Reducing Interest Rates, Good or Bad?

Market and Economic Update – Fortnight Ended 12th July 2019

Peter Flannery CFP AFA

“If you have one economist on your team,

it’s likely that you have one more than you’ll need.”

Warren Buffett

The Markets

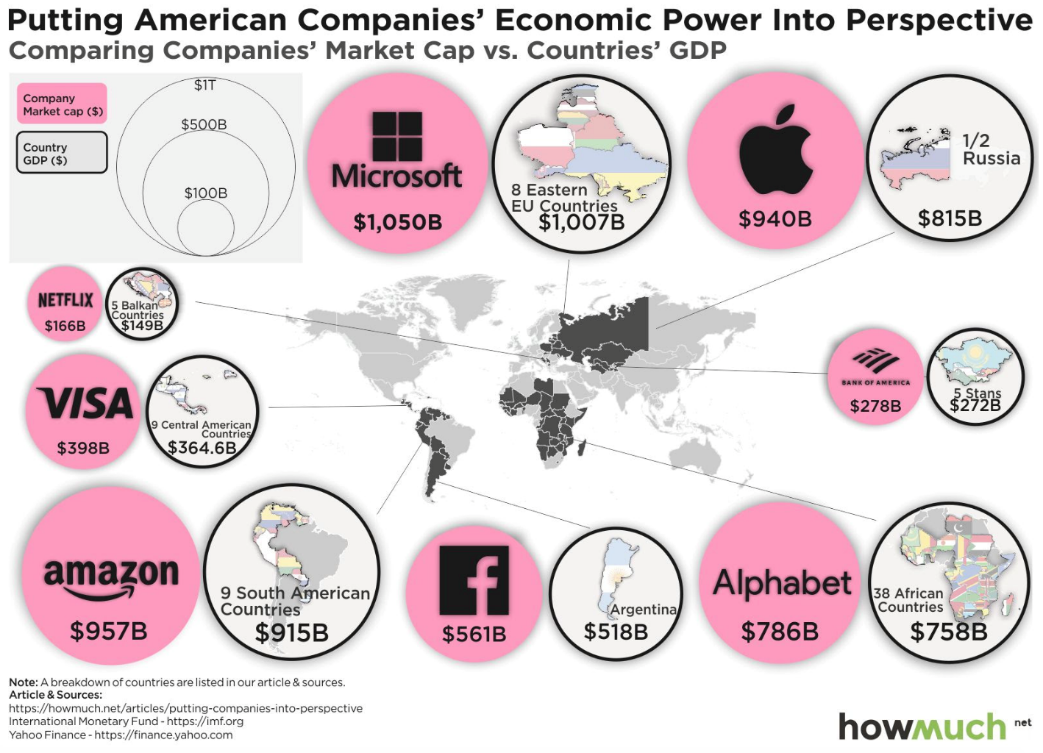

This chart shows how some of America’s largest businesses compare to whole countries.

America has not only some of the largest but best performing businesses in the world. Sure, other countries have large, strong businesses too. This chart though, I believe, highlights that economic powerhouse, the machine that whilst, it may stumble from time to time, remains innovative and progressive. Wealth across America is not evenly spread. This is not just an American problem though. The living standards of the everyday American are among the best in the world and as you can see, some of the businesses that have sprung from that American economy, are partly responsible. They supply the goods and services that make our lives better that we sometimes take for granted. Imagine, for example, a life without being able to search effectively on the internet (Alphabet).

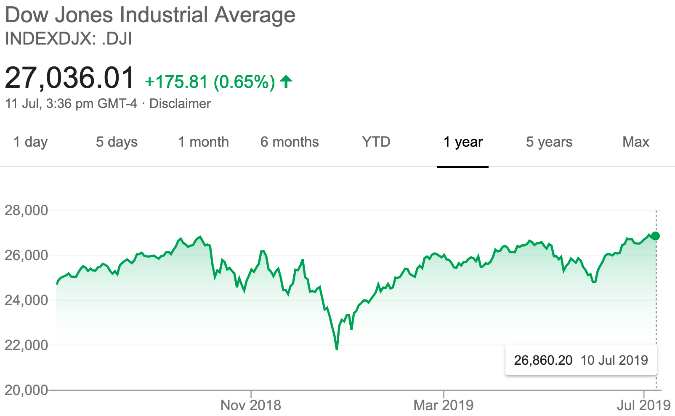

The left hand chart shows the increase in the Dow Jones over the last month. The right hand chart shows the increase in the Dow Jones over the last 12 months.

