From Warheads to Brunch

Global Economic Update – March 2018

Peter Flannery CFP AFA

“If you have one economist on your team,

it’s likely that you have one more than you’ll need.”

Warren Buffett

Donald Trump and Kim Jong Un making conciliatory tones.

It wasn’t that long ago that nuclear warfare was ringing across the headlines of the internet and good old-fashioned, mainstream newspapers. Now, it is all about how Kim Jong Un and Donald Trump are going to have a meeting, which let’s face it, is a step in the right direction. Obviously, nuclear warfare is a difficult economic scenario to work through and one almost not worth thinking about. More likely (happily), it will be other less evil events that we will need to contend with.

Trade tariffs initiated by Donald Trump could potentially have far-reaching implications for many economies, including New Zealand. However, before we get too depressed, let’s just see what shape they take and how far reaching they actually turn out. Within days of the announcement, Donald Trump pushed forward with plans for 25% tariffs on imports of steel and a 10% tariff on aluminium but stated that exceptions would be made.

The next thing you know, Australia has been given dispensation as per Donald Trump’s post on Twitter. Basically, in exchange for “security arrangements”, Donald Trump mentioned in his tweet, that there would be no need to impose steel or aluminium tariffs on their ally, the great nation of Australia.

China, on the other hand is warning of a trade war, which would end badly for everyone, an understatement if things get out of hand. China, of course, continues to vow that it will defend its “legitimate rights and interests” if targeted by US trade sanctions. The Chinese Commerce Minister, Zhong Shan, said that China does not want a trade war and will not initiate one. He said, “There are no winners in a trade war, it will only bring disaster to China and the United States and the world.” Well said.

China, for its part however, could respond by targeting US coal. It just so happens that this sector is reasonably central to Donald Trump’s political base as well as his election pledge of restoring US industries and blue collar jobs. By some calculations, the US is the world’s largest importer of steel, having purchased around 35 million tonnes of raw material over 2017, of which 6.6 million tonnes came from Japan, China, South Korea and India. Actually, China accounts for only a small amount of US steel imports, however its significant industrial expansion has helped to create a glut of steel across the globe that has in turn driven down prices. Anyway, early days yet for tariffs. Let’s just see how it plays out.

As for Europe, Donald Trump “upped the ante” and the ongoing row over trade tariffs, suggesting that if the European Union did not lower its trade barriers on US products, he might consider introducing import tariffs for European cars. In his own eloquent style, he said, “We’re gonna tax Mercedes Benz, we’re gonna tax BMW.” A tax on cars would be particularly problematic for Germany, as the auto industry is an important part of the German economy. As Angela Merkel, the German Chancellor, pointed out, A “tit-for-tat” war could result in higher prices and reduced growth around the world.

And in other news, the global economy remains stable, with economic growth underway, although fragile.

In light of last month’s market volatility and the concerns around possible inflation, at this stage, the threat of inflation appears limited. Wages growth is underway, although it is not significant either. Interest rate rises are a mixed bag around the world, with the US Federal Reserve looking to implement four increases at 0.25%, which would still take us to a place where interest rates are low and accommodative.

I am thinking that “deflationary funk”, including levels of marginal productivity around the world, still has a firm grip on the global economy, although I note that economic growth around the world, as measured by GDP, is looking reasonably buoyant over the next year or so.

The United States of America

Trade tariffs are on their way.

Trade Sanctions against America’s trading partners one imagines(?) has been well thought out and discussed around the table, in order to avoid those same sanctions hurting not only the American economy but also blue collar workers in America. As I said before, it is early days yet.

