Interest Rates in New Zealand Projected to Remain Flat Longer

Market and Economic Update – Week Ending 24th August 2018

Peter Flannery CFP AFA

“If you have one economist on your team,

it’s likely that you have one more than you’ll need.”

Warren Buffett

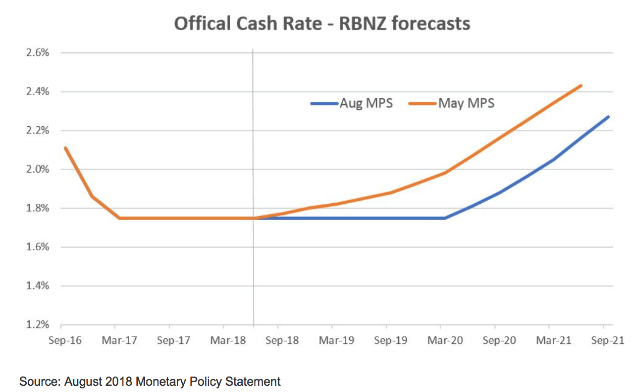

The above chart shows a delayed increase in interest rate hikes here in NZ (the blue line).

Adrian Orr is the new Governor of the Reserve Bank of New Zealand and surprised a number of people when he announced recently that interest rates, whilst they could move either up or down, may well be on hold until 2020 (the previous Reserve Bank Governor suggested mid to late 2019). This means that short term interest rates could possibly reduce slightly.

As for investors, this may mean that much needed interest rate rises, for those who prefer fixed interest type investing, are further out into the future still. Anyway, interest rates in New Zealand remain accommodative while the US has been hiking interest rates and is on track for another two rises this year. New Zealand looks to be behind that cycle and any normalisation of interest rates in New Zealand looks further out into the future still.

That is a good thing because of course, low interest rates help to support economic activity and growth. It is a bad thing though because that economic growth is fragile, hence the support with low interest rates.

Malcolm Turnbull, the Australian Prime Minister, may soon be replaced, as his support has dwindled sharply. He could be gone within 24 hours (or by the time you read this update). Interestingly, since 2007, there has been no prime minister that has been able to serve their full term in office – they do things differently over there in Australia.

Anyway, there appear to be two leadership contenders; both from the conservative right wing of the party, namely Treasurer, Scott Morrison, who is considered to be a social conservative and Home Affairs Minister, Peter Dutton, who is known to be an enthusiastic champion of Australia’s hard line immigration policies. That could be interesting for some kiwis.

Although the economic impact on New Zealand is likely to be minimal, particularly in the long run, it will be interesting to see what changes in immigration policy are made or not made should Peter Dutton secure the top job in parliament in Australia.

Turkey’s problems continue. For the Turkish president to get into an argument with Donald Trump and have to deal with a country the size of America, could prove tricky for the Turkish president. At the same time, Turkey’s economy has been growing strongly to the point where, because of limited controls, the Turkish economy has become overheated and inflation is looking as though it could get out of control. The government estimates inflation to be around 15% in July, although other estimates suggest the real rate is quite a bit higher than that.

The decline in Turkey’s currency highlights a crisis of confidence over Turkey’s economic policies, which appear to have minimal regard for prudent measures required to maintain economic stability. Foreign cash is vital for Turkey’s economy, however with the current lack of confidence, the resolution to Turkey’s currency decline looks to be further out into the future.

In the meantime, I suspect conditions in Turkey will continue to get worse. Even though Qatar, the oil rich state, has promised $15 billion in support of Turkey’s currency, this would only provide a short-term band aid to help stabilise the Lira.

The real problem is Turkey’s less than prudent economic policies. Debt fuelled expansion, along with limited government controls, indeed government support of uncontrolled borrowing has seen confidence lost by the international community and inflation possibly running out of control.

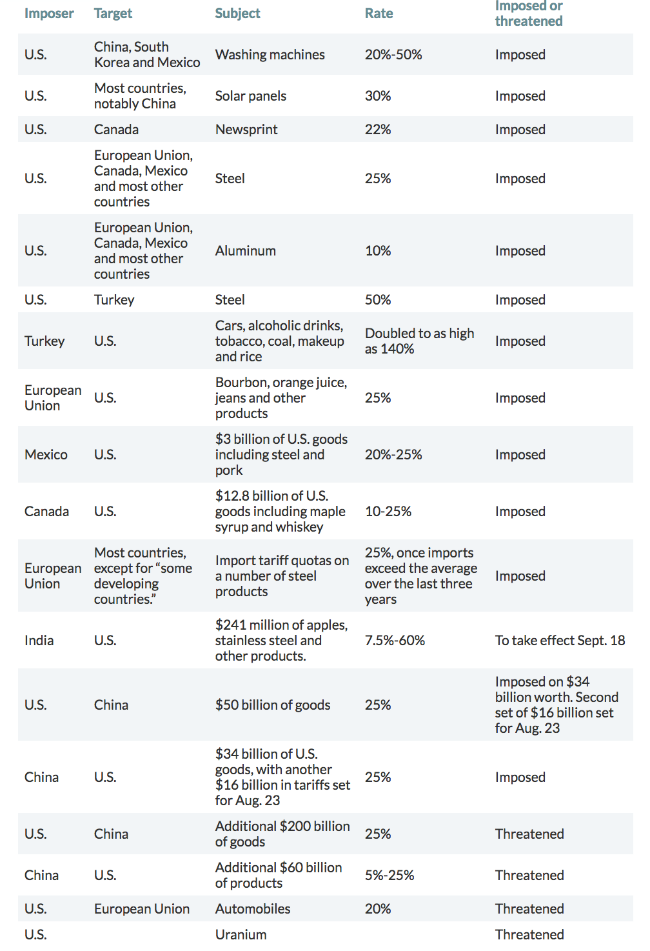

Meanwhile, the US Federal Reserve is talking about the strong possibility of another rate hike in the US in September. Current market odds suggest a 96% probability of the September rate hike and a 60% chance of a December rate hike. Some officials in the US have suggested a pause in the gradual rate rise trajectory might be appropriate if there is an escalation in trade tariffs and trade related disputes. Most agree that a trade war represented a serious downside risk to the US economy.

Speaking of trade tariffs, here is an update:

There are numerous reasons as to why trade tariffs could destabilise economic growth in the US, however the opposite has occurred so far.