The charts are all green as markets continue to rise – happy days roll on. As you may know, this has been driven, to some extent, by signals of interest rate declines, not only in the US but also in New Zealand and Australia too. So, if I did not know anything, I would think that rising share markets mean good times ahead. Share markets are often considered a leading indicator about what is possibly happening in the future.

As a value investor, you and I are less inclined to go along with these types of indicators because they are market driven and markets can sometimes over emphasise the good times and the bad times as well. Many analysts look to models that have been used over many decades, in an attempt to read into the markets and where we are heading. In my view, because of central bank intervention over the last 12 years or so, some of those models just do not work anymore.

Therefore, following them can be unreliable to say the least. Anyway, we have had one of the longest runs of positive economic activity in America, ever. This is usually a signal that it is about to come to an end. As I have alluded to before, one of the most talked about charts around the world is the one showing long term interest rates declining below short term interest rates. In the past, this has been a reasonably reliable indicator of upcoming recession but not this time. That said, anything is possible; however, in my view, whilst that chart is worth knowing about and being aware of, because of central bank intervention, which is ongoing (let’s face it, they have got no choice), those types of indicators that have been used over many market cycles and several decades may not as accurate as they once were.

So, what is the solution? That is simple. Let’s invest in quality businesses, so that in good times and in bad, we will be okay. In good times, the cash up value of our portfolio will rise and we might even feel good about that. When things get volatile and the market starts running scared, we will largely still be okay, although small caps tend to be more vulnerable when markets become very uncertain and volatile (especially when banks restrict lending).

You may choose to feel unhappy in this situation, as the cash up value of your portfolio declines. I suggest you do not waste one breath or one second of your life feeling unhappy when asset prices all around you are getting cheaper! We all know that market linked investments, like direct shares, do not rise in a straight line. Indeed, they do rise over time but in a random way.

Economic Update

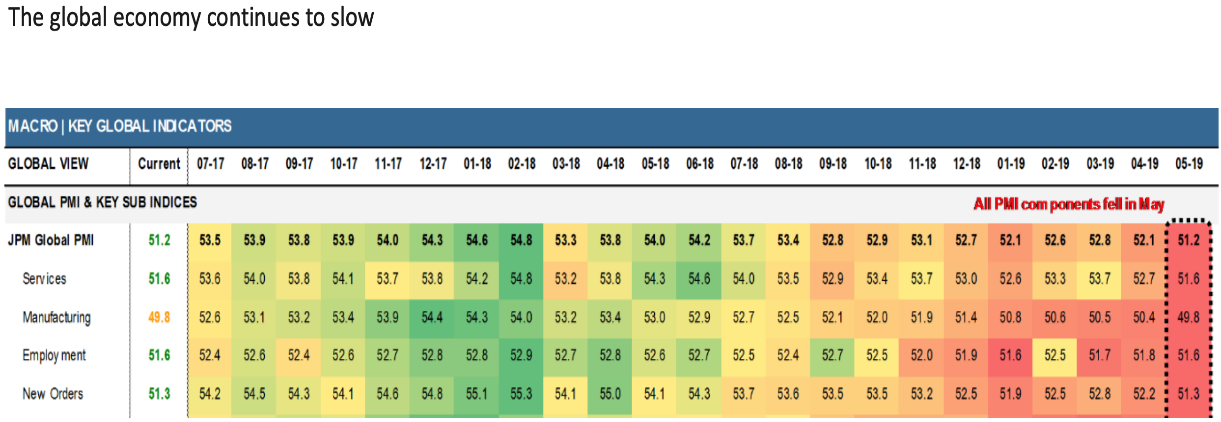

The above chart shows the global economy continuing to slow.

The global economy continues to slow. This is old news and may be sounding a bit repetitive. The global economy just does not follow any particular time line. It is difficult to predict just how slow the global economy will grow in due course; however, we now have what is being termed “Modern Monetary Theory”. Should the global economic slowdown develop real momentum, leading towards a deflationary contraction in global activity, central banks will act. Of course, there are no guarantees about that.

