Everything You Need to Know About Modern Portfolio Theory

Investment Perspective – May 2016

Peter Flannery CFP AFA

“Neither the investing method nor the fundamentals of the business are right or wrong because the mood of the market is favourable or unfavourable toward the “stock”. That is because when you really think about it, “stocks” (shares) are all about the financials and the trading price, the share price… the cash up value. What matters more is the economics of the business”

Peter Flannery

Common Practice and Best Practice:

Last month I canvassed the idea that common practice in the world of investing being best practice is questionable. In fact, it sounds to me like an oxymoron.

If you think about how markets operate, if everyone is chasing after the same thing the price will go up (the basic rule of supply and demand). Whether it’s property, shares, unlisted businesses and privately held enterprises, or anything else you can think of. If everybody wants it… “it” becomes expensive. And yet, as herd animals we instinctively want to do what everyone else is doing (believe it or not we are “wired” that way)!

The problem is, when we apply that to the investment world, if we are lucky we have “dumbed down” and mediocre investments. More likely though is a less fortunate outcome.

It’s not rocket science. If we invest in poor quality investments, pay too much, then the chances are that we are not going to make much money in the long run unless we are in early and a bit lucky.

Anyway, for us as Value Investors, we invest in businesses – we don’t play the markets. We diversify to capture opportunity rather than diversify widely to protect ourselves from capital loss. That is our advantage.

We just need to work out what we are getting when we invest (the intrinsic value) so that when we invest it is in a good business. Then it becomes a matter of pricing – paying as little as possible to at least cover the risk of that investment – or better still, get a bargain.

Pricing for Risk

The risk then becomes a function of how much we pay for that business.

If it is a poor quality business that relies on a variety of factors that may or may not come together for us to make money, then we had better not be paying much for this type of investment, if we go there at all. Of course, for some, those types of investments sometimes have the “promise” of spectacular gains – if they work out. Start-up technology companies come to mind for example. New listings (IPO’s) are another. When they go well it is mostly luck that we have them in our portfolios.

On the other hand if we have a business that can demonstrate sound business economics (sustainable competitive advantage, strong branding, uses capital well and consistently etc) then we have greater certainty about investment success. We can afford to pay a bit more for this opportunity because of the good quality and therefore increased certainty.

No need to be slicing and dicing our portfolio in order to spread it far and wide in the hope that we don’t lose any of it. Do you see what I mean?

The academics of course will argue that what I have just suggested is far from common practice (and therefore not best practice). They would be right about it not being common practice – nothing like stating the obvious. It’s not unheard of though. Ever heard of Warren Buffett… Berkshire Hathaway?

Sure, he and Charlie Munger have talent that few possess.

At the same time, the methodology (as distinct from their skill) is not rocket science and something that once we understand can readily deploy. Investing in good businesses at a fair price may not be common practice however I would argue that a good business at the right price is best practice.

That way we not only protect our capital from loss (I never said that was not important) but we also improve our chances of success and betterment. That is because we are investing in a quality business that we can understand, a productive asset of a calibre that improves our chances of investment success and helps reduce risk. By paying a low price, we reduce risk further.

There are no absolute guarantees but we don’t need them. In fact, I argue “The Rule of Five” is the only guarantee we need.

Fads (and Fools?)

Modern Portfolio Theory is a system. Whilst, not one that I believe offers us real opportunity, nonetheless, a better system than not having one at all for uninformed hapless investors using luck and hope as their strategy.

It offers a great way for academics and those who abdicate the responsibility of their own money and future financial security to others, a way to feel good about themselves.

But it’s not for everyone. There are problems with it.

What follows may feel a bit like “analysis paralysis” but if you would like to be a better investor, please stay with me. My thanks to John Mauldin who put some of this together in a way that is a bit intense but something I agree with 100%. So here we go… this is a way for you to stand aside from the herd – happily, confidently, by design and with conviction. Once you know this …

First the Jargon, then the Terminology

Modern Portfolio Theory (MPT) in the simplest of terms is about diversification and minimising pricing volatility to reduce risk (okay it’s about a bit more than that, but let’s just be happy with that for now). Modern Portfolio Theory has developed over several decades and so too has with it the jargon, the terminology and the complexity.