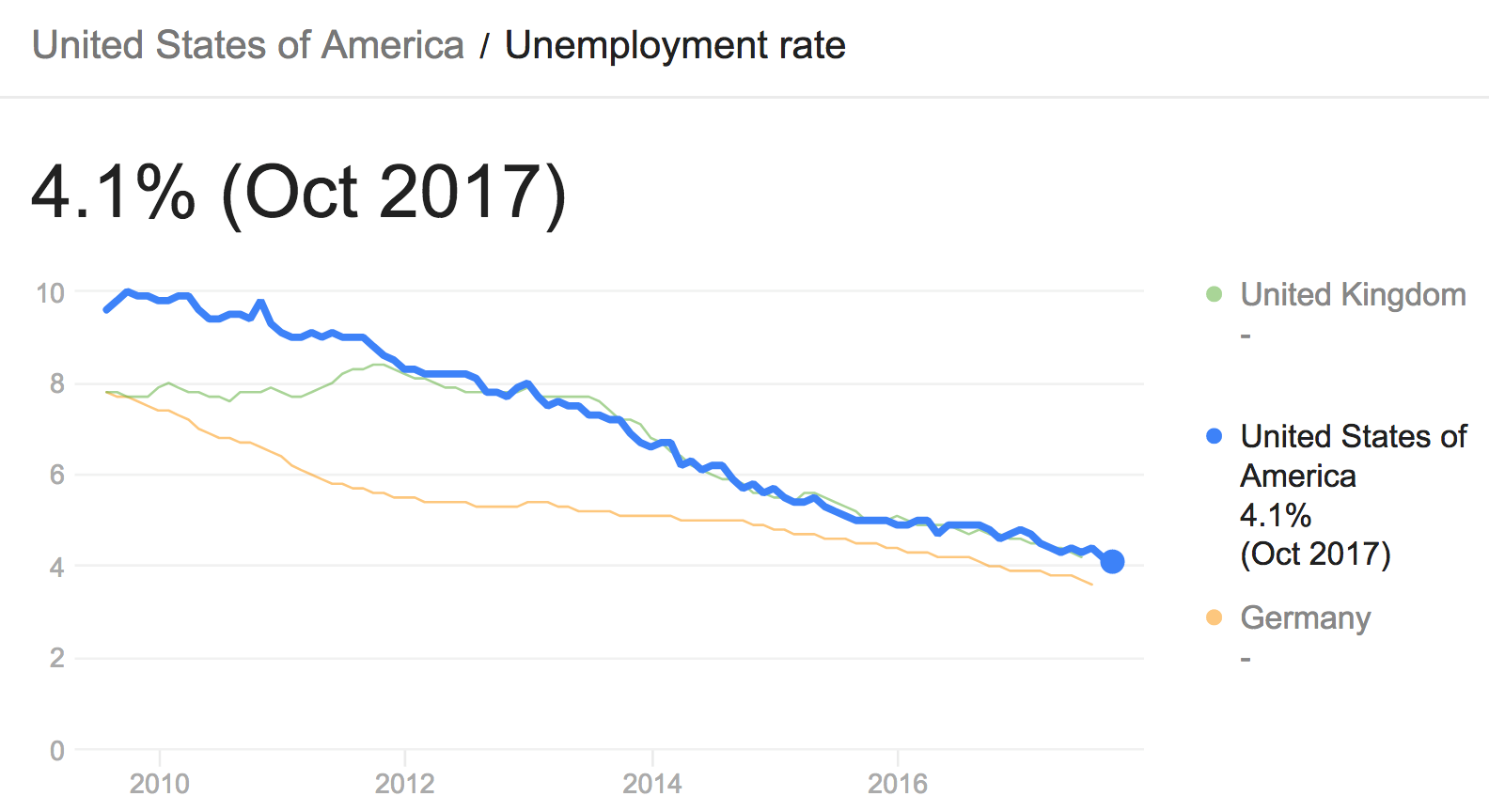

Note: unemployment in the US is similar to the United Kingdom and Germany and continuing to decline.

Reducing unemployment, inevitably, is good news, not just for large businesses but also for everyday citizens who need work to live.

