Global Economy Looks Stable

Global Economic Update – January 2018

Peter Flannery CFP AFA

“If you have one economist on your team,

it’s likely that you have one more than you’ll need.”

Warren Buffett

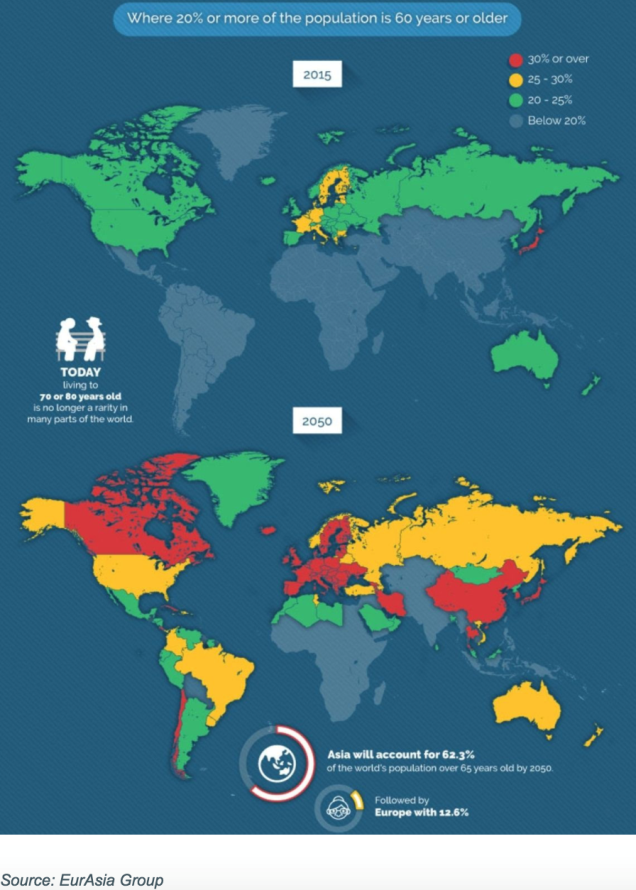

The above chart shows aging demographics for the global economy. Note the difference between the 2015 chart at the top and the 2050 chart at the bottom.

Global demographics is an often forgotten indicator of economic growth (or lack of it … e.g. Japan potentially). With an aging population and low birth rate Japan looks to be facing a difficult demographic in the not too distant future. For the developed world, that issue looks quite a bit further out into the future and is of little concern at the moment. For emerging markets, their demographics are positive.

Right now the global economy remains stable and whilst there are a number of potential trouble spots, the significant debt across the global economy is one that right at the moment in my opinion, will NOT cause a serious crisis. Longer term maybe, but not right now.

Excessive debt may create difficulties at some point however Governments and their economies, particularly the larger ones, tend to bluff their way with it. The US, China and the European block, which makes up a large proportion of the global economy, have a raft of tools at their disposal to dodge the debt bubble blow out problem. Ironically in some cases they just make it a bigger bubble.

So, debt is a problem but not one that the global economy will collapse over in the immediate future. Longer term we will just have to wait and see how the issue is dealt with. Inflation and ramping up the cost of goods and services is one answer to the debt bubble however at the moment inflation seems hard to come by, right round the global economy. Deflation remains entrenched.

America’s unique “package” started off around 1750 and apart from a few ups and downs, has not stopped since.

America has a unique economic package not replicated elsewhere. Whilst there may well be faster growing economies and obviously many would point to China as a case in point or India, however the United States of America remains unique. It has among other things the strong combination of low population per hectare, massive resources, a comparatively highly educated population, strong rule of law, innovation and global scale which has provided the United States of America with a powerful economic engine second to none. It is a robust and resilient economy. Although from time to time they manage to make a mess of things, the economic power house of the United States of America remains resilient.

The Chinese economy continues to grow at a robust pace.

In short, the economic reforms that I have talked about in China over the last 12 months or so in a number of my economic updates is a key factor for the Chinese economy. Basically, scaling back those inefficient state owned enterprises in favour of other structures as well as taking real control over decades of in-built corruption are both important for China.

In my opinion China’s increasing debt could potentially be a problem however that may not be the case for some time. More likely in my view, is the shadow banking dilemma that has grown to a significant size. Indeed, the size of the problem is significant and would impact on the global economy if it were to collapse. Secondly, is the inferior quality of that lending. That’s why if things do go bad in this area, in my opinion the Chinese government will have no option but to step in.

It wont erupt just because you and I are talking about it. Nor will it go away anytime soon!

Elsewhere in the global economy the Eurozone is stable and growing at a slow pace, even Japan is showing some growth although of course it is supported by significant stimulus. The Australian economy is doing okay and here in New Zealand, the new Labour Government is really only still settling in. I suspect that, whilst the New Zealand economy, which tends to follow global trends to some extent anyway (because we are so small) will continue on at a reasonable pace of growth all things equal (est. 2.5% – 3.0%), however it will be interesting to see if Jacinda Ardern can maintain her personal “favoured nation status” and if so for how long?

Without doubt the Labour Party has minimal fiscal wriggle room and things need to go pretty much as planned given the spending programme they intend to roll out over the next two or three years and beyond. How will they fund it all?

Interest rates are reasonably stable although it would not be a bad idea to watch the US Federal Reserve. In short they are keen to ramp up interest rates which I suspect will steadily unfold over time, especially as interest rates globally remain accommodative. They are looking at another three rate hikes over the next 12 months.

There is nothing obvious in front of us all in terms of a major economic catastrophe, however that doesn’t mean to say that something won’t suddenly emerge from an economic corner that few are looking at. I wouldn’t lose any sleep over it yet. Indeed, the current so-called “Goldilocks phase” (good times / bull markets etc) are only about half way through by some measures. Not that I would rely on historical economic cycles and data to map out my life but nonetheless that is an interesting bit of information.

Although nothing is obvious, the economy can be full of surprises because it is pretty much a random walk. As I said earlier, let’s not loose sleep over that. Instead, lets all remain focused on our investment goals and maintain the discipline around our Value Investing methodology – regardless.

Happy New Year and all the best for 2018.