It is useful to note that MPT considers price movement as risk, particularly on the downside. Value investors see rising prices as a potentially increasing risk, especially when the intrinsic value does not rise with the price. Value investors actually see price declines as opportunity, particularly when a margin of safety emerges.

So, to be clear, for MPT investors declining price means more risk (bad). For Value investors declining price can mean both lower risk and improved opportunity (good). OK?

Beta: This is a measure of volatility or systemic risk of a security or a portfolio in comparison to the market as a whole. Basically it indicates whether an investment is more volatile than the market. Beta is used in the capital asset pricing model (CAPM), a model that calculates the expected return of an asset based on its Beta and expected market returns. Also known as “Beta Co-efficient”.

Alpha: also a measure of “risk”, measures the underperformance or excess performance of a portfolio compared to the market.

So, Beta is a gauge of volatility of a specific investment by comparing it to the performance of a related benchmark over a period of time. MPT investors / fund managers use Beta to see how much downside risk (price decline) they can expect from an investment. Kiwi saver is a well-known example of a managed fund structured and governed by MPT.

Sifting out the…

I have observed numerous ideas (fads) that have come and gone over the last 30 years as an advisor and an investor. Often these “ideas” are based on the collusion of a variety of factors unusually coming together to create a specific result that can be academically argued, but in practical terms, not easily replicated / repeated and ultimately unsustainable.

Smart Beta is a recent “idea” that has emerged in the world of modern portfolio theory and is promoted by academics and fund managers as a way to beat the market (but what is it really?).

Smart Beta attempts to use a set of investment strategies using “alternative index construction methods” (read, not mainstream) that are different to standard modern portfolio theory practices like capitalisation-based indices (e.g. invest in the 20 largest companies). Sorry, let me explain that a bit …

One method used for many years by fund managers was simply to replicate for example the 20 largest companies trading on the New York stock exchange or the New Zealand Stock Exchange. Investing in the 20 largest companies sounds like a good idea, safe, believable, right – at least on the surface. The investment mandate of the portfolio was around those 20 companies and they would trade within those 20 companies depending on price variance and other market or company related news.

Okay, back to where we were. “Smart Beta” attempts to capture investment factors or market inefficiencies in a structured rules based and transparent way. In short, they are doing much the same thing as everyone else although in a slightly different way, suggesting that this difference is an edge that will make investors richer. The idea is to beat the returns of those cap-weighted indices (the 20 largest) that I alluded to just before. They will attempt this using risk adjusted returns (the Beta Co-efficient) to demonstrate their success.

EDITOR’S NOTE: “Fund managers are always looking for a new angle, a new idea that they can come up with to stem the flow of funds out of their portfolios, particularly when the strategy they have used in the past or market conditions force them to show low returns or negative returns compared to their experience in the immediate past. Fickle investors don’t like lower returns than before. Worse, those uninformed fickle and sometimes defensive investors really hate even small losses. They readily “jump ship” to the next promising “idea” (bright shiny new object). So, fund managers look for new ideas and new ways to capture the imagination of investors and their money. For example, 25 years ago, investing in an emerging market fund was considered a cool idea. Inevitably the weight of money that went into those markets and pushed the prices of sharemarket indexes to unrealistic highs could not be sustained and crashed. You can imagine then what those fickle investors thought about those fund managers and the idea of emerging markets”.

A Bit More Jargon

Attribution Analysis: this looks at where returns came from. For example if there is out performance then why did it happen and is it likely to continue? In other words what generated the returns?

So, “Smart Beta” is a recent term that is gaining increasing popularity and refers to not just systematic contrary investing but also a number of automated strategies or “tilts” that a fund manager wants to tag as “Smart Beta”. Ironically, if everyone starts really doing contrary investing then contrary investing can no longer exist.

So there are now “Smart Beta” products and funds that have factors or tilts towards value, momentum, small companies, profitability and other investing “ideas”. By tagging an investing “idea” or slant as “Smart Beta” the market (the herd), believes this automatically offers above market performance. As it increasingly becomes common practice it becomes believable, more “normal”.

Here’s the thing, a lot of these strategies are using recent performance and short dated (recent) back testing to demonstrate how good they are. What do you make of that?

