections.

Let us face it, like him or hate him, Donald Trump has been positive for the American economy. Some of his opponents would initiate an outright attack on the status quo, including direct targeting of the likes of Alphabet, Apple and other successful corporates that continue to offer their staff, consumers and businesses more options and a better life.

Is Donald Trump just the least worst option?