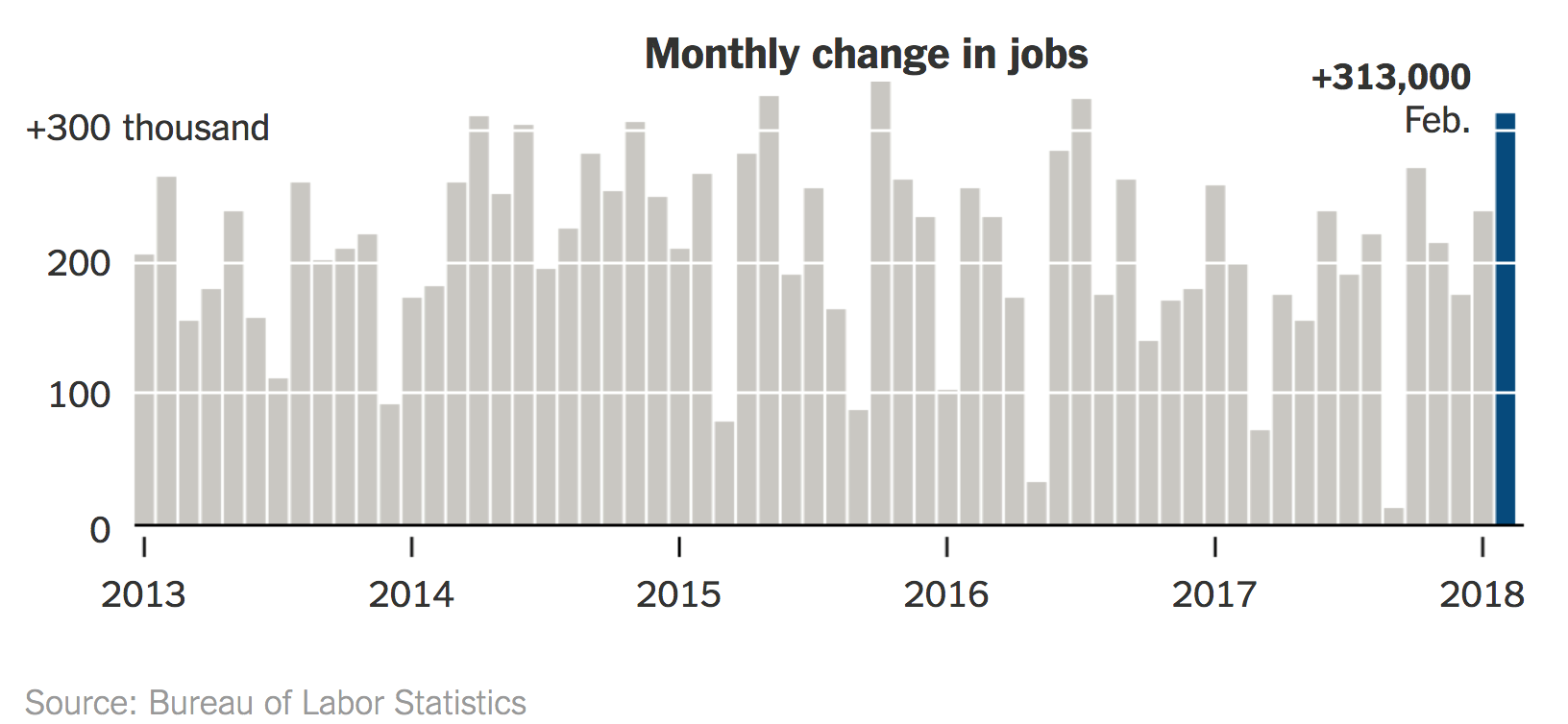

The US economy added yet another 313,000 jobs in February.

What is significant about the above chart is that the addition of 313,000 jobs is quite good, however it takes on a whole new meaning when we consider that unemployment is down to 4.1%. This is significant because economists have been expecting wages growth to ramp up, possibly leading to inflationary pressures, however so far, this has not emerged. I reckon it is simply a delayed effect and inevitably, we will see some lift in inflation at some point as a tighter labour market leads to a shortage of good talent and therefore pressure on wages to rise. However, this could take a while, given other deflationary factors that remain at play.