Fund managers parading a line-up of recent best performance factors and strategies usually are just setting themselves and their investors up for some bad news in the future.

Some of these strategies by the way involve trading and as you know, trading comes with a cost – to the investor. The 20 largest companies’ strategy I mentioned before would have investors moving in and out any and all of those same companies several times. Is it just me or is moving in and out of the same company several times based on the price moving up and down a complicated and expensive way to protect capital and make money?

Unnecessary buying and selling is an efficient way to reduce returns. Accurately predicting price movement long term is difficult. Every trade costs money That is why at WISEplanning we have a low turnover policy built into our portfolio design. We select carefully, watch and keep adjustments to a minimum.

Another interesting point about some of these approaches is that they became Smart Beta “strategies” through price movement and becoming more expensive. The price of certain investments rises above other investments and does not go unnoticed by the canny fund manager looking to impress. It’s as though the unusual set of variables coming together are somehow a strategy, a way of investing that is suddenly better than everything else.

Unless the fundamentals of the underlying investment follow the rising price, what we have is increasing risk, not necessarily a better investment. Prices significantly outpacing what is really going on below the surface never last. A correction occurs at some point. Those who get in late don’t get rich.

So let’s take a look at the core of this issue (pictures coming)…

Understanding What Drives the Numbers

Those less familiar with economics, how numbers can be arranged to tell a story and statistics, can sometimes be quite sceptical about what the numbers are really trying to say – in other words they wonder, are the numbers honest?

What I can confirm, is that some fund managers and other players in the market use numbers in a way that makes their investment offerings look better than they really are.

As I mentioned previously, for example, many fund manager’s use back testing with short-term recent data highlighting a specific period in time, which doesn’t really tell the full story.