Although conspiracy theorists have other ideas (who knows, they may be right for all we know?!), there is really no organisation that is in control of the global economy and its direction. That said, the people within those economies are generally hardwired for progress, improvement and betterment. It is just that sometimes things get out of hand. The American economy is arguably one of the most powerful economies in the world but it too is prone to what some might call stupidity.

So, are we heading into economic Armageddon? I do not believe so – not anytime soon. As I have mentioned to many of you during our meetings, I am looking for that black swan (the signal that tells us the world is in for a serious depression) and it could well be there; however, I just do not see it.

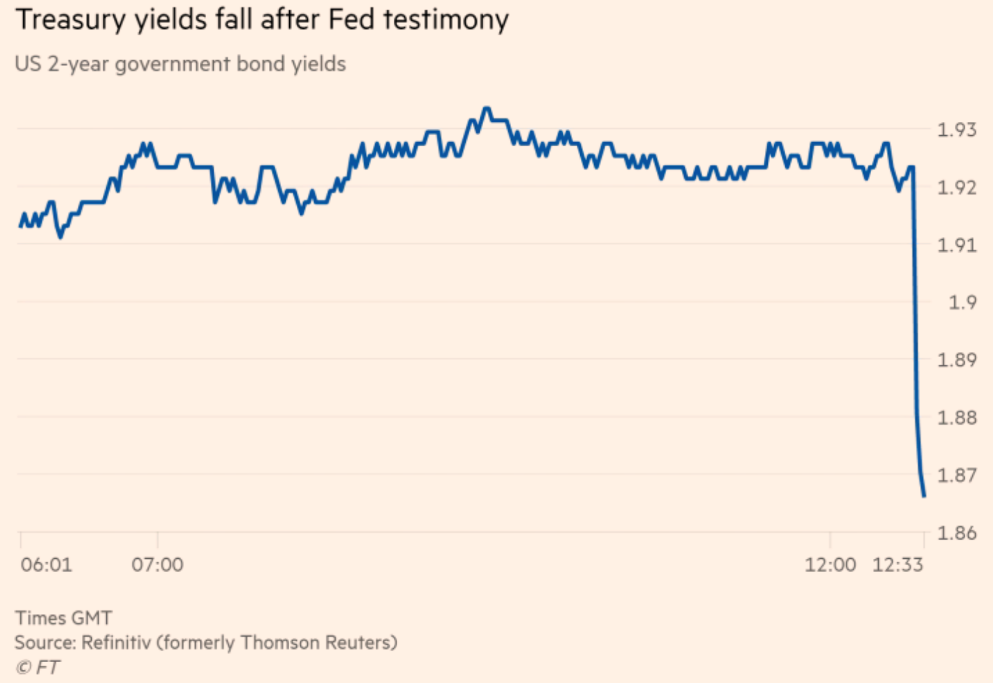

The above chart shows the sharp decline in treasury yields after the Fed governor mentioned the possibility of a rate cut in the US.

Jerome Powell, the US Federal Reserve Governor in the US signalled a softening stance around interest rates at its June meeting. More recently, he has initiated discussion around the real possibility that a rate cut at some point might be possible; however, he has been non-committal about when a rate cut might take place or the extent of any rate cut.

Although Washington and Beijing have recently been making conciliatory tones around their trade dispute, nothing is certain and I imagine Jerome Powell is thinking that the ongoing trade dispute is far from over. That, of course, is a risk for the global economy and therefore to US economic growth in the future; however, Mr Powell’s baseline outlook, he says, is still based on US economic growth being solid, given strong labour markets and his expectation that inflation in the US will move up over time to its 2% target.

The Fed governor continues to stress that wage gains are still tame and there are a few signs of an overheating job market in the US. In his words, “To call something hot, you need to see heat.” Of course, one of the risks for the Fed, if it cuts rates now, is that this leaves less “wriggle room” in the future to stimulate the economy, should any upcoming recession come with a strong bite. That said, the Fed governor says he does not expect a severe downturn in the US economy and insists that the tools that he has at his disposal will be adequate to tackle any future crisis. So there you have it.

Government bonds in Europe are yielding less than zero.

