Is Your Money Safe?

Investment Perspective – September 2019

Peter Flannery CFP AFA

“Neither the investing method nor the fundamentals of the business are right or wrong because the mood of the market is favourable or unfavourable toward the “stock”. That is because when you really think about it, “stocks” (shares) are all about the financials and the trading price, the share price… the cash up value. What matters more is the economics of the business”

Peter Flannery

Will ‘value’ matter with $250 trillion of world debt leveraging the markets?

$253 trillion of debt is a lot, whatever you way you measure it. The question that sometimes comes up is … “With all that debt (leverage), will value investors still be okay if things go really bad?”

As we know, it is difficult to predict the future.

The good news around that is, this has more to do with timing than it has to do with the severity of any event – providing we are properly positioned. There are certainly some ‘grey swans’ floating about. For example, an increasing proportion of global debt is moving closer to junk bond status. What this means is that the quality of this debt continues to decline.

What that means is, should real trouble strike, bond investors are less likely to be repaid their full investment, if indeed they get any money back at all. This is a global phenomenon.

Here in New Zealand, we see bonds appearing on the market (as you may be aware, WISEplanning does not normally participate in these bond issues because we have other options as value investors) as businesses seek to take advantage of low interest rates. These bonds are increasingly of lower quality, coming out as subordinated debt and not guaranteed. Because the yields are better than bank, investors flock to them as they try to compensate for interest rates that are at so called 1,000 year lows.

We also have an increasing proportion of debt (bond investments) offering negative yields. Simply, this is where investors accept a low return for a time and the possibility of even making a loss over the term of the investment. Such is the unhappy combination of a lack of understanding of how to invest in growth investments and the fear of loss from investing in anything other than a fixed interest type of investment (be it term deposits or bonds).

Global debt appears to be growing faster than the increase in global activity (GDP), which is also not ideal; however, the global economy continues to grow. Economic activity continues to expand. This does go some way toward supporting high levels of debt. The reality is that levels of debt are likely to continue to grow.

The point worth perhaps raising here to make it clear is that, even though investors cling to term deposits and fixed interest type investments, such as bonds, those investments may offer little in the way of any guarantee that investors money will be safe. We only need to look back as far as 2007 through 2011 to see the demise of large institutions that had been around for over 100 years. Investors unwittingly discovered to their frustration and horror that this simple approach to investing only works … until it does not.

Are central banks running out of “bullets”?

I have been hearing for over 10 years, a line of thinking suggesting that at some point, the markets will stop believing in central banks and then it is “game over” (for the global economy).

I struggle to see how this could actually unfold in practical terms. For one thing, game over means total global economic Armageddon. There are no winners and nobody has anything to gain (perhaps apart from a few cunning speculators).

The reality is that central bankers have a variety of macro prudential tools at their disposal.

China is possibly the best example, off the top of my head, if we look at an example of a central bank that uses a number of tools to manage the Chinese economy.

For example, interest rates is an obvious tool but there is also quantitative easing. In addition to that, there is also another approach, whereby the Chinese Government, in the past, has reduced the level of reserves banks must hold. This means that banks can lend out more money, which in turn means people borrow and spend more which results in increased economic activity and expansion.

The point here for investors is, to be safe in fixed interest type investments, it is possible that local authority debt (possibly) and government stock may represent safe havens but then the yields that can be achieved on those types of investments are edging ever close to zero or in many cases around the world, are now negative.

What about property?

Property can be a useful investment although it is not considered to be a productive asset.

Property around the world, particularly residential property, has enjoyed that unique set of circumstances over the last 30 years, which includes easy money conditions, ever reducing interest rates and a consequential increase in the price of property.

This in turn has encouraged money to flow into that area to that point where, in New Zealand, in my opinion, property is no longer an investment, but what I often refer to as a religion. In other words, people invest in this area in blind faith because they have likely enjoyed success over the last 30 years and also one wonders if it is convenient to continue to believe or want to believe (rear vision mirror investing). This is sometimes known as blind faith.

Many of my clients have done the numbers already and whilst they have enjoyed good gains out of owning their own rental properties, ever increasing prices and ever reducing returns have made this difficult – especially when prices level off and cease to support returns.

Quick number crunching easily shows that when you add in maintenance costs, insurance and rates, residential property, without price growth, is not an ideal option.

More recently, we have seen hungry investors seeking out listed and unlisted property trusts here in New Zealand. For those looking for an income stream, they offer reasonable yields, particularly when compared to term deposits and other fixed interest options, such as bonds. Beware of those unlisted property trusts though that lack liquidity. When credit becomes tight try getting any yield at all, not to mention getting your money out.

The share market?!

As you know, playing the share market is to be avoided.

Value investing

If we think about what value investing really is about, we can see that it revolves partly around paying fair prices.

Back in the day, after the 1930s shake out of the markets and the ensuing depression, trading prices of shares were beaten down well below historical norms. It was a time when Benjamin Graham went about buying up cheap stocks. This was a successful method over many years.

Warren Buffett adopted this approach and even to this day, we still have many investors believing that value investing is simply about buying cheap stocks.

Several decades ago, Warren Buffett and Charlie Munger began working together. At one point, Charlie Munger raised the question to Warren Buffett, “Why, when you are investing in these cheap stocks, don’t you consider the quality of the business that you’re investing in with the same rigour?”

From that time on, value investing became more about buying quality businesses and paying a fair price than buying cheap stocks.