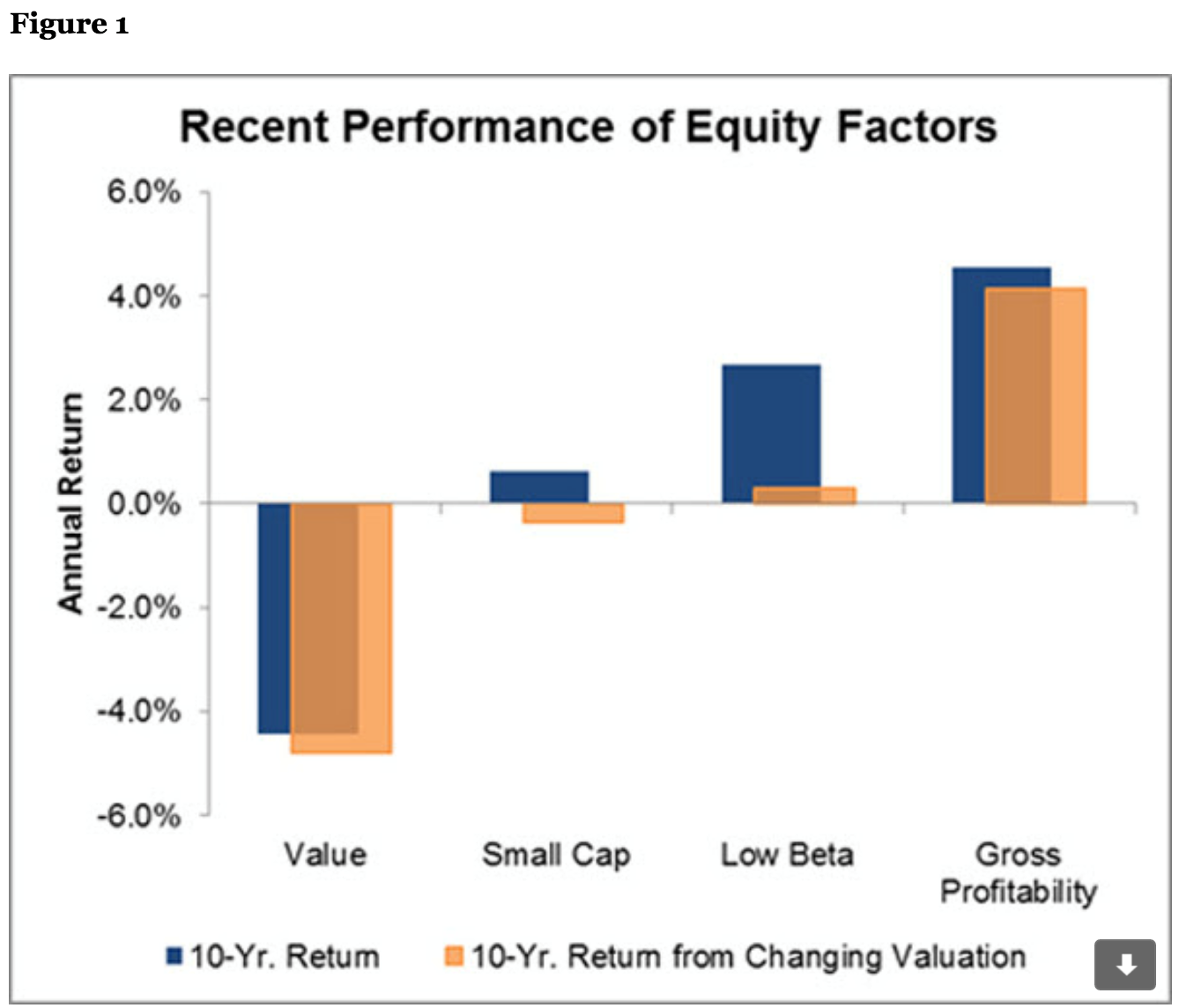

Take for example the two charts below.

Figure 1 above (using a back test with short term data) could easily lead you to believe that Value Investing is a lost cause when compared to the other approaches of investing in small companies, low volatility investments and those companies that show a high gross profit margin.

