First Turkey, Now Argentina…

Market and Economic Update – Week Ending 7th September 2018

Peter Flannery CFP AFA

“If you have one economist on your team,

it’s likely that you have one more than you’ll need.”

Warren Buffett

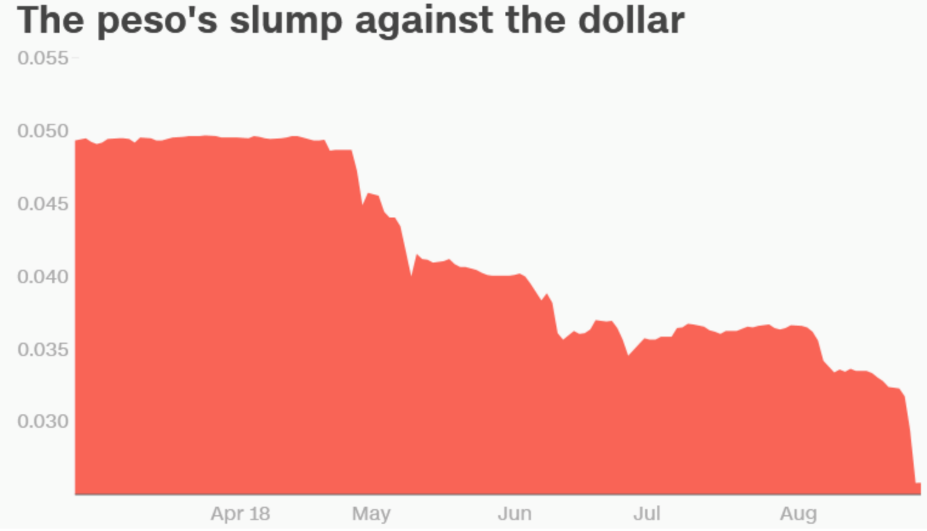

Argentina’s currency continues to freefall.

Argentina’s peso has more than halved in value against the US dollar since the start of 2018. Earlier this year, Argentina asked for some help from the International Monetary Fund (IMF) and recently asked the IMF to speed up the payment of that $50 billion lifeline. Unfortunately for Argentina, the lifeline has failed to stop the ongoing decline in the peso. The heart of this problem is the significant debt owed by Argentina and the fact that most of this debt is in foreign currency. With the peso slumping, the amount owed by Argentina increases considerably and so too does the repayments on all of that debt.

Last week, Argentina’s Central Bank hiked its key interest rate from (this is not a misprint) 45% to 60%, as it attempted to encourage investors to hang on to their pesos. Interest rates in Argentina will likely stay elevated for quite some time. For now, the peso remains in the so-called ‘doldrums.’ Inevitably, this will impact on everyday citizens in Argentina and potentially could become contagious, infecting other markets around the world. Something for us to keep an eye on.

The Turkish lira has also declined significantly since the start of this year. Indeed, the lira is down by around 40% against the US dollar since January this year. Initially, the disagreement between President Recep Tayyip Erdogan, the Turkish president and Donald Trump, set off the decline in the lira (as reported last week). Like Argentina, Turkey’s Central Bank may look to increase interest rates in an attempt to stabilise the Turkish economy.

Turkey, of course, is not a member of the European Union and therefore is less likely to receive a bail out in the same way that Greece did. In some ways, Turkey is therefore standing alone. There could be further trouble ahead for Turkey, as the central bank in Turkey is reluctant to raise interest rates significantly but perhaps more telling is the unwillingness of the Turkish president to back down on his spat with Donald Trump.

Last week, Erdogan called for a boycott of US electronics, suggesting Turkey’s citizens purchase smart phones from local brands or from Samsung instead of Apple. The challenge for Erdogan is that he may need to call for an IMF bailout, however he will be reluctant to do that because that will come with strict austerity measures. Perhaps the real issue behind this is it would mean a significant political loss of face for him.

Some commentators have likened the current situation to the so-called ‘Asian contagion’ in the late 1990s, which you may remember? In my opinion, it is too early to make this comparison, however those emerging markets with significant offshore debt, may face difficulties ahead as the US Federal Reserve continues to hike interest rates.