To be clear, there is a real difference between buying stocks using the usual financials (eg P/E ratio, PEG ratio, discounted cashflow, and other financial analysis) when compared to looking at the underlying business and the economics of that business. The short of it is that you are unlikely to get the same answer when you carry out those different sets of analysis.

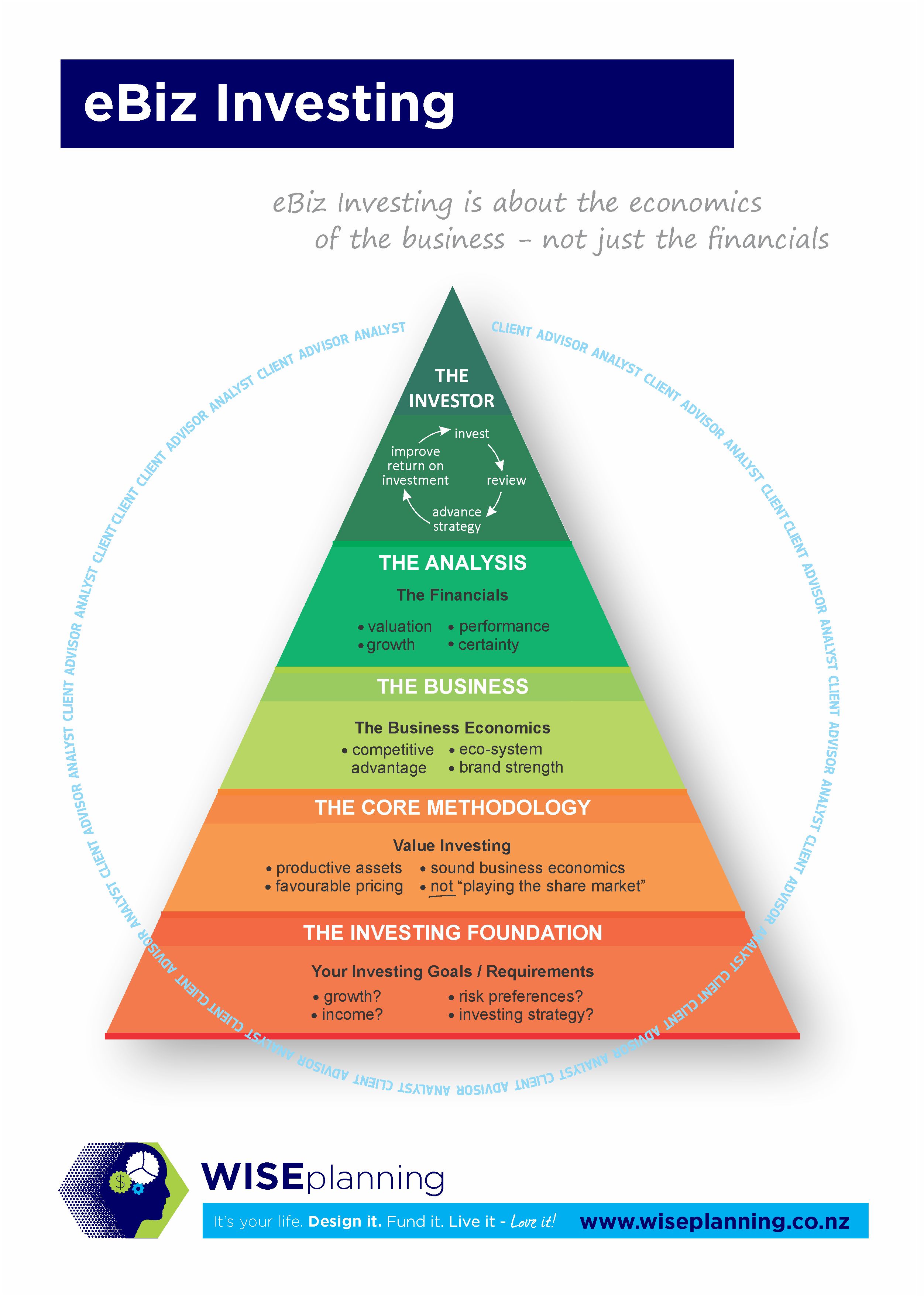

Value investing and e-Biz investing

Value investing has further developed at WISEplanning into what we now call e-Biz investing.

As you can see from the above diagram, e-Biz investing includes not only the usual financials that share brokers typically use but also the investors’ goals and requirements, along with the all important economics of the business.

So, what is the point?

Where this discussion gets to is the point that, quality investments are still the key to protecting our capital should a significant market related event erupt.

The idea that allocating capital to a bank or fixed interest investment to keep it safe is outdated and frankly, potentially dangerous in the environment that we are now in.

Investing in banks and other fixed interest investments may well reduce volatility in the short term but what is the point of that if the capital becomes compromised?

As we saw over 2007 through 2015, investing in quality businesses (as distinct from playing the stock market) was successful, particularly when compared to high risk fixed interest investments that the market generally followed as they looked to maximise their returns.

Value investing, or as we now call it at WISEplanning, eBiz Investing, still works even though markets are structured in an unusual way.

Being defensive as an investor offers no guarantee of safety.

eBiz investing helps investors to invest in quality businesses that will be resilient when markets suddenly become volatile and turbulent.

Sure, the trading price and the quality of a business all decline because the market becomes fearful.

The trading price and the underlying intrinsic value are not always the same thing, especially for us as eBiz investors.

A quality business with strong economics, however, will more likely remain resilient, protecting investors’ capital but not only that, offering investment growth for those conservative investors who can be patient but who prioritise growth and progress over fear and defensive investing.

What do you think?