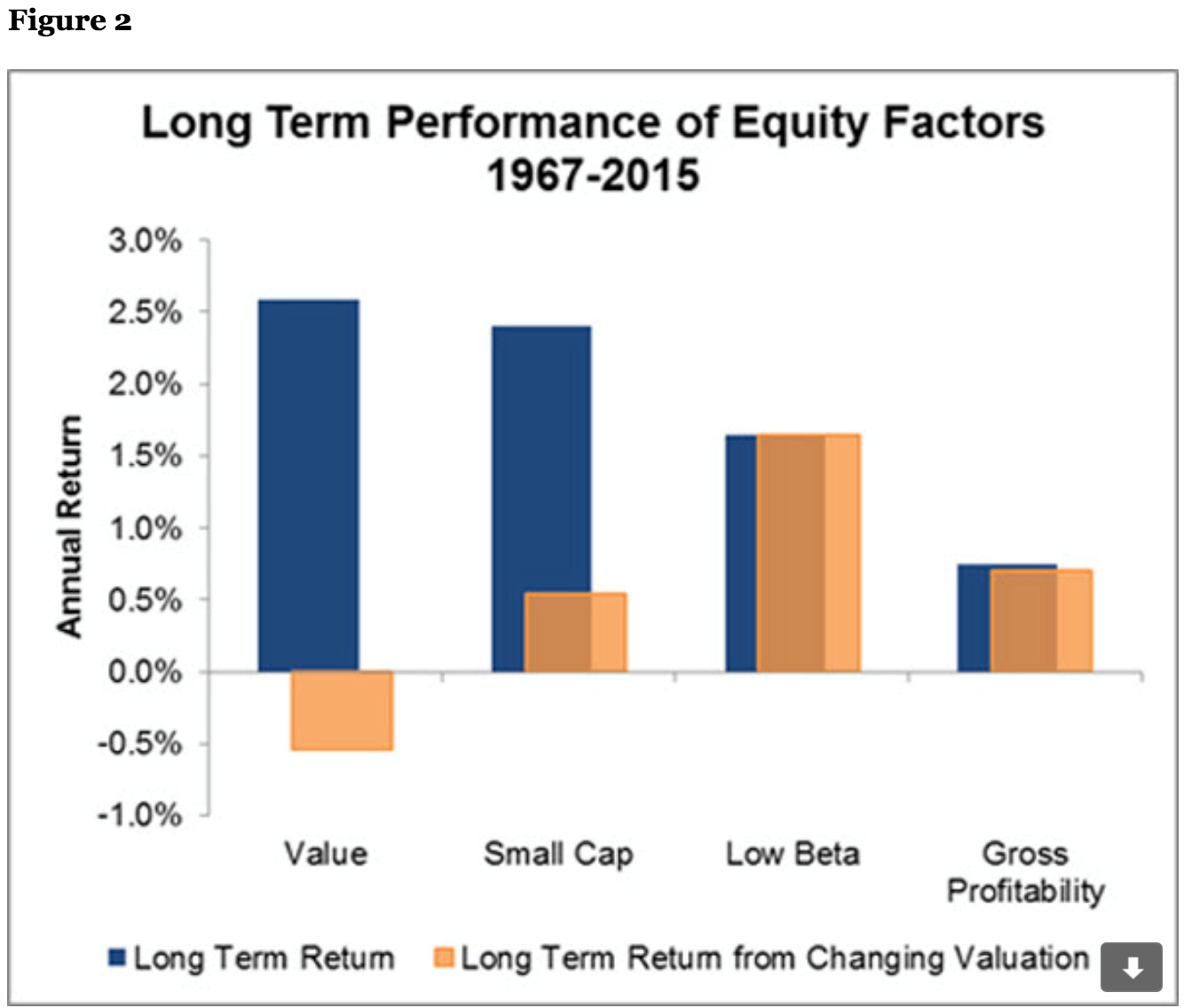

The chart above (figure 2) offers a different perspective from 1967 through 2015. The short term back testing data showed that gross profitability was the winning strategy however the longer term back testing data using arguably a more full sample of information tells the real story.

“Modern Portfolio Theory (MPT) is classic blind academic devotion to systematic investing stupidity, readily available in Brainy Stupidland”.

The Editor

After All… We Are as Humans, Herd Animals… With the Inbuilt Herd Instinct

For most people, seeking out best returns and keeping capital safe triggers certain emotions when specific information is presented in a certain way. We then make decisions based on emotion, then rationalise with intelligent sounding logic.

Interestingly too, in my experience many people with money in their pockets feel the need to either spend it or invest it. They struggle with the idea of sitting on it and waiting for opportunities to emerge (that is also true of some of my own clients who know better!).

Sometimes it’s as though if the money is not invested immediately, opportunity is lost every minute that rolls by thereafter.

We all make decisions on the basis of instinct and emotion and then rationalise with logic backed up by an educated sounding rationale. It seems that the more educated we are the better we are at this – but not necessarily more successful as investors.

Here is One Thing that Works Well for Investors

Developing / using a methodology based around the fundamentals and then adopting a very disciplined approach around that method, particularly over the long run, will see decent results emerge over time. Investment success.

The trick it seems for many is to get through the supposed “academic prudence” of MPT as well as the common overemphasis on tracking investment returns based on the cash up value of an investment over short timeframes as a measure of investment success or failure.

Price and value are not the same thing.

That’s why measuring the success of an investment portfolio on the basis of its popularity (the cash up value of the portfolio rising and falling) is non-sensical, especially in the short term.

Sure, longer-term, price and value are likely to be more closely aligned but frankly it’s difficult to know what that timeframe should be. For no real good reason or any sound logic at all, five years might be a starting point.

Even then though, because market trends that impact pricing can stretch over decades, a five-year timeframe may not necessarily reflect the full story. For example, the liquidity bubble, a phenomenon that I have talked about now since 2003, has arguably had its beginnings in the 1970s’ and has been building for several decades.

Of course, investing in something and waiting for 30 years to see if it works is highly impractical to say the least.

Here is What We Can Do

In my view, this brings us back to something we can rely on: methodology – THAT…is what works. As an investor you and I have an advantage when we understand the Value Investing methodology. That way we can have real control over our investments both in the short term and the longer term.

We have an even stronger advantage when we apply that method with real discipline, unwavering in the face of short term pricing fluctuations and, at times, significant market “noise” (market banter suggesting we are going in the wrong direction or have done it all wrong!).

We cannot control the markets or the pricing, particularly in the short term. We don’t need to. We can position ourselves with the right method. It is workable gives us control and we can be successful investors long term, regardless of economic conditions.

“Warren and I have a long attention span, that’s why…“

Charlie Munger – Warren Buffett’s partner

(when asked why he and Warren Buffett were so rich )