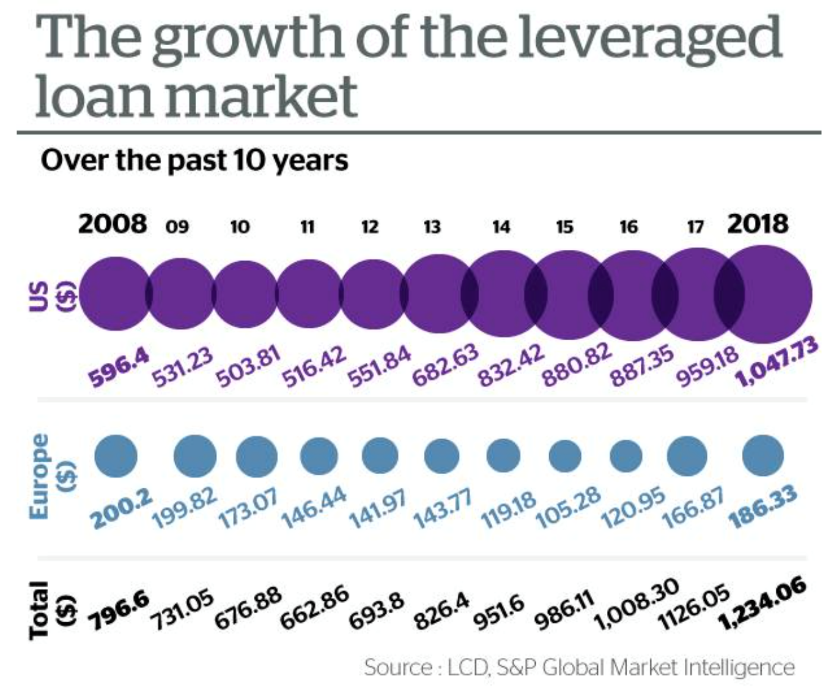

The above chart shows a meaningful increase in the size of leveraged loans outstanding.

The ticking time bomb was the ‘click bait headline’ highlighting the increase in the amount of money outstanding on collateralised loan obligations (CLOs). Basically, CLOs are a type of structured credit instrument, whereby several types of debt are combined into one single vehicle. These can often be commercial loans extended to businesses, the main point being that they are sometimes of low quality and below investment grade. Businesses use these types of loans to support mergers and acquisitions, fund dividend payments, refinance debt, along with other business initiatives.

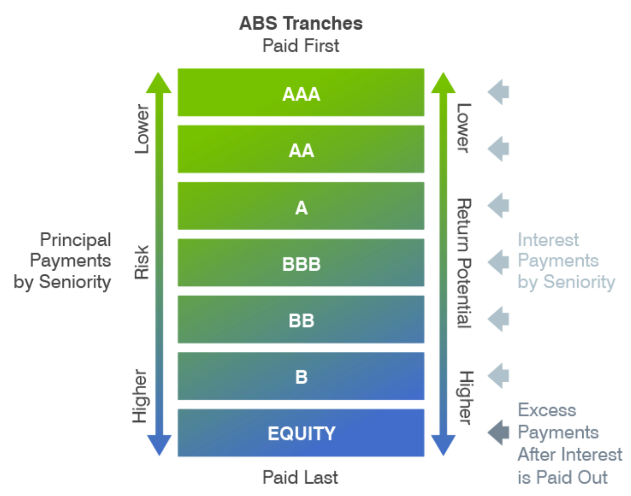

CLOs generally issue asset backed securities, divided into separate ‘tranches.’ Each tranche can represent a specific level of risk and reward potential. Investors can select a tranche that aligns with their goals and their investment risk tolerances. In return, they receive the cashflows from the payments made on the underlying loans. Importantly, each CLO tranche has a separate and different risk/return profile.

Collateralised debt, like other types of fixed interest investment is complex and arguably understood by few – especially mum and dad investors.

CLOs are favoured in the current environment, as they are less impacted by rising interest rates than traditional bonds and other fixed interest type investments. Bonds and other fixed interest type investments lose value as interest rates rise, whereas CLOs are less affected by rising interest rates, which is why they are popular with some investors in the US and elsewhere.

In short, they are a good investment until they are not. They are not when an event occurs in the economy, that causes those organisations and loans of inferior quality to struggle or default. The point here is that the underlying poor quality of many of these CLOs is the potential ticking time bomb. Whether or not we should lose any sleep over it right now is questionable though.

The US economy remains robust, even though Donald Trump, the President of the United States, continues to face opposition, even from within his own support group. The so-called ‘deep state’ surrounding Donald Trump are those who favour the Republic of the United States of America first over President Trump. In short, they are becoming tired of his impulsive, at times childish and stupid behaviour and so, they are colluding behind the scenes to make life difficult for Donald Trump. Interestingly, the president cannot be criminally prosecuted, although apparently that changes when he leaves office. Donald Trump has shown strong resilience and simply does not care who he upsets. In that regard, he appears to have no fear and an apparent disregard for the consequences. The problem is that he is distracted and cannot possibly be functioning effectively as president, which from the outside looking in, appears to be his own doing (ie consequences).

