“Small Caps” Deliver Better Returns

Investment Perspective – May 2019

Peter Flannery CFP AFA

“Neither the investing method nor the fundamentals of the business are right or wrong because the mood of the market is favourable or unfavourable toward the “stock”. That is because when you really think about it, “stocks” (shares) are all about the financials and the trading price, the share price…the cash up value. What matters more is the economics of the business”

Peter Flannery

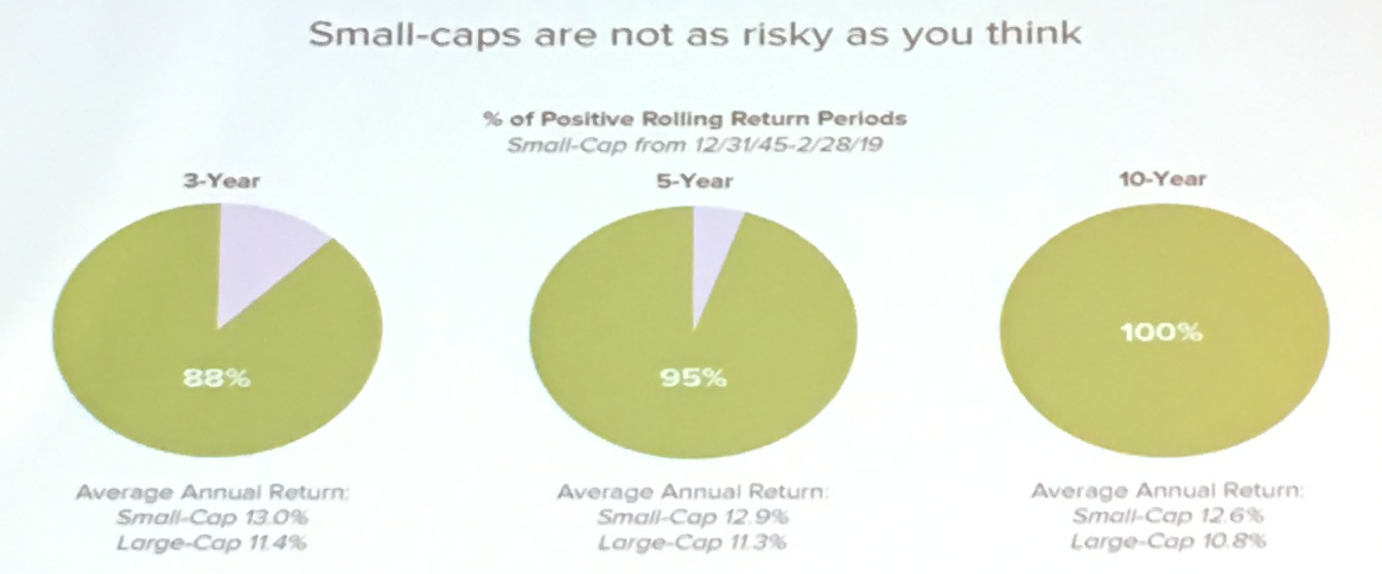

The above chart shows the growth on small caps and compares it with the growth on large caps from December 1945 through February 2019. The chart also looks at the percentage of positive returns over three years, five years and 10 years.

It is clear, if you want to improve the return on your investment portfolio (ROI), adding in some “small caps” (businesses with a market capitalisation of US$2 billion or less), is a simple way to achieve to achieve this.

Hang on, what is a small cap and a large cap?

Sorry for the jargon. Small caps refer to small businesses (generally US$2 billion or less).

Mid-caps refer to those businesses between US$2 billion and US$10 billion in size.

Large caps are those businesses $10 billion or more by market capitalisation.

Market capitalisation just means the number of shares that a particular company has issued, times its share price. For example

Apple (APPL): Total shares outstanding 4.60 billion shares X current share price US$197.18 = Market Cap US$907.03 billion (nearly back to US$1 trillion).

Starbucks (SBUX): Total shares outstanding 1.21 billion shares X current share price US$78.42 = Market Cap US$94.89 billion (much smaller than APPL but still a large cap).

Why do small caps perform better than large caps generally?

The simple answer is that smaller businesses can grow faster than larger businesses because smaller businesses have significantly greater room for growth.

Larger businesses, on the other hand, sometimes get to the point where they “top out”, if you like, and saturate their market or are having to deal with competitors, thereby struggling to grow at the same pace as when they were small and in expansion mode with limited competition.

Large businesses can still be good investments and can be more suitable for investors that deem large businesses to be safer.

What’s the catch though?

So, small businesses can be higher risk and indeed are generally more risky than more well established, larger businesses, that have scale. They can see their turnover, profit and trading price be much more volatile when compared to large caps.

For the sake of exaggerated comparison, think about a large business, that has perhaps been around for more than 50 years, that has no debt, “sticky” (loyal) customers, strong branding, along with solid management, and is in control of its niche. That is a quality business.

Again, for the sake of exaggerated comparison, think about a small business, that has possibly been around for less than five years, has a reasonable level of debt, although is not actually profitable but growing fast. They may not have properly established processes or a culture that allows the people in the business to genuinely focus on looking after their customers.

The challenge for smaller businesses is that they do not necessarily have the management depth, scale and resources to cope when economic conditions suddenly change or a competitor comes along, making life difficult. At the extreme end of it, those small caps can sometimes default. The chances of default, for a large cap, is minimal (although still possible), whereas for a small cap, it is more possible, particularly if the financials and the economics of the business are not sound.

Therefore, at the risk of stating the obvious, when investing, whether it be large, mid or small cap, what works is to have a sound, underlying methodology for selecting those good businesses and deselecting those lower quality businesses. That way, the risk of default is minimal regardless of size. The opportunity for real growth and improved return on investment (ROI) is enhanced.

A little bit is a lot

Most people, unless they work in business or in finance, do not spend much time crunching numbers and in some ways, have less exposure to the importance of how only small adjustments to their investments can make a significant difference to the amount of money (real dollars in the hand) that they make over time.

The image at the start of this Investment Perspective shows a difference of approximately 2% between large caps and small caps. We can make that gap bigger, of course, by adjusting our selection model. Remember, that chart only looks at the broad index. There is no selecting within the index which can improve returns yet further.

Here is what a better ROI looks like. Let’s say the portfolio size is $500,000. 2% (additional return) on $500,000 is $10,000. Multiply that by 10 years and there we have $100,000. An additional 2.00% per annum = an additional $100,000 over 10 years. Do you see what I mean?

Human behaviour is not a mathematical equation to be solved.

Francesco Parames (The Warren Buffett of Spain).

Francesco Parames and Peter Flannery – Omaha conference May 2019