Have the markets gone crazy!?

Investment Perspective – March 2016

Peter Flannery CFP AFA

“Neither the investing method nor the fundamentals of the business are right or wrong because the mood of the market is favourable or unfavourable toward the “stock”. That is because when you really think about it, “stocks” (shares) are all about the financials and the trading price, the share price… the cash up value. What matters more is the economics of the business”

Peter Flannery

Actually, the markets have not gone crazy, they always were …

As you know, the price of shares is determined every waking moment by the market. The market responds or rather, usually reacts, to recent news. It might be news of a general nature about the state of the world economy or it could be news about a particular company in which we are investing.

Either way, the market determines the price. By the way, I am not saying that the market is stupid. There are hundreds of thousands of highly educated and intelligent people carrying out analysis right across the markets every day. In fact this goes on 24/7.

I am suggesting though that markets are anything but sane and logical.

How do we measure success in the so-called share market ?

This is more difficult than most people realise.

Using simple price movement as a gauge of investment success just doesn’t make sense and yet it is the most common method used. Typically investors, analysts and others will look at a one month, six month or 12 month timeframe and use that as their benchmark.

Long term that starts to make sense however within the numbers reported there are some variables that make those numbers less than transparent. For example, is the stated return of 15% over the last 12 months gross before tax or after tax? Is it before fees or after fees? Is it before inflation or after inflation?

This complexity of course serves to either keep many confused about what it all means or to just keep people away from this area of investing because it is all too difficult and complicated. Not only that, there is the dreaded ongoing pricing volatility that few understand and fewer can tolerate.

Is that an advantage I see?

If everybody understood how the sharemarket worked, everyone would be doing it and it would be much more difficult to take advantage of price and mismatching value.

Many years ago as I was learning to be a financial adviser I was trained in modern portfolio theory. Basically the idea is to diversify and treat pricing variability as a risk to be avoided.

Later I learned that in fact diversification damages long-term returns and price variability is not a risk but in fact an opportunity.

As my friend Murray from Wellington has stated on occasion, “Investing can be counter-intuitive”.

Indeed one of the problems / opportunities is that falling prices on the surface looks like a bad thing until we understand the difference between price and value. What is interesting about this is that highly educated and intelligent people may well grasp the difference readily… academically.

That does not mean though that they are at one with it psychologically. That is to say, watching the cash up value of their investments decline through pricing volatility can still trigger anxiety and even fear. Interesting isn’t it when you would think they know better!

As I have often said, the logic is one thing however, the underlying psychology is quite another …

Let’s take a look at a couple of quick examples

The first one is a company called LinkedIn. Recently the trading price of LinkedIn dropped by nearly 60%, which meant that those who invested recently have lost 60% of their investment if they were to cash up now.

As obvious as it sounds, my clients and I adopt an approach that is based on strategy that spans 10, 15, 20 years and longer, so cashing up now is not on the agenda.

Something that many experienced investors know is that shifting money around from one thing to the next all of the time is generally a recipe for disaster long term. The traders will no doubt skite about the one or two big wins they had which makes it all sound so easy and doable (and Value Investing boring and slow). Usually though you hear less about the many losses that they incurred to get to that point.

Anyway, if we are going to invest long term let’s invest in things that are worthwhile so that we don’t need to worry about having to take our money out all of a sudden. That way we can take our time, let things unfold and if need be, we can buy some more should the price decline below our original purchase price.

Anyway, back to LNKD (by the way, please ignore the 119.35 top left of the screen shot – look at the price peaks and lows on the graph)…

Note the price peak of USD$253.22 on September 1 2013.

We are now May 11 2014 and the trading price of LinkedIn has dropped to USD$147.02. That represents a 42% loss for anyone who bought into LinkedIn at the peak. Fast forward now to January 25 2015 which is right over to the right hand side of the above chart.

Look what happens next …

As you can see, the price within the space of only a couple of days dropped from around USD$200 per share to nearly USD$100 per share which of course is around a 50% drop.

I have shown this example because the decline in the share price is a recent event and one that we are in the midst of working with as we average down the original buy price.

For those who invested some time ago there is a minor decline in the price from their original purchase and in some cases it is not worthwhile averaging down but nonetheless the opportunity exists to take advantage of the current low price. For others, who purchased shares in LinkedIn more recently there is the opportunity to average down the original buy price any time now.

When you invest like you are buying the whole business it is not about that last transaction and whether you made money on it or not. It is about the economics of that business and the opportunity to get more of it if you can – preferably at a bargain price if possible.

But why did the price decline though – something must be wrong!

The reason for LNKD’s sharp price decline was because the management at LinkedIn announced that they expect growth moving forward to be slower than previously anticipated.

Analysts following LinkedIn all over the world would immediately have gone to their computers, calculated the money that they will now not make because of the lower growth over the next several years (because even a small amount of growth decline can mean a significant drop in the amount of money that can be made in the future, particularly over the long term). They would have run the numbers and for a variety of different reasons initiated a sell on LinkedIn.

Some would have initiated the sell because they want instant growth this week and are happy to move on and redeploy their funds elsewhere in the hope of getting it – speculators looking for the next trade.

Some will have initiated a sell order because they speculated on the fast pace of company growth and hopefully the rising stock price too, now not rising at all!

And then there are those who sell because other people are selling – they are not sure why but they find a decline in the trading price an unbearable event that they can’t live with and so they move out – often at a loss.