Even Germany, the Netherlands and Denmark are showing 10 year bond yields are in negative territory. The concern for central bankers in Europe is that negative interest rates mean this is one less tool that they have at their disposal to help stabilise the economy. Although they do have other macro prudential tools at their disposal, it is also a concern because, very low inflation can turn into deflation, which history shows is difficult to resolve. Japan is the most obvious example. It has now been over 25 years and Japan remains unable to shake off the strong grip of deflationary funk.

So, why can’t the world economies shake off this deflationary funk? I am not sure. Who knows what the real answer is; however, it would appear that some Asian countries, such as China, Japan many years ago, and other emerging economies have reduced the cost of manufacturing, as has technology. What this means is that lower costs of manufacturing have created a form of deflation, which has been exported by these emerging economies around the world to developed economies.

For example, the motor vehicle manufacturing industry in many countries around the world struggled against Japan’s highly automated motor vehicle industry of 20 years ago. This is interesting because I am not sure how manufacturing could return to the likes of America, where the average hourly wage rate for everyday Americans is significantly greater than that of the everyday citizens of emerging economies, including China. Is that one reason?

Has the global economies addiction to debt become unshakeable?

What about interest rates? Has the global economy, businesses across the world and mums and dads around the world, become so conditioned to low interest rates that there would be significant economic disruption if interest rates were to rise, not to mention rise too quickly?

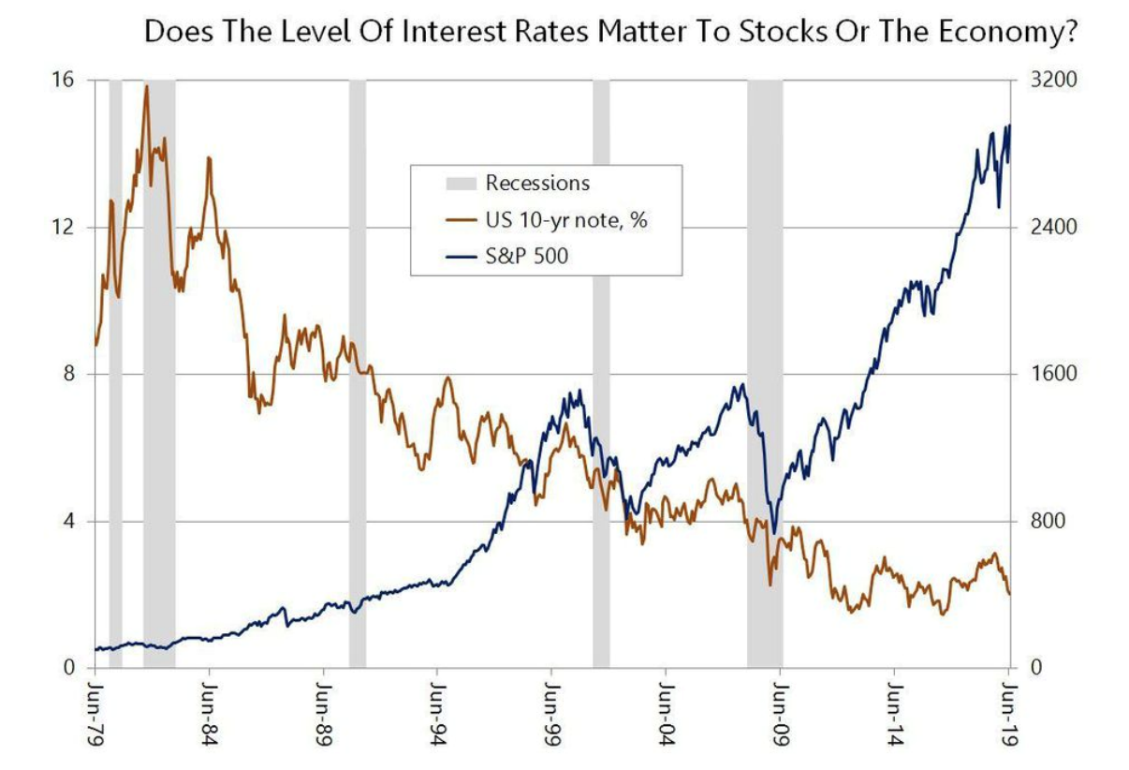

The above chart shows recessions (the grey bars), the American share market as measured by the Standard & Poor’s 500 (the dark blue line against the right side vertical axis) and US 10 year treasury note yields (the brown line against the left hand vertical axis).

