Conflict: Investing for Growth and Income

Investment Perspective – August 2019

Peter Flannery CFP AFA

“Neither the investing method nor the fundamentals of the business are right or wrong because the mood of the market is favourable or unfavourable toward the “stock”. That is because when you really think about it, “stocks” (shares) are all about the financials and the trading price, the share price…the cash up value. What matters more is the economics of the business”

Peter Flannery

Income and growth can work against each other.

If you are accumulating wealth and do not need income off your assets, then the focus of your investment portfolio is likely growth (not income).

If you are financially independent (“retired?”) then income will likely be the focus. After all, if you are financially free you will no longer be relying on generating cashflow through physical exertion (unless “work” is fun and you prefer not to stop).

Why does income and growth work against each other?

So, why is it that receiving income off investments works against the long term growth of those same investments?

If the rents received from a property are paid out as income then the only way they can grow is through capital appreciation and by borrowing money to add other properties that generate more cashflow (although that debt will need serviced by the new rents).

If you are looking for cashflow every month then the rents coming in on those properties will need to be used for consumption and will not be able to be allocated towards servicing debt on additional properties or stacked up in a bank account.

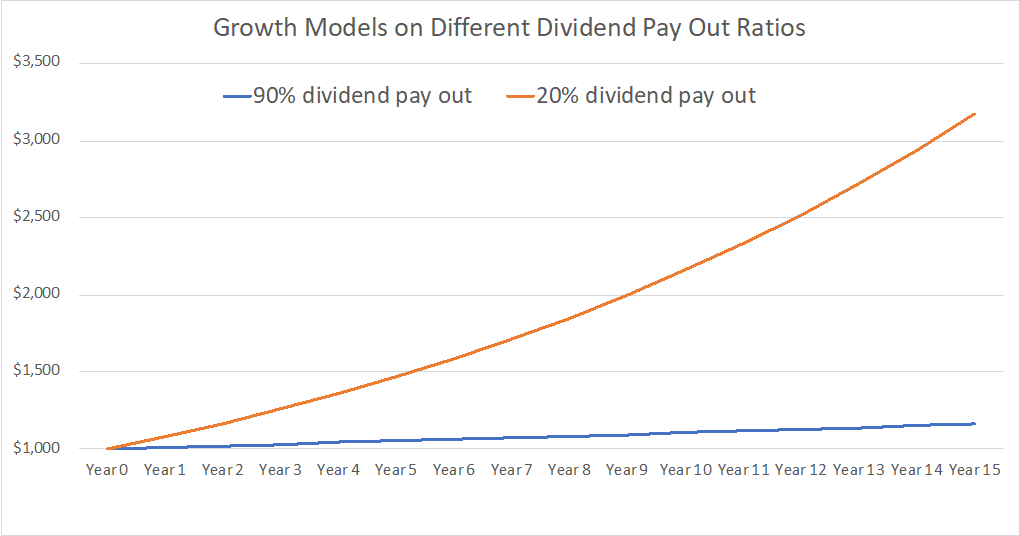

Looking at businesses listed on the market, if we take the example of a business achieving a 10% return on its capital, let’s say it pays out 90% of its profit. This means that the dividend to pay-out ratio would be 90% in this case. The remaining 10% is likely not enough to be set aside for growth.

It is not difficult to do the numbers. If you compound your investment in that type of business over 15 years, the money you will make as an investor is very different to one where the dividend pay-out ratio ratio is lower. Obviously, the retained profits will either stack up inside the business increasing the intrinsic value or better still, will be redeployed to grow the business, increasing that intrinsic value at a faster pace.

The above graph shows the difference between investing in a business with a high dividend payout ratio (the blue line) and another with a low dividend payout ratio (the brown line).

Actually, income and growth can work well together.

So, on the one hand using all of a businesses cashflow or all of the rents from a property as consumption might be necessary in order to fund income requirements. The long term outcome is a very different one compared to other business with a growth mandate ( and a low dividend payout ratio).

For those looking for cashflow ( income to spend), the ideal approach is often to combine income generating investments with growth investments together in a portfolio mix. That way you get the best of both worlds.

You get income to fund living needs, but at the same time, build in some growth to off-set those draw downs and protect your capital against the rising cost of goods and services.

Money to spend every month AND … the security of part of the portfolio growing to be there later and / or provide additional lump sum withdrawals when needed – without affecting the regular monthly income of the portfolio …even when markets do not play nice.

“If past history is all that is needed to be successful with money, the richest people would all be librarians”

Warren Buffett