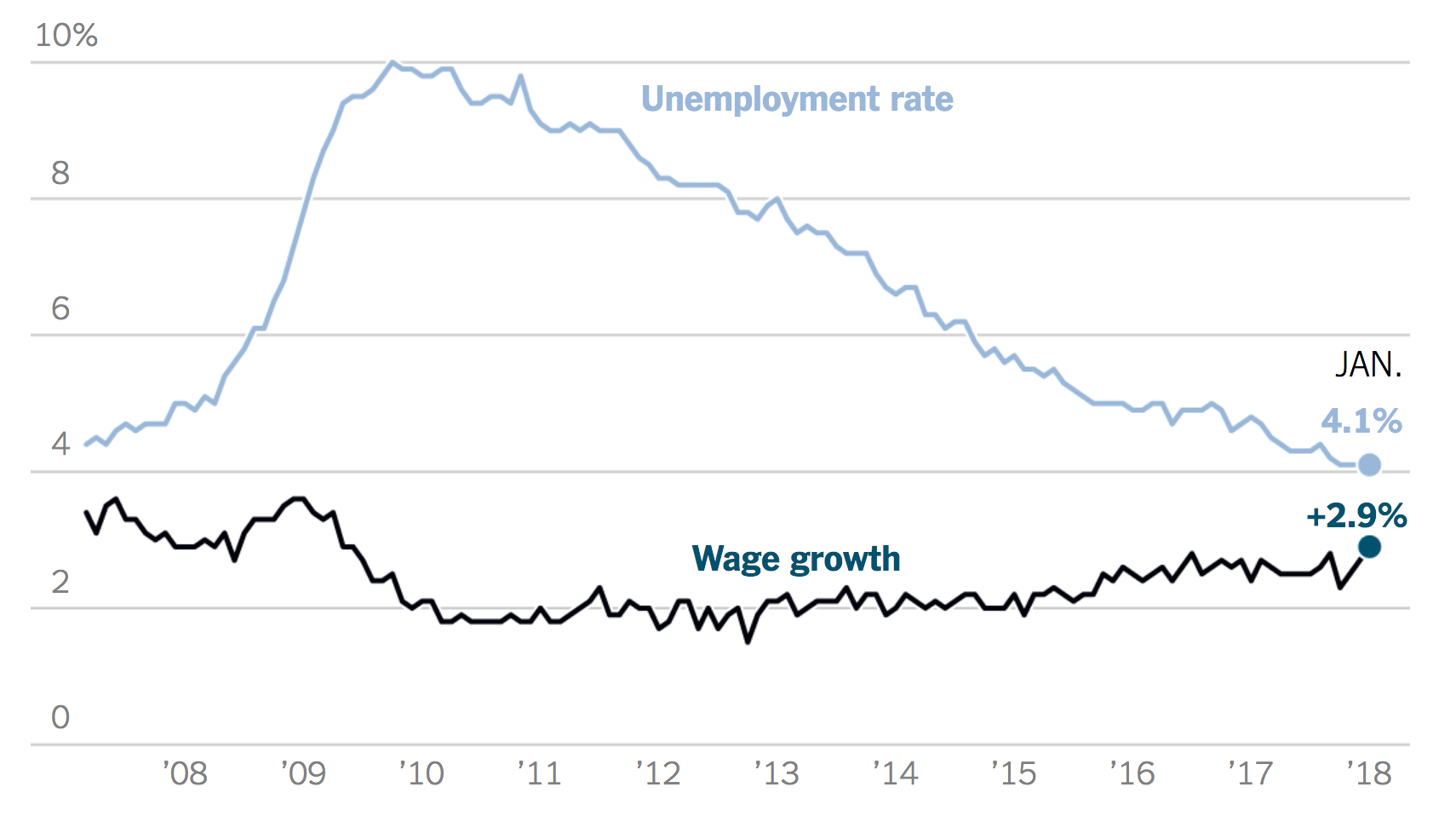

Wages growth in the US declined in January.

‘The Phillips curve’ suggests that declining unemployment will lead to wages growth, which indeed has been underway since around June 2017. This is a key indicator to watch for those who are concerned about the impact of rising inflation and rising interest rates.

Declining unemployment should eventually lead to wages growth.

The worry about wages growth for some is that this may lead to rising inflation and therefore rising interest rates. Basically, the army of analysts around the world, with their spreadsheets, calculating the impact of interest rates at various levels, can trigger market corrections, a bit like we saw in February. Expect more of the same in the future as interest rates continue to rise, as per the US Federal Reserve mandate of four increases over the next 12 months. As I said earlier though, even with those four increases, interest rates still remain accommodative and low. The real question though is always around how the market will react (??).

China

President Xi Jinping.

Back to one man rule. Xi Jinping has had the limit on the number of terms that a president can serve removed, which means that he could rule for life.

Some worry that this concentration of power could compromise future governance of China and decision making around its economy because some top officials might be less likely to push back against the powerful president, even if they thought the president’s plans may harm the economy. That remains to be seen. What we do know is that unlike Russia, that basically disintegrated from a once powerful nation, China has a good chance of staying the course long term and maintaining its power base as a communist state under Xi Jinping’s rule. He has pushed the much needed reforms in China along and many believe he will continue to do so moving forward, which is good for China. Some compare Xi’s strong position to those European counterparts, whose leadership positions are weaker, making it harder for them to push through reforms. There are risks with concentrated power, participating in an economy the size of China’s, however there may also be some upsides in terms of continuity of power and ongoing economic progress, maintaining China’s power as one of the most powerful in the world.

China’s economy produced 23.12 trillion dollars in 2017 based on purchasing power parity. It is the world’s largest economy. The European Union is second at 19.9 trillion, with the United States of America third, producing 19.3 trillion dollars. China’s economy, however, only produces $16,600 per person, compared to America’s $59,500 per person. Lower wages mean that China can pay their workers less than American workers. That means China can make products cheaper, which encourages manufacturers from other countries to outsource jobs to China. They then export finished goods to America, which is China’s largest trading partner.

Donald Trump’s problem, of course, is the $375bln deficit (2017), hence trade tariffs. The trade deficit exists because US exports to China were only $130bln, while imports from China were $506bln.

Donald Trump’s other issue is the strength of the Yuan against the US dollar. Long story short, Donald Trump wants the Chinese Government to raise the Chinese currency against the value of the US dollar, which in turn helps to make America a bit more competitive in the global economy. There is some evidence that suggests the Chinese Yuan is actually not undervalued and so, if that is true, then China may not share Donald Trump’s enthusiasm for that idea. Let’s watch this space.

Europe

Cars for export at a shipping terminal near the German town of Bremerhaven.

