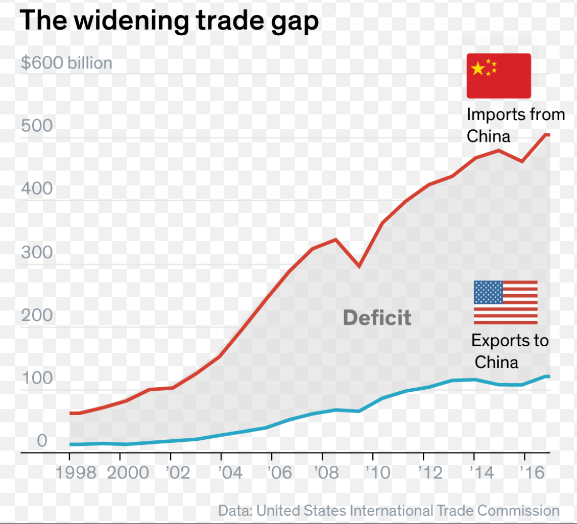

The Widening Trade Gap

Market and Economic Update – Week Ending 21st September 2018

Peter Flannery CFP AFA

“If you have one economist on your team,

it’s likely that you have one more than you’ll need.”

Warren Buffett

The widening gap continues to grow – hence Donald Trump remains unhappy.

Here’s where things stand at present: The US and China have imposed tariffs of $50 billion on each other’s goods. Effective Monday, 24 September 2018, Washington is imposing a 10% tariff on another 200 billion in Chinese imports. Then, if there is no ‘deal’ by the end of 2018, that 10% becomes 25%. Beijing’s response has been with a new 5% to 10% lot of tariffs on 600 billion in US imports, also effective Monday, 24 September 2018.

What is noticeable about these tariffs is that up until now at least, they have been targeting big ticket items that everyday consumers do not necessarily buy. Large businesses buy big chunks of steel, whereas everyday Americans do not, but nonetheless eventually feel the impact of tariffs, as those goods and services made from steel cost more. Mind you, I imagine like everyday Kiwis, everyday Aussies, US citizens are busy navigating their way through each day, paying bills, looking after their kids and attending meetings, so are not directly connected to trade tariffs. That, however, could change once the next round of tariffs includes consumer products, such as barbeques, vacuum cleaners and the like. In short, price increases might be noticeable by consumers in America soon.

Donald Trump is pretty handy with technology and his Twitter account. He has been spreading the message along the lines of …. “when it is wartime, everyone must make sacrifices”. He, of course, is hinting to everyday Americans, that they will also need to make sacrifices (when the cost of goods increase). He will be saying in the future, that everyday Americans are not doing their part to win the trade war if they are not prepared to go along with higher costs to serve the greater good.

In July this year, Donald Trump had a meeting with the European Commission President, Jean Claude Juncker. They jointly announced a goal of moving towards zero tariffs and trade barriers between the US and the EU. Right there, we have a simple answer to the whole thing; zero tariffs and trade barriers between China and the US. I wonder if they might consider that idea!

What about China’s economy? China is working hard to maintain economic stability and has achieved it so far. However what about if America’s so-called ‘trade war’ (now I’m sounding dramatic!) adversely impacts on the Chinese economy and the spin-off is that, as China slows down, it impacts on the economic growth of all of its trading partners, including the US and Europe? Indeed, Europe is one of China’s biggest trading partners. Whilst the Chinese economy performed quite strongly last year, growing 6.9% according to government figures, there are signs of China’s economy is slowing down somewhat, which will not be helped by trade tariffs out of the US. The Chinese Government predicts economic growth will be around 6.5% over 2018 although the trade tariffs out of the US could impact negatively on that level of growth.

I do not believe we are talking about a serious economic recession in China, however those trade tariffs could also spin-off into dampening down confidence throughout the Chinese economy. Whilst the mainstream media continue to target China’s growing debt, I do not believe this is a serious issue for China right now (not saying it may not be at some point). The Chinese Government are well aware of it and I imagine will be looking to take steps before it unhinges the economic growth that the Chinese Government has been vigorously defending for many years.

Why would they ignore something so obvious as debt after making so much effort for so long with a comprehensive array of other initiatives? Anyway, manufacturing and real estate are too big economic drivers of economic growth in China and both continue to perform well at the moment. Whilst debt is an obvious issue and there are other adjustments that the Chinese economy must make, the Chinese economy remains stable and so, an overly pessimistic view on China at this stage seems inappropriate.

Over in Europe, markets were watching the Bank of England and the European Central Bank, as they held their September meetings. The European Central Bank held its interest rate at 0% and looks to be maintaining that rate until possibly mid-2019. The Bank of England basically followed suit and unanimously decided to hold its policy rate at 0.75%. This result was widely expected as almost everyone is mindful of the uncertainty overshadowing interest rate policy that Brexit continues to pose.

Closer to home, what is happening with interest rates? Well, for one thing, the Aussies are raising interest rates whilst here in New Zealand, interest rates and in particular the two year favourite kiwi lock in rate, has been slowly declining.