Although some disagree, I believe that interest rates and asset prices are related. The above chart shows how 10 year US treasury note yields have declined since 1979 and how the US share market has climbed over the same period. Does this mean that the American share market will come crashing down the moment interest rates rise? Markets will likely adjust share prices down in the short term but, longer term, quality businesses continue to grow – regardless of their short term popularity. Quality businesses continue to grow long term, even though interest rates may have some impact in the short term.

Europe

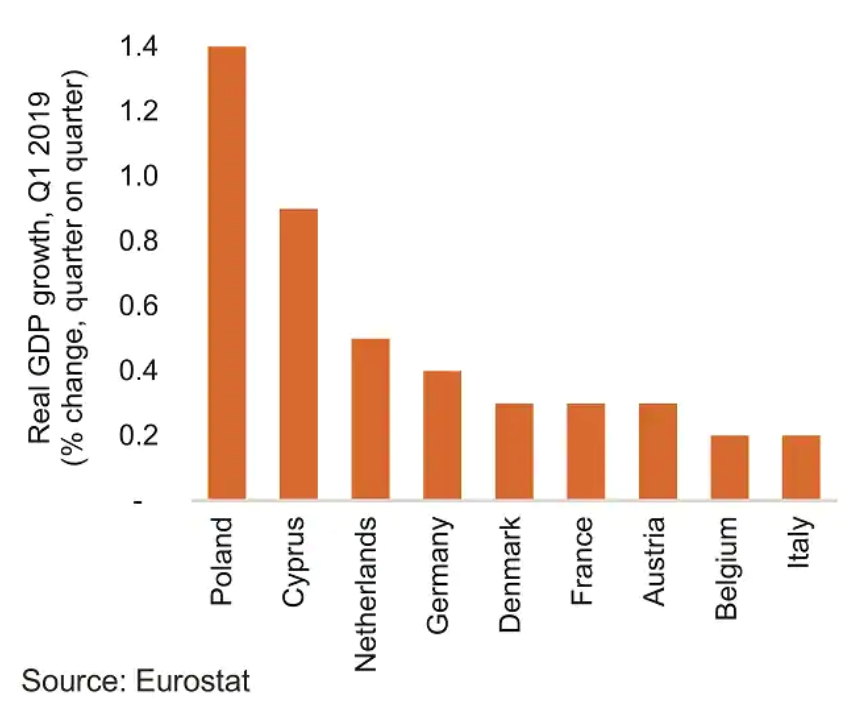

Eurozone: after a rocky 2018, the European economy is stabilising and possibly returning to growth.

The above chart shows the growth in some economies over the first quarter of 2018.

The European economy grew by 0.4% in the first quarter of 2019. Germany is an important component of the European economic engine and appears to have stabilised after deteriorating economic performance in the second half of 2018. Other more peripheral economies, such as Ireland, Portugal and Spain, continue to grow at rates that are faster than the regional average. The real challenge now facing the European economy is dwindling inflation expectations. I imagine the central bank in Europe will initiate more stimulus unless there is an uptick in inflation across the Eurozone. We will know more by around September this year, as a new set of data is released. The other risk, unsurprisingly, is the possibility of US tariffs being imposed on European goods. Although not the end of the world for Europe, nonetheless, any tariffs that are imposed would impact on those specific sectors of the European economy – a headwind, to be clear.