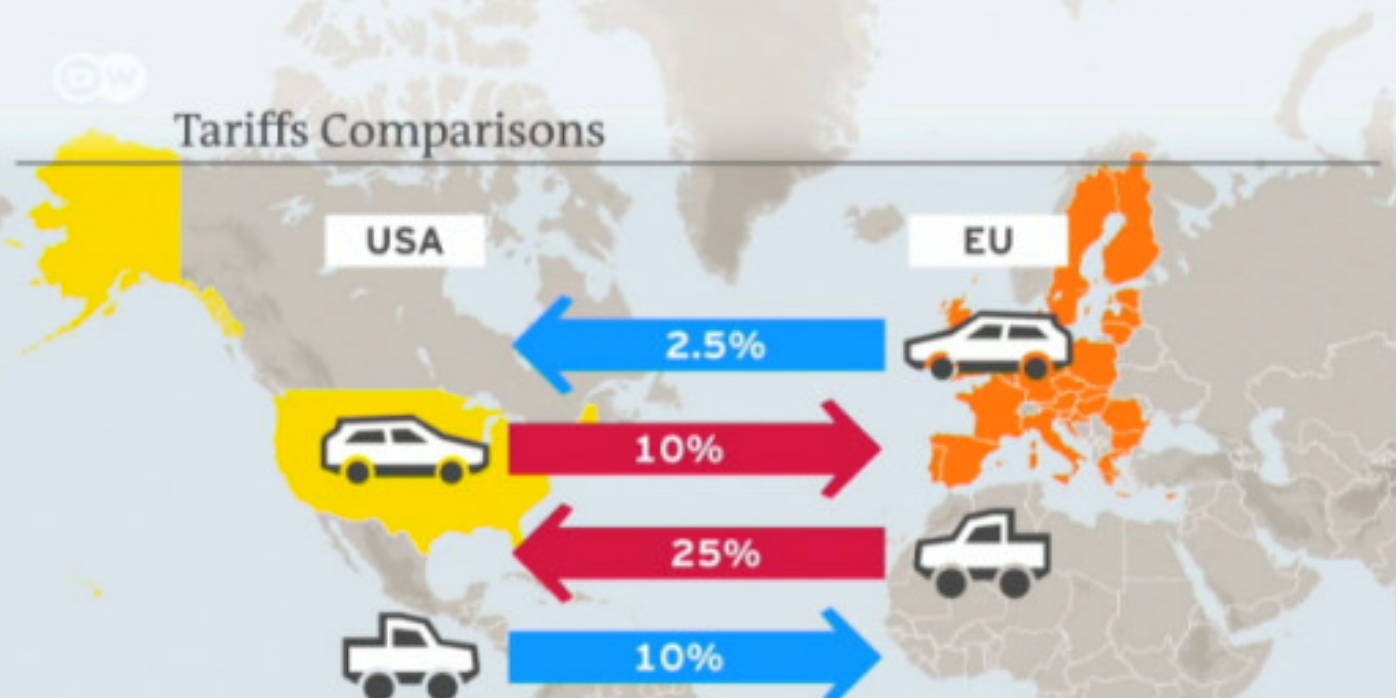

Donald Trump, in his usual fashion, appears to be refusing to yield to US businesses and foreign trading partners, who are concerned at the prospect of a trade war. The US imposes a 2.5% tariff on cars assembled in Europe and a 25% tariff on European built vans and pickup trucks. Europe imposes a 10% ban on US built cars. Donald Trump accused the European Union of, “Banding together in order to beat the United States at trade.” The US accounts for around 15% of worldwide Mercedes Benz and BMW brand sales, while it accounts for 5% of VW brand sales and 12% of Audi sales.

The US had a $22.3bln automotive vehicle and parts trade deficit with Germany in 2017 and a $7bln deficit with Britain, according to US Government statistics. Obviously, Donald Trump’s recent implementation of 25% on imported steel and 10% on aluminium will impact on European automakers. Amusingly, the day after Donald Trump announced his tariffs, the European Commission President went on German television to say that, “We will put tariffs on Harley Davidson, bourbon and blue jeans (Levi).”

Back in January 2017, Trump mentioned then that he may impose a border tax of 35% on German vehicles, imported into the US market. This looks like one of those election promises that he is determined to see right the way through. That said, it still remains to be seen exactly how it plays out.

Otherwise, the European economy maintains fragile but stable growth, with any impact from trade tariffs well too early to have any impact right now.

Australia

Australia and the United States negotiate trade tariffs.

In a post on Twitter, Donald Trump said he was negotiating directly with the Australian Prime Minister, Malcolm Turnbull. The bottom line is that Australia has an exemption, although there is some debate around what Australia needs to do as a close security ally of the US. Australia is one of America’s close military and security allies and a member of the Five Eyes intelligence alliance. The Australian Government, which believed it had already previously been given a promise of an exemption, had nonetheless been working very hard behind the scenes to win similar exemptions to those granted to Mexico and Canada.

Elsewhere in the Australian economy, interest rates remain on hold, inflation remains low (indeed too low for the Governor of the Reserve Bank of Australia). Economic growth is sluggish but stable and wages growth also remains slow, like many other countries around the world.