Note how the floating rate is creeping up, whereas the two year fixed rate is slowly declining.

In simple terms, a key driver of mortgage interest rates is the official cash rate (OCR), which is basically the cash rate which provides the base wholesale rate and expectations of what lies ahead. Then, there is those funding conditions for banks, in terms of how easy or difficult it is for the banks to access funds, in order to lend it out. Banks, where possible, achieve full funding from term deposits, however that is not always the case. That means that banks, even now, are having to look elsewhere and pay market rates for funds, in order to on-lend it. As interest rates rise in the US, for example, this may put some pressure on interest rates globally and could be a factor that may cause interest rates here in New Zealand to rise at some point.

Meanwhile, the New Zealand residential property market is very much an ongoing ‘mixed bag.’ Although residential property remains one of the favoured investments (behind money in the bank actually), there are some uncertainties gathering in terms of prices not always rising all of the time, talk of interest rate rises but actually the opposite has been happening (however that prospect is still unsettling for some) and of course, government regulation, around which the rhetoric has been getting louder and louder.

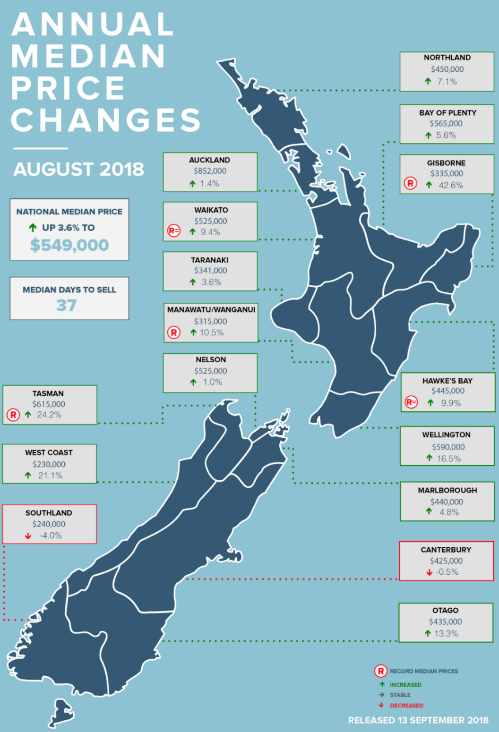

The above chart shows the annual medium price change (increase or decrease) for the 12 months ended August 2018.

Note the national medium price increase is up by 3.6% to $549,000. This Is not a bad outcome but significantly less than many inexperienced property investors might be thinking is normal. Note the difference between Otago up by 13.3% for the period and Southland right next door, down by -4% for the same period. Canterbury, of course, continues to move sideways and is down 0.5% for the year. Gisborne, however, is the standout area, with an increase of 42.6% for the 12 months ended August 2018.

Whilst business sentiment in New Zealand continues to remain negative, as I suggested a couple of weeks ago, actual results do not always reflect academic surveys.

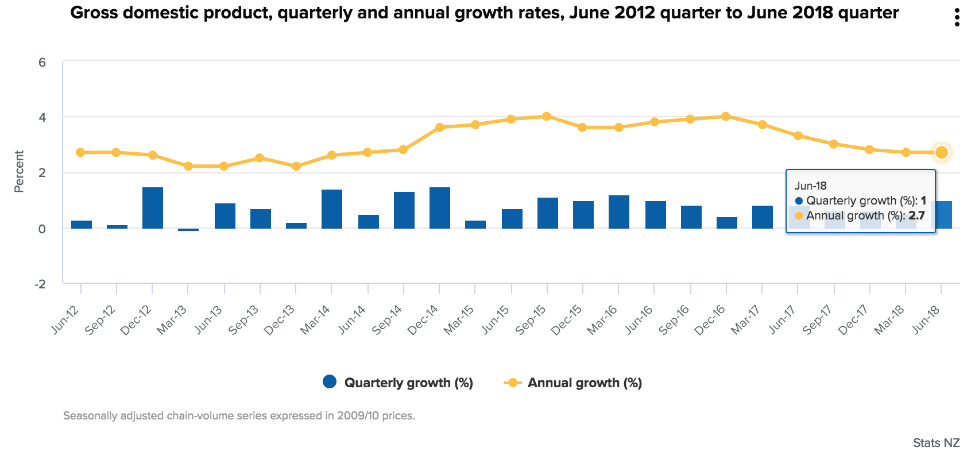

Quarterly growth at 1% is good in most languages, most countries.

Growth in the New Zealand economy was broad-based, which is a good thing, with 15 of 16 industries recording higher production. Mining was the notable exception but more of a reflection of a one-off factor (the unplanned shut down of Marsden Point, stalling gas production). Although service industries have performed well, the largest contributor to growth came out of agriculture, up 4.2%. Also, wholesale, transport, retail trade and accommodation are all performing well, reflecting higher household spending. The ongoing consistent strength of services and the broad-based growth in the economy does not represent a so-called ‘rock star economy’ but is good news and a reasonably solid underpinning of future growth, all things equal.