Australia

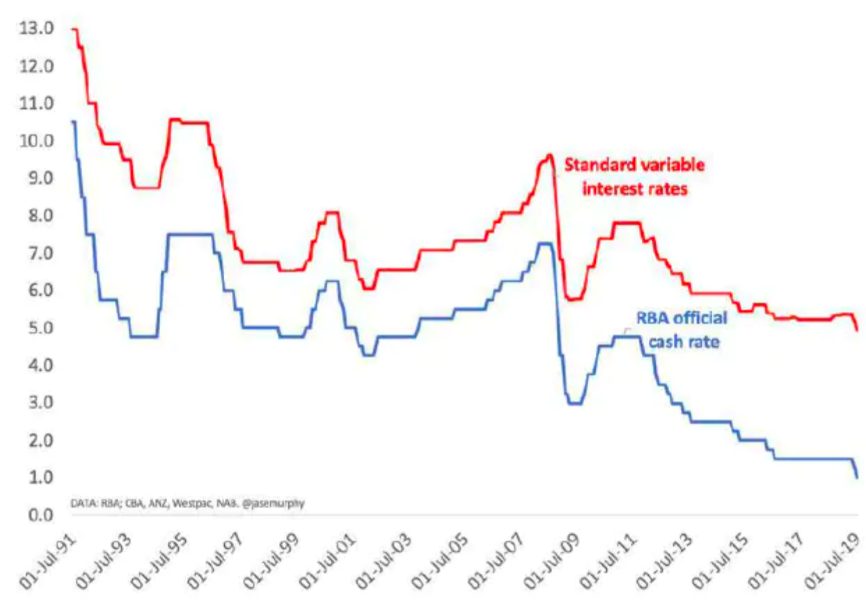

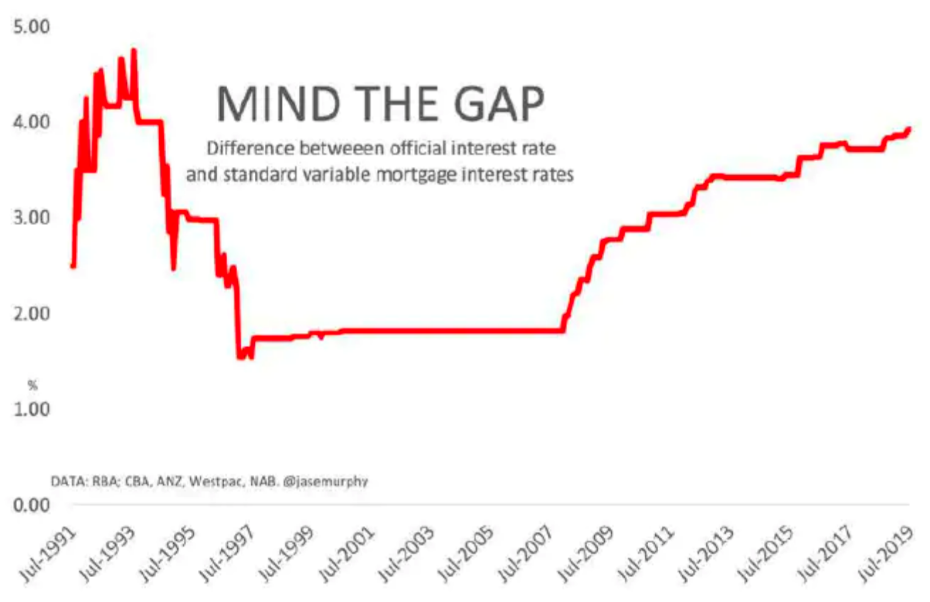

Interest rates in Australia continue to decline

The above chart compares both the Reserve Bank of Australia’s official cash rate and standard variable interest rates available across the market.

What is interesting about the above chart is the gap that exists now between variable rates and the official cash rate. This gap is now at its highest level since around 1993.

The gap between standard variable rates and the reserve bank cash rate continues to widen

The above chart measures the gap between the official interest rate, as set by the Reserve Bank of Australia, and standard variable mortgage interest rates.

So, as you can see, that gap continues to increase. Why is that? Is it because banks are just being greedy? Banks do have specific targets around profitability and until recently have enjoyed good times for at least the last two decades. They are now less profitable though and the reality is, they still need to attract savers, to be able to lend out money. With interest rates declining, this is becoming more and more difficult.

Banks still attract a large amount of funding from depositors. Many of whom are too afraid to invest elsewhere and so, in my view, the banks will always have a strong following. We are noticing though, here in New Zealand (it will be the same in Australia), there is a section of their usually loyal depositing community, that is becoming frustrated with low returns and now are starting to look for other options beyond term deposits.

The reality is that if interest rates continue to decline, it is conceivable that the amount of income that can be achieved from a bank account will move closer and closer to zero.

This is the case in a number of countries around the world. The short of it is that interest rates are continuing to decline in Australia. Whilst interest rates remain high compared to many other economies around the world and there is a fair way to go yet before they reach zero, this nonetheless appears to be the direction that interest rates in Australia are heading.

