October’s Volatility and What Warren Buffett Might Say…

Investment Perspective – November 2018

Peter Flannery CFP AFA

“Neither the investing method nor the fundamentals of the business are right or wrong because the mood of the market is favourable or unfavourable toward the “stock”. That is because when you really think about it, “stocks” (shares) are all about the financials and the trading price, the share price…the cash up value. What matters more is the economics of the business”

Peter Flannery

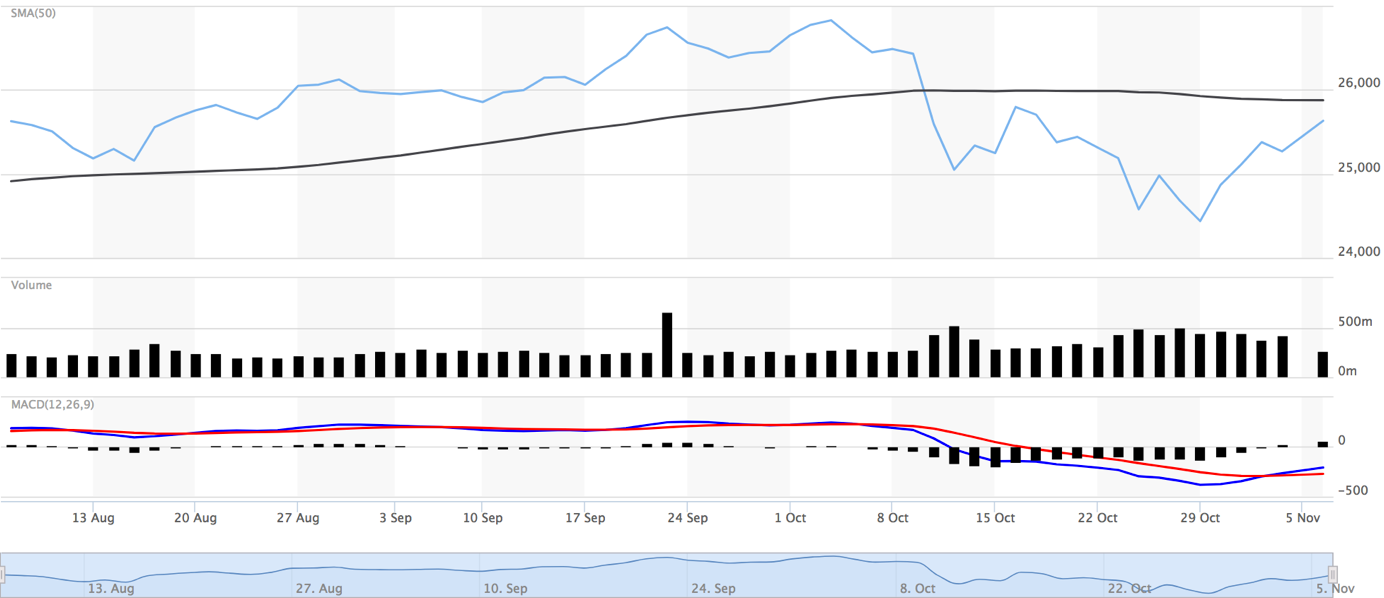

VOLATILITY – ARE WE THERE YET!?

The correction across the Dow Jones index did not come to much.

The volatility over October was stressful for the markets and yet refreshing for us as value investors.

The real question though is, are we there yet? Was that decline in trading prices enough for us?

From a general market perspective, the answer is no. However, from a business perspective (invest in the business rather than play the share market), the answer is less clear. The reality is that most businesses trading across the markets (but not all) are expensive. At least, that is to say, by traditional share market financial analysis measures. This gets us to the point, where we invest is one thing but how we invest is another.

Where and how?

Firstly, the ‘where to invest’ question could be along the lines of choosing between real assets, such as property or productive assets, such as large businesses invested on share markets around the world or even more closely held businesses that are private and unlisted. For example, some of Berkshire Hathaway’s holdings are difficult to track and follow because they are unlisted but then, America is a much larger, deeper and broader market than what we know about here in New Zealand (one reason to like the US market).