Fund managers for example may initiate a sell because their mandate dictates that, for example, if the trading price declines by say a 10% benchmark over say 3 days then they must automatically sell out.

Hopefully you can see that these reasons have little to do with the underlying business of LinkedIn.

Anyway, this is a good example to show you because we are right in the middle of a significant price decline and the averaging down process is only just underway.

Let’s take a look at another example from our client files

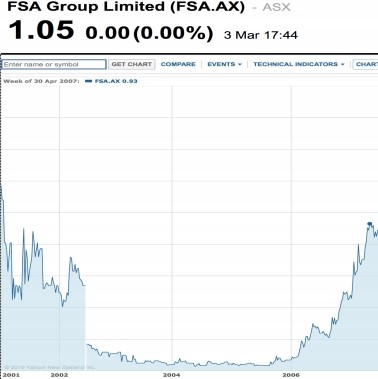

This (real life) example which some will know of is FSA. A small company out of Australia, FSA provides debt restructuring advice and more recently the funding for any restructuring of loans as well (please ignore the 1.05 number). Take a look at the peak…

The above chart shows the peak trading price of FSA at AUD$0.93c on 30 April 2007.

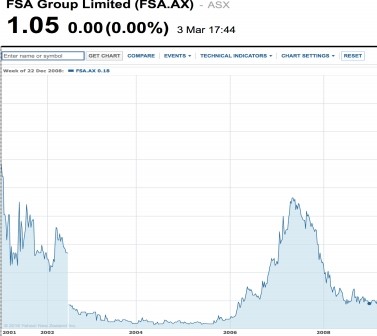

The above chart shows a trading price at AUD$0.18c on 22 December 2008.

Those who purchased at the peak of AUD$0.93, with the trading price now having declined to AUD$0.18 on 22 December 2008 have encountered an 80% loss – that’s small caps for you!

I know, this is bearable when it is just a few numbers that you are reading on a screen and not your money. When it is your money you’re looking at it takes on a whole new meaning. The question is what does it mean for you? How would you feel?

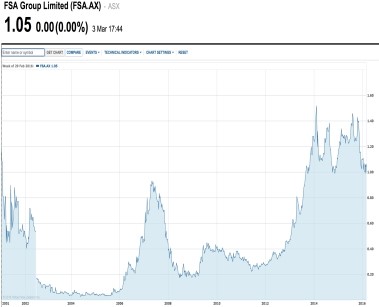

Let’s fast forward to March 2016 …

So, without boring you too much with relentless lines of numbers, most of my clients trebled and quadrupled their money even though they may have lost money on their initial purchase early on.

That is because we averaged down and bought more as the price declined. Not only that, my clients were patient, kept the faith and subsequently in some cases have sat on the gains, taking a long term view, happy to tolerate the pricing volatility. Others have either removed their original investment or taken profits (a greater amount of money) and repositioned elsewhere. Their remaining holdings in FSA owe them $0.00. They take some delight in reminding me about that from time to time!

Just to give you an idea of what it looks like in real life, I asked Sean Yang from our investment desk to put together real numbers from our client files…

Christchurch Client

07/12/2007 Purchased 8073 shares cost AU$4,469.06

01/02/2008 Purchased 14492 shares cost AU$4,976.55

22/12/2008 worth AU$4,062 against total cost AU$9,445.61

16/01/2009 Purchased 10526 shares cost AU$2,187.83

05/03/2016 worth AU$34,746 against total cost AU$11,633.44

FSA is a small company and of a higher risk nature than a large organisation like Google or IBM for example. Still, even large companies can see their share price decline steadily by a significant amount over time or rapidly because of some unexpected news.

The market, analysts, share brokers, fund managers and lots of advisers will initiate sell orders often based on reasons that arguably are valid, at least in the short term from a pricing perspective. We need to remember though that almost all investors and advisers are not Value Investors. They are playing a different game – thankfully.

Warren Buffett was asked in the 1980s why everyone didn’t invest the same way he did. His response was to say that he had noticed no discernible shift towards Value Investing in his experience.

In my experience, Value Investing is now “out there” so to speak and people in the financial world know about it because Warren Buffett has been so successful.

Without doubt he has special skill that is difficult to replicate – I can vouch for that! That said, most don’t grasp the idea of business fundamentals and confuse financial analysis with the underlying economics of a business. They are not the same thing.

As Warren Buffett has mentioned many times, there is a massive industry based on modern portfolio theory that promotes diversification to manage risk and the idea that price variability is a risk to be avoided.

Investing really can be counter-intuitive

That is because price and value aren’t the same thing and the logic of it whilst easy enough to understand is not the same thing as psychologically understanding it, knowing it.

Academia looks for complicated formulas and logarithms that require extensive education and ongoing analysis.

It seems to me that people somehow think the more we analyse something the better the decision we will make and the smarter we must be. There is usually little credence given to the underlying wisdom of methodology and the merits of keeping things simple – based around what works.

The challenge that most face is that the limited experience and conditioning by the market at large does not prepare them well for what works best. And yet, many of my clients can attest that the virtues of Value Investing resonated quickly and easily with them, right from the moment they first heard me talk about it.

It becomes a matter of investing in good businesses at a fair price and buying more of them should the crazy markets take the price lower even though the business remains sound.

“In the early years when we invest the money we make is determined by the voting machine (market sentiment driving the price up or down). The longer we invest though, the more the weighing machine (the underlying fundamentals of the business) determine how much money we make.“

Warren Buffett