New Zealand

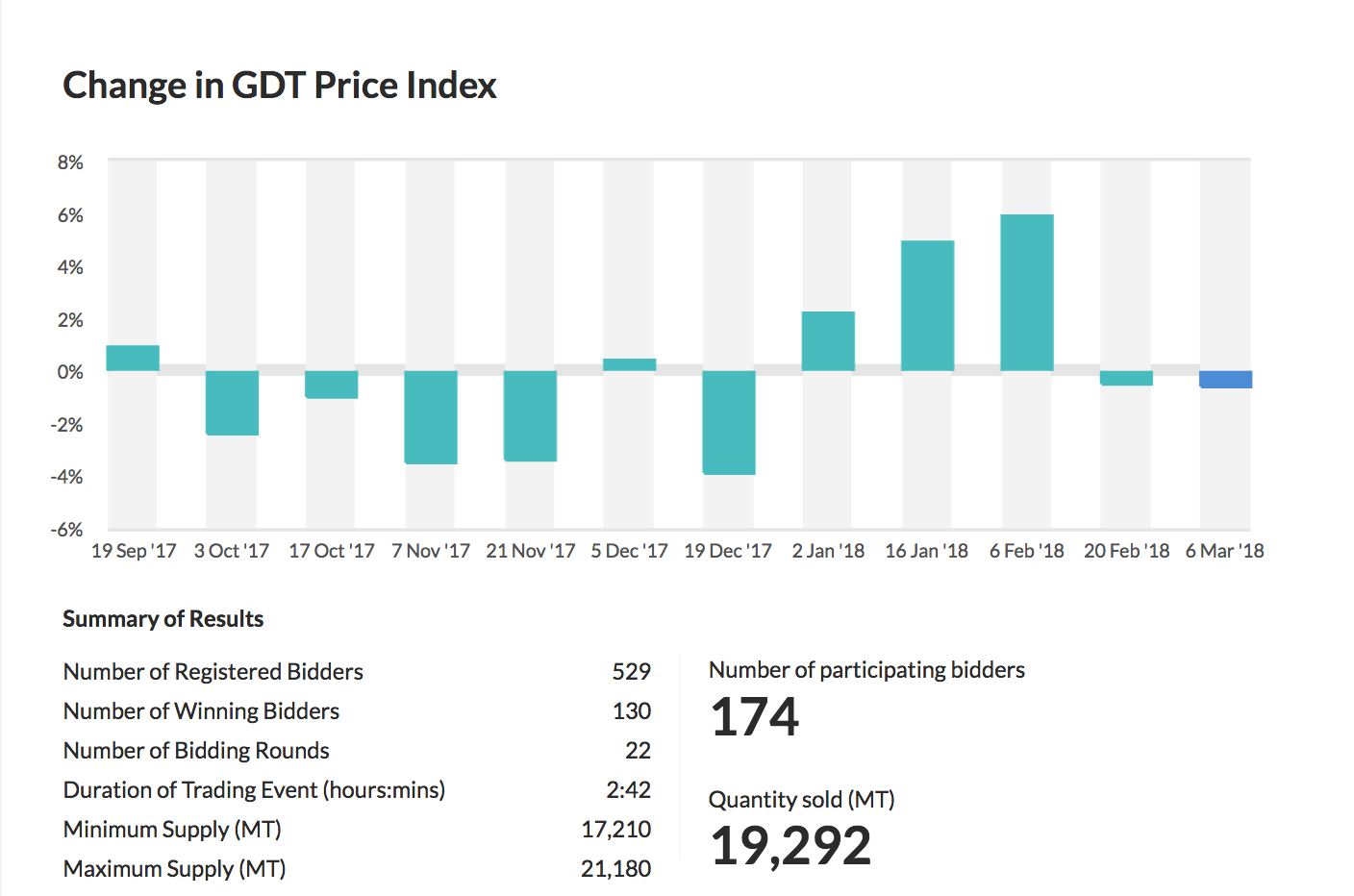

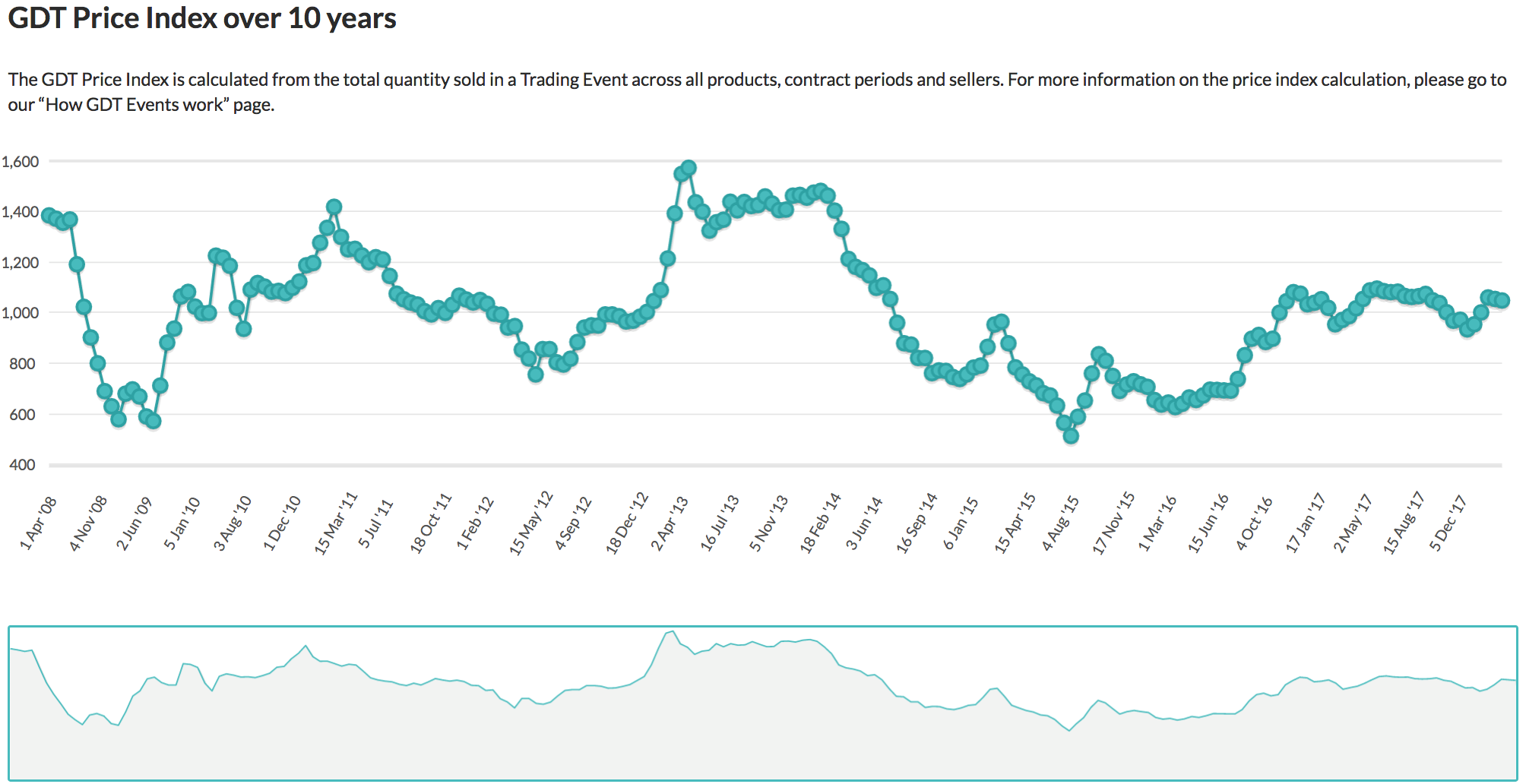

The above charts show the volatility of the dairy price, understandable though, when you consider milk solids are a commodity and subject to supply and demand.

Although the index declined a bit at the March 6, 2018 auction, the average price in US dollars remains at $3,593, which is a modest margin above the magic $3,000 threshold that in theory means break even for New Zealand dairy farmers.

Of course, the real question remains around what impact trade tariffs around the world might have. US farmers are concerned that the backlash against America could result in tariffs being placed on agricultural products, which could easily impact on New Zealand agricultural products too. Indeed, this is a real possibility, although a bit early to know for sure right now.

Elsewhere in the New Zealand economy, the new Labour Government appears to be settling in with the National Party reorganising itself as the new opposition. An interesting new line up, let’s see what they can do.