New Zealand

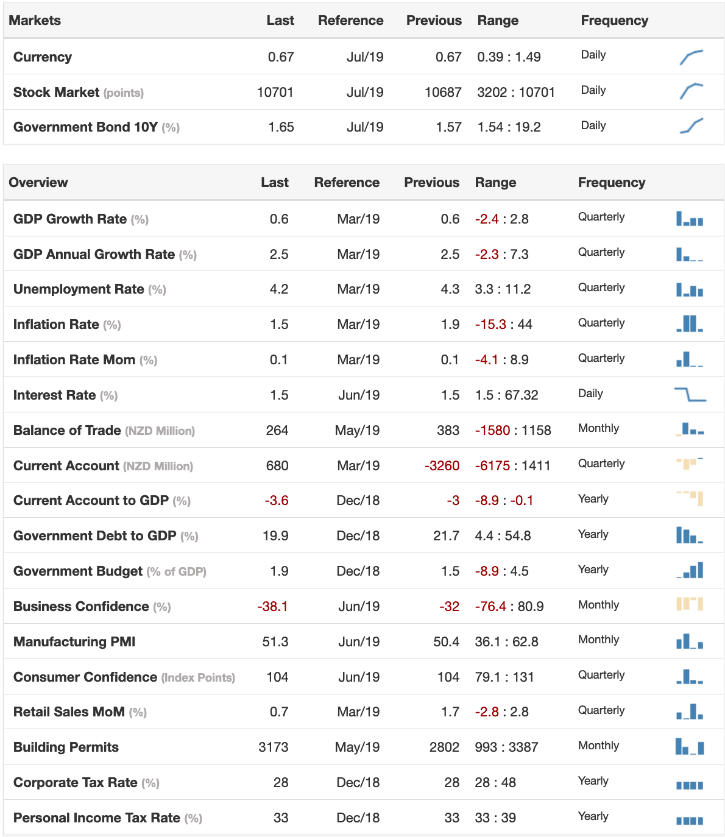

This chart provides a useful overview of New Zealand economic data.

It appears that even New Zealand may be getting caught up in global deflationary funk. A number of my clients, when asked how much detail they want around the global economy tell me, basically, to skip it. They feel that we are insulated here in New Zealand and that global economics do not really matter. What do you think?

The consensus is that the New Zealand economy is doing okay and that nothing is broken. Whilst a bit simplistic, I agree this is somewhat correct; however, that overlooks the fact that New Zealand is indeed part of the global economy and that our economy is very narrow, relying on agriculture, tourism and interestingly, logging (a fickle commodity). I mention logging because by some measures, it is the third largest income earner (or has been of late). That, of course, was at a time when logging prices were favourable and that may change.

Anyway, it highlights the point that New Zealand’s economy may well ‘punch above its weight’, so to speak, but remains vulnerable to significant global economic shocks. Reducing interest rates and the New Zealand Reserve Bank reviewing the strength of bank balance sheets are a couple of examples that are directly related to the global economy.