Donald Trump has had the advantage of being somewhat quirky and out of step with mainstream politicians. That has meant that other seasoned politicians have not quite known how to deal with him, however the so-called ‘deep state’ appears to be gaining momentum and strength and so, the word is that, whilst Donald Trump will need to appear as though he is in charge; listen to what he says but focus much more on what he actually does (or does not do).

The US economy continues to grow, as evidenced by weekly jobless claims dropping to a 49-year low. Although wages growth remains somewhat absent, low unemployment signals a generally sound economy. This will also likely mean that the US Federal Reserve is on track to raise interest rates for the third time this year this month. The labour market in the US is viewed as being somewhere near full employment (although we all know that the way this is measured was changed many years ago).

Anyway, the ADP national employment report showed private payrolls increased by 163,000 jobs last month. Employment growth appears to be well above the pace required to absorb new entrants into the labour force. This means that the unemployment rate may remain low and may even continue to decline slowly in the future.

The US economy grew at a rate of 4.2% annualised in the second quarter of this year. That is the fastest rate in nearly four years. Some data around consumer and business spending out of July suggests growth may be ongoing. Interestingly, whilst there is concern around trade tensions, so far this has yet to show up in the data. Indeed, the US economy’s growth was recently underscored by a report last week from the Institute for Supply Management (ISM). It showed manufacturing activity increased 2.8 points to 58.5 last month, which is a good reading. A reading above 50 indicates expansion in the sector. This is important because it accounts for more than two thirds of US economic activity. Whilst tariffs and trade tensions could create some challenges for the US economy, so far, the sentiment around business conditions in the US economy remains reasonably positive.

The new US–Mexican trade deal designed to replace NAFTA basically means that Canada is somewhat out in the cold and China might even be the big loser. The US-Mexican deal means that the US has a new market for US soya beans in Mexico. This means that Donald Trump may have removed the Chinese threat to buy fewer soya beans from the US. Although Donald Trump has what appears to be some serious housekeeping to sort out, this deal nonetheless could give Donald Trump some political mileage, which may help with the upcoming midterm elections. This in turn makes the Chinese deal less urgent. Further, if Canada is somehow brought into the US-Mexican fold, this could make China’s leverage diminish further. In simple terms, it looks as though ‘team Trump’ has somewhat outflanked China with the Mexican deal. This by no means is the end of trade tensions between the US and China but a meaningful victory for team Trump nonetheless. As I have mentioned previously, it seems to me illogical that China can win a trade war against the US because of the very significant trade imbalance that Donald Trump has been targeting all along.

Ironically, recent data out of the commerce department in the US shows the deficit in goods and services (the difference between what the US exports versus what it imports from other countries) increased to $50.1 billion in July from 45.7 billion in June. Ironic because the strong domestic demand, that is helping to support the US economy, is effectively sucking in imports at the same time. This is not exactly the outcome that the White House would be wanting.

Meanwhile, back here in New Zealand, negative business sentiment remains an interesting indicator to keep an eye on, although as I reported last week, business sentiment does not necessarily tie in with business economic activity and expansion.

The New Zealand Central Bank Governor, Adrian Orr, is maintaining interest rates at the current level, he says, possibly until early 2020, “All things equal.” Indeed, there appears to be some pressure for a rate cut in New Zealand, although in my mind, this seems unnecessary right now.

New Zealand new vehicle sales reached a record in August, the highest level ever. New vehicle registrations increased 1% to 13,200 in August, from the same month earlier, edging ahead of the previous record in August 1984 by approximately 43 units, according to the Motor Industry Association. The top selling model for the month of August, by the way, was the Ford Ranger, selling 785 units, followed by the Toyota Hilux at 693 units and the Toyota Corolla with 597 units, (381 of which were rentals though). It appears that rising petrol prices and New Zealand’s declining currency may have increased demand for smaller vehicles.

Residential property prices dropped by 1.6% nationwide in the three months to August. This leaves the national average value at $672,504. Still, values increased nationally over the last 12 months and after adjustment for inflation were up 3.3%. It is a mixed bag though with Auckland properties dropping by 0.4% over the past quarter and after adjustment for inflation by 0.8% over the past year. The average value in Auckland, by the way, is currently $1,048,956 (August). Christchurch values continue to flatline but Wellington’s house prices continue to rise. Dunedin house prices were up 10.7% over the last 12 months and Invercargill was up 13.3% over the last 12 months. It will be interesting to see if spring puts any bounce into property price numbers over the next couple of months.