Anyway, it might be that the ‘where’ question is about the types of shares or the types of businesses that we might choose. In other words, I may look at sectors (actually, as an investor in productive assets, I do not but those that play the share market do).

Getting to the ‘how’ of it is about understanding what we get when we invest.

The vernacular used by those familiar with value investing is Intrinsic Value. Without getting too carried away, there are a variety of well known share market valuation ratios that are applied. I use them too here at WISEplanning as (a small) part of the methodology to establish intrinsic value. These are methods such as price to earnings growth ratio, price to sales ratio, forward price earnings ratio and the like.

Exploring this in more depth, it becomes clear to us that these are share market and financial analysis measures used when analysing shares.

The point here is that when we start to look at a business, as distinct from a direct share, we are now looking at the economics of the business, as distinct from the financial analysis related to the direct share.

Now, we are moving from ‘where to invest’ to ‘how to invest.’ We are now delving into the economics of the underlying business. Investing in a business is a different process to investing in the share market. That is because we are taking into account the underlying economics of the actual business, which is beyond the fundamental analysis of the direct share or as the Americans say, “The stock.”

What do we mean…the economics of the business?

What is the economics of the business all about anyway?

For a start, it is not about the turnover of the business or the turnover (revenue) compared to its earnings (profit). That is known as the price to earnings ratio and that is an often used measure of value for a stock or a direct share.

We are looking at the intrinsic value of the business and to determine that, we need to understand how well the business performs. That’s because Intrinsic Value is based on the performance of the business. The fact that turnover increased this quarter over the last quarter is not a measure of business performance. It just measures increasing turnover. The market can interpret that to mean the the business is performing better (not necessarily true).

Similarly, the fact that profit or earnings increased this quarter or this year over the previous period does not mean that the business is performing better.

That is because business performance is measured by taking into account how well the business uses its capital. Although overly simplistic, we can use the return on shareholders’ funds and the return on capital to get some idea. The point here is that the earnings or the profit that is achieved should be compared to the assets deployed to achieve those earnings. Whilst that does not give us an intrinsic value, it does start to give us some idea about how well a business performs.

It is about the economics of the business

(along with the financials of the “stock”)

The financials are part of the process and useful. The problem with using the financials alone is that they only tell part of the story. Also, if we are investing using the financials only, the chances are, we may be significantly increasing the risk that we take as investors – make sense?

As for the economics of the business, the competitive advantage has been central to both Warren Buffett and Charlie Munger’s thinking for more than half a century. New technology does not mean that the wisdom of investing in sound businesses no longer works. It may mean though that the way we analyse businesses might need to adjust for fledgling so-called technology businesses (Amazon might be a good example).

That said, it is hard to get into too much trouble when you have a reliable method of investing that works regardless of economic conditions and you stick with that methodology in a very disciplined way.

It may well mean that we give up returns and money we could have made elsewhere, however isn’t the certainty with which we invest and the reliability of our outcome in the future an important consideration too?

We are not there yet, however …

Unfortunately, markets over October did not drop near enough for us as value investors. Prices remain generally expensive.

At the same time, there are some strong businesses with reliable and predictable cash flows that may not be on offer at bargain prices but are worth topping up, averaging down or adding to our portfolios, even though the pricing is not ideal. That is because the quality and strength of those businesses will see us right in the long run. The price we pay for the risk that we take for businesses with strong economics can still be a worthwhile investment with the recent drop in prices. We need to be selective.

Sometimes investing is not as glamorous as taking advantage of bargain prices in the midst of a share market crash. Sometimes it is just the plain, boring, ‘chipping away’ when even small opportunities present themselves that allows us to build in a bit more profit in the long run. In the absence of a massive price correction, why not?

“I do not look to jump over 7ft bars: I look around for 1ft bars that I can step over.”

Warren Buffett