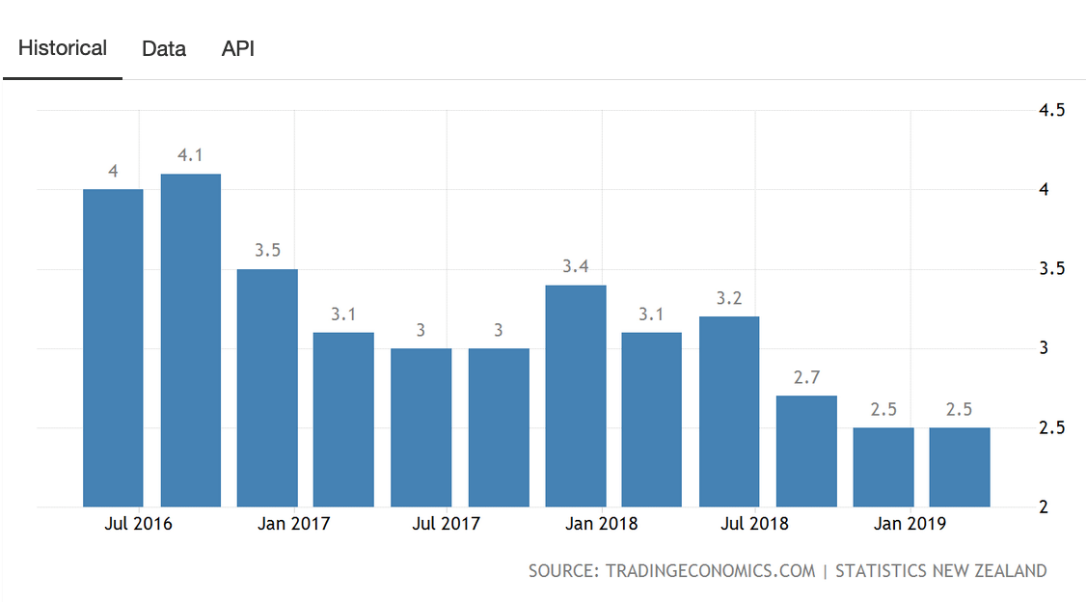

New Zealand economic growth, as measured by gross domestic product (GDP)

The above chart measures economic growth in New Zealand.

As the chart above shows, economic growth in New Zealand has been slowing and I suspect if global economic growth continues to slow, then it would be increasingly difficult for New Zealand to grow at a faster pace. Our economic growth is okay, but it is worth remembering that the Governor of the Reserve Bank in New Zealand has been making noises about supporting the New Zealand economy with lower interest rates. That is because it is vulnerable to a slowing global economy and other global events such as, for example, trade disputes.

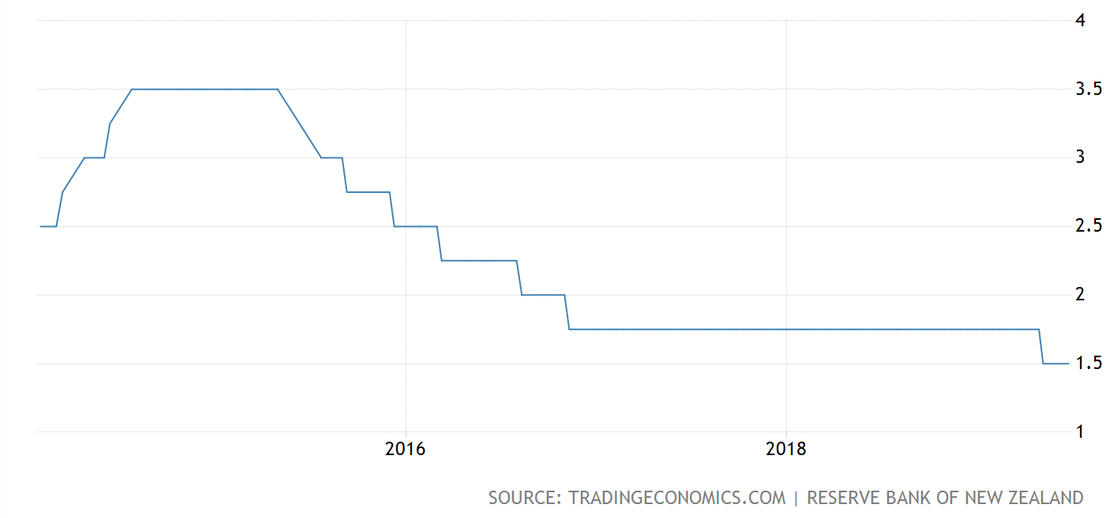

New Zealand’s official cash rate

This chart tracks the official cash rate as set by the Reserve Bank of New Zealand.

The official cash rate in New Zealand remained unchanged from the Reserve Bank of New Zealand’s June 2019 meeting, which was widely expected. The point here is that at 1.5%, this is a record low – the lowest interest rates in New Zealand ever.

What is more interesting is that many countries around the world also have their interest rates set at all time lows. Some of those rates are lower than New Zealand’s. Some are negative. The market likes the idea of reducing interest rates. You can see this when share markets suddenly rise on the back of any signals that interest rates might decline.

Homeowners and property investors also like lower interest rates because their ability to invest is significantly determined by their ability to service debt. Low interest rates mean better serviceability. That said, the banks are placing much greater scrutiny on homeowners and investors when they look to borrow money for their own home to live in or a property to invest in.

The reality is, in general terms, that property and share markets are tied into economic activity. In the short term, the market determines the price and therefore the market does not usually focus on the broader implications of slowing economic growth. Indeed, as I have mentioned, the everyday property owner does not rate global economic data worth even thinking about, not to mention taking into account as they make decisions over their investments in property.

I suspect they are investing in the past and those ideal economic conditions that made residential property in New Zealand and other countries an easy option. Of course, we invest in the future.