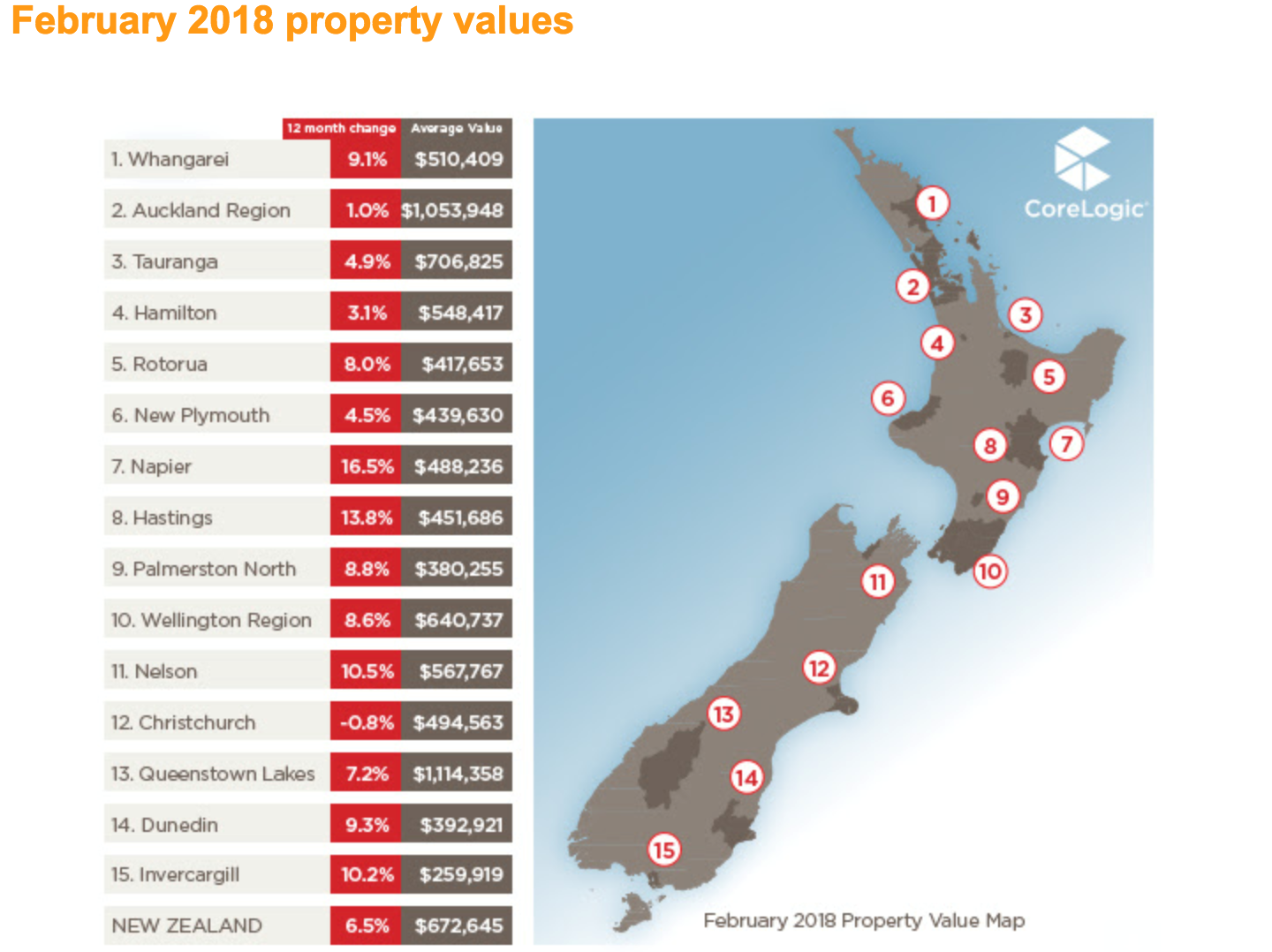

Overall, price rises across New Zealand are slowing.

Again, Christchurch is outstanding with an annual decline in residential property prices of -0.8%. It appears that the ripple effect is underway, whereby the rises started in Auckland and moved to other main centres. More recently, Auckland price rises have declined and provincial areas are now rising strongly, eg Invercargill 10.2% and Napier 16.5%. This slow down in property price rises is good news, not only for first home buyers, who now have half a chance but also for the New Zealand economy, which at this stage, looks likely to avoid any serious residential property pricing correction (all things equal).

Elsewhere, in the New Zealand economy, like a number of other countries around the world, economic growth remains stable but somewhat fragile, interest rates low and accommodating with inflation not really evident at this point. Unemployment remains low, however wages growth stubbornly slow too.

Will the new Labour Party be able to fund its proposed expenditure over the next two or three years?

Will trade tariffs actually turn into a trade war with far reaching implications across the globe including New Zealand?

Will its impact remain moderate and targeted, allowing the global economy to work its way through it, continuing to grow?

To Summarise …

Trade tariffs could easily lead to an all-out trade war that would definitely impact on the New Zealand economy, however at this stage, that point of view is merely speculation. It is possible but not inevitable.

The World Trade Organisation, attempting to warn Donald Trump that his proposed levies on steel and aluminium could trigger a domino effect, leading to a global recession and what they fear is the first full scale tariff war since the 1930s. It sounds really bad when you put it that way!

Europe, China and other economies will respond. Although you never know what Donald Trump is planning or thinking and whether or not he listens to his advisers. However, it appears that he is looking to even things out rather than initiate a full scale global trade war (although his efforts could potentially have a similar impact). He has shown a willingness to negotiate with some allies and make some concessions. Whilst I am over-simplifying it, it appears that China is his main target, although Europe and the UK are also in his sights too.

As I mentioned earlier, American farmers and food manufacturers are very focused on any retaliation by the European Union and China. These countries are among the top export destinations for US producers.

The above chart highlights some of the imbalance between the US and the European Union, that Trump is unhappy about.

When the European Union threatened to reciprocate against Trump’s latest tariffs, Donald Trump swung back with threats of additional taxes on European cars, which would likely hurt luxury German and British car makers the most.

Trade wars notwithstanding, countries outside of the US are already talking to each other and looking to lock in trade agreements with each other, in response to the Donald Trump tariff machine.

Like any number of economic events, this one has the potential to have a significant impact on specific countries around the world and yet, it is just too soon to speculate. Let’s bear in mind too, that trade tariffs, economies and trade wars that may develop, are not things that you and I can control.

Anyway, we are much more interested in the quality of our investments and hopefully less concerned about fluctuating prices, driven by big picture global events.

Whilst this may mean the end of a lengthy period of market stability, this could be the beginning of better investing opportunity as markets become uncertain and prices ebb and flow.

“Despite a voluminous and often fervent literature on “income distribution,” the cold fact is that most income is not distributed: it is earned